Sustainable investing – concepts, considerations and conversations

‘Sustainable’ or ‘Responsible’ investing is now very much part of the mainstream investment landscape.

Introduction

Once considered a niche investment category – or even an indulgence – ‘Sustainable’ or ‘Responsible’ investing is now very much part of the mainstream investment landscape, with more than 60% of funds under management in Australia and New Zealand and half of FUM in Europe and Canada[1] being managed in accordance with Sustainable Investing (SI) principles. In 2018 it was estimated[2] that more than $30 trillion USD was managed in this way around the world, representing growth of 34% over the previous 2 years.

Sometimes confused with the more narrowly defined ethical investing (‘investing with a conscience’), SI is a more comprehensive approach to investing which ultimately views environmental, social and governance (ESG) considerations through a financial lens, quantifying risks and costs and taking a longer-term view.

The rapid growth of SI has been driven by many factors, including the massive wealth transfer taking place between boomers and the more socially aware millennials, the increasing public desire to mitigate the global ‘climate crisis’, and more regulator mandated transparency in areas as diverse as nutrition, financial reporting, and manufacturing practices.

And, despite widespread perceptions that sustainable/responsible investing comes at the cost of lower returns, there is a growing body of conclusive quantitative evidence that investments managed under SI principles actually outperform non-SI investments over most time frames and asset classes[3]. Put simply, Sustainable Investing can genuinely drive better investment outcomes.

Many of these drivers will only become more powerful over time, which is why it is imperative that financial advisers properly understand ESG principles and offerings, consider how to evolve their own business and advice processes accordingly, and equip themselves for increasingly frequent client conversations on this topic.

The genesis of Sustainable Investing

The possession of a social consequence is not a new phenomenon, and history is full of examples of highly impressive and forward-thinking philanthropists. In terms of organisations actually codifying an investment philosophy based on social concerns, one of the earliest recognised examples is the 18th century church, when Quakers refused to invest in anything involved with the slave trade then prevalent in many colonised countries. In the second half of the twentieth century, as the legislation of equality in human rights became (belatedly) more widespread, we saw the beginnings of SI on an international scale in the 1970s with the boycotting of investments in South Africa, in response to the racial inequality of the apartheid regime.

By the late eighties, the concept of sustainability in resources and development was gaining more traction, and in 1987 the United Nations World Commission on Environment and Development – known as the Brundtland Commission – released its landmark report ‘Our Common Future’.

With a mandate to examine ways to strengthen international cooperation on environment and development, the Commission sought to “raise the level of understanding and commitment to action on the part of individuals, voluntary organizations, businesses, institutes, and governments”[4].

Focussing its attention in the areas such as population, food security, the loss of species and genetic resources, energy and industry, it was this report that coined the term ‘sustainable development’, which it defined as “development that meets the needs of the present without compromising the ability of future generations to meet their own needs”[5].

With the report putting a responsibility for sustainability on the shoulders of individuals and businesses – not just governments – many corporations started to evolve their practices, and in the 1990s entrepreneur John Elkington[6] was the first to articulate the concept of the ‘triple bottom line’; people, planet and profit. In this framework businesses assessed their performance in each of these areas, recognising a focus on all three was vital to their own sustainability as a business.

Over the last two decades, the triple bottom line concept has given rise to a plethora of responsible business models, frameworks, and operational methodologies, including ESG, an approach which arguably forms the bedrock of most Sustainable Investment processes.

Different approaches to SI

Demand for sustainably managed investment offerings is growing strongly (in Australia SI managed assets grew 13% in 2018[7]) and reflects a diverse range of motives held by investors.

An individual investor may want to follow their personal beliefs in not wanting to invest in contentious things; they may want to use SI as a means of improving their risk/return profile; or they may like the idea of contributing towards positive change in society.

Rather than being a ‘one size fits all’ philosophy, Sustainable Investing should therefore be thought of as an umbrella concept which reflects all these motivators.

For our purposes, we define SI as comprising three core approaches

- Exclusions;

- ESG integration; and

- Impact investing.

Exclusions

Perhaps the oldest and easiest way to engaging in SI is by refusing to invest in a company that has controversial business practices. Such practices may range from business activities deemed to be harmful to health or the environment, such as tobacco or mining, to outright criminal behaviour such as corruption or forced labour.

The relevance and application of exclusions has become more widespread as economies and investment opportunities have become more globalised and we become more aware of the practices and attitudes that different cultures and societies deem acceptable or not (think Japanese whaling or third world ‘sweatshops’).

Many exclusion-based strategies avoid investing in firms involved in the so-called ‘sextet of sin’ – tobacco, weapons, alcohol, nuclear power, gambling and pornography. But what is deemed controversial evolves over time. For example, over recent years, it has become more common to exclude thermal coal miners, while some now view sugar as ‘the new tobacco’.

Whilst individuals are motivated to apply exclusions by their own moral/ethical code, for corporate investors the prospect of reputational damage – or put more simply, the fear of looking bad – can also be a reason to avoid investing in something that some groups in society disapprove of. The growth of social media has undoubtedly amplified this risk.

ESG Integration

This is the systematic use of financially material ESG criteria to improve the risk/return profile of investments, and therefore boost performance. Importantly, this approach is integrated into an existing framework that incorporates other – more traditional – metrics and is not used in isolation.

The United Nations Principles for Responsible Investment defines this process as:

“The explicit and systematic inclusion of environmental, social and governance issues in investment analysis and investment decisions. Put another way, ESG integration is the analysis of all material factors in investment analysis and investment decisions, including environmental, social, and governance factors.”[8]

Key here is ‘financial materiality’ – the factors being considered are not just ‘nice to have’ but have a direct impact on the company’s bottom line. For example, an investor will not just look at factors such as pollution or excessive waste from the perspective of harming the environment. Such behaviour may also have a financial impact on the company, from attracting fines, to raising costs and regulatory risks due to poor resource conservation.

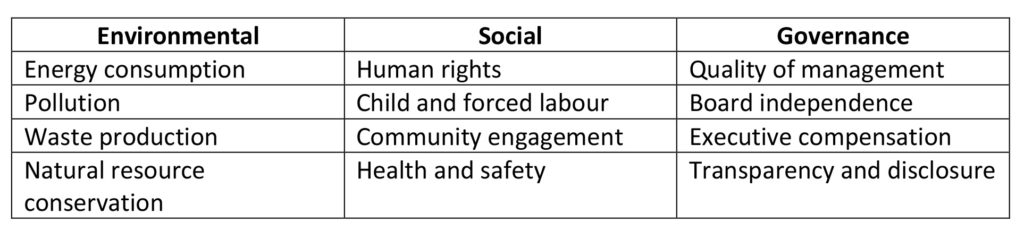

Some examples of ESG attributes used to assess a company/investment are listed below:

ESG integration is usually done in three steps. The first is to identify and focus on the most material issues affecting the company. Then the investor can analyse the likely impact of these material factors on the company’s business model. Finally, this information can be incorporated into the valuation analysis to form a fundamental view.

A big advantage of ESG integration is that it works across all asset classes – it has been proven to work just as well in fixed income markets as in equities and can also be applied to commodity or real estate portfolios. In general, ESG analysis in equities seeks to identify an upside that is not necessarily reflected in the share price, while analysis in bonds seek to expose any downside that may not show up in its credit rating.

Two specific ways of applying ESG analysis to investment decisions are positive screening, which seeks out those securities with higher ESG scores, and Best-in-class which takes this one step further and solely targets companies with the highest ESG scores in a particular sector.

Whilst the best-in-class approach is becoming a popular means of creating sustainability-themed portfolios, it does have the drawback of relying solely on ESG criteria as the only driver of future return.

Impact investing

Impact investing involves making investments with the aim of creating a measurable beneficial impact on the environment or society, as well as earning a positive financial return.

In 2015 the United Nations General Assembly adopted 17 Sustainable Development Goals (SDGs). These goals include the eradication of poverty, clean water and sanitation, gender equality and good health and wellbeing.

Many investors choose to target funds that in some way or other contribute to one or more of the goals. For example, a fund may seek to buy food producers that are investing in healthier and cheaper products (eradicating hunger – SGD 2), or health care companies that are developing vaccines for use in emerging markets (good health and wellbeing, SDG3), among others.

Impact investing has three key components. First, there must be intentionality: an investor is making a deliberate, targeted effort to exert a positive impact. Second, it should generate a positive return on investment; this is not charity. And third, the financial, social and environmental benefits of impact investment should be measurable and transparent.

SI growth drivers

The growth of Sustainable Investing has been driven by many powerful and interconnected global forces. These include megatrends such as climate change and digitalisation, evolving regulatory frameworks, an increased focus on the UN SDGs, and the massive wealth transition that is putting more money – and power – in the hands of millennials.

Climate change

It is important for investors to assess the impact of climate change on asset class return expectations. The most significant physical impacts of climate change will be seen in the second half of this century, but the consequences for forward-looking asset markets may become apparent much sooner. When expectations for climate change are adjusted, the markets and asset prices will reflect these developments, possibly sooner than the physical changes of global warming make themselves felt.

Obvious examples of areas impacted by climate change include resources, energy production, manufacturing and insurance.

Digitalisation

The increasing connectedness of societies and economies is leading to risks of security breaches, data privacy issues and false information. No matter how much companies spend on technical cybersecurity solutions, success ultimately hinges on the judicious and disciplined implementation of cybersecurity policies. Investors therefore need to anticipate both IT spending and organisational culture when assessing the risk profile of a potential investment target.

Evolving regulatory frameworks

Regulatory frameworks around the world are increasingly forcing companies to take a more sustainable approach. In some instances, this is a response to global shocks like the GFC, in others it is to ensure progress towards agreed climate targets or Sustainable Development Goals.

Perhaps the most famous is the Paris Agreement that was ratified by 174 countries on 22 April 2016 – now designated by the UN as ‘Earth Day’.

In financial markets, regulation ranging from Basel III to Solvency II has put in place measures to prevent another global financial crisis, which has changed the ways in which banks and insurers operate. Stewardship codes are becoming increasingly common.

Other initiatives on the way include plans by many governments to force companies to reduce sugar levels in foods to combat obesity, possibly with sugar taxes now being trialled in various countries including the UK and Mexico.

Many countries – including Australia – have adopted modern slavery laws, requiring greater checks in supply chains to root out any child or slave labour, dangerous working conditions or other socially unacceptable practices. And in some countries, exclusions are legally enforceable, such as the Dutch ban on investments in controversial weapons such as cluster bombs.

In some jurisdictions, regulations are also evolving to reflect the increased demand for, and awareness of, ESG issues. In Australia for example, APRA has recently announced[9] its intention to update superannuation Prudential Practice Guide SPG 530, which addresses the integration of ESG issues into investment processes.

Wealth transfer to socially aware millennials

Meanwhile, a major wealth transition is taking place in which more capital is gradually being controlled by millennials – the generation born since the mid-1980s. Research shows that this cohort have much more interest in investing sustainably than their parents or grandparents – and they will have a lot of money to play with. Millennials will inherit up to USD 59 trillion between now and 2060, creating the largest intergenerational wealth transfer in history, according to the Center on Wealth and Philanthropy at Boston College.[10]

In Australia, this transfer has been estimated at AUD 3 trillion[11].

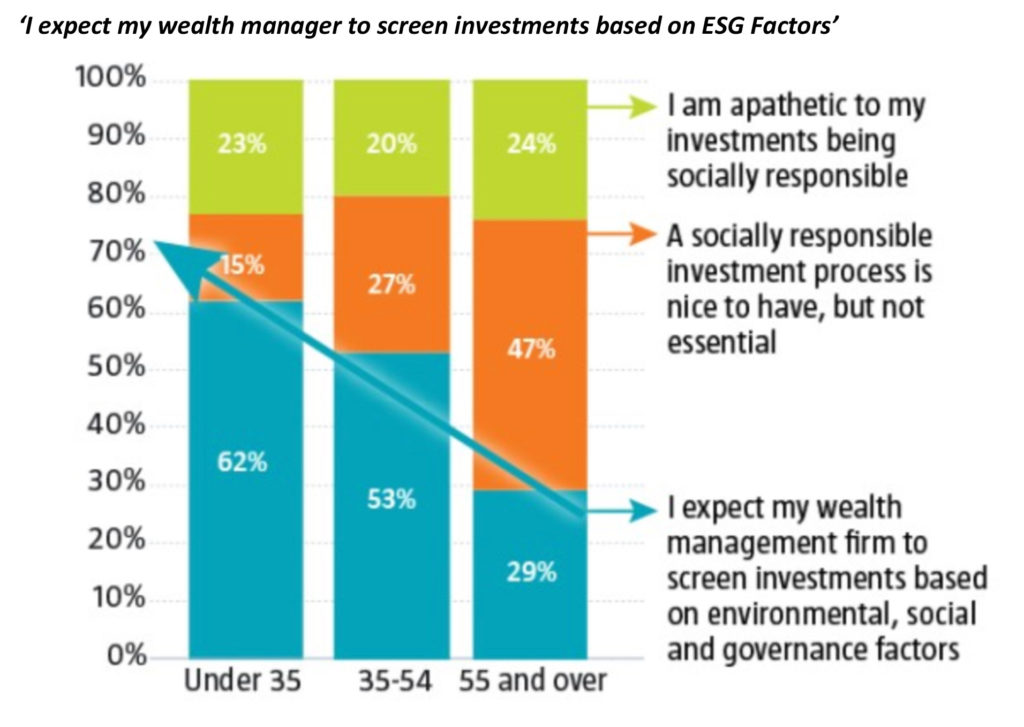

Morgan Stanley’s 2017 ‘Sustainable Signals’ report found that millennials are twice as likely as other investors to want to contribute to a better world as well as make a financial return. “A younger generation of investors, who overwhelmingly believe that their investment decisions can make an impact, is leading the sustainable investing charge,” it said.[12]

These attitudinal differences between generations are summarised in the graph below, based on 2017 research by Factset[13].

Adviser considerations and implications

For financial advisers, the growing interest in Sustainable Investing philosophies has a number of important implications and considerations.

- As advisers engage with more and more millennial clients, they will encounter more interest in SI philosophies and demand for SI products;

- Rather than being a niche investment category, SI is mainstream, with the majority of professionally managed investments in Australia are managed in accordance with SI principles;

- The ubiquity of SI reflects not only increasingly powerful social and regulatory factors, but also the superior investment returns achieved by funds managed sustainably;

- Rather than SI being a homogenous, one size fits all framework, SI should be thought of as an umbrella concept, under which sit several different approaches;

- These approaches reflect the diverse range of motives – including ethical concerns – that drive individuals to invest sustainably.

- Advisers should identify whether there are any gaps between increasing demand for SI offerings on the part of their clients, and the extent to which these offerings are understood and available for client consideration.

- Any regulatory guidance around consideration of SI issues in line with growing investor demand for – and awareness of – SI offerings should also be considered.

In summary, a growing desire to make a positive impact on the planet exists at all levels, government, business and individual. As the momentum behind Sustainable Investment continues to grow, financial advisers have an ideal opportunity to engage with both new and existing clients, helping facilitate outcomes which can meet both ethical and financial objectives, and adding a new dimension to the value of their advice.

Read more about sustainable investing: CPD: Sustainable Investing in action in Australia

———-