Sustainable Investing in action in Australia

Tracing its origins back several centuries, Sustainable Investing is an important and growing part of the global investment landscape.

Introduction

In the previously published first article of this two-part series (‘Sustainable investing, concepts, considerations and conversations’), we introduced the topic of Sustainable Investing (SI), focussing on the different types of SI, its origins, and growth drivers. In this second part we will take a closer look at Sustainable Investing in action in Australia, including the regulatory framework, the nature of active investment, and performance track record of funds managed under SI principles. We will also bust some of the most common SI myths.

Sustainable Investing – a brief recap

Tracing its origins back several centuries, Sustainable Investing is an important and growing part of the global investment landscape. Driven by several factors, including the growing impact of climate change and increasing regulatory oversight of areas such as governance, corporate culture and supply chain management, socially aware investors are placing more emphasis on the SI credentials of investment vehicles.

For our purposes, SI is not confined to ethical investing, but rather refers to a more comprehensive approach to investing which ultimately views environmental, social and governance (ESG) considerations through a financial lens, quantifying risks and taking a long-term view.

As depicted in Figure 1 below, we define Sustainable Investing as comprising three core approaches: exclusions, ESG integration, and impact investing. More detail on each of these approaches can be found in our earlier article.

Sitting beneath these umbrella SI approaches are a number of specific strategies, including negative and positive screening, thematic sustainable investing, and active ownership (a strategy we will examine in more detail later in this article).

Sustainable Investing is now the dominant approach, and it is still growing

Far from being a niche category, SI is becoming a dominant approach globally.

In 2018 it was estimated[1] that more than $30 trillion USD were managed according to SI principles around the world, representing growth of 34% over the previous two years.

Furthermore, the Global Sustainable Investment Review estimated[2] that in 2018 more than 60% of funds under management in Australia and New Zealand and half of FUM in Europe and Canada were being managed in this way.

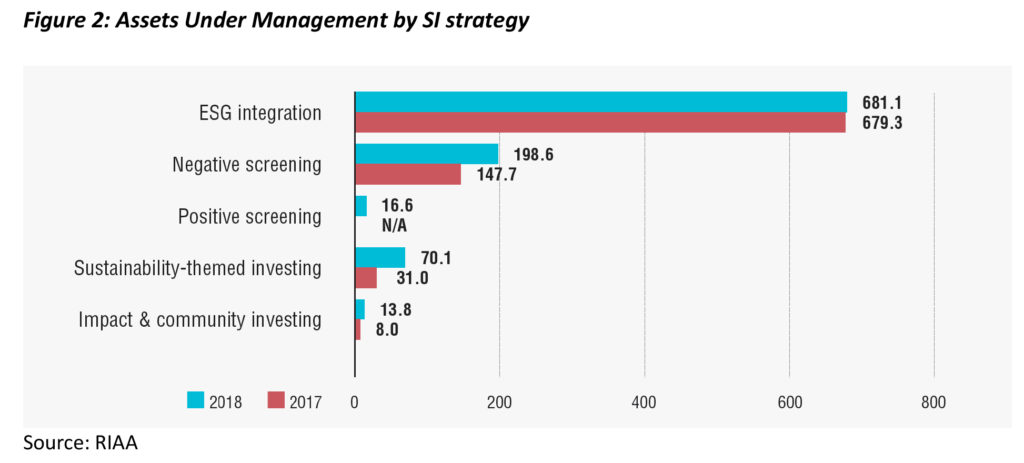

Breaking this down by approach, ESG integration is by far the most used common strategy, although negative screening is also gaining traction, as can be seen in Figure 2 below[3].

Active ownership

Shareholders in a business are owners of that business, and increasingly investors are using this ownership power to influence how firms are run in order to protect or enhance their investments. This kind of ‘active’ ownership is now at the forefront of Sustainable Investing, and in Australia it is estimated around one third of sustainable investment managers are employing active ownership strategies[4].

Whilst for some the term ‘shareholder activism’ conjures negative images of small groups of investors wielding disproportionate amounts of power, disrupting shareholder meetings and pursuing social causes, the reality of active ownership, particularly in Australia, is more about ongoing corporate engagement, with a particular focus on governance issues.

The two main types of active ownership are corporate engagement and shareholder voting.

Corporate engagement

Corporate engagement is the process of entering into a formal dialogue with those companies that are seen to have sustainability issues that could affect their future performance and value.

Engagement can be on issues across the environmental, social and governance spectrum, and whilst perceived governance failures are undoubtedly a major driver of investor engagement activity, investors have realised that environmental and social issues are also better dealt with through engagement. It is, after all, easier to influence a company’s behaviour by engaging with it than by excluding it or divesting it from a portfolio. Divesting thermal coal producers, for example, may make a portfolio more sustainable, but it has no effect on achieving decarbonization overall. Instead, investor efforts have focused on trying to persuade fossil fuel producers to change business models and switch to renewables.

Shareholder voting

One of the most powerful points of leverage investors have in terms of exerting influence over the direction of a company is of course their ability to vote against that company’s policies at shareholder meetings.

While individual shareholders with only a small percentage of the stock may not be able to make a difference unilaterally, many investors now band together to create a more powerful, collective force of influence. This has been seen in the growth of investor associations, who often use a sophisticated approach to gathering voter proxies, giving them the power to be heard on bigger issues.

For Australian shareholders, executive remuneration is a particularly important topic, and one on which legislation affords them significant power via the ‘two strikes rule’.

Under this rule, introduced in 2011, if shareholders vote down a company’s executive remuneration package two years in a row, the board may be voted out of office. Even if voting against it does not immediately curtail the pay levels at a company, it has proven very effective in creating enough reputational damage or embarrassment for companies to ensure action is eventually taken.

Two well-publicised Australian examples of remuneration strikes are AMP, who in 2018 became the first ASX 50 company to record a remuneration strike[5] (in the midst of the Hayne Royal Commission), and Westpac, who recorded a second strike in late 2019. Whilst Westpac’s shareholders declined the opportunity to spill the board at this time[6], the associated fallout did cost the CEO and Chair their jobs (as was also the case at AMP).

Whilst Australian corporate law is seen as particularly conducive to active ownership – through the two strikes say-on-pay vote or the ability to call a shareholder meeting pursuant to the Corporations Act – some experts believe that this actually allows institutional investors much better access to boards and senior management, especially at larger companies. This access has in turn allowed Australian investors – relative to their global peers – to use behind the scenes engagement more than the blunt instrument of public shareholder activism, as borne out in Figure 3 below[7].

Busting the SI performance myth

Despite the obvious – and growing – scale of Sustainable Investing, some legacy misconceptions persist. The most powerful – and pertinent for advisers – is that ESG led investment processes carry a performance penalty.

In fact, there is now plenty of evidence – ranging from academic studies to actual performance data – showing that an SI approach can enhance returns.

The 2015 paper ‘From the Stockholder to the Stakeholder: How Sustainability Can Drive Financial Outperformance’ by Oxford University and Arabesque Partners[8] examined more than 200 sources and concluded that “80% of the reviewed studies demonstrate that prudent sustainability practices have a positive influence on investment performance”.

A separate survey later that year by Deutsche Bank’s Asset and Wealth Management division in conjunction with the University of Hamburg went even further[9]. This research looked at the entire universe of 2,250 academic studies published on the subject since 1970 and concluded that an ESG approach made a positive contribution to corporate financial performance in 62.6% of cases and produced negative results in only 10% of cases (the remainder were neutral).

Actual performance data also bears out these findings, with Figure 4 showing that investments managed under SI principles actually outperform non-SI investments over most time frames and asset classes[10].

Other common misconceptions about Sustainable Investing

Another pervasive myth is that sustainability is only about green issues. While the environment remains important, ESG means focusing on social and governance factors as well.

Issues as diverse as education, energy, food production and supply chains are all important ones for investors to consider (the latter two becoming very top-of-mind during the panic buying seen as a result of COVID-19). Renewable energy is arguably one the biggest business opportunity of our times, and for many this is less about the environment and more about the fact that unsubsidised renewable energy is now most frequently the cheapest source of energy generation[11].

Meanwhile, a very 21st century misconception is that only millennials are interested in sustainability. While, it is true that younger people are more likely to believe in it more than their parents or grandparents, research referenced in our earlier article showed that more than half of respondents aged 35 – 54 and nearly 30% of those aged 55 and over expected their wealth manager to screen investments based on ESG factors[12].

ESG in action case study – CSL

If ever a company deserved the accolade ‘market darling’, it would be CSL.

When assessed purely from a shareholder return perspective, it is an absolute standout, and after years of consistent profit growth it has surpassed the major banks and miners to become the largest in terms of ASX market capitalisation.

Yet as a story in the AFR[13] alludes to, even CSL – who specialises in the collection and supply of blood plasma – is finding itself under intense scrutiny by analysts who are pricing in a degree of ESG risk, related to the way the company solicits blood donations.

Specifically, there are questions about whether donations – for which donors are paid are concentrated in more disadvantaged areas. This raises both financial and reputational risks. Should such activities be seen to be exploitative, possible scenarios could include CSL ends up paying more to donors, or there being a crackdown on migrant donors, or the maximum donations per year being lowered. All of which would have the effect of raising costs.

Whilst CSL flatly rejects any suggestion that its practices are exploitative – and most experts agree with them – the story does illustrate that ESG considerations are much broader than ‘green issues’, and they can be absolutely financially material.

The Australian regulatory framework for SI

The global nature of investment markets sees investors operate across a range of complex and ever-changing social and regulatory frameworks.

From an SI perspective, the main architects of the framework in Australia are the Federal Government, along with ASIC and APRA – who drive a lot of the detail – and the various industry associations who help provide vital market feedback and input into an evolving set of rules and regulations.

Of particular relevance to the topic of SI is the legislative landscape in areas such as climate change, labour exploitation, resource degradation, energy and education, and some of the evolution in Australian laws in these areas relates, directly or indirectly, to Australia fulfilling its commitment to the 17 Sustainable Development Goals (SDGs) adopted by the United Nations General Assembly in 2015.

One high profile example is the Modern Slavery legislation, which came into effect in Australia at the start of 2019, and which other G20 countries – including the UK - have also put in place.

Owing much to the highly publicised ‘sweatshop’ scandals which enveloped global fashion brands such as Nike over a decade ago, the intent of this legislation is to force companies – across all industries – to examine their supply chains and eradicate any reliance on ‘slave’ labour by any of its suppliers.

Much of ASIC’s work and guidance around sustainability has focused on climate risk, and the extent to which companies disclose the nature and quantum of that risk to investors and other stakeholders.

In September 2018 they released Report 593, an examination of climate risk disclosure by Australian listed companies. High-level recommendations set out in that report included companies adopting a proactive approach to emerging risks, including climate risk, and the development and maintenance of strong and effective corporate governance which helps in identifying, assessing and managing risk.

In August 2019, ASIC followed up Report 593 by announcing[14] updates to two Regulatory Guides, 228 and 247. These updates included:

- RG 228 (Prospectuses: Effective disclosure for retail investors) – updated to incorporate the types of climate change risk developed by the G20 Financial Stability Board’s Taskforce on Climate Related Financial Disclosures (TCFD) into the list of examples of common risks that may need to be disclosed in a prospectus; and

- RG 247 (Effective disclosure in an operating and financial review) – updated to highlight climate change as a systemic risk that could impact an entity’s financial prospects for future years and that may need to be disclosed in an operating and financial review (OFR).

APRA’s view and intentions in this space were clearly articulated back in 2017, by Executive Board member Geoff Summerhayes:

“The days of viewing climate change within a purely ethical, environmental or long-time frame have passed…… Some climate risks are distinctly ‘financial’ in nature. Many of these risks are foreseeable, material and actionable now. Climate risks also have potential system-wide implications that APRA and other regulators here and abroad are paying much closer attention to.”[15]

In February 2020, APRA sent a letter[16] to all APRA-regulated entities outlining plans in a number of areas. These plans included the development of a new climate-related financial risk prudential practice guide, and the updating of superannuation Prudential Practice Guide SPG 530 Investment Governance (which includes sections relating to environmental, social and governance (ESG) investments). They also announced their intentions to conduct a climate change financial risk vulnerability assessment in 2021.

To the extent that ESG considerations are now identified as core business risks with material financial implications, such guidance is eagerly sought by many stakeholders, not least the board of directors who can be held liable for breaching their legal duty of due care and diligence if they don’t afford such risks due consideration.

Elements of self-regulation are also common across the Australian financial sector, with relevant examples in SI being the Australian Asset Owner Stewardship Code, to which many members of the Australian Council of Superannuation Investors (ASCI) are signatories, and the FSC Standard on Asset Stewardship.

Stewardship principles include active ownership by asset owners and asset managers over investment assets, with signatories to the ACSI Code committing themselves to activities including monitoring assets and service providers, engaging with companies and holding them to account on material issues, and voting and publicly reporting on the outcomes of these activities.

Guidance specific to financial advisers

Although there are not currently any specific legal requirements for advisers to explicitly address ESG matters with their clients, there are several relevant pointers to be found across various Acts and Regulatory Guides.

Section 961B (2) of the Corporations Act sets out various things that an adviser must do to be acting in a client’s best interests including identifying the objectives, financial situation and needs of the client.

ASIC regulatory guide 175 provides further guidance on how advisers can satisfy their duty to the client.

When it comes to enquiries about the client’s view on sustainability (or ESG factors), RG 175 suggests Advice providers must form their own view about how far s961B requires inquiries to be made into the client’s attitude to environmental, social or ethical considerations:

“Advice providers may need to ascertain whether environmental, social or ethical considerations are important to the client and, if they are, conduct inquiries about them”. (RG175.311).

The RIAA, in its Financial Adviser Guide to Responsible Investment[17], suggest that, in order to comply with their legal duty, advisers ought to ask clients a full and comprehensive set of questions including seeking out any sectors they may not be comfortable investing in.

The Guide refers to the EU’s proposal to place a positive requirement on advisers to proactively seek out the sustainability preferences of their clients and suggest that this may become the ‘new norm of knowing your client’.

There seems little doubt that proactive consideration of ESG issues will increasingly form part of the financial advice process, whether mandated or driven by client demand.

Conclusion

Far from being niche, Sustainable Investing is now ‘mainstream’, with formal consideration of environmental, social and governance (ESG) issues becoming common – and often mandatory – practice for businesses across all industries.

This article builds on our earlier partner article – ‘Sustainable Investing; concepts, considerations and conversations’ – to create a comprehensive overview of the Sustainable Investments category.

Having previously explained the origins of SI, the size of the SI market and its growth drivers, as well as the different SI strategies, this article takes a more detailed look at Sustainable Investing in action in Australia, including the evolving regulatory framework and the nature of ‘active’ investment. We also address some of the most common SI misconceptions and prove beyond doubt that SI practices tend to enhance – rather than dampen – investment performance.

An understanding of the concepts covered across both articles will better equip advisers to respond to the increasing market interest in Sustainable Investing, allowing them to facilitate advice outcomes which can meet both the ethical and financial objectives of their clients.

Read more about sustainable investing: CPD: Sustainable investing – concepts, considerations and conversations

———