Investment markets and key developments over the past week

Global share markets pulled back over the last week on worries about “second waves”, the economic outlook and tensions with China. Australian shares were hit too with concerns about trade tensions with China and worries about the banks but good gains in materials, telcos and health shares saw the market down only slightly over the week. Bond yields fell slightly as did copper prices, but the oil price rose for the third week in a row as oil production fell and demand rose (with US gasoline demand up 46% over the last five weeks). The iron ore price also rose to around $US90 a tonne but the Australian dollar fell as the US dollar rose in line with risk aversion in share markets.

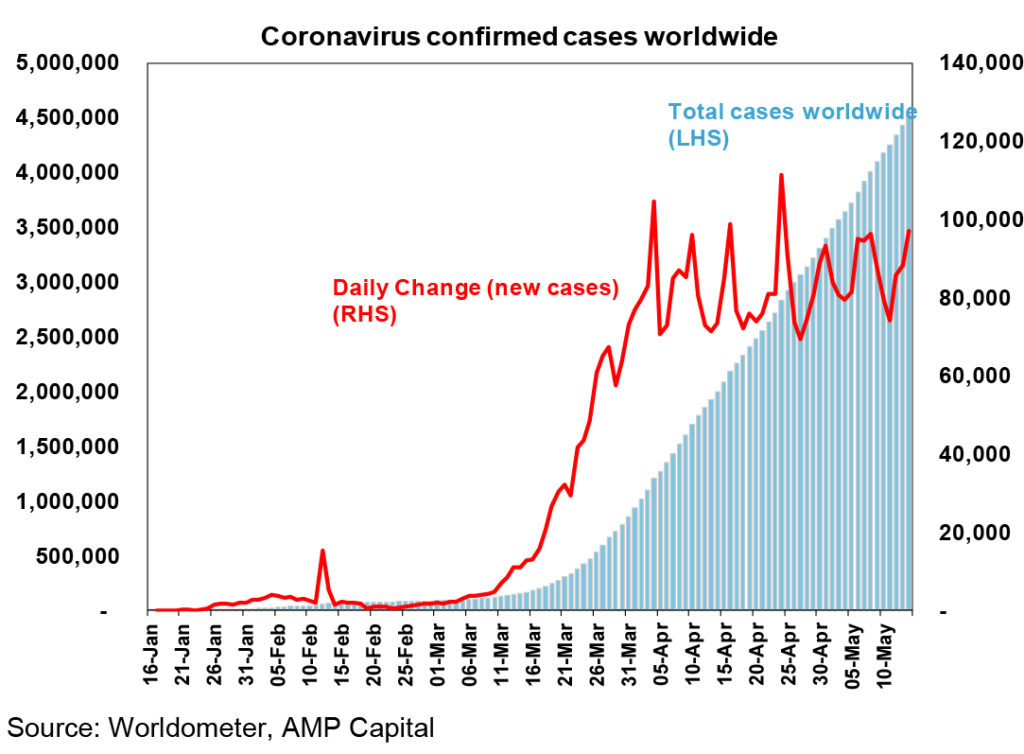

The picture is little changed with coronavirus. New global cases are continuing to trend sideways.

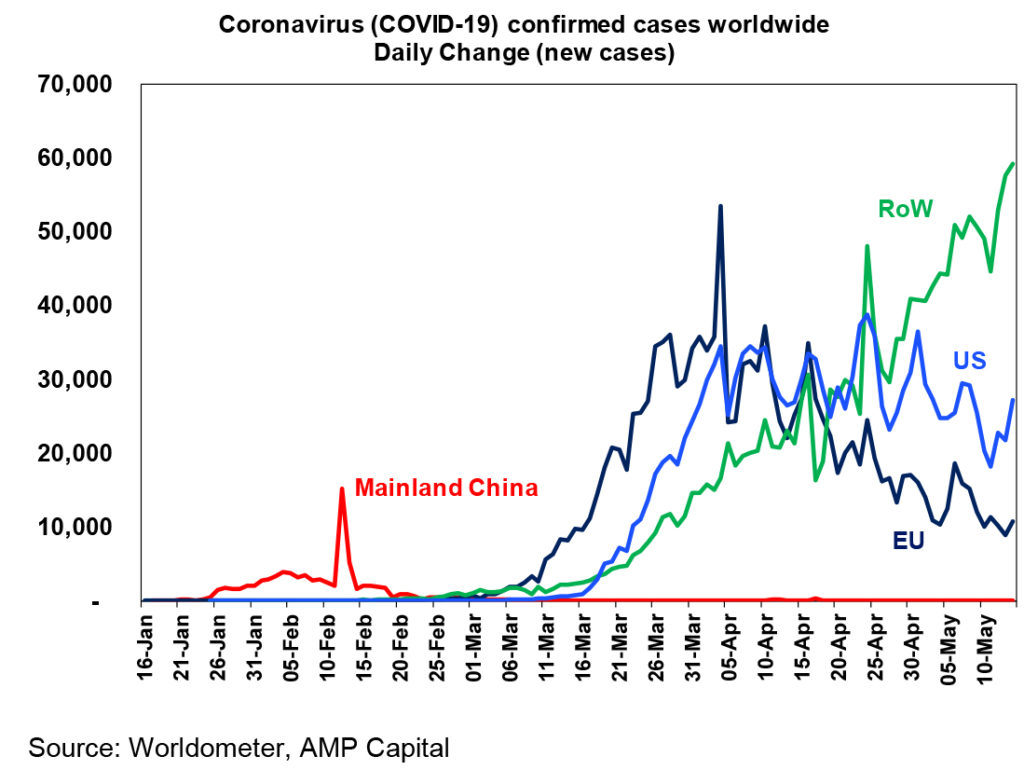

Europe is continuing to see a decline in new cases despite occasional clusters. Japan looks to have got its early April breakout under control. New cases look to have peaked in the US and UK. However, various less developed countries are driving a still rising trend in the rest of the world. This includes Brazil, India, Mexico, Iran and Russia.

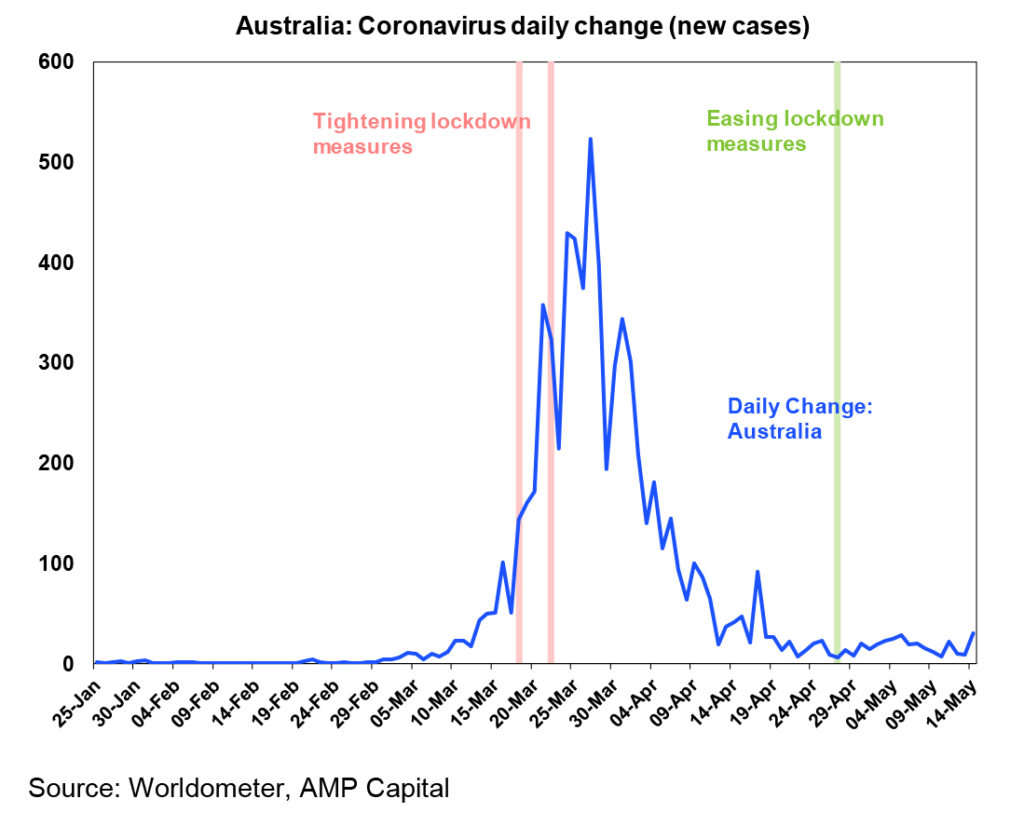

Australia is continuing to see a low number of new cases, but still has some problems with clusters.

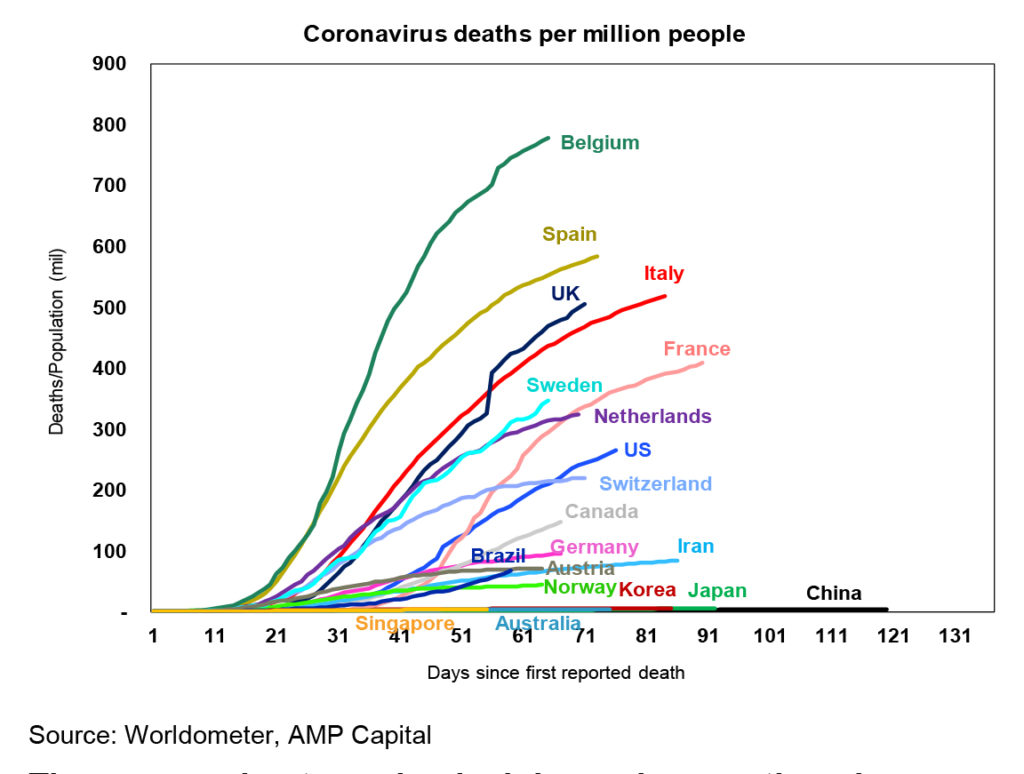

Reflecting this, deaths per million people remain very low in Australia at around 4, which is similar to Korea, Japan, Singapore and China. This contrasts with the UK and Italy where deaths are around 500 per million people which if the same had occurred in Australia would have meant around 12,500 deaths as opposed to around 98.

The progression to easing lockdowns has continued across Europe, the US and Australia. The risks are probably greatest of a second wave in the US as some states and cities have moved ahead of the medical checkpoints in the Government’s reopening Guidelines – although many of those states are less densely populated and so less at risk and nearly 80% of US GDP is located in states seeing declines in new coronavirus cases. Australian states have generally moved to implement the Federal Government’s reopening roadmap, albeit with Victoria moving more slowly.

While economic activity remains weak, high frequency data continues to indicate that activity may have hit bottom. Our weekly economic activity trackers for the US and Australia based on high frequency data for things like restaurant bookings, confidence, retail foot traffic, box office takings, credit card data, mobility indexes & jobs data are up from their lows in mid-April – albeit only a bit and more so in Australia. In Australia weekly consumer confidence has risen for six weeks in a row, surveys show a pick in consumer spending and traffic flows have picked up – in fact the traffic last Saturday in Sydney seemed to resemble a normal Saturday (even without kids sport!)….which all tells me that there is a bit of pent up demand out there.

On the policy stimulus front there were a few more developments over the past week:

- India announced a headline stimulus package of around 10% of GDP – although details are lacking and in terms of actual fiscal stimulus its likely to come in below 5% of GDP.

- New Zealand increased its fiscal response to around 20% of GDP, which looks consistent with budget deficits running around 10% a year.

- The Reserve Bank of New Zealand left its cash rate at 0.25% but almost doubled its bond buying QE program and signalled that negative rates are likely in early 2021 and that the direct purchase of bonds from the government has not been ruled out.

- On negative rates, Fed Chair Powell reiterated that they are not being considered, that evidence as to their effectiveness is “very mixed” and that forward guidance and QE are the Fed’s core tools now. But he did repeat that the Fed will basically do whatever is necessary. And he urged more fiscal support given downside risks to the economy.

- Speaking of which the process towards another stimulus package is now underway in the US. Republicans have as expected rejected a Democrat $3trillion stimulus (13.6% of GDP) plan but it does look as if a path to a more realistic plan is starting (slowly). The question is whether it will get there without much prodding from markets or whether another market tantrum is needed? I suspect it’s the latter.

Will the RBA move to negative rates and the direct buying of bonds if say NZ does? I doubt it. Soon after RBNZ Governor Orr expressed an openness to negative rates last year RBA Governor Lowe dismissed them in relation to Australia. Like the Fed the RBA can’t see much benefit from the negative rates experience in Europe and Japan (and nor can I). Lowe has regularly stated that 0.25% is the effective lower bound. And his 21 April speech emphasised that the RBA is not buying bonds directly and spoke in favour of the separation of monetary and fiscal policy. And don’t forget New Zealand’s lockdown was more severe than Australia’s and so the hit the economy was greater so they need more desperate measures – ha ha I can say that as my Mum is a New Zealander and after Australia there is no better place than NZ!

How serious is the threat posed by China’s threatened tariffs on Australian barley and the suspension of beef imports from four Australia abattoirs (including one which is owned by a Chinese company)? Its hard to know. On the Australian side this is seen as tangled up with Australia’s call for an independent inquiry regarding the coronavirus outbreak. But China also has trade gripes with Australia with the barley and beef issues having been around for a while and a concern regarding tariffs put on Chinese steel, aluminium and chemical imports which are seen by many as protectionist (eg 144% on Chinese steel pipes!). Such issues have flared up before only to flare down again before they spread – remember last year with bans on imports of Australian coal to various Chinese ports. Hopefully the same happens this time around again – because so far, our exports appear to be benefitting from the recovery in the Chinese economy (with iron ore export volumes out of Port Hedland up 11% year on year in April).

For now, shares are still at risk of a further pull back after the strong run up since 23rd March. It may turn out to be no more than a consolidation, but a deeper pull back is risk. But providing we are right, and April or May prove to be the low point in economic activity then given the massive policy stimulus already seen shares should be higher on a 12-month outlook. The three big risks remain: a second wave of coronavirus cases (that’s a low risk in Australia, but high in the US); collateral damage from the shutdowns resulting in a delayed or very slow recovery; and an escalation in US/China tensions. On the latter, the risks will likely escalate dramatically if Trump’s approval rating collapses leading him to conclude that he has nothing to lose by trying to “wag the dog”.

Major global economic events and implications

US small business optimism fell in April, albeit it was stronger than expected and jobless claims remained high but fell for the sixth week in a row. Inflation fell sharply with core inflation falling to 1.4% year on year.

The never-ending Brexit story still hasn’t gone away. Its fallen of the market radar given coronavirus…but not a lot of progress has been made in trade deal negotiations between the UK and EU and the mid-year deadline to extend the transition period from year end (after which free trade between the UK and EU comes to an end if there is no deal) is rapidly approaching. It will mostly likely be extended but there is a risk that the UK decides to allow a disorderly exit given its economic impact will be swamped by that of the coronavirus shock.

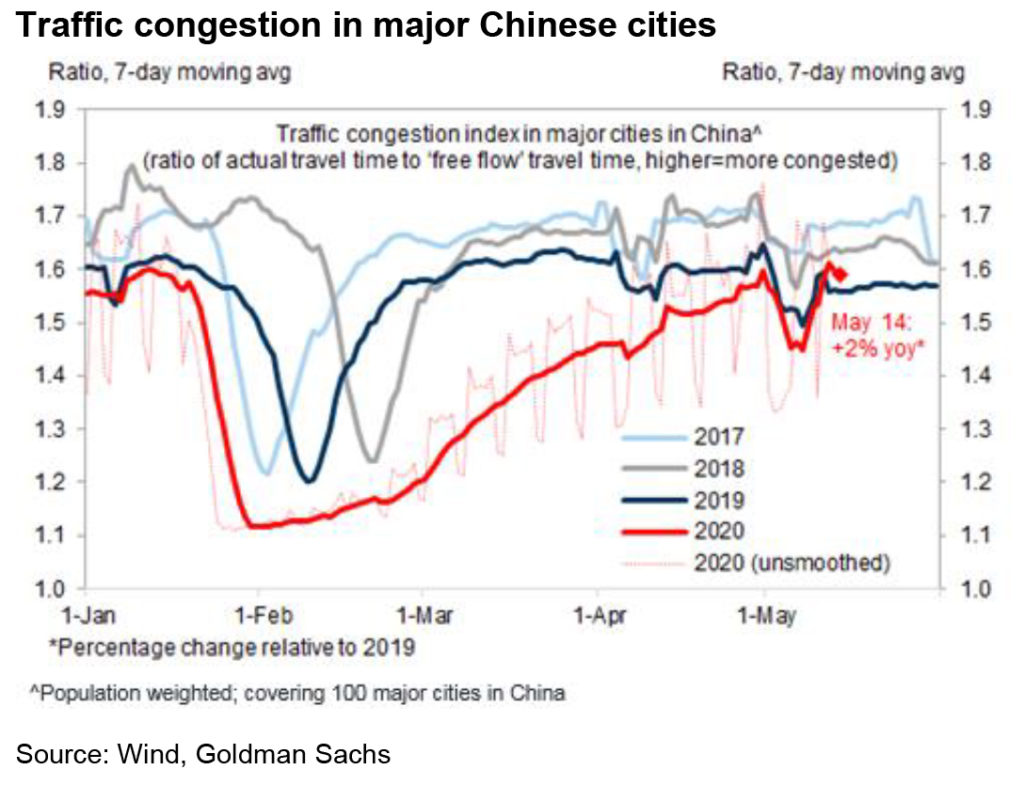

The Chinese economy is continuing to recover. Over the year to April industrial production rose a stronger than expected 3.9%, but this is up from a -13.5% fall in January and February. Retail sales fell -7.5%yoy, but this is up from -20.5% in Jan/Feb. And investment fell -10.3%, but this is up -24.5% in Jan/Feb. The recovery is also evident in passenger car sales which were down -82% year on year in February but have since picked up to be down just -2%yoy in April. Growth is not yet strong enough to stop unemployment rising to 6% in April, but the recovery in activity is consistent with high frequency data showing that the low point in the Chinese economy was in February. For example, traffic congestion in major cities is back to around normal. Meanwhile, Chinese money supply and credit growth accelerated in April reflecting policy easing and inflation fell sharply with core CPI inflation of just 1.1%yoy.

Australian economic events and implications

Australian jobs data provided a confusing picture with a much smaller than expected rise in unemployment to 6.2% masking a significant deterioration in the labour market. Basically, while roughly 600,000 jobs were lost last month, around 500,000 people left the workforce which meant that the unemployment rate “only” rose to 6.2%. The decline in workforce participation was presumably because laid off workers didn’t look for work due to either the lockdown or on the assumption that they will just go back to their old job when the lockdown ends. The changed rules enabling people to access JobSeeker without having to seek paid employment may have also encouraged many to temporarily leave the workforce. Were it not for the fall in participation the unemployment rate would have been 9.6%. But there is still a huge hit to household income due to a 9.2% drop in hours worked with 2.7 million workers either leaving employment or having their hours reduced (as indicated by a rise in underemployment to 13.7% and a rise in labour underutilisation to around 19.9%). And of course, were it not for JobKeeper employment would have fallen a lot more than the 594,000 decline reported – in fact over 5.5 million workers are now protected by JobKeeper. Thankfully! The other piece of “good news” is that Australia has avoided confidence zapping headlines around “surging unemployment.” We still see unemployment rising from here, but the April report gives us more confidence that it won’t get above 10%. In fact, it may not get much above 8% given that the big hit to the economy and jobs was in April. The main risk will be after September if the economy hasn’t recovered much and JobKeeper and the enhanced JobSeeker ends seeing more workers defining themselves as unemployed.

Our view remains though that by September the economy will be on the mend, consistent with the easing in the lockdown. Consistent with this both business confidence (as measured by the NAB survey) and consumer confidence (as measured by the Westpac/MI and ANZ/Roy Morgan surveys) have moved up from their lows with consumers less negative on the labour market.

The slump in housing construction will continue well into 2021 though with HIA data showing a fall in new home sales to record lows and the cancellation of 30% of new projects and reports of a sharp rise in rental vacancy rates according to SQM. Housing starts are probably on their way to around 120,000 this year down from a peak in 2017-18 of 230,000. This is part of a necessary rebalancing of the housing market to allow for a collapse in immigration. Government’s may have to start thinking about enhanced first homeowners’ grants and allowing immigrants back in to restart housing construction.

What to watch over the next week?

Markets will likely remain focussed on continuing evidence that the number of new Covid-19 cases is slowing and on progress in easing lockdowns.

In the US, business conditions PMIs for May (Thursday) are likely to bounce a bit after the sharp fall seen in April helped by economic reopening. Meanwhile, expect the NAHB home builders’ conditions index for May (Monday) to rise slightly, but housing starts (Tuesday) and existing home sales (Thursday) to fall sharply. The minutes from the last Fed meeting (Wednesday) are likely to remain dovish.

Eurozone business conditions PMIs for May (Friday) will also be watched for a bounce after the extreme low seen in April helped by moves towards reopening.

Japanese business conditions PMIs will also be released Thursday and inflation for April (Friday) is likely to have fallen.

In Australia, the ABS’ household impacts of coronavirus survey (Monday) and weekly payrolls and wages data (Tuesday) will be watched for signs of stabilisation after the sharp fall in employment reported into mid-April. Preliminary retail sales for April (Wednesday) are likely to fall by 15% or so after March’s 8% panic buying driven rise. CBA business conditions PMIs (Thursday) for May will be watched for a bounce after sharp falls into April. The minutes from the last RBA meeting (Tuesday) are likely to remain dovish with the RBA reiterating that it is committed to “do what it can to support jobs, incomes and businesses.

Outlook for investment markets

After a strong rally from March lows shares are vulnerable in the short term to a pull back or consolidation. But on a 12-month horizon shares are expected to see good total returns helped by an eventual pick-up in economic activity and massive policy stimulus.

Low starting point yields are likely to result in low returns from bonds once the dust settles from coronavirus.

Unlisted commercial property and infrastructure are ultimately likely to continue benefitting from the search for yield but the hit to economic activity and hence rents from the virus will weigh heavily on near term returns.

The Australian housing market has slowed in response to coronavirus. Social distancing has driven a collapse in sales volumes, and a sharp rise in unemployment, a stop to immigration and rent holidays pose a major threat to property prices. Prices are expected to fall between 5% to 20%, but government support measures including wage subsidies along with bank mortgage payment deferrals along with a plunge in listings will help limit falls as will a reopening of the economy in the months ahead.

Cash & bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.25%.

The hit to global growth from Covid-19 and its flow on to reduced demand for Australian exports and lower commodity prices still risks pushing the $A lower in the short term. But expect a rising trend once the threat from coronavirus recedes, particularly with the US expanding its money supply far more than Australia is via quantitative easing and with China’s earlier recovery likely to boost demand for Australian raw materials.

By Shane Oliver