Investment markets and key developments over the past week

Most major share markets fell over the last week as concerns about “second waves” of coronavirus cases, uncertainty about the growth outlook and geopolitical risks continue to rattle investors. The weak global lead and concerns about rising cases in Victoria also contributed to a fall in Australian shares with sharp falls in energy, industrial, IT and property shares. Bond yields were little changed although they fell in Europe. Oil prices fell, the copper price rose but iron ore was flat and the $A rose slightly as the $US fell.

After their huge rally into early June shares remain vulnerable to a further correction or period of consolidation, but we continue to see it as a pause in a rising trend. Risks around the growth outlook flowing from second wave worries remain significant and could drive a further correction. However, contrarian support for shares remains from a record amount of cash on the sidelines and investor sentiment remaining relatively cautious. The three big risks are: a second wave of coronavirus cases necessitating a renewed shutdown; collateral damage from the shutdown resulting in a slow recovery after the initial bounce; and the US presidential election with Trump likely to try and appeal to his base by ramping up tensions with China (and maybe even Europe), particularly if his approval rating continues to slide.

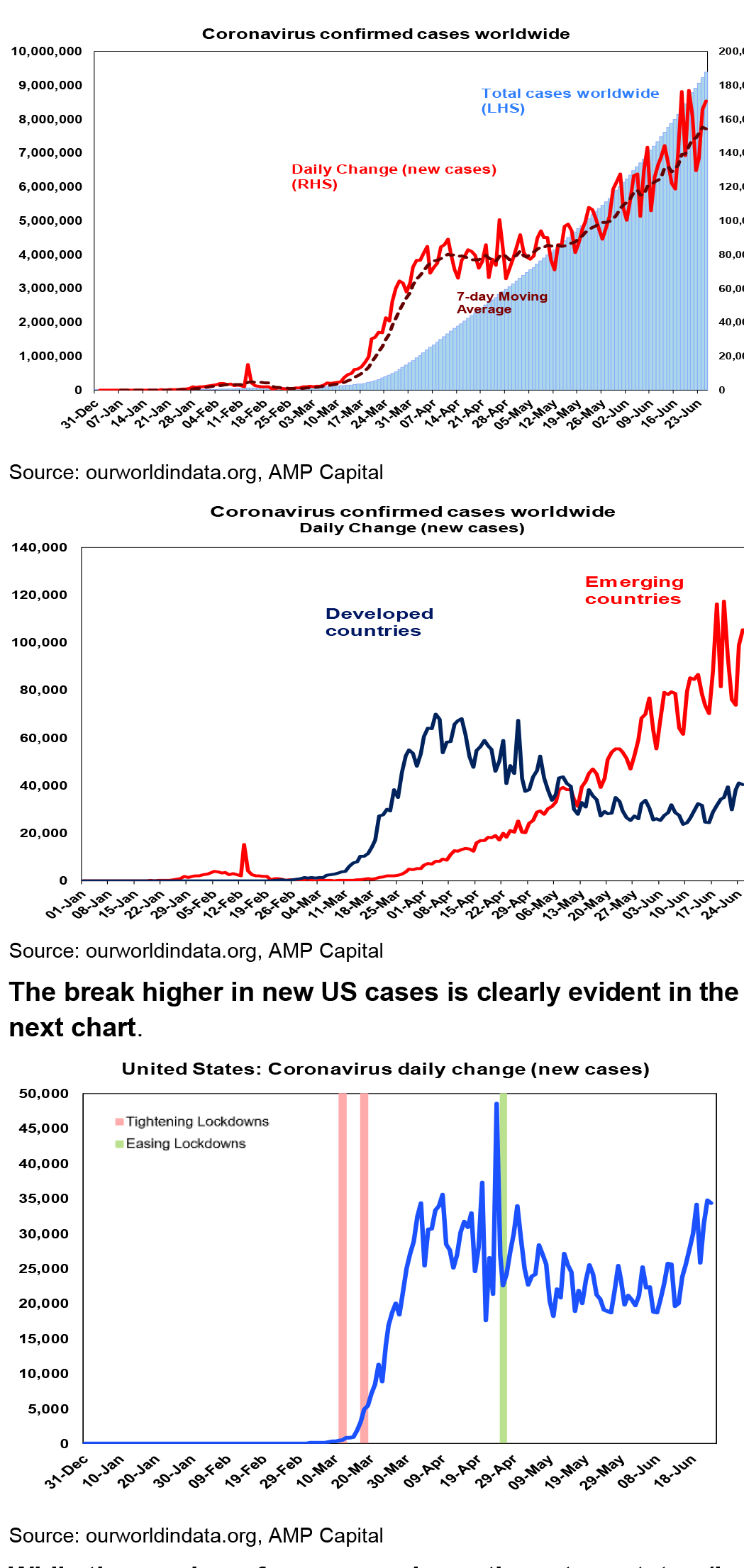

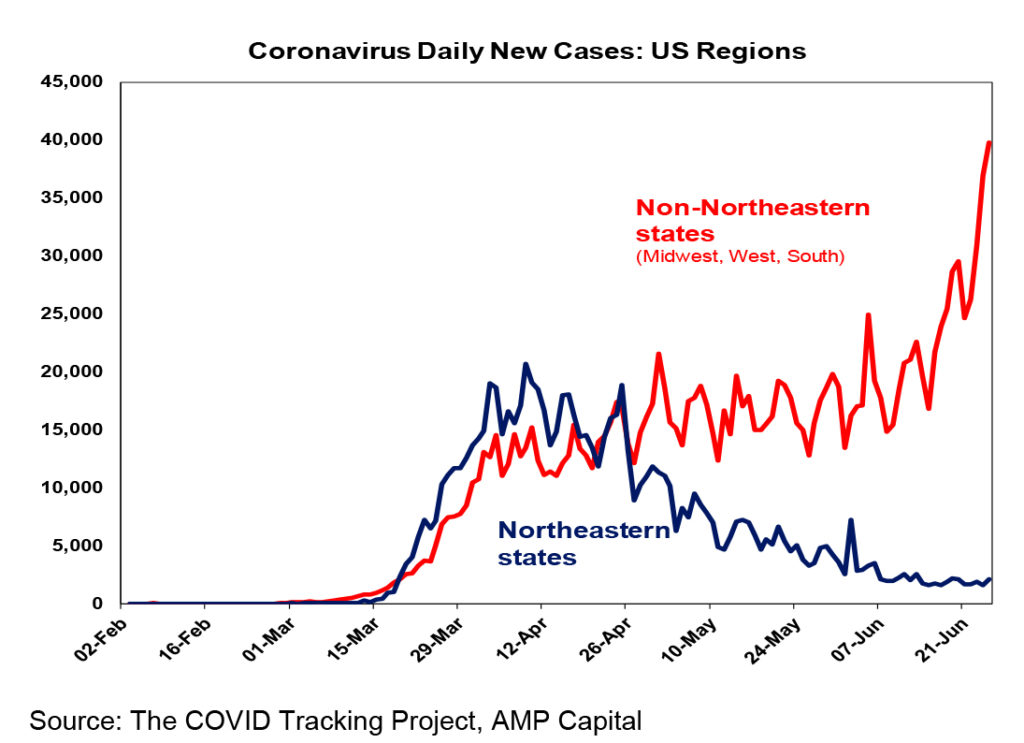

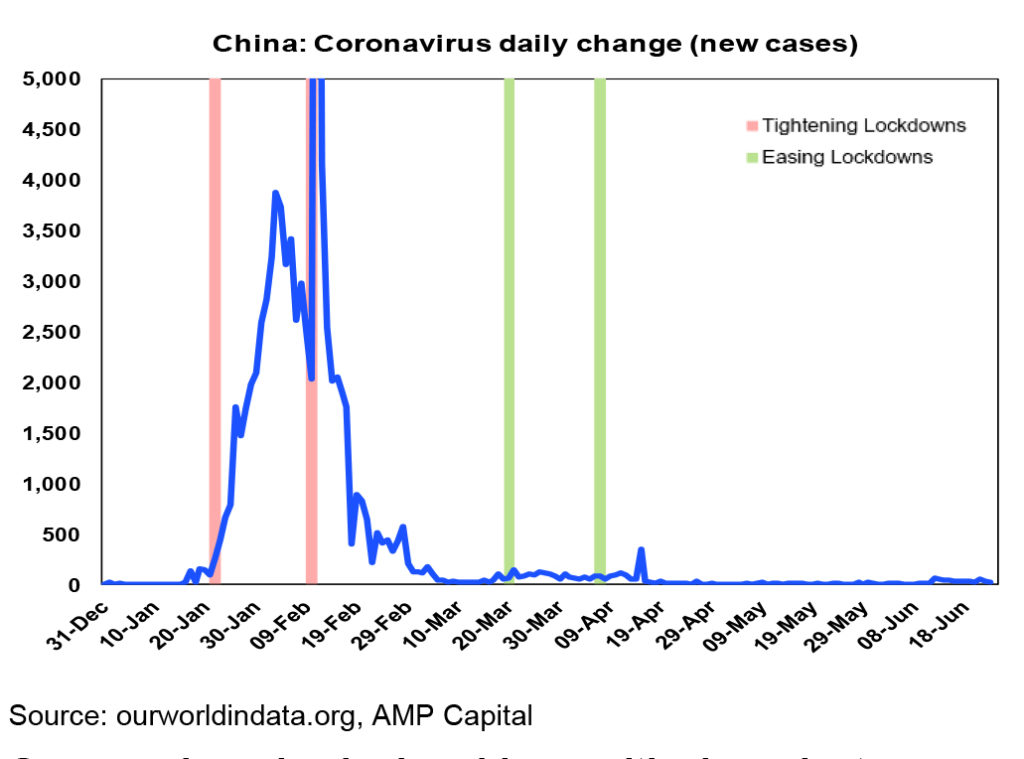

“Second wave” coronavirus fears have really escalated over the last week. The global trend in new cases remains up and this continues to be mainly driven by the emerging world. However, the big change is a renewed surge in new cases in developed countries due to the US.

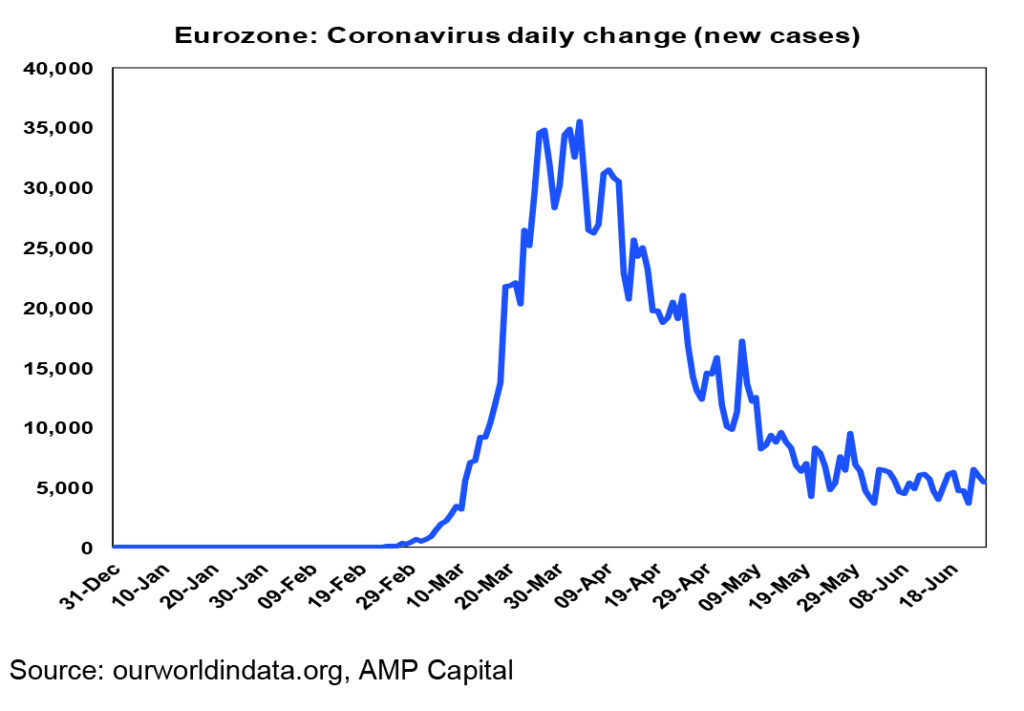

While the number of new cases in north eastern states (led by NY) remains down its been offset by a surge in cases mainly in the south and west (particularly in Texas, Arizona, Florida and California).

So far hospitalisations and deaths in the US remain well down from their highs earlier this year. This may partly reflect more young people being tested (due to a big increase in testing), better protections for older people and better management of new cases. All of which may mean that the latest wave of new cases may not be as deadly as that seen in the first wave. However, hospitalisations are starting to pick up in the south and the west with some states at risk of running out of capacity.

![]()

China appears to have limited the growth in new cases following the outbreak in Beijing (which was not due to imported salmon despite earlier speculation), albeit its still elevated compared to a few weeks ago.

Germany has also had problems with virus clusters (including around 1500 testing positive at a meatworks) although so far Eurozone new cases have continued to trend sideways, albeit at around 5000 a day.

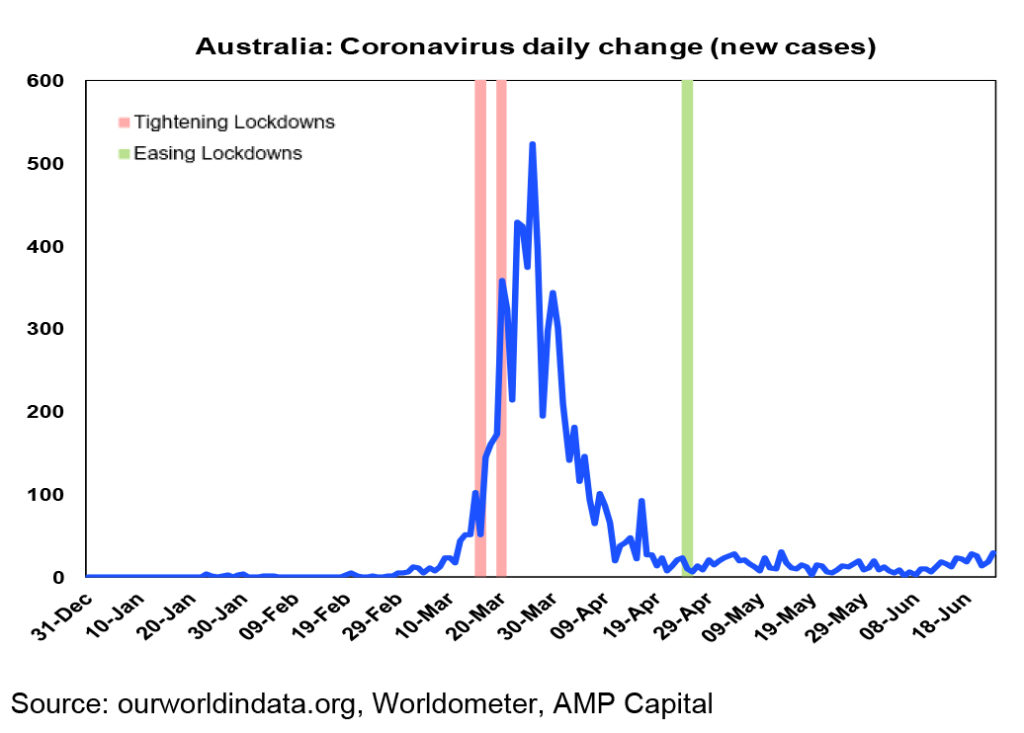

Finally, while Australia’s new case numbers remain relatively low they have continued to pick due mainly to various family related clusters in Victoria, raising concerns about a second wave in Australia.

This all begs the question as to whether we will see a reversal of the reopening that has occurred since April. I suspect that the hurdle to return to the severe “stay at home” lockdown is now immense: there is now significant shutdown fatigue and authorities may conclude that the economic cost of doing so is just too high. And don’t forget that the aim of curve flattening was to reduce the number of cases such that the medical system can cope and that has been more than achieved in Australia, NZ, much of Europe and much of the US but it’s now clear that in the absence of a vaccine its very hard to completely eliminate the virus. So we may just have to learn to live with it and manage outbreaks (as Korea, China and others have done over the last few months) with only partial and targeted lockdowns, travel restrictions (like those between Australian states and between some US states) and rigorous testing, tracking and quarantining and a renewed emphasis on social distancing such as limits on gatherings and possibly making masks compulsory while in public. Of course, if medical systems are overwhelmed then it’s a different story and a return to more severe lockdowns may become inevitable. Either way shares are in for a bit more volatility but if it’s the former then the pullback in shares seen over the last few weeks will remain just a correction with the rising trend likely to resume in the next few months as economic recovery continues.

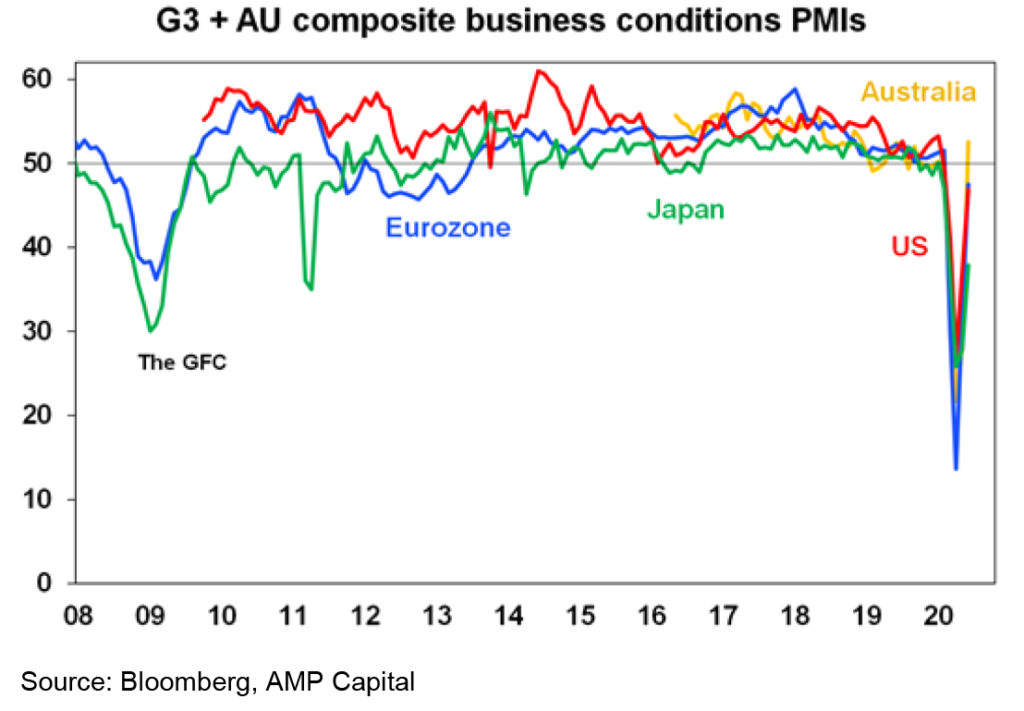

For the time being economic indicators continue to point to recovery. June business conditions PMIs for the US, the Eurozone, Japan and Australia rose sharply again and are now well up from their April low with the rebound looking very much like that seen in Japan. Bear in mind though that this does not mean that economic activity is now nearly back to normal, but it is consistent with it going in the right direction.

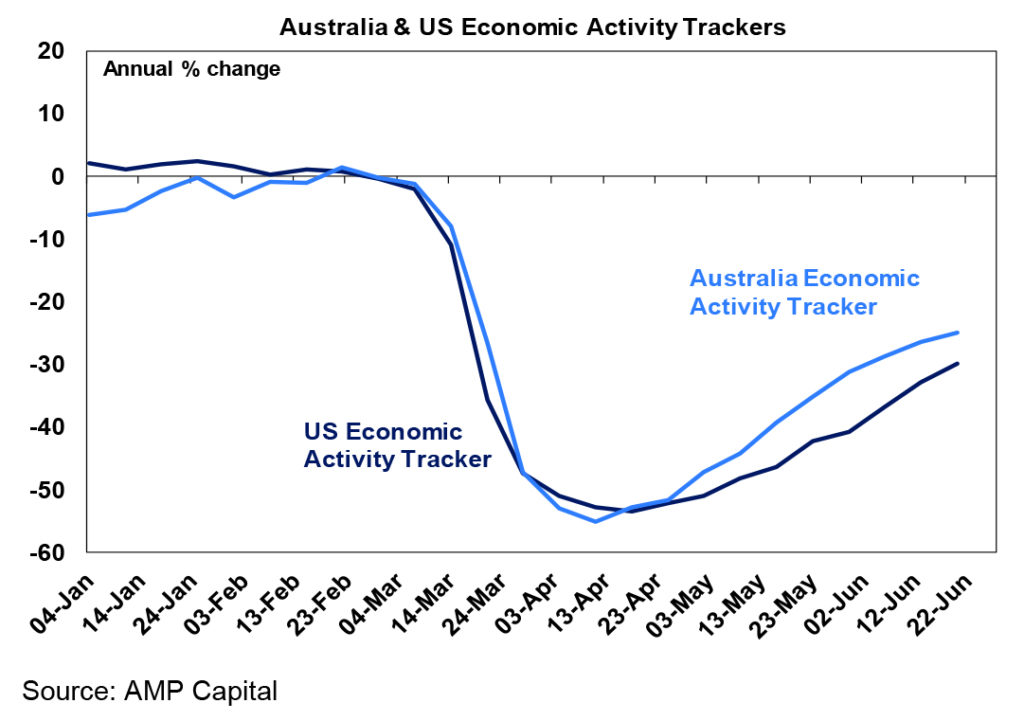

Our weekly economic activity trackers for the US and Australia based on high frequency data for things like restaurant bookings, confidence, retail foot traffic, box office takings, hotel bookings, credit card data, mobility indexes & jobs data are probably a better and more timely guide. They are telling us that economic activity is continuing to improve from its April low but they have still only recovered half the initial collapse in Australia and a bit less than that in the US. The Australian tracker is now up for 10 weeks in a row.

I suspect that the recovery going forward will be slower than the “Deep V” rebound seen so far in some recent data releases. First second wave fears will add a bit to consumer caution in terms of going out to restaurants and shopping. Second the easy gains from reopening including the unleashing of pent up demand may have already been seen but distancing requirements and travel restrictions mean that it will take a long time for some industries (like travel) to get back to normal. And even if there is a vaccine soon the coronavirus shock has accelerated the shift to a digital world and cost cutting associated with automation which is now likely occurring faster than new jobs are created all of which adds to a long tail of unemployment which will in turn constrain growth. Some call this a square root recovery, ie an initial Deep V rebound then slower growth. Obviously, it would be better than a W.

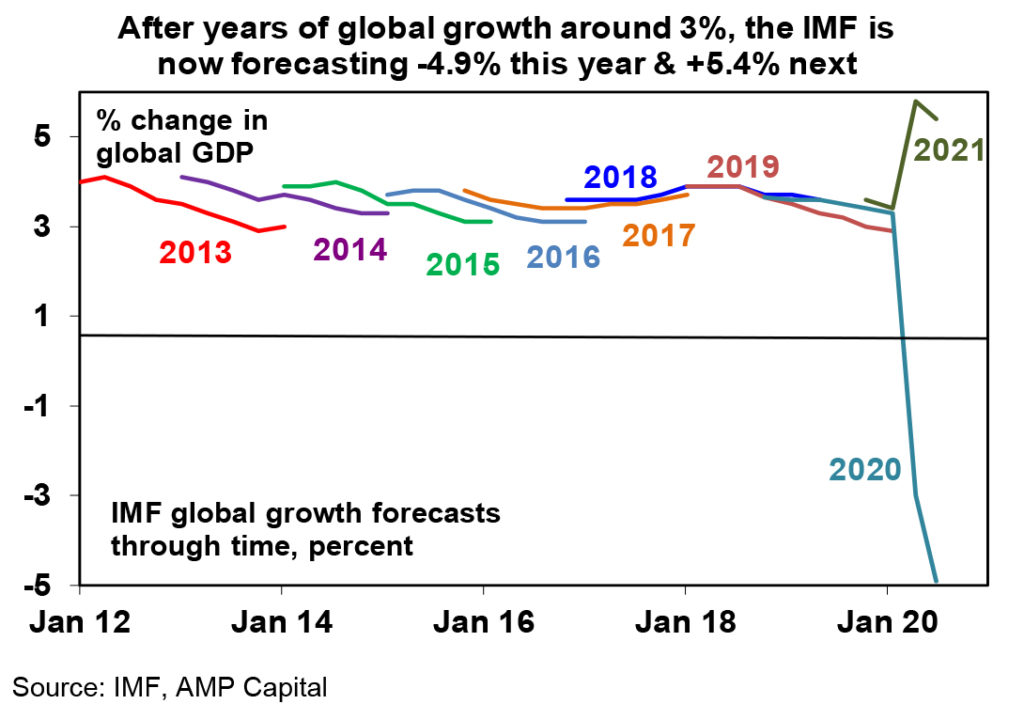

While the latest downgrade to the IMF’s global growth forecasts caused the usual excitement, it’s just catching up to market expectations. It’s forecast fall in global GDP for this year has been revised down to -4.9% (from -3%) and growth next year is forecast to rebound by 5.4% but its less negative than the OECD’s forecasts released two weeks ago and our own forecast for global growth to contract by -5.7% this year. Meanwhile, the IMF’s Australian growth forecast for this year was revised up from a too pessimistic -6.7% contraction to -4.5% which is similar to our own forecast.

It seems every week now there is some new geopolitical issue to worry markets and in the past week it was the US announcing it was considering tariffs on $3.1bn of imports from Europe. This flowed from a 15-year dispute about aircraft subsidies and was authorised by the WTO and $3.1bn is pretty trivial compared to total trade flows. However, the risk is one of retaliation by the EU (again possibly authorised by its own WTO action regarding aircraft subsidies) resulting in an escalation. And its consistent with Trump ramping up the pressure to show his base that he is strong on protecting American industry. Like China tensions its likely to remain an issue up until the election (and maybe beyond).

Major global economic events and implications

US business conditions PMIs rose nearly 10 points in June consistent with a rebound in regional business surveys, existing home sales fell but new home sales surged as did durable goods orders after a plunge in April. However, while jobless claims continue to fall the pace of decline has slowed and they remain very high suggesting a long tail of layoffs and unemployment likely to remain high for a while yet and that it may even have increased in June.

Eurozone business conditions PMIs surged nearly 15 points in June with similarly strong gains in French and German business confidence.

Japanese business conditions PMIs rose 10 points in June.

Australian economic events and implications

In Australia, business conditions PMIs rose a strong 24.5 points in June and are now above those for the US, Europe and Japan suggesting a stronger recovery in Australia.

While ABS job vacancy data fell sharply over the three months to May, Seek job ads have picked up since then. Preliminary goods trade data showed a sharper fall in imports than exports in May with iron ore exports remaining strong suggesting that the trade surplus remains large and that net exports continued to provide a positive contribution to growth in the June quarter.

Meanwhile, the announcement of various job losses including at Qantas provides a reminder that its going to be a long time before unemployment comes back down to around 5%. And in the very short term with JobSeeker seeing the return of some “mutual obligation requirements” this month unemployment could spike higher as some of the 600,000 or so people who have left the jobs market since March are forced to return and look for a job. If they all return unemployment would spike to around 11%. All of which highlights the need for some sort of support measures to continue beyond the September end point for JobKeeper and for an economic reform agenda to help boost long term growth and job creation.

Australian Government budget data for May is running around $60bn worse for the financial year to date than what was expected in last December’s MYEFO. About half of this is due to the stimulus boost to spending and around half reflects the weaker economy hitting revenue, particularly corporate tax. Its consistent with a significant blow out in the budget deficit this financial year to around $100bn (even allowing for the saving on JobKeeper).

What to watch over the next week?

Trends in new coronavirus cases will continue to be watched closely, particularly in US states which are seeing rising trends, but also in China and Victoria.

In the US, the main focus is likely to be on jobs data for June to be released Thursday which are expected to show a further 3 million rebound in jobs and a further fall in the unemployment rate to 12.5% as furloughed workers return to work following the reopening of the economy. Other data is expected to show a rebound in pending home sales (Monday), an increase in consumer confidence (Tuesday) and a rise in the June ISM manufacturing conditions index (Wednesday) consistent with PMIs. The minutes from the Fed’s last meeting (Wednesday) are likely to remain dovish.

Eurozone economic confidence data for June (Monday) is expected to show a rebound consistent with the upswing in business conditions PMIs. Meanwhile, core inflation for June (Tuesday) is likely to have remained weak and unemployment in May (Thursday) is likely to have increased.

Japanese jobs data for May is likely to remain weak but industrial production may show some recovery (with both due Tuesday). The Tankan business survey for the June quarter (Thursday) is likely to show a sharp deterioration in conditions.

Chinese business conditions PMIs for June (Tuesday and Wednesday) are expected to be little changed.

In Australia, expect credit growth to remain soft and the ABS’ payroll and wages survey for mid June is likely to show an improvement consistent with reopening (both due Tuesday), CoreLogic home price data for June is likely to show a further 0.7% decline in home prices and building approvals for May are likely to fall 8% (both due Wednesday), the trade surplus (Thursday) is likely to have remained large and final retail sales data for May (Friday) are likely to confirm something like the 16.3% or so rebound already reported for preliminary data by the ABS.

Outlook for investment markets

After a strong rally from March lows shares remain vulnerable to short term setbacks given uncertainties around coronavirus, economic recovery and US/China tensions. But on a 6 to 12-month horizon shares are expected to see good total returns helped by a pick-up in economic activity and massive policy stimulus.

Low starting point yields are likely to result in low returns from bonds once the dust settles from coronavirus.

Unlisted commercial property and infrastructure are ultimately likely to continue benefitting from a resumption of the search for yield but the hit to economic activity and hence rents from the virus will weigh heavily on near term returns.

The Australian housing market has slowed in response to coronavirus. Home prices are falling and higher unemployment, a stop to immigration and rent holidays pose a major threat to property prices into next year. While government policies to support jobs and incomes and the bank payment holiday out to September have headed off the risk of a 20% plus fall in prices, they are still expected to fall by around 5 to 10% into next year.

Cash & bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.25%.

Although the Australian dollar is vulnerable to bouts of uncertainty about the global recovery and US/China tensions, a continuing rising trend is likely if the threat from coronavirus continues to recede. Particularly with the US expanding its money supply far more than Australia is via quantitative easing and with China’s earlier recovery supporting demand for Australian raw materials (assuming political tensions between Australia and China are kept to a minimum).

By Shane Oliver