Weekly market update – week ending 31 July, 2020

Investment markets and key developments over the past week

Share markets were mixed over the last week with Chinese shares up solidly and US shares rising slightly on the back of good earnings results, particularly for tech stocks, but Eurozone, Japanese and Australian shares fell on uncertainty regarding the economic outlook. Australian shares were dragged lower by sharp falls in energy, financial, health, property and utility stocks. Bond yields generally fell again. Oil prices fell but metals and iron ore rose and gold rose to a new record high as the US dollar fell further. The falling $US also saw the $A rise above $US0.72.

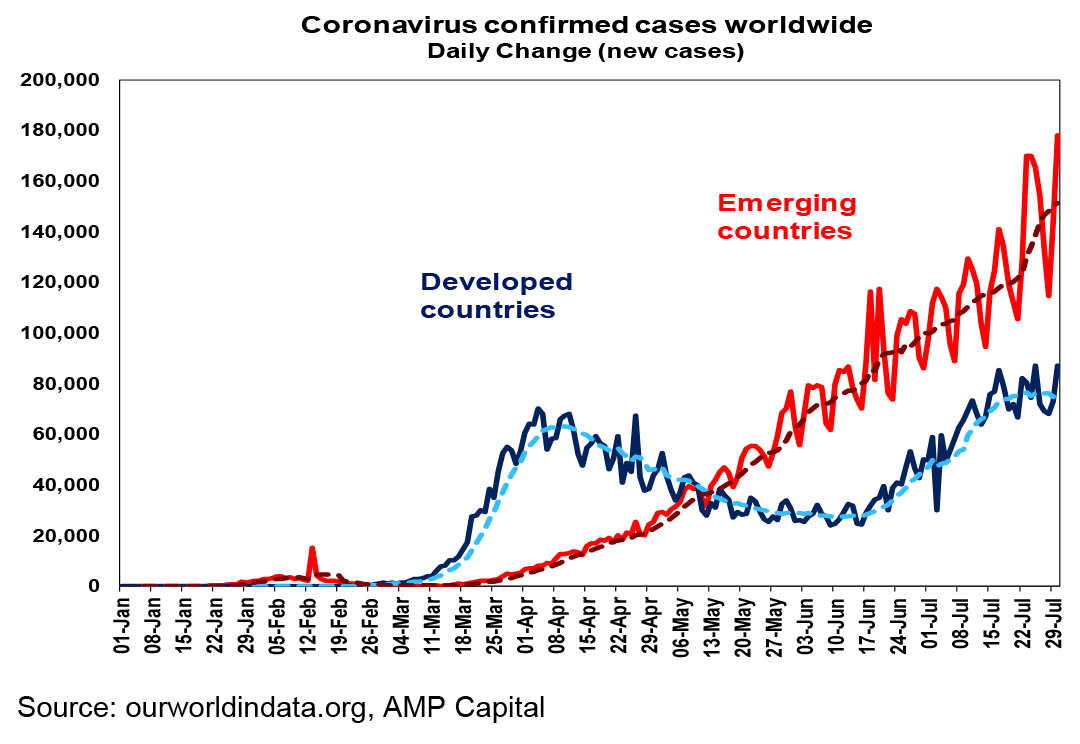

The rising trend in new coronavirus cases globally still shows no let up. This is primarily driven by emerging countries, with developed countries showing some signs of stabilisation over the last few weeks.

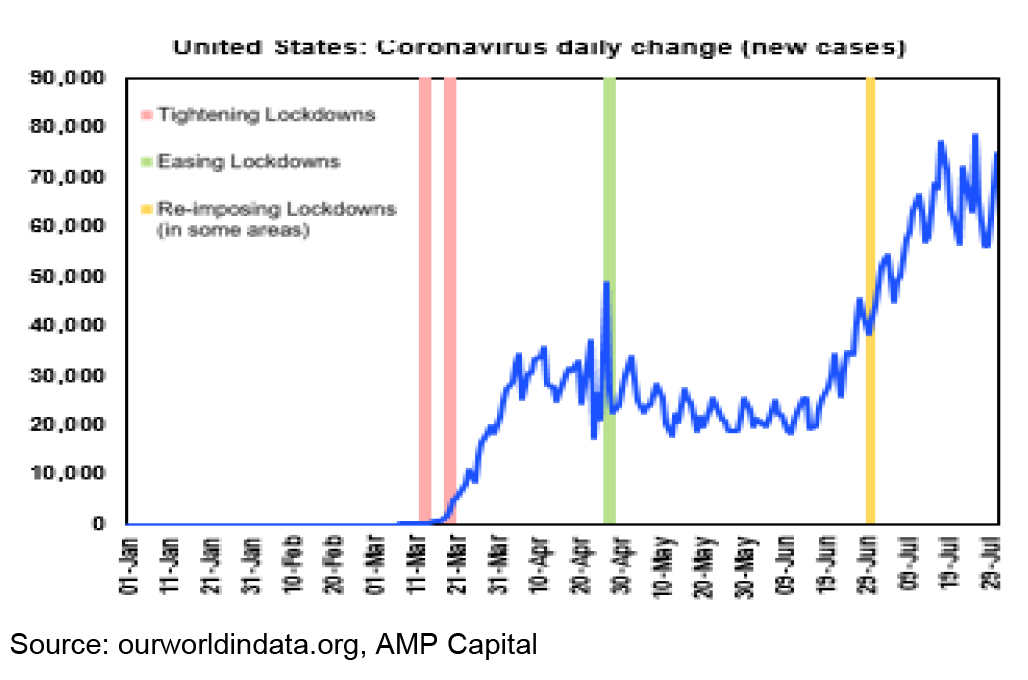

The stabilisation in new cases in developed countries reflects some slowing in the US – notably in southern and western states, suggesting that the return of some restrictions and the mandated use of masks in many states may be working.

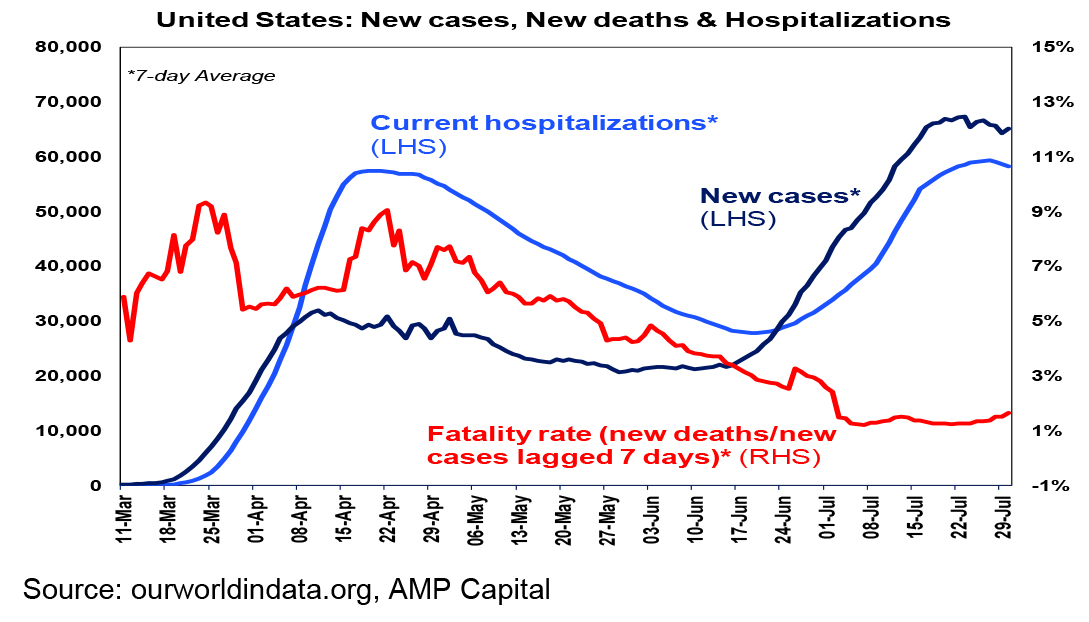

The US is also seeing hospitalisations roll over and the fatality rate is around 1.5% compared to around 7% during the first wave in April. This is consistent with a greater skew in new cases towards younger people, better protections for older people and better treatments. And it adds to confidence that a generalised lockdown will be avoided.

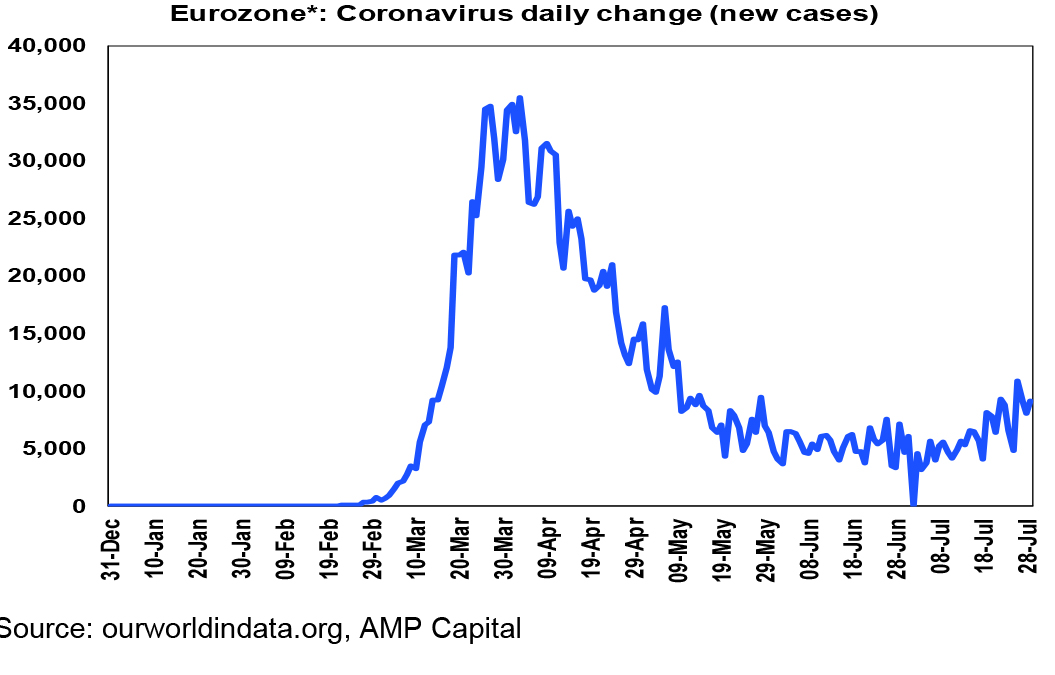

Against this Europe is seeing new cases edge up again, as is Canada, and Japan has seen a big rise. Even China has seen a pick-up in new cases (albeit it remains very low).

All of this highlights how hard it is to contain coronavirus and the importance of maintaining social distancing.

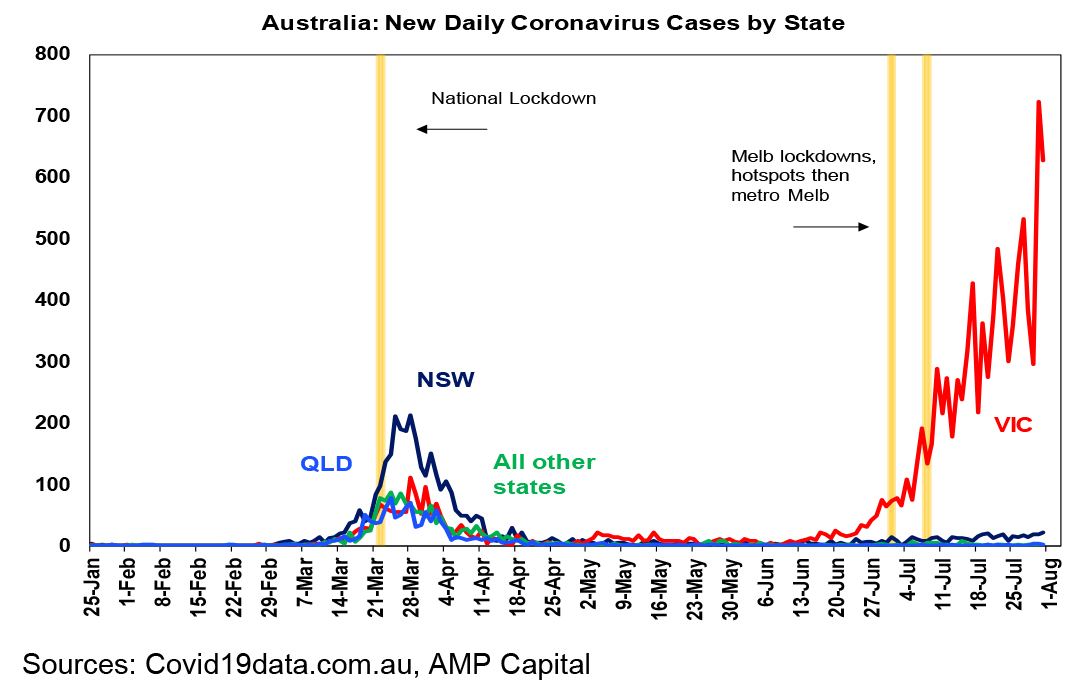

Unfortunately, Victoria in Australia is also still struggling to put a lid on new cases with a continuing uptrend. So far so good in NSW – although the 7-day rolling average case count is trending up and the risk of a break higher is significant.

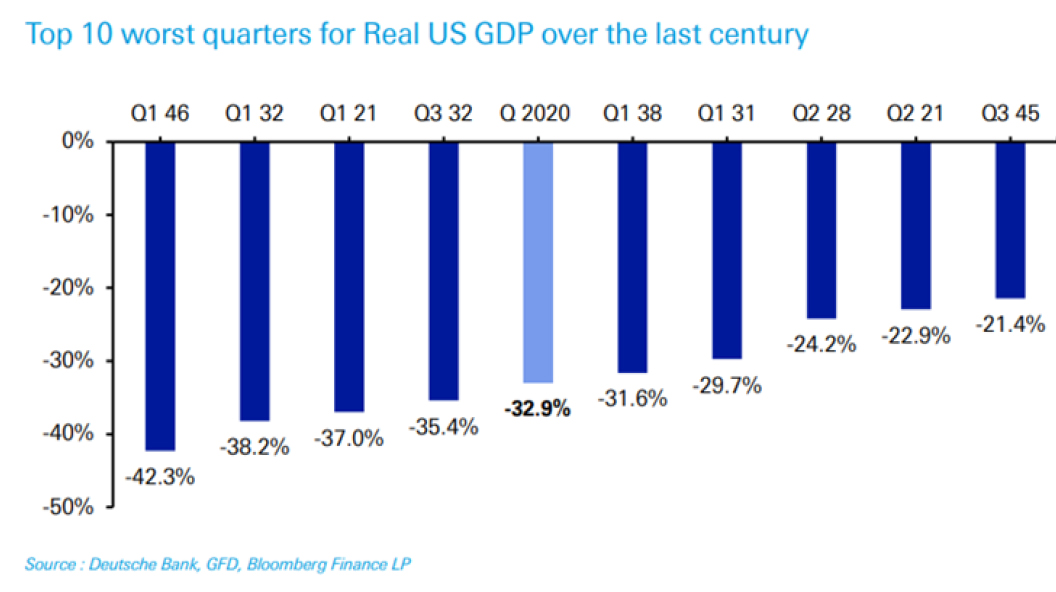

Meanwhile, June quarter GDP data for the US and Germany confirmed a huge hit from coronavirus shutdowns. US GDP plunged 9.5% quarter on quarter (or by -32.9% annualised) and German GDP fell 10.1% quarter on quarter with the falls being broad based. For the US this is the steepest decline since the March quarter 1946 (see chart which compares annualised declines) and for Germany its the worst since 1970.

Naturally for the US (and Australia as it too will also report a big fall when June quarter GDP data is released in a month) this is seeing comparisons to the Great Depression come up again – but there are big differences: first, there was no period of prior excess like the “roaring twenties” that needs to be unwound; second, the current slump was brought on by government decisions to lockdown society as opposed to being a cyclical economic downturn that has to run its course; and thirdly, the current period has seen rapid and massive monetary and fiscal stimulus whereas the 1930s initially saw the opposite. All of which should mean a faster recovery once the virus is controlled. The US and German June quarter GDP slump was also largely as expected back in late March/early April, so is already factored into our global and Australian GDP forecasts. And its old news to the extent that the low was probably in April and since then economic activity has started to recover with “reopening”. The bad news is that the recovery will be slow after the initial bounce and its threatened by ongoing surges in coronavirus cases and this is evident in a rise in jobless claims in the US over the last two weeks.

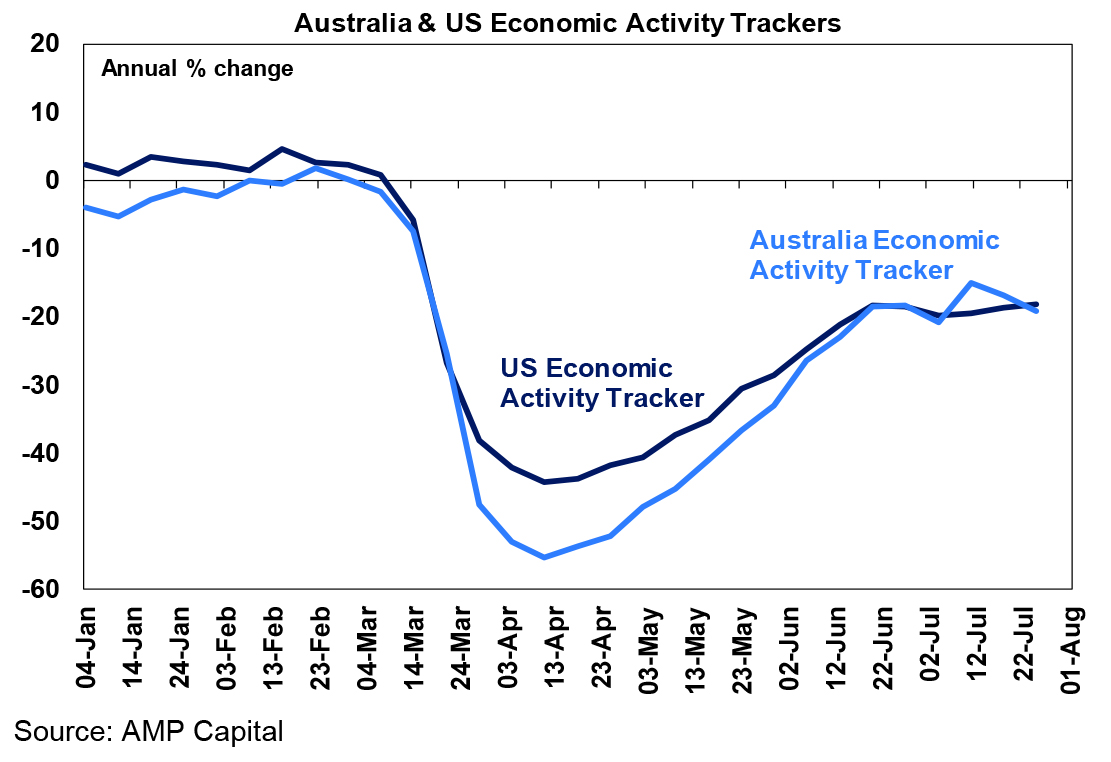

The resurgence in new cases, the reversal of reopenings and the associated negative headlines are continuing to impact our weekly Economic Activity Trackers for the US and Australia, but so far it’s just seen the recovery stall since the second half of June as opposed to collapse. These activity trackers are based on high frequency data for things like restaurant bookings, confidence, retail foot traffic, box office takings, hotel bookings, credit card data, mobility indexes & jobs data. Our Australian Economic Activity Tracker fell back again over the last week reflecting weakness in consumer confidence, restaurants, job ads, credit card data, mobility, hotel bookings and retail traffic. Victoria appears to be the main driver of the weakness.

The Fed remained in dovish, “whatever it takes” mode over the last week. While it left monetary policy on hold as expected, the clear message from Fed Chair Powell is that the Fed is ready to stay accommodative for a very long time. Meanwhile, the Fed’s policy review is likely to be complete by September and is expected to see a move to a 2% inflation averaging strategy which will imply a desire to overshoot the target after a period of undershooting. The Fed is also likely to move to outcome based forward guidance and more definitive QE. All of which are very dovish.

The negatives for shares remain: rising new coronavirus cases, the pausing or reversal of reopening, very high unemployment, the hit to earnings, the US election, US/China tensions and we are now in a seasonally weak period of the year for shares. But these are arguably more than offset by a long list of positives including continuing good news on coronavirus treatments and vaccines, the second wave in the US being less deadly than the first, several countries showing that it is possible to contain the virus, China tracing out a Deep V recovery, the safe haven $US is falling which is normally a positive sign, monetary and fiscal policy remains ultra-easy, low interest rates and bond yields make shares look cheap and there is a lot of cash on the sidelines. Shares are still vulnerable to further volatility, with renewed lockdowns and US/China tensions being the main risks. But the positives should keep any volatility to being a correction in a still rising trend.

Should we worry about the rise in the gold price to a record high signalling some sort of flight to safety that we should all jump on to. The short answer is no. The rise of gold partly reflects a desire by some for a hedge against quantitative easing causing a surge in inflation and a collapse in the real value of paper currencies. But it also reflects an emerging cyclical decline in the value of the US dollar versus other currencies, which is normally a good thing because it means that safe haven demand for it is falling and global reflation may be working, and a collapse in interest rates which makes it cheaper to hold gold but also makes it cheaper to hold other assets. And just as gold has gone up so have other commodities with oil having more than doubled since April and metal prices up nearly 30% from March lows and again this is normally a positive sign for global growth. Finally, while I think there is probably more upside for the gold price (albeit not in a straight line) it should be noted that it produces no income, is highly volatile and someone who bought into gold the last time everyone got excited back in 2011 has only now just broken into profit after suffering a near 50% plunge in value into 2015 – so it’s not always a safe haven. Of course, back then the much-feared surge in inflation on the back of post GFC QE failed to eventuate and it may take a while to eventuate in the years ahead as well given such high levels of unemployment.

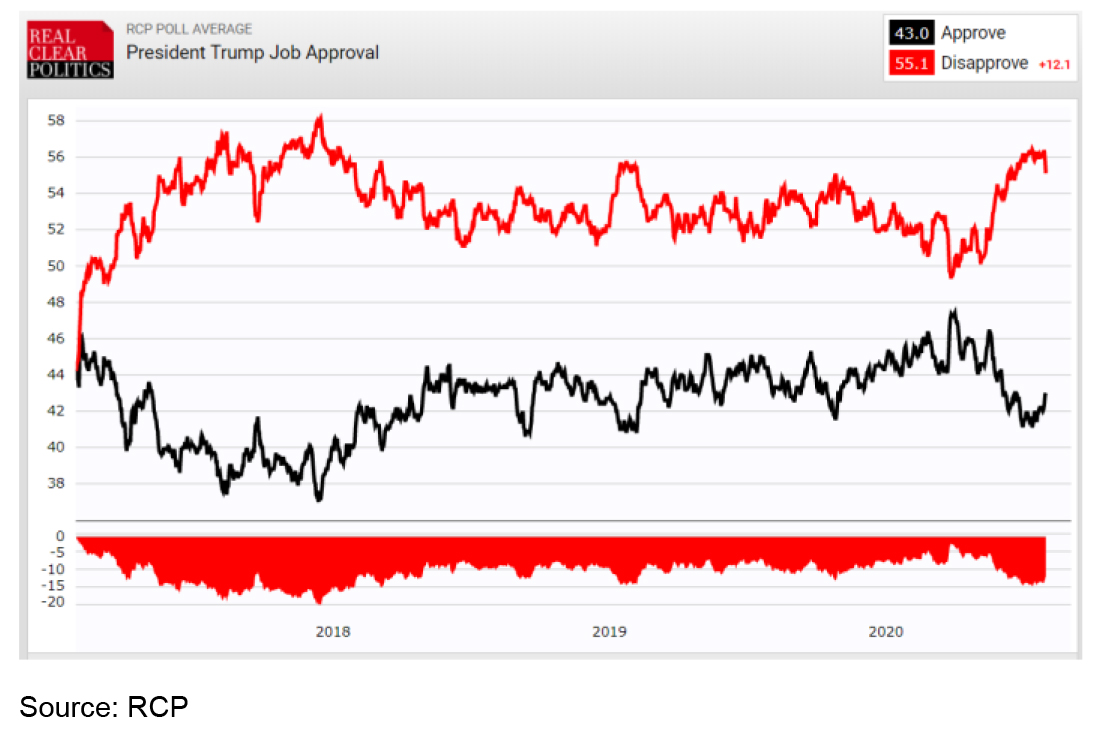

Is President Trump setting up a challenge to the election result if it goes against him and is close? For a while now he has been claiming that mail in voting leads to fraud and he has now suggested that the election should be postponed due to the pandemic. While he does not have the authority to postpone the election – that’s with Congress and both Republicans and Democrats have said no – he may be laying the ground for a challenge to the result if it goes against him. If so, this could make the 2000 election controversy look like a non-event. Trump’s comments on this may suggest he is not feeling that confident about the election – although out of interest his approval has gone up a bit in the last few weeks.

Ever since Light Years I have been a glued on Kylie fan and she keeps churning out great songs, including her latest Say Something, which marks a return to electropop after the country pop Golden. More nice head candy.

Lots of entertaining Bachelor in Paradise over the last week – bit sad to see both Helena and Jamie go though!

Major global economic events and implications

US June quarter GDP data showed a -9.5% hit to GDP (or -32.9% annualised). Thanks to the earlier than expected reopening it was a bit less bad than had been expected several months ago and based on our US Economic Activity Tracker the low point was probably in April so it’s also rather old news. More current US data was mostly better with strong gains in durable goods orders for June, a strong rise in pending home sales and a further recovery in several regional manufacturing indexes for July but flat house prices in May. However, a fall back in consumer confidence in July and a second weakly rise in jobless claims highlights that the resurgence in coronavirus is threatening the recovery.

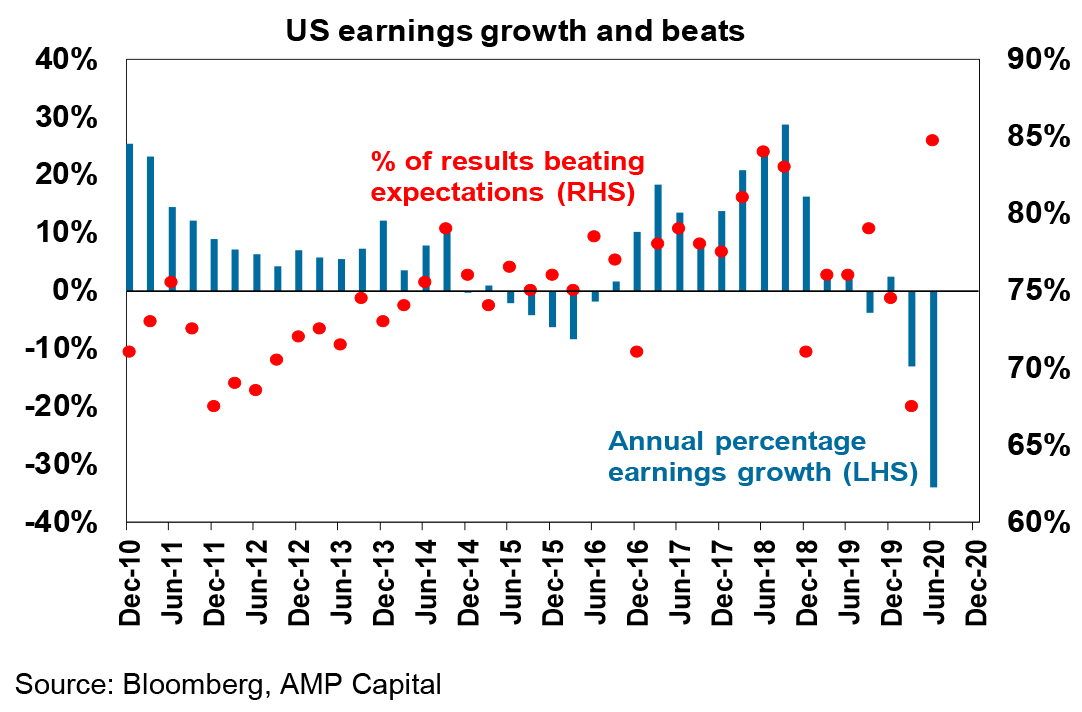

So far around 60% of US S&P 500 companies have reported June quarter earnings and results have remained better than expected with a bigger than average 85% beating on earnings by an average 22.7% and 67% beating on sales. This has seen significant upwards revision to consensus earnings expectations, with earnings now expected to fall -34%yoy in the June quarter compared to -44% a few weeks ago.

German June quarter GDP fell 10.1% in the June quarter and Eurozone unemployment rose to 7.8% in June. Against this the German IFO business conditions index rose further in July as did Eurozone economic sentiment pointing to a strong initial rebound in growth and bank lending to corporates was strong, albeit it was soft to households.

Japanese retail sales rebounded sharply in June, industrial production rose more than expected and unemployment fell slightly. However, the ratio of job openings to applications fell to the lowest since 2014 and the resurgence of coronavirus cases this month in Japan will weigh.

Chinese business conditions PMIs remained solid in July with the composite PMI falling just 0.1pt to 54.1, suggesting that the economic recovery is continuing.

Australian economic events and implications

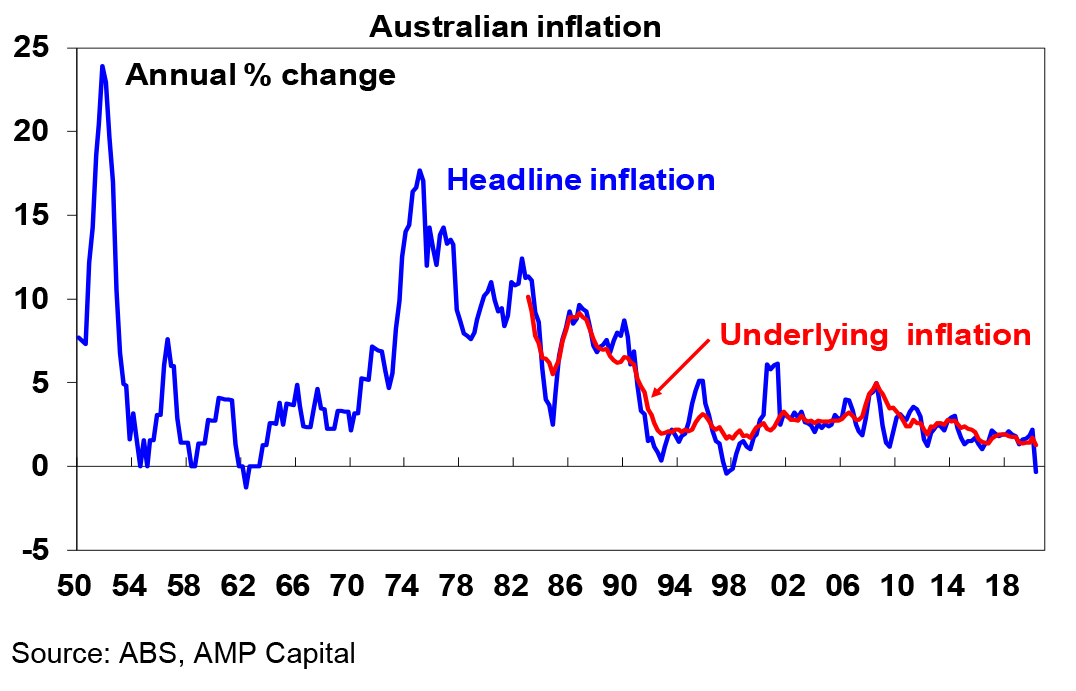

Australia saw its biggest quarterly bout of deflation in the 72-year history of the CPI and its biggest annual decline since 1997 – expect a rebound in the current quarter but underlying inflation is likely to remain weak. The -1.9% plunge in the CPI was basically due to government decisions to provide childcare, pre-school (in some states) and before and after school care for free and a plunge in petrol prices. With free childcare having ended and petrol prices back up the CPI is expected to rebound this quarter (probably by around 1.5%qoq). So it’s best to focus on underlying inflation as it excludes the volatile, often government related, moves in some components. Underlying inflation fell to just 1.25% year on year which is its lowest on record and reflects the plunge in demand in the economy and huge amounts of spare capacity. With spare capacity likely to be with us for some time to come expect underlying inflation and the trend in headline inflation to remain weak notwithstanding volatility driven by government decisions and changes in petrol prices.

Australian economic data was on the soft side with payroll jobs falling over the three weeks to mid-July, particularly in Victoria (although this data has a tendency to get revised up), the terms of trade falling slightly in the June quarter (although after a huge surge in the March quarter), private sector credit contracting further in June and home building approvals plunging again. Fortunately, approvals for alternations and non-residential building rose and the HomeBuilder scheme along with increased stamp duty concessions for first home buyers of new property should provide some support for home building. Meanwhile, the July ABS Business Impacts of Covid survey found 42% receiving some form of government assistance but found more businesses expect to raise headcount than cut it.

What to watch over the next week?

Trends in new coronavirus cases along with pressure on medical systems will continue to be watched closely, particularly in the US and Victoria.

In the US, jobs data (due Friday) will be the focus with market expectations for the return of another 1.6 million payrolls jobs and unemployment to fall to 10.5%, but a renewed weakness in jobless claims on the back of the resurgence in coronavirus cases raising the risk of disappointment. In terms of other data, expect the July manufacturing conditions ISM (Monday) to show a further improvement to 53.5 consistent with regional manufacturing surveys and the non-manufacturing conditions ISM (Wednesday) to fall back slightly to 55. US June quarter earnings results will continue to flow.

In China, the Caixin manufacturing PMI (Monday) is expected to hold around 51.2 and trade data (Friday) is expected to show a further recovery in import growth but softness in exports.

In Australia, the RBA is expected to leave monetary policy on hold for the fifth month in a row on Tuesday and will release its quarterly Statement on Monetary Policy on Friday. Having provided massive monetary stimulus back in March the RBA is still in “watch and wait” mode, and the policy focus now remains largely on fiscal policy. The RBA is unlikely to make any major changes to its economic growth forecasts but it may lower its underlying inflation forecasts given June quarter underlying inflation came in lower than it expected and it will continue to emphasise the uncertainty surrounding the outlook. Its views on the further rise in the value of the Australian dollar will also be watched although its unlikely to be too concerned as its still around fair value and its rise is consistent with higher commodity prices. Against this backdrop and given the risks flowing from Melbourne’s renewed lockdown, the RBA is likely to reiterate its dovish forward guidance on rates and note that it stands ready to do more if needed. In terms what it might do if it does ease further in the months ahead it has all but ruled out negative interest rates, foreign exchange intervention and the direct monetary financing of government spending, but sees still lower but positive interest rates and the purchase of more government bonds as possible options. A rate cut to 0.1% would hardly be worth the effort which leaves more QE as the main tool for any further easing. Meanwhile, rate hikes are at least three years away.

On the data front in Australia, expect CoreLogic home price data for July (Monday) to show a further -0.8% decline in average dwelling prices, June retail sales to show a 2.4% gain consistent with preliminary data already released resulting in a -3.3% decline in real June quarter retail sales and the trade surplus for June to remain strong at around $8bn (all due Tuesday), June housing finance data (Wednesday) to show a 2% rise after a huge fall in May.

The Australian June half profit reporting season will also start to get underway but with only a handful of companies due to report including Resmed (Thursday), IAG, News Corp and REA (Friday). It’s going to be the worst reporting season in years with consensus expectations for a -20.5% slump in earnings due to the hit from coronavirus which will be the biggest fall since the GFC. Financials will be the hardest hit with an expected -27% slump in earnings led by insurers and the banks, followed by industrials with a -15% fall in earnings and resources with -13%. Health care may be the only sector to see a rise in earnings (and even that’s iffy).

Outlook for investment markets

After a strong rally from March lows shares remain vulnerable to short term setbacks given uncertainties around coronavirus, economic recovery and US/China tensions. But on a 6 to 12-month horizon shares are expected to see good total returns helped by a pick-up in economic activity and policy stimulus.

Low starting point yields are likely to result in low returns from bonds once the dust settles from coronavirus.

Unlisted commercial property and infrastructure are ultimately likely to continue benefitting from a resumption of the search for yield but the hit to economic activity and hence rents from the virus will weigh heavily on near term returns.

Australian home prices are falling and higher unemployment, a stop to immigration and rent holidays will push prices lower into next year. Home prices are expected to fall by around 5 to 10% into next year from this year’s highs, with the risk of bigger falls if the renewed rise in coronavirus cases leads to a renewed generalised lockdown. Melbourne is particularly at risk on this front as its renewed lockdown pushes more businesses and households to the brink.

Cash & bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.25%.

Although the Australian dollar is vulnerable to bouts of uncertainty about coronavirus, the economic recovery and US/China tensions, a continuing rising trend is likely. Particularly with the US expanding its money supply far more than Australia is via quantitative easing and with China’s earlier recovery supporting demand for Australian raw materials (assuming political tensions between Australia and China are kept to a minimum).

By Shane Oliver