Weekly market update – week ending 25 September, 2020

Investment markets and key developments over the past week

Global share markets fell again over the last week on concerns about rising coronavirus cases, tightening social distancing restrictions in Europe and the lack of progress towards additional fiscal stimulus in the US. Australian shares managed a decent gain through the week with banks boosted by the Government moving to relax the responsible lending laws and strong gains in health, utility, industrial and consumer shares. Reflecting the risk off tone globally bond yields, commodity prices and the $A fell as the $US rose.

The correction in equity markets has now seen US shares fall 10% from their high, the tech heavy Nasdaq pullback 12%, and Eurozone and Australian shares have seen about a 6% decline to their lows. We remain of the view that it’s just a correction after an excessive run up in US shares and not the start of a renewed bear market and that a continued but gradual and messy recovery along with ultra-easy monetary policy will underpin a rising trend in shares on a 6-12 month horizon, providing coronavirus is controlled. But it remains too early to say the correction is over – seasonal weakness often continues into October, coronavirus could worsen into the northern winter, the next round of US fiscal stimulus remains uncertain and the US election is likely to add to volatility.

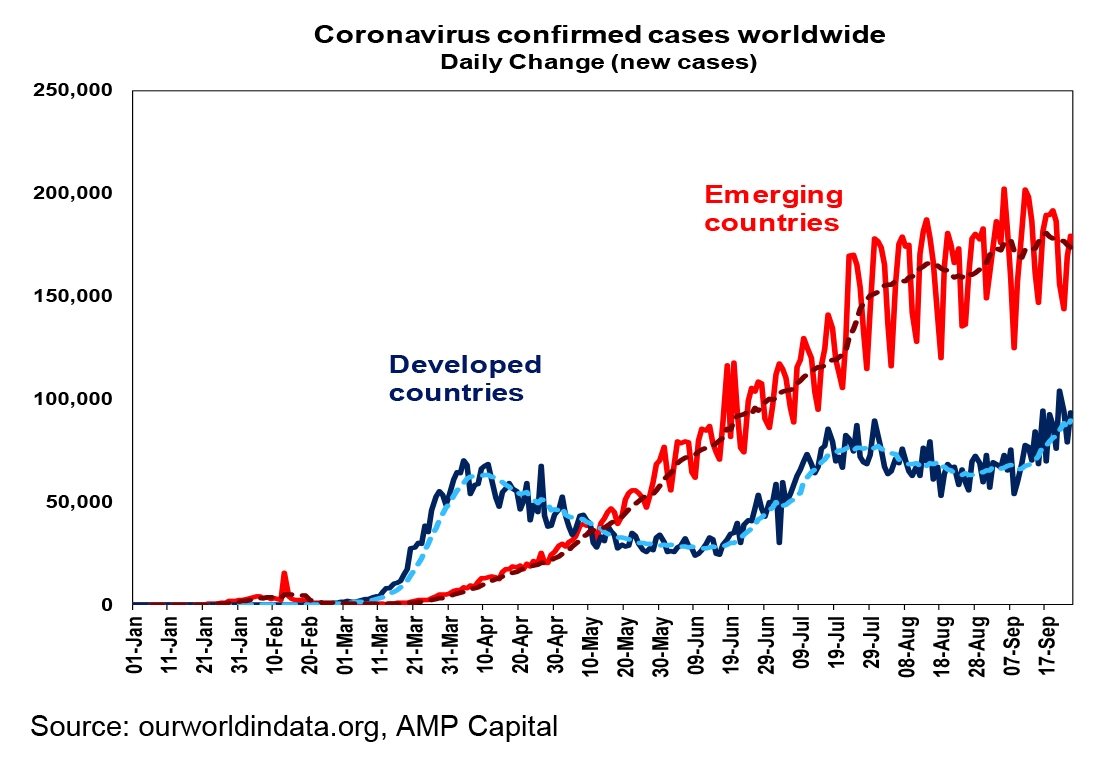

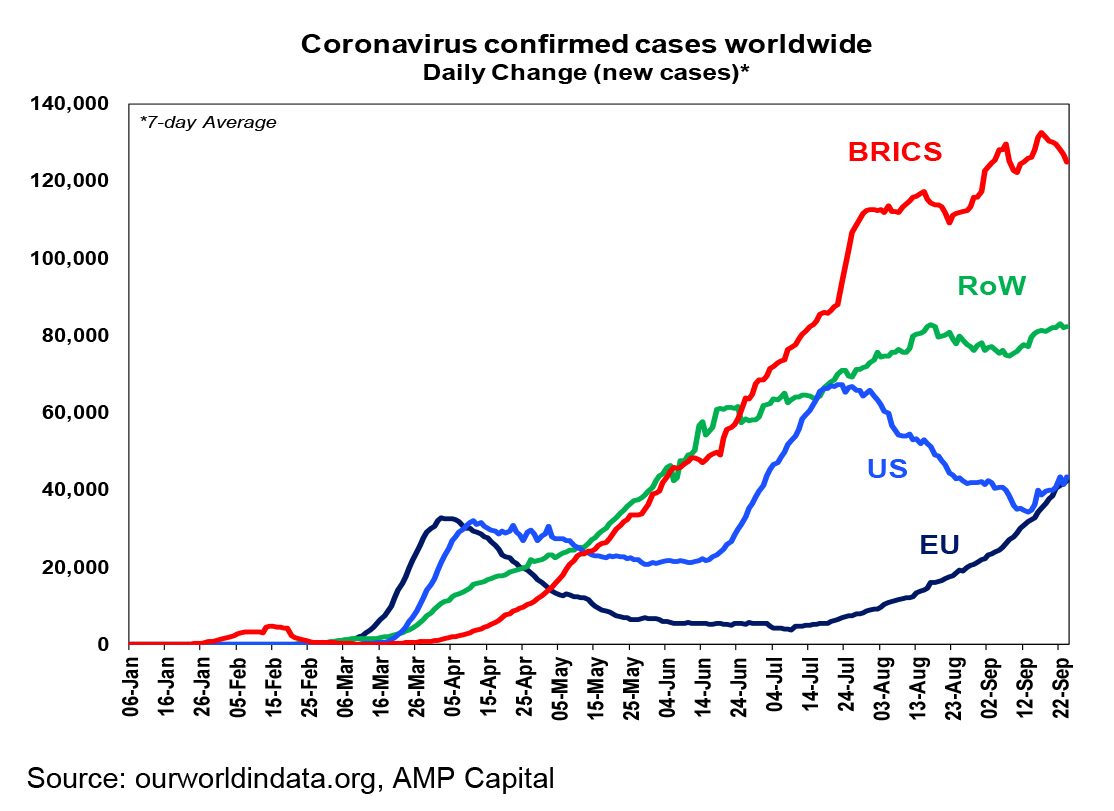

The past week or so has seen the trend in new coronavirus cases continue to rise particularly in developed countries

A continuing strong surge in Europe is the main driver but the UK and Canada are also rising solidly, and the US has hooked back up (particularly in the south).

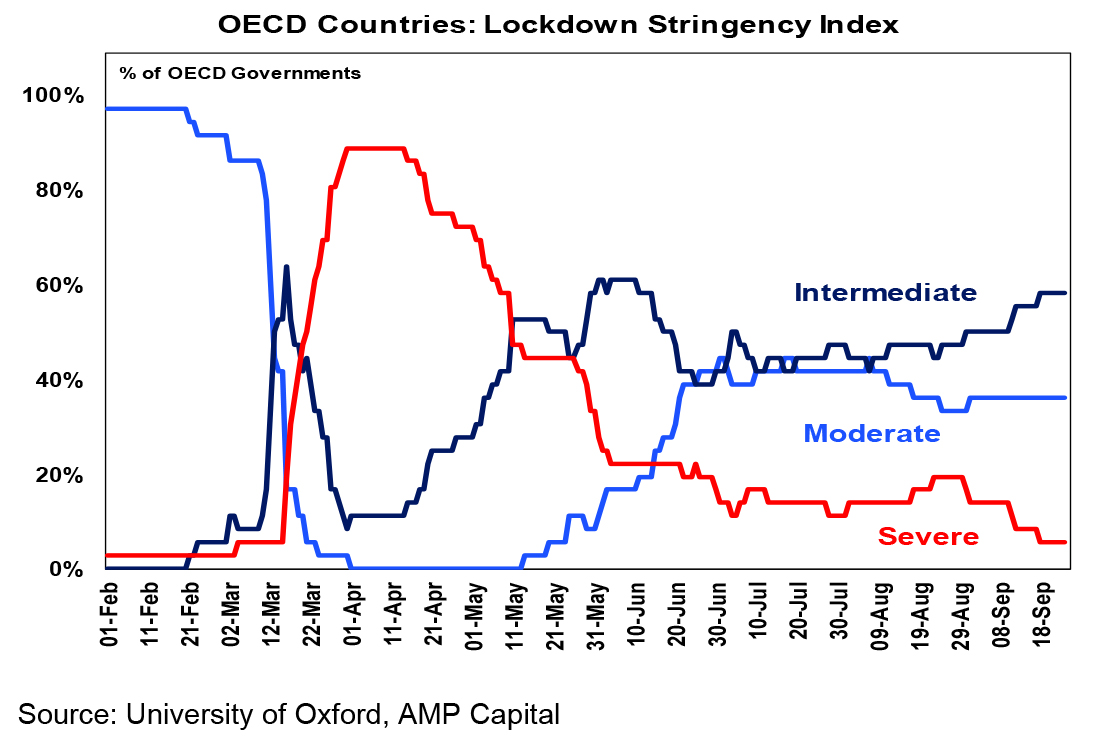

This has seen various countries – eg the UK and France – tighten some restrictions around bars, restaurants and public gatherings, resulting in a rising proportion of countries in “intermediate lockdowns”. See the next chart.

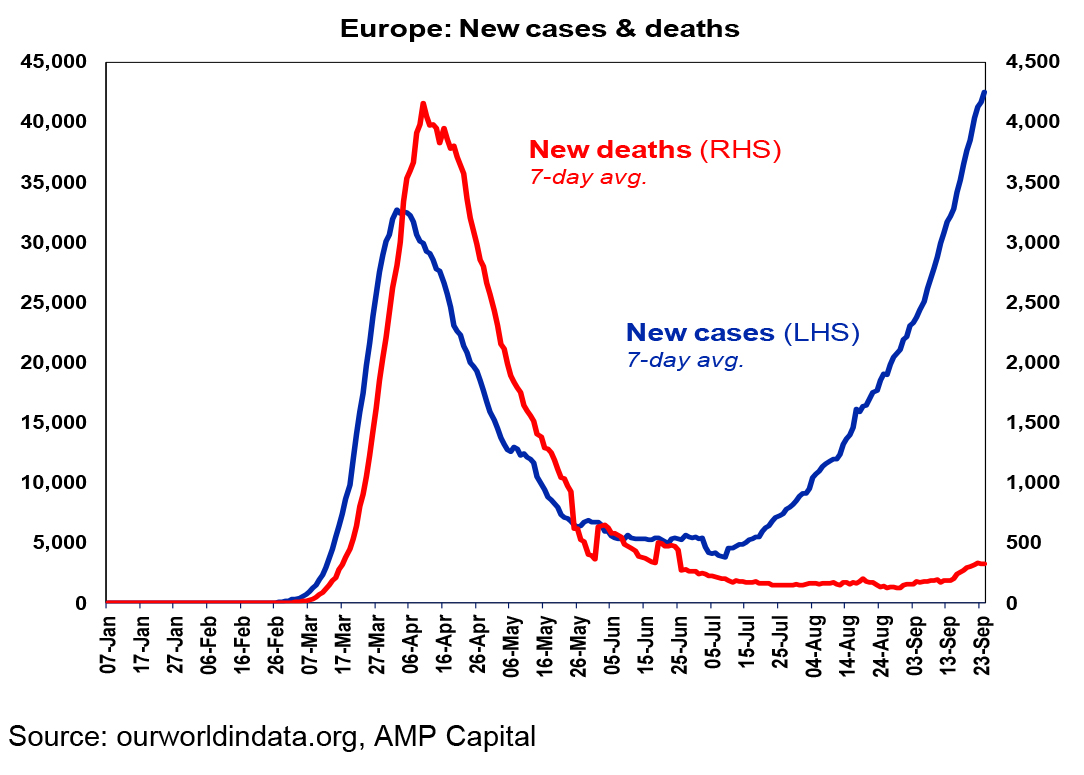

Fortunately, the number of deaths remains well down on what was seen earlier this year across developed countries. See the next chart for Europe. This in turn should hopefully help avoid a return to generalised lockdowns in most countries – in favour of targeted measures – and help confidence hold up. Of course, the risk is high going into the northern winter.

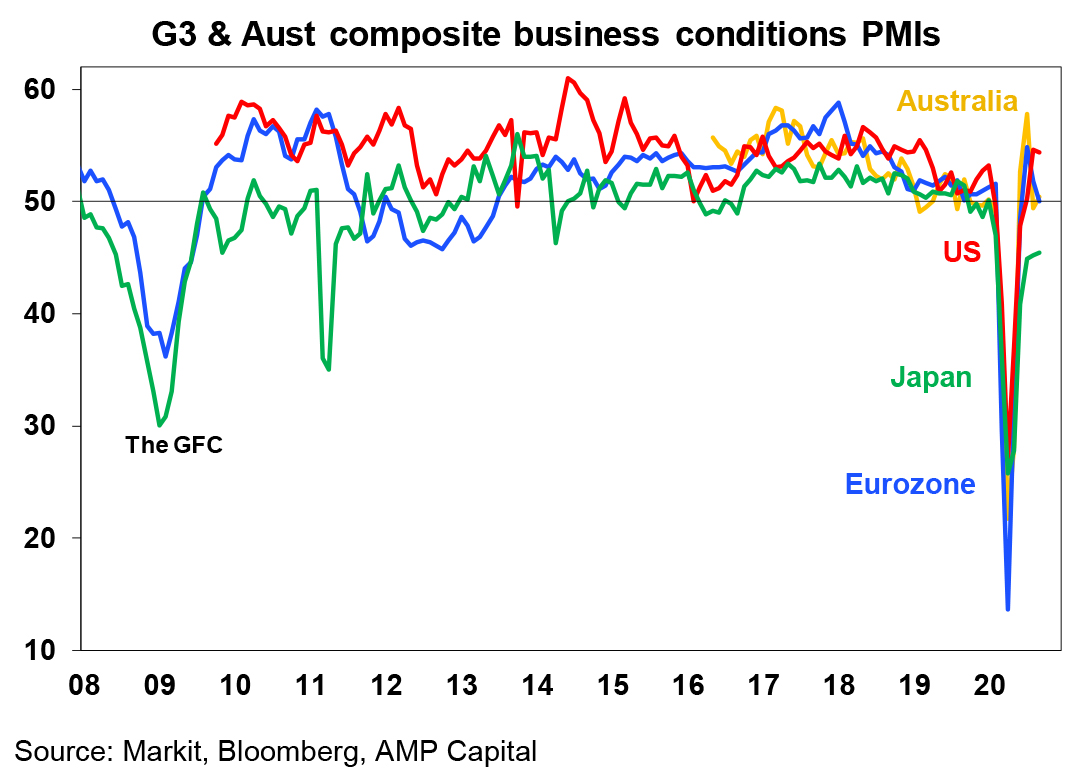

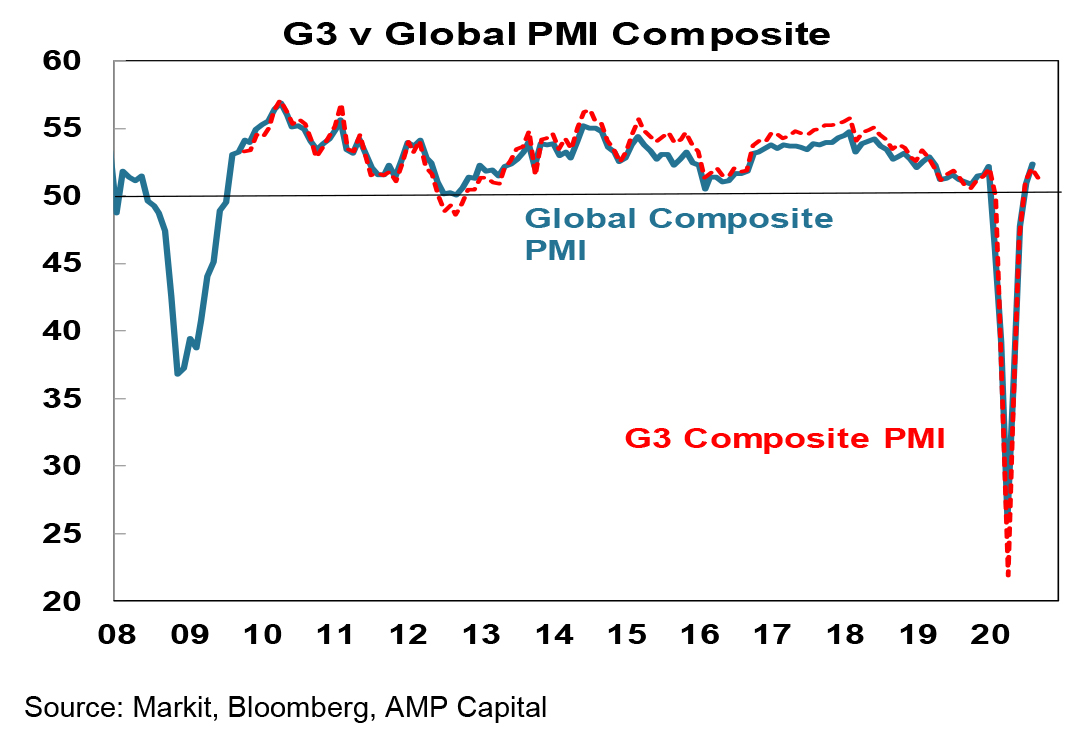

Business conditions PMIs provided a mixed picture in September but generally remain ok. They fell again in Europe and in the UK on the back of rising new coronavirus cases and renewed shutdown fears, they rose slightly in Japan and Australia and held solid in the US.

Critically, they remain well up from April lows and suggest that the full country global PMI will remain at levels consistent with continuing recovery when its released in the week ahead.

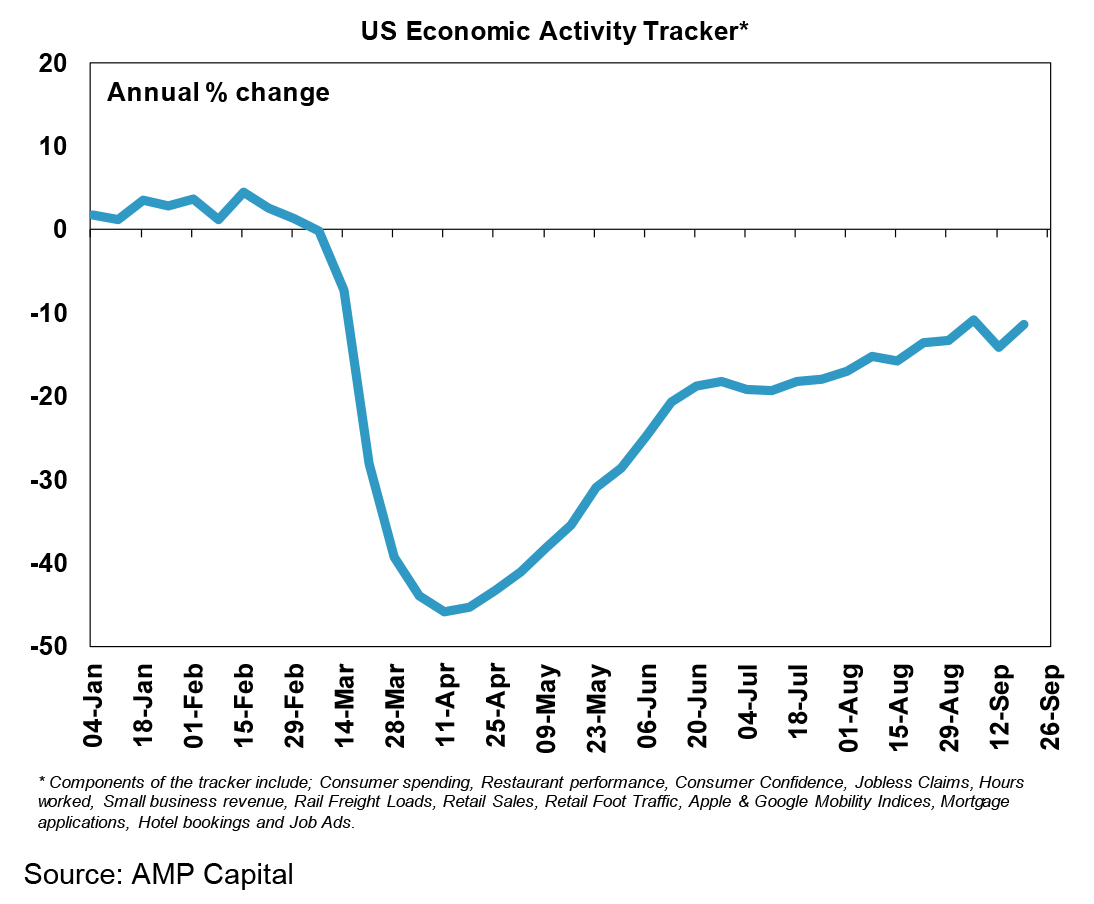

Our US Economic Activity Tracker picked up again over the last week with gains in most components and continues to trace out a gradual recovery, after the initial reopening driven rebound in May.

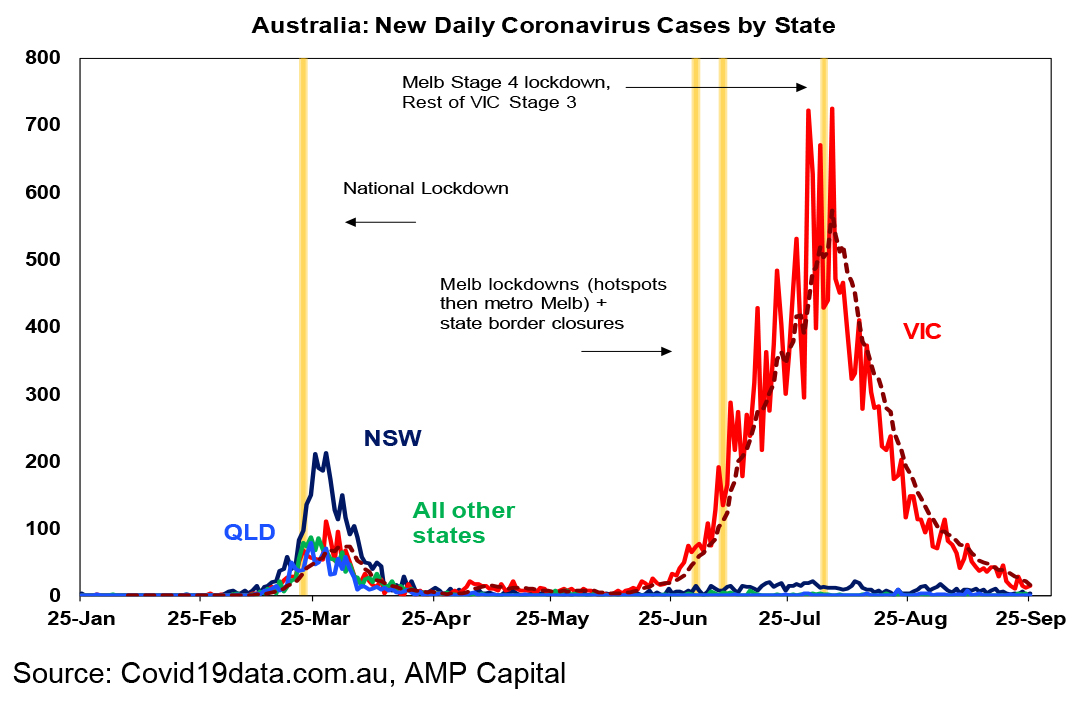

Australia is continuing to see better news on coronavirus with new cases in Victoria plunging below levels set as necessary for Melbourne’s Step Two reopening in the week ahead, holding at the prospect of a somewhat faster reopening. NSW also relaxed some distancing restrictions and various border restrictions have been relaxed or removed.

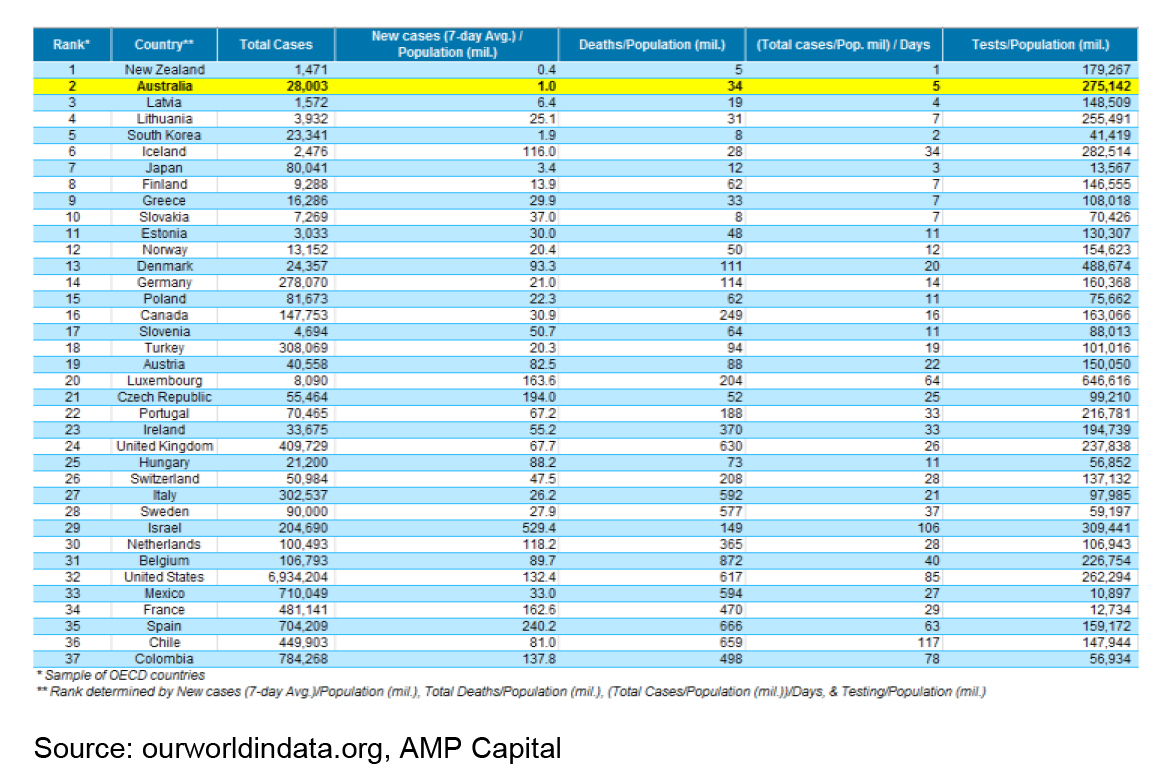

Despite the second wave in Victoria, Australia ranks only behind NZ in terms of virus control as measured across deaths, new cases, total cases and tests per capita. Which should help Australia’s recovery and Australian asset classes

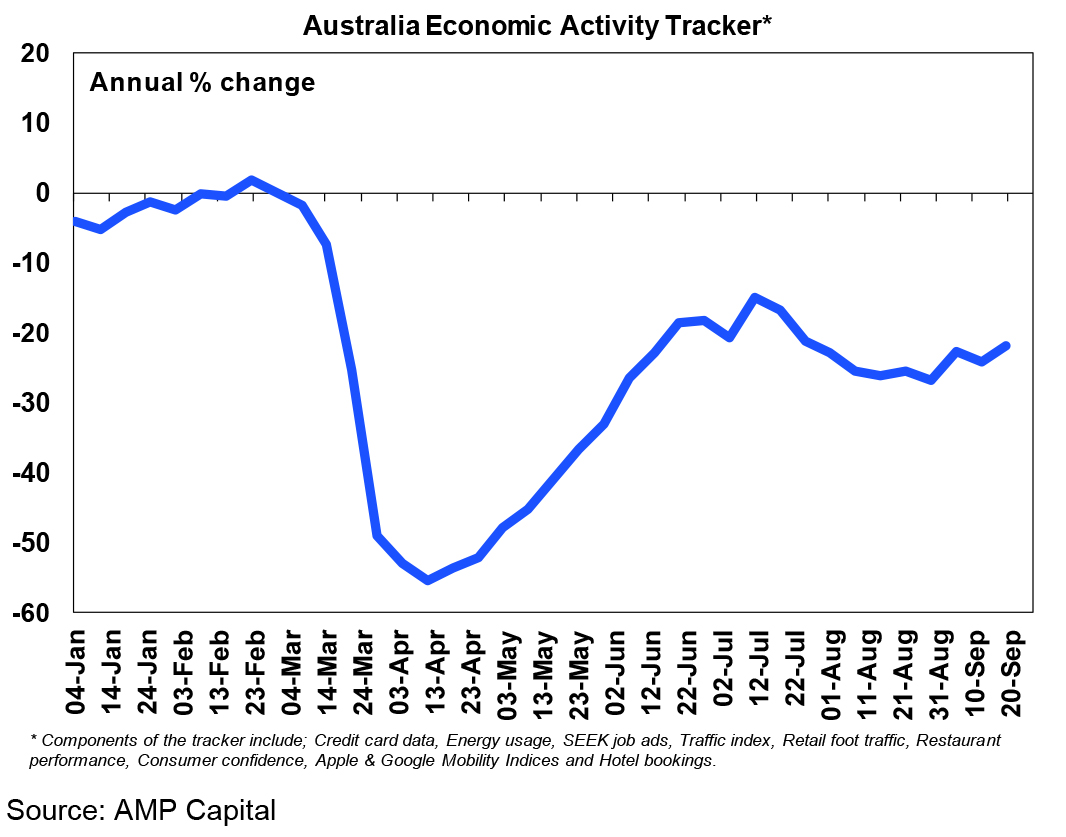

The decline in new cases has seen our Australian Economic Activity Tracker hook up from August lows. Expect a rising trend to continue as Victoria moves to a gradual reopening and other states continue to recover.

There are mixed signals regarding the next round of US fiscal stimulus with the political fight over the replacement of Supreme Court justice Ruth Bader Ginsberg adding to the divide but indications of fresh talks between Treasury Secretary Mnuchin and House Speaker Pelosi. The gap between both sides has narrowed to $1.5trn from Trump and $2.4trn from the Democrats and Trump would be mad not to agree to something as not getting it done will hurt him more than the Democrats. Ultimately, we think they will get there but it’s a close call.

On the central bank front there was lots of dovish news over the last week:

- Comments by ECB President Lagarde were dovish and consistent with an increase in quantitative easing in the months ahead;

- While repeated calls from Fed officials for more fiscal policy stimulus may be adding to market nervousness, Fed Chair Powell also said more is required from monetary policy. While some seem to want more clarity in terms of what the Fed plans to do this seems to be asking too much given the current uncertainty – the key is that it is very dovish and stands ready to do more;

- The RBNZ indicated that a cheap bank funding for lending program is set to be introduced soon and reiterated the possibility of a move to negative interest rates.

- RBA Deputy Governor Debelle provided confirmation that the RBA is considering options for more easing given that the outlook is not consistent with its objectives. His list of options was not new with negative interest rates and foreign exchange intervention remaining out of favour, but a rate cut to 0.1% and more bond buying looking more likely.

We continue to expect further easing by the RBA probably at its October meeting so as to present a united “Team Australia” front with the Federal Government as it’s the same day as the Budget. This is likely to involve cutting the cash rate, the three year bond yield target and the Term Funding Facility rate to 0.1%, tweaking forward guidance to not raise the cash rate until full employment is reached and inflation is sustainably within the 2-3% target band and adopting a more traditional quantitative easing program, although this may not come all at once.

Meanwhile the Australian Government announced several measures to further boost growth with: the NBN to spend $4.5bn over two years on fibre connections for nearly 10 million homes thereby upgrading the NBN towards what it was originally supposed to be; a relaxation of insolvency rules for small businesses; and the responsible lending laws for banks to be rolled back.

The relaxation of the responsible lending laws is a big move. The 2009 responsible lending laws were reinforced by the Royal Commission and had shifted the focus in lending decisions from “borrower beware” to “lender beware” such that many including the RBA argued the banks had become too conservative and it was taking too long to get loans as banks checked everything borrowers said down to how much they spend on coffee. This move will shift the onus back to the borrower and may speed up the flow of lending to home buyers and small businesses. APRA’s prudential lending standards will remain but it may help the recovery at the margin. The risk is that it just helps pump up the property market again down the track, pushing already high household debt levels even higher and opens the door again to “liar loans”. Its not an issue now but could be several years ahead once economic conditions are stronger.

It was a tough ending for The Bachelor this year – I reckon Irena was the right choice, but I felt really sad for Bella (and Locky). Pity Osher couldn’t make it. But back to music. I am a bit of an album person because they represent a body of work by the artist, the good ones have a common theme running through them and they are often a counter reaction to the artist’s last album (eg contrast the indie folk of Taylor Swift’s Folklore with the full on pop of Lover or the Pet Shop Boy’s Very with Behaviour). One of my favourite albums of all time is The Beach Boys’ Sunflower. It was their first album with Reprise/Warner Records after they left Capitol. While Brian Wilson is clearly evident it had brilliant contributions by all band members such that every song is a classic. Dennis Wilson’s Forever is up there with the best Beach Boys’ songs. As is Mike and Brian’s dream pop (before dream pop) All I Wanna Do. Unfortunately, the album wasn’t a big commercial success but I reckon I have played it over several hundred times.

Major global economic events and implications

US data was generally strong, with further strength in home sales, strong gains in house prices and business conditions PMIs remaining solid for September. That said the decline in initial jobless claims looks to have stalled.

The Eurozone’s composite business conditions PMI fell further driven by services in September although they remain around pre-coronavirus levels. Against this, the German IFO and French INSEE business surveys showed a further small improvement. Meanwhile Italy’s governing coalition parties received good support in electoral tests with constitutional reform which was supported by the Five Star Movement getting strong support in a referendum and the Democratic Party doing well in regional elections. Not so good for the Northern League.

Japan’s business conditions PMI’s rose slightly in September. While still soft at least they are well up from their April low.

Australian economic events and implications

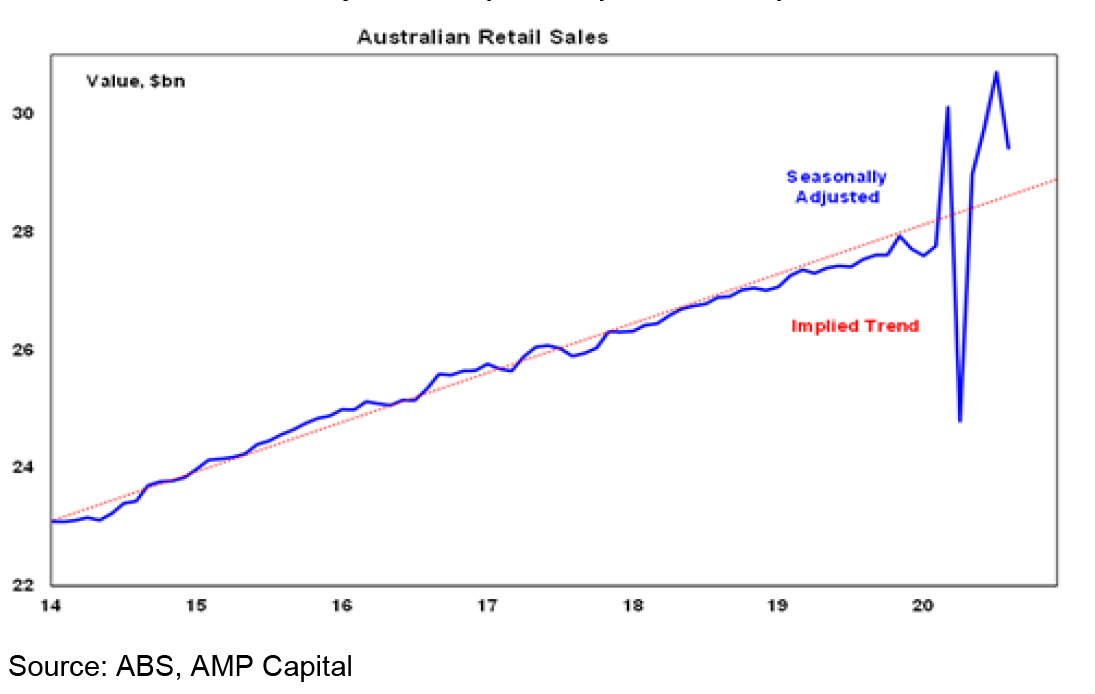

Australian data was mixed over the last week with business conditions PMIs up but payroll jobs down (but they tend to underestimate jobs growth) and retail sales down. The latter fell 4.2% in August as the surge in spending in previous months had brought spending forward and Victorian retail sales fell sharply. Retail sales remain well above trend, but this partly reflects the switch in spending from services to goods, and retail sales look likely to be up this quarter despite Victoria.

Population growth slowed to 1.4% year on year in the March quarter but the hit to immigration will see it fall to around 0.6% this financial year, its lowest since 1917. This will mean that underlying demand for dwellings will be around 80,000 less than the norm of around 175,000 pa which in turn will keep rental vacancy rates up, put downwards pressure on prices and mean less housing construction (although HomeBuilder will provide an offset).

What to watch over the next week?

In the US, September jobs data to be released Friday are likely to be the main focus. Payrolls are expected to continue to recover but the pace of gains is likely to slow to around 850,000 with the unemployment rate falling to 8.2% after the surprisingly sharp fall seen in August. In other data, expect gains in consumer confidence (Tuesday) and pending home sales (Wednesday), another solid rise in personal spending (Thursday) despite a fall in personal income on reduced unemployment benefits and continued strength in the manufacturing conditions ISM for September (also Thursday). Meanwhile, core personal consumption deflator inflation for August (Thursday) is expected to rise slightly to 1.5%yoy.

Eurozone core CPI inflation for September (Wednesday) is expected to remain low at around 0.4%yoy with unemployment (Thursday) rising slightly.

Japan’s September quarter Tankan business conditions survey (Thursday) is expected to show an improvement but August jobs data (Friday) is likely to soften slightly.

China’s September business conditions PMIs (Wednesday) are expected to remain around reasonable levels.

In Australia, expect August credit growth to remain soft (Tuesday), August building approvals (also Tuesday) to rise slightly after a big rise in July, CoreLogic September home price data (Wednesday) to show a 0.2% fall led by Melbourne, ABS job vacancies for the 3 months to August (also Wednesday) to show a solid rise and August retail sales (Friday) to confirm a 4.2% decline.

Australian budget preview – the delayed Federal 2020-21 budget (6th October) is expected to be big on spending and economic reforms all designed to spur demand and jobs. Reflecting another hit to revenue assumptions along with an extra $30bn in stimulus the projected deficit for this year is likely to be around $230bn (up from $184.5bn back in July). The key fiscal measures are expected to be a bring forward of the July 2022 tax cuts to July 2021 (at a cost of around $15bn), an investment tax break for companies, an extra $10bn in infrastructure spending, a new wage subsidy tied to employment, more support for home building, more health spending and possible stimulus payments for welfare recipients. More details around how the Government proposes to further its reform agenda around training and education, deregulation and industrial relations are also likely. The Government has also committed to not commence budget repair until unemployment is comfortably below 6% and its committed not to raise taxes when it does so.

Outlook for investment markets

Shares remain vulnerable to short term setbacks given uncertainties around coronavirus, economic recovery, the US election and US/China tensions. But on a 6 to 12-month view shares are expected to see good total returns helped by a pick-up in economic activity and stimulus.

Low starting point yields are likely to result in low returns from bonds once the dust settles from coronavirus.

Unlisted commercial property and infrastructure are ultimately likely to continue benefitting from a resumption of the search for yield but the hit to economic activity and hence rents from the virus will weigh heavily on near term returns.

Australian home prices at present are being protected by income support measures and bank payment holidays but higher unemployment, a stop to immigration and rent holidays will push prices lower into next year. Home prices are expected to fall by around 10%-15% from their April high. Melbourne is particularly at risk on this front as its Stage 4 lockdown has pushed more businesses and households to the brink.

Cash & bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.25%.

Although the $A is vulnerable to bouts of uncertainty about coronavirus, the economic recovery and US/China tensions, a continuing rising trend is likely to around $US0.80 over the next 6-12 months helped by rising commodity prices, the return of a positive bond yield differential versus the US and a cyclical decline in the US dollar.

By Shane Oliver