Weekly market update – week ending 16 October, 2020

Investment markets and key developments over the past week

Global share markets were mixed over the last week being buffeted by the rising number of new coronavirus cases and waxing and waning stimulus talk in the US. US and Chinese shares rose but Eurozone and Japanese shares fell. Australian shares were given a strong boost by the RBA signalling further easing ahead and lower for even longer interest rates with strong gains in IT, financial, consumer, utility and telco stocks pushing the ASX 200 to its highest level since early March. Bond yields generally fell with Australian 10-year bond yield falling to its lowest since April on the back of prospects for more aggressive RBA bond buying. Oil and metal prices were little changed but the iron ore price fell back to around $US120 a tonne. The Australian dollar fell on the back of a rise in the $US and expectations for more RBA easing.

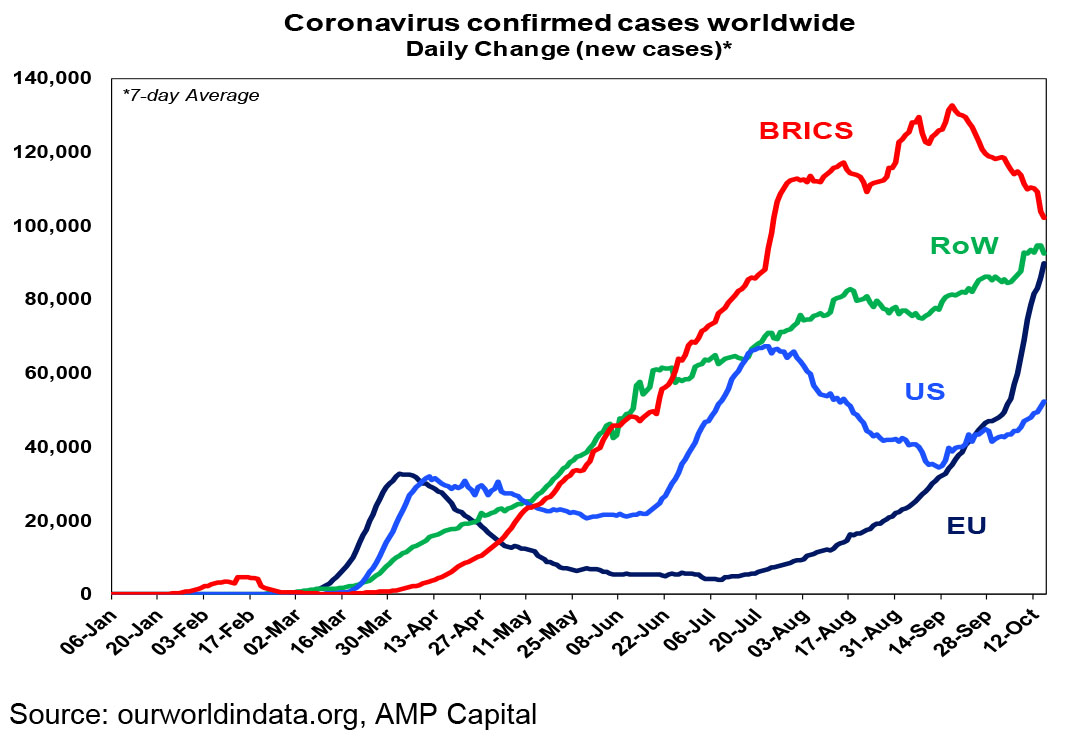

The past week has seen a continuing surge in the number of new global coronavirus cases – to be now running around 350,000 a day. The latest surge is mainly being driven by developed countries – particularly Europe, the UK and Canada but with all US regions also seeing an upswing.

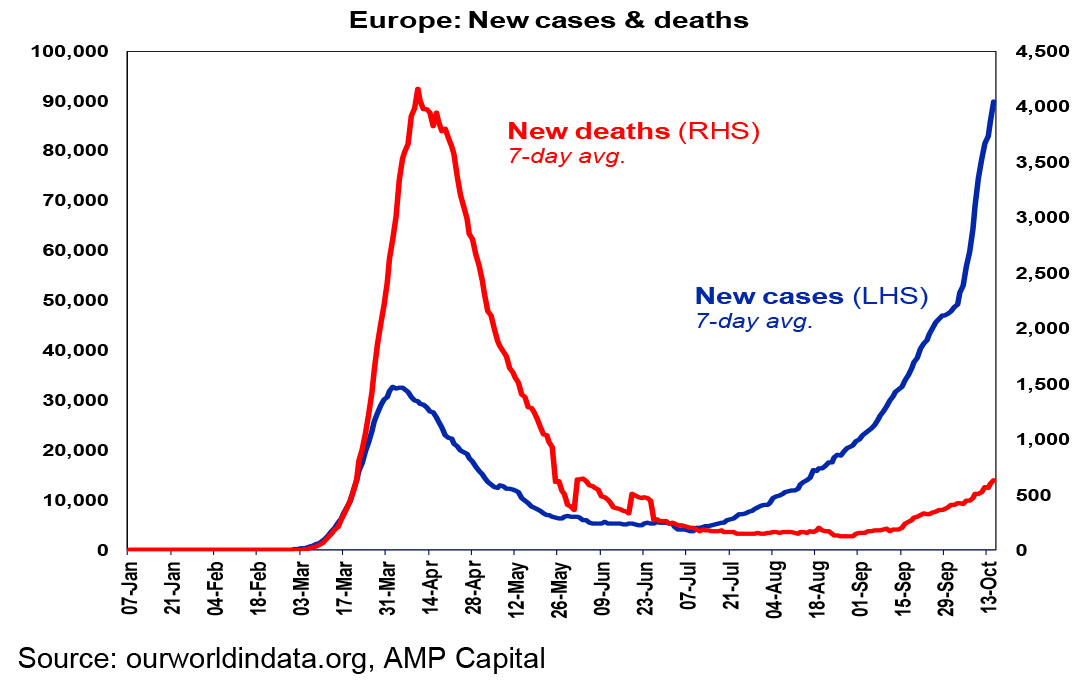

Fortunately, the number of deaths in developed countries remains well down compared to earlier this year reflecting more testing, better treatments and better protections for older people and this should help avoid a return to hard lockdowns. See the next chart for Europe

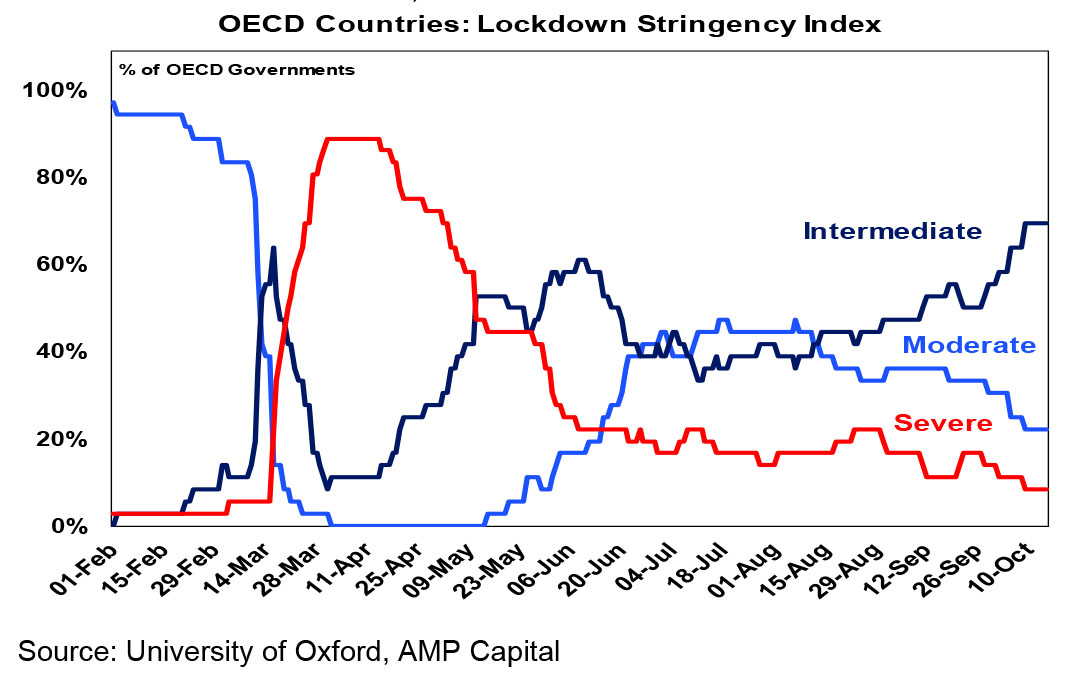

But we are nevertheless seeing a tightening in restrictions, evident in the percentage of OECD countries moving back into intermediate lockdowns, from moderate.

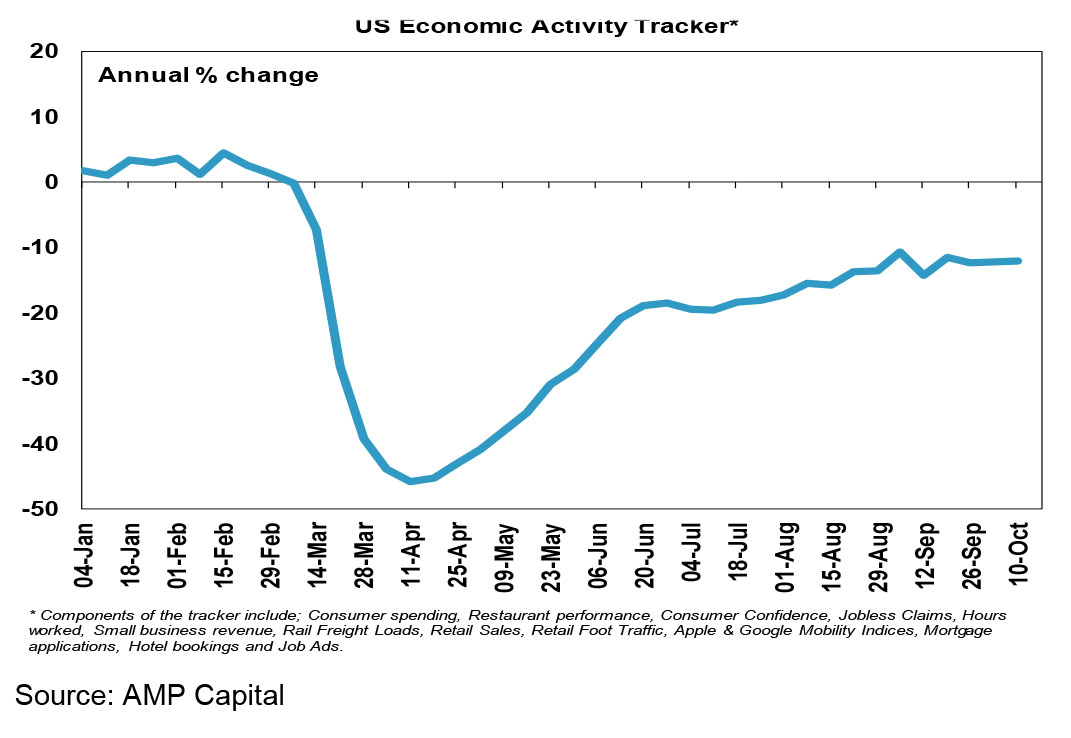

Possibly reflecting the latest rise in US cases, our US Economic Activity Tracker has been flat for several weeks now suggesting the US recovery may be stalling again.

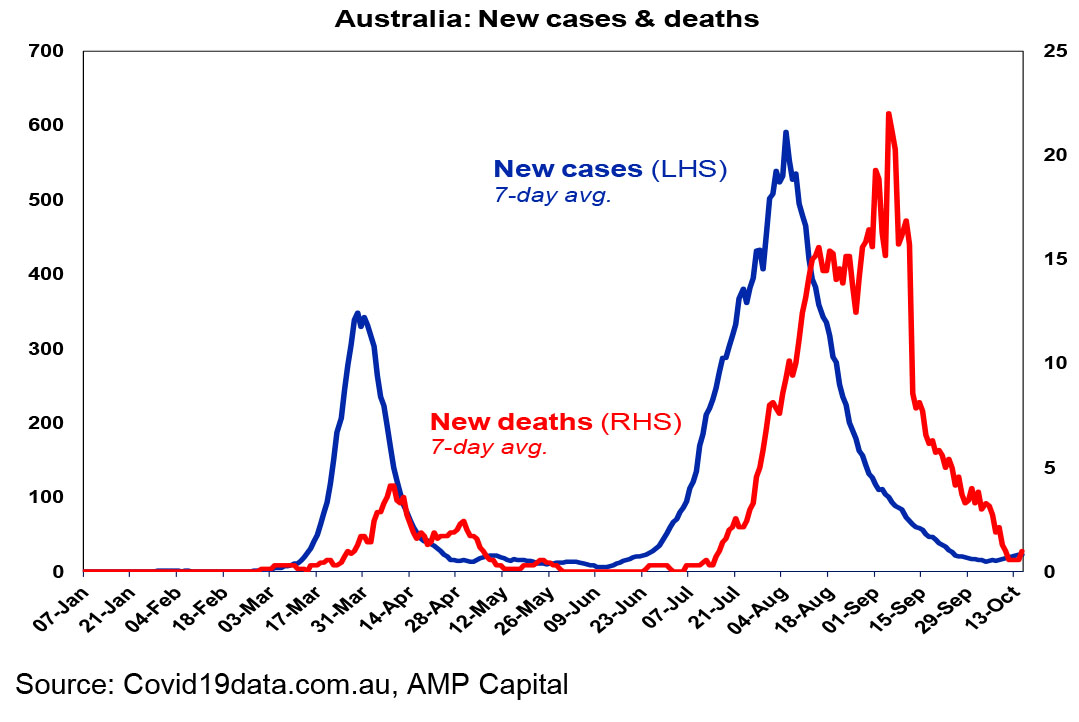

Australia is seeing new coronavirus cases remaining low and deaths have fallen. While the conditions for a Step 3 reopening in Victoria on Monday have not been met some significant further reopening is likely from Monday. NSW is continuing to see various clusters of community transmission which is delaying further reopening there.

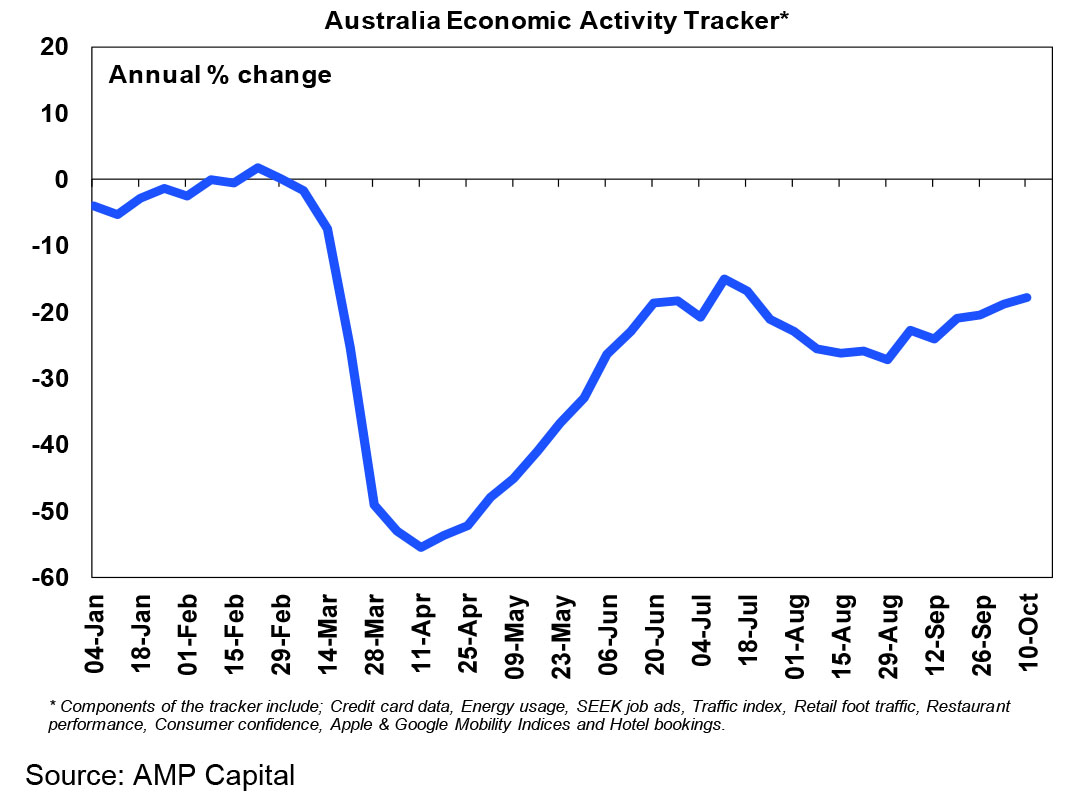

The decline in new cases has seen our Australian Economic Activity Tracker continue to hook up from August lows with gains over the last week in consumer confidence, restaurant bookings, traffic, retail foot traffic & credit card transactions. Expect the trend to remain up as Victoria gradually reopens and other states continue to recover.

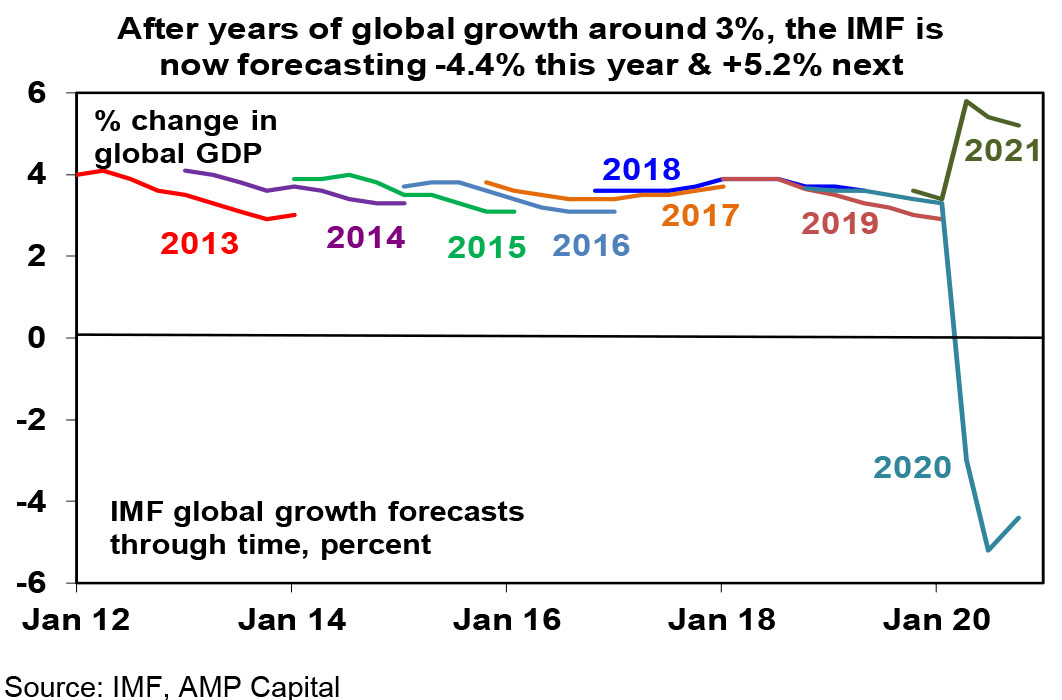

While the IMF revised up its 2020 global growth forecast to show a -4.4% contraction it revised down its 2021 forecast to 5.2% and noted the recovery will be prone to setbacks until coronavirus is tamed – we have heard that before!

The on again off again soap opera around a pre-election fiscal stimulus in the US continued over the last week. While the White House is getting desperate for a pre-election deal and so seems to be coming around to the Democrats demands in terms of size and content, Senate Republicans are still resisting although Trump will likely pressure them to support any deal. If a deal is not passed before the election it will come up again afterwards with its passage there likely assured if either Trump wins (in which case the Democrats will agree to whatever they can get in the national interest) or if the Democrats win a clean sweep (which would almost certainly see it pass the Senate). Prospects for more stimulus will be more questionable though if Biden wins without the Democrats taking the Senate (as Republican’s would likely suddenly resume their distaste for deficit spending – funny that!).

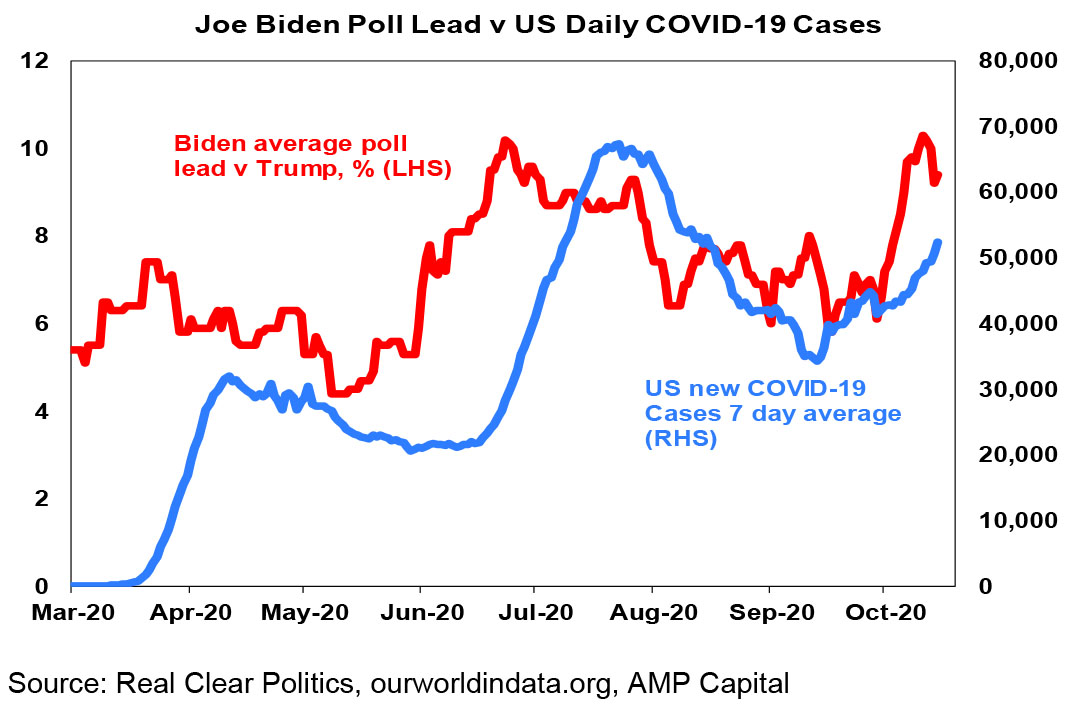

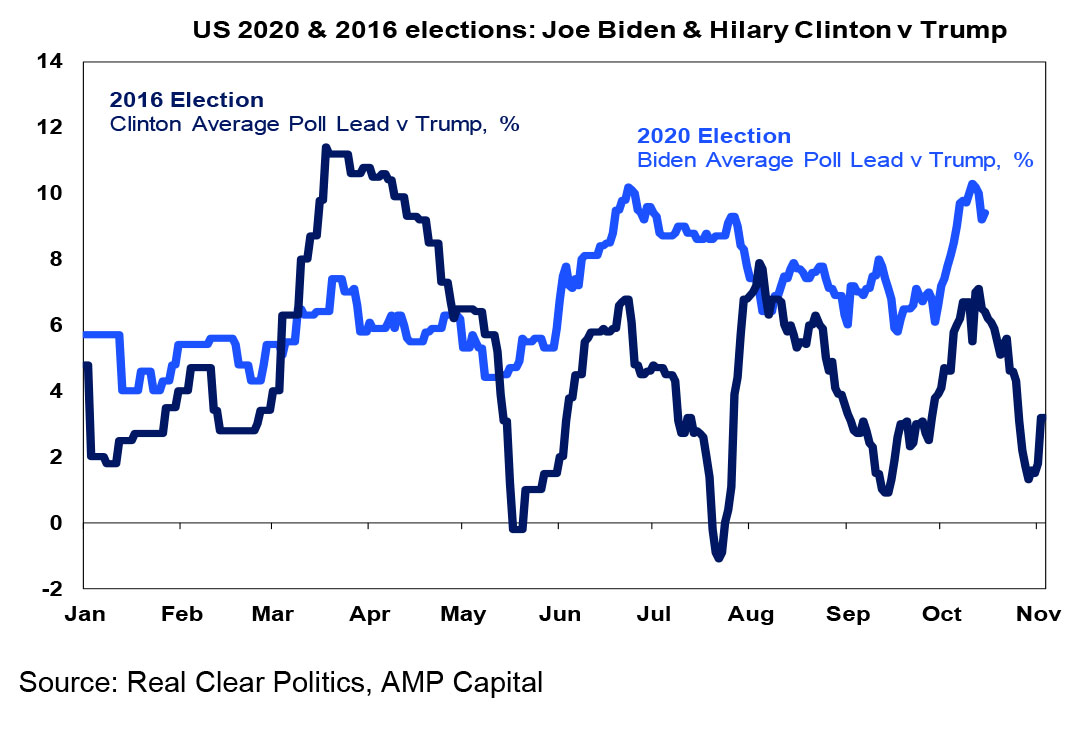

On the election front, Biden’s average poll lead held on to most of his recent gains and is around 9.4 points, his average poll lead in battleground states is around 4.4 points, Trump’s approval rating is around 44.7%, the PredictIt betting market puts Biden’s probability of winning at 66% and the probability of a Democrat clean sweep at 58%. While the debate and Trump’s behaviour after his treatment for coronavirus may have worked against him so too may be the resurgence of new coronavirus cases in the US with Biden’s lead showing some correlation with it in recent months. Along with Comedian in Chief, Trump seems to want to play Super Spreader in Chief with his high covid risk rallies and his desire to kiss everyone at the rally in Florida. Maybe he hasn’t seen the next chart!

There are still more than 2 weeks to go, but it’s interesting to note that Biden’s poll lead over the last six months has been wider and more stable than Clinton’s was in 2016.

So why isn’t the US share market fretting more at the prospect of a Democrat clean sweep which would usher in higher taxes and more regulation? Several reasons: the negative impact of higher taxes and more regulation would be offset by more fiscal stimulus; a clear Democrat victory would avert a worse case contested election; Biden will likely mean more stable policy making with less trade wars; and/or of course after 2016 many may not be expecting it.

RBA Governor Lowe announces a profound shift in the way it does monetary policy and flags that further easing is likely on the way. The clear message from RBA Governor Lowe’s speech in the last week is that it is essential for the recovery from the “uneven recession” for households and businesses to have the confidence to spend – and that while containing the virus is critical here along with the recent further support in the Budget, monetary policy still has a role to play too. On this front, Governor Lowe announced a fundamental shift in the RBA’s forward guidance to be far more dovish with a shift from focussing on “forecast inflation” to focussing on “actual inflation” in the way it runs monetary policy. As such it is now committing not to raise the cash rate until actual inflation is sustainably in the 2-3% range (as opposed to its forecast for inflation being in the range) and consistent with this wants to see more than just “progress towards full employment”. This is big move towards inflation average targeting – without the RBA actually naming it – similar to the Fed’s recent shift and means lower for even longer interest rates. More broadly, Lowe indicated that the RBA is still considering further monetary easing noting that: as the economy opens up further monetary easing would get more traction; the financial stability risks of further easing need to weighed against helping people get jobs; and that other central banks’ balance sheets have risen more than the RBAs which pushes up the Australian dollar. As a result, we continue to see further RBA easing at the November board meeting with a cut to 0.1% in the cash rate, 3-year bond yield target and Term Funding Facility rate and expanded bond buying both likely. Interestingly Lowe’s speech may suggest more of a leaning towards the latter.

In terms of something more interesting, I used to think Deep Purple were a bit too heavy for me, but the Once Upon a Time in Hollywood soundtrack got me listening to Hush which is a real classic.

Major global economic events and implications

US manufacturing conditions in the New York and Philadelphia regions remained strong in October and small business optimism rose in September. However, while continuing jobless claims (which reflect layoffs and hiring) are still falling initial jobless claims rose suggesting a stalling in the labour market recovery. Meanwhile, core CPI inflation was 1.7% over the year to September, but outside of used car prices there wasn’t much inflation in the month.

Brexit trade deal talks have yet to be resolved, increasing the risk of no-deal Brexit. A deal still seems slightly more likely than not but it’s a very close call. No deal on free trade would be far worse for the UK as nearly 50% of its exports go to the EU, whereas only 5-10% of EU exports go to the UK.

Chinese exports strengthened further in September, imports rebounded, and credit growth accelerated by more than expected, all of which is consistent with a continuing expansion in China. Meanwhile consumer price inflation slowed to 1.7%yoy and producer prices remain in deflation.

Australian economic events and implications

Australian data was mixed with the Westpac/MI measure of consumer confidence surging on the back of the further stimulus in the Budget (although the ANZ Roy Morgan measure was nowhere near as strong), but the recovery in employment and unemployment stalling in September.

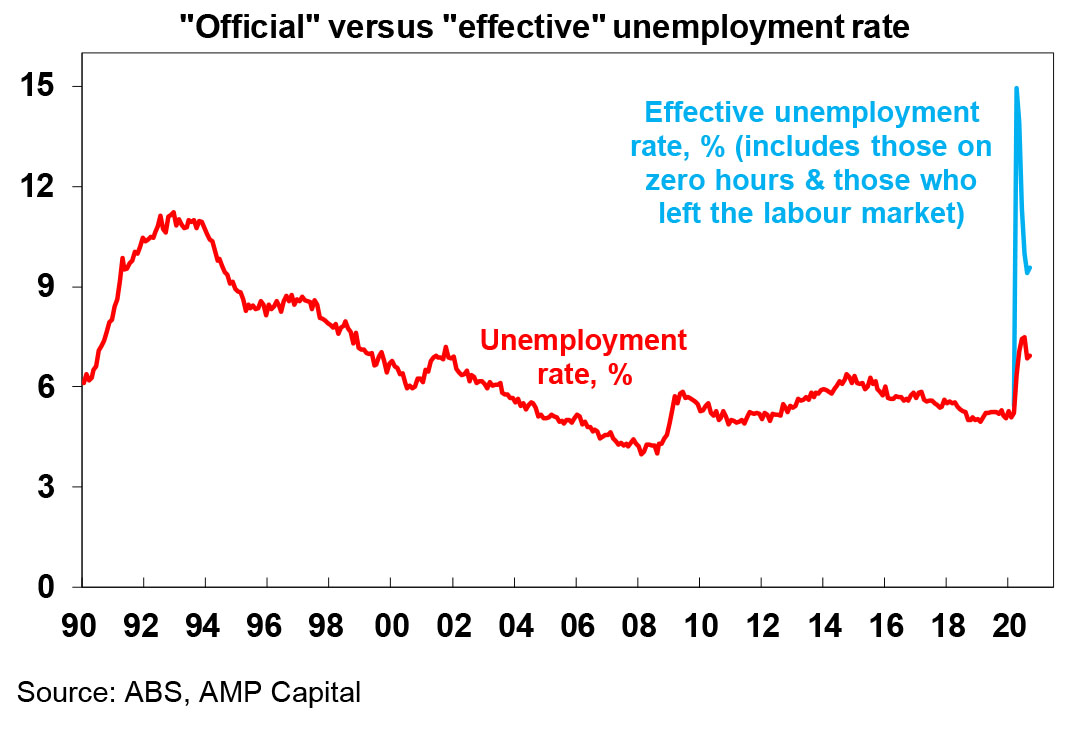

While the 29,500 fall employment was driven by Victoria, the jobs recovery has also slowed outside Victoria. Although effective unemployment (which adjusts for the impact of JobKeeper and reduced participation) has fallen from 14.9% in April to now 9.6% it remains very high as does labour market underutilisation (ie unemployment and underemployment) at 18.3%. So far just over 50% of the jobs and hours lost through April and May have been recovered but it now looks like the “easy gains” are behind us (outside of Victoria which still has catching up to do) and that the recovery going forward will be a lot slower, which in turn means that actual unemployment and underemployment will take a long time to get back to pre-coronavirus levels let alone “full employment”. With actual unemployment likely to converge on effective unemployment as JobKeeper winds down next year the Government’s forecast for unemployment of 7.25% at June next year looks too optimistic.

On the housing front continuing strength in new home sales in September confirm that HomeBuilder and other incentives to buy or build new homes are working – but note that arrivals data for September confirm that net immigration is starting to go negative.

Finally, reports suggest that China has stopped coal orders from Australia. This could be a temporary move similar to what occurred last year, or it could be reflective of a continuation of the political tensions between the two countries. Australian coal exports to China amount to around 0.7% of Australian GDP, just above education. Hopefully, it’s resolved soon rather than allowed to spread further to iron ore and other products.

What to watch over the next week?

In the US, expect to see continuing strength in the NAHB’s home builders’ conditions index for October (Monday) and increases in housing starts (Tuesday) and existing home sales (Thursday) with the composite business conditions PMI for October (Friday) remaining around its September reading of 54.3. September quarter earnings reports will start to ramp up with the consensus expecting a decline of -21%yoy, but its more likely to come in around -15%yoy.

The Eurozone’s composite business conditions PMI for October (Friday) is expected to fall slightly from September’s reading of 50.4 reflecting tightening social distancing on the back of the second wave of coronavirus cases.

Japan’s business conditions PMI for October is likely to show a further recovery and core inflation for September is expected to remain around -0.1%yoy (both due Friday).

Chinese data is expected to show a continuing expansion in the economy after the hit from the coronavirus lockdown in the March quarter. September quarter GDP is expected to rise by 3.3% quarter on quarter after the 11.5%qoq recovery seen in the June quarter. This would take annual growth to 5.4% year on year. September data is also likely to show a further acceleration in growth in industrial production to 5.8%yoy and with retail sales growth picking up to 2%yoy.

In Australia, the Minutes from the last RBA meeting (Tuesday) and a speech by RBA Deputy Governor Debelle (Thursday) will be watched for any clues regarding future monetary easing although the Minutes are now a bit dated given Governor Lowe’s recent speech. On the data front payroll jobs data for the 3rd of October (Tuesday) will be watched for signs of further improvement, preliminary retail sales data for September (Wednesday) are likely to show only a 1% or so rise after August’s 4.2% fall and the CBA’s business conditions PMIs for October (Friday) are expected to rise.

Outlook for investment markets

Shares remain vulnerable to further short-term volatility given uncertainties around coronavirus, economic recovery, the US election and US/China tensions. But on a 6 to 12-month view shares are expected to see good total returns helped by a pick-up in economic activity and stimulus.

Low starting point yields are likely to result in low returns from bonds once the dust settles from coronavirus.

Unlisted commercial property and infrastructure are ultimately likely to benefit from a resumption of the search for yield but the hit to economic activity and hence rents from the virus will weigh heavily on near term returns.

Australian home prices at present are being protected by income support measures and bank payment holidays but higher unemployment, a stop to immigration and weak rental markets will push prices down by another 5% into next year. Melbourne is particularly at risk on this front as its Stage 4 lockdown has pushed more businesses and households to the brink. Smaller cities and regional areas are in much better shape.

Cash & bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.25%.

Although the $A is vulnerable to bouts of uncertainty about coronavirus, the economic recovery and US/China tensions, a continuing rising trend is likely to around $US0.80 over the next 6-12 months helped by rising commodity prices and a cyclical decline in the US dollar.

By Shane Oliver