Weekly market update – week ending 2 October, 2020

Investment markets and key developments over the past week

Global share markets mostly rose over the last week helped by dip buying in the US, some hope (which is now fading) for a new US stimulus deal and mostly good economic data. Australian shares fell though, after bucking the trend of falling markets in the previous week and with energy, consumer staple, utility, health and financial shares particularly hard hit. Bond yields fell in the Eurozone but mostly rose elsewhere. Commodity prices generally fell but gold rose as did the $A as the $US fell

While global shares have had a bit of a bounce over the last week led by the US it remains too early to say the correction is over – seasonal weakness often continues into October, coronavirus could worsen into the northern winter, another round of US fiscal stimulus is now looking less likely until after the election and the US election is likely to add to volatility. News that President Trump has been tested for coronavirus and will quarantine will likely add to the short-term uncertainty. However, we remain of the view that it’s just a correction after an excessive run up in US shares and not the start of a renewed bear market and that a continued but gradual and messy recovery along with ultra-easy monetary policy will underpin a rising trend in shares on a 6-12 month horizon, providing coronavirus is controlled.

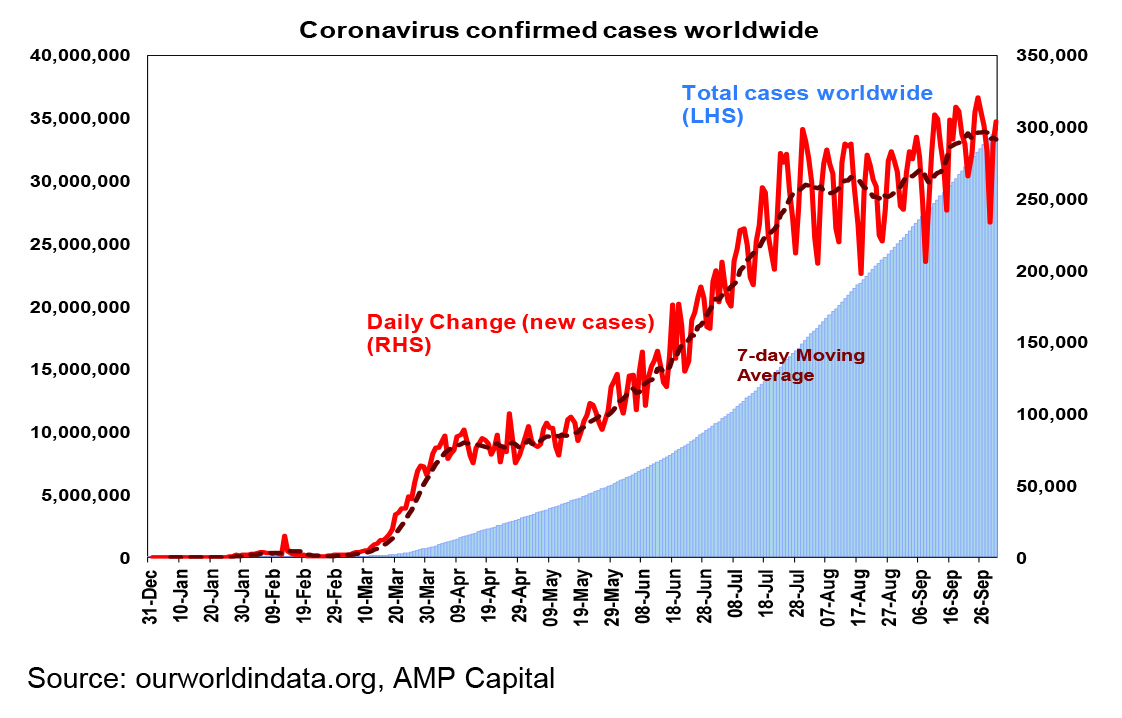

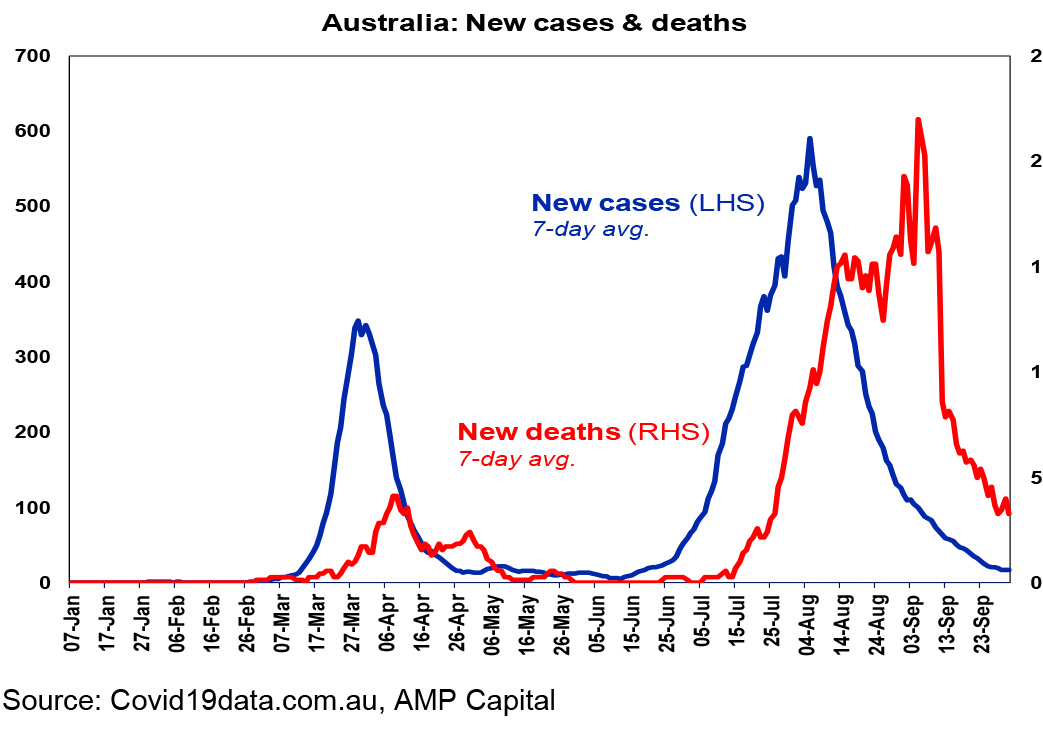

The past week has seen the trend in new coronavirus cases track sideways at just below 300,000 a day.

While emerging countries have seen a bit of a decline in new cases – with India, Brazil, Mexico, Saudi Arabia and Bangladesh all seeing falls from their highs – developed countries are still seeing a rising trend, particularly in Europe, the UK, Canada and possibly the US (where the trend is down in the south but up elsewhere including the north east.)

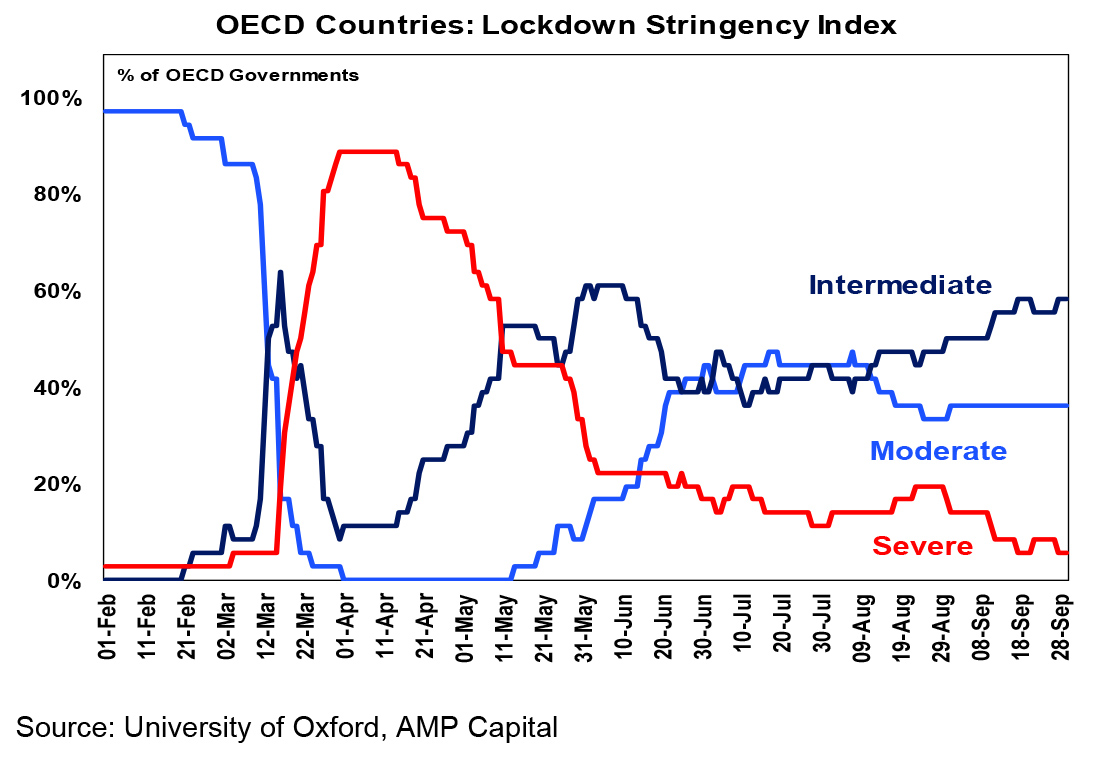

This is continuing to see various countries tighten restrictions raising concerns about new lockdowns.

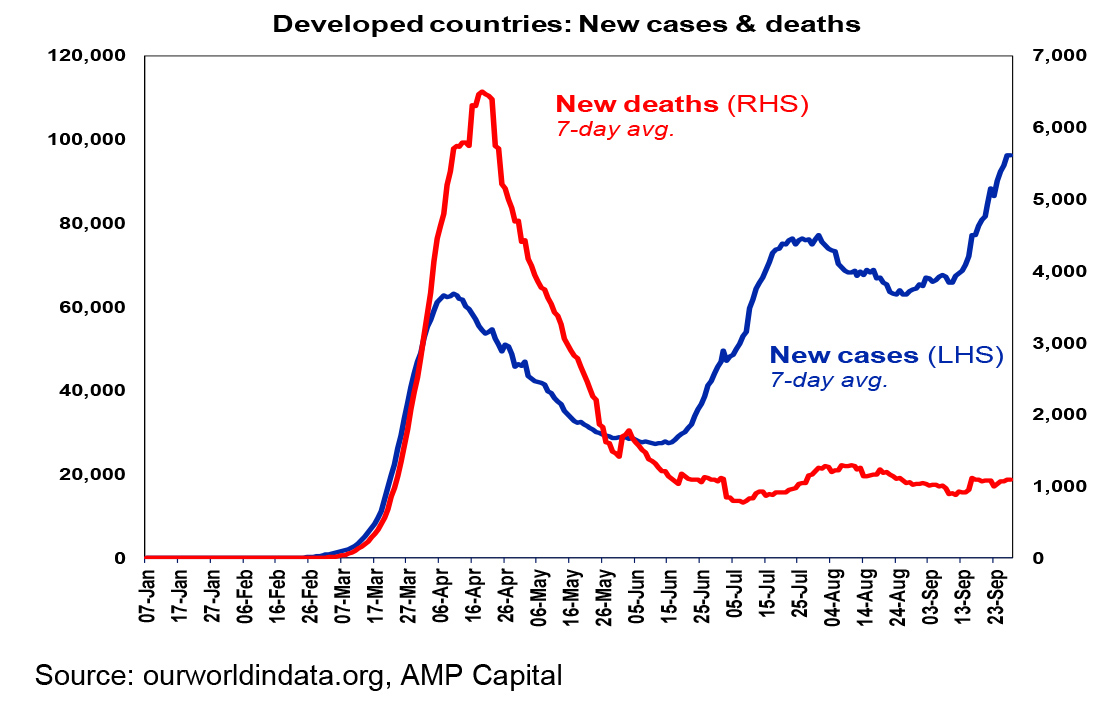

But as indicated in the second chart above the number of deaths remains well down compared to earlier this year reflecting more testing picking up more younger cases, better treatments and better protections for older people and this should help avoid a return to hard lockdowns.

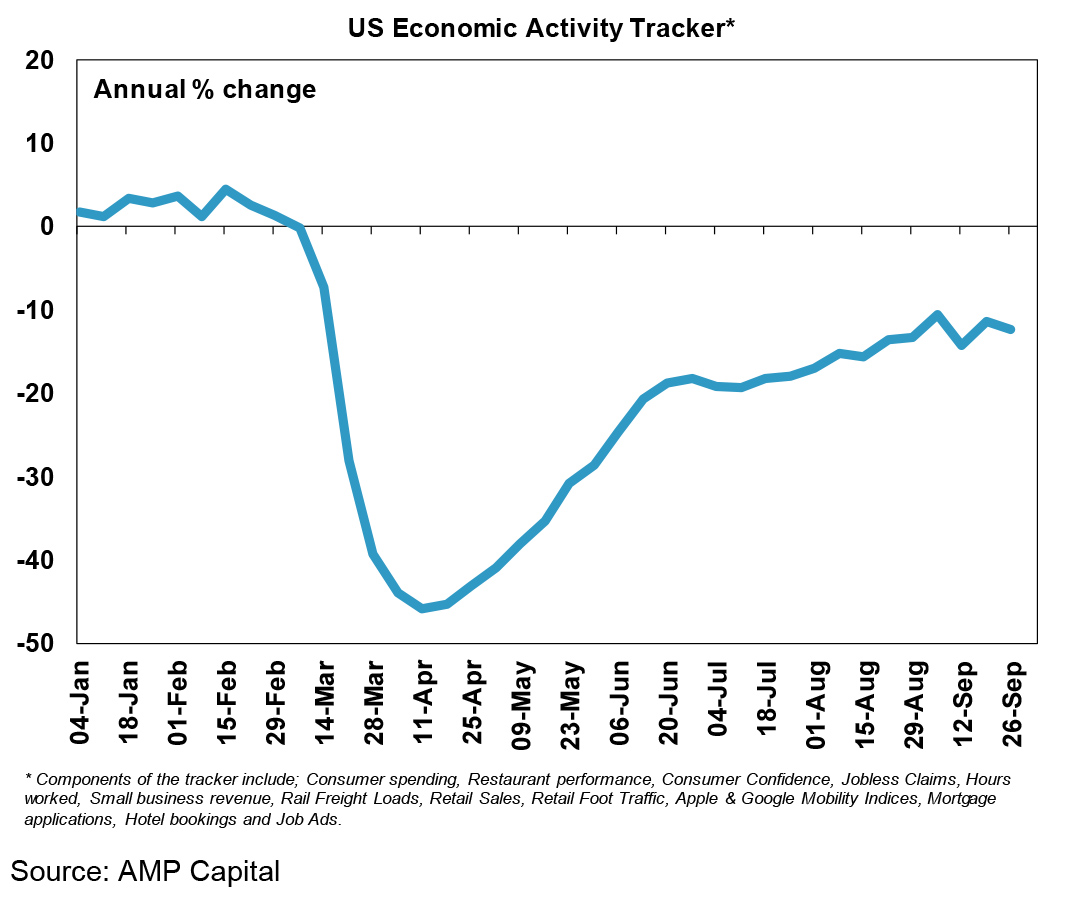

Our US Economic Activity Tracker ticked down again in the last week but is continuing to trace out a gradual rising trend after the initial rapid pick up from April.

Australia is continuing to see better news on coronavirus with new cases in Victoria plunging enabling reopening to proceed a bit faster than originally envisaged and a possible bring forward of its Step Three reopening to the middle of the month.

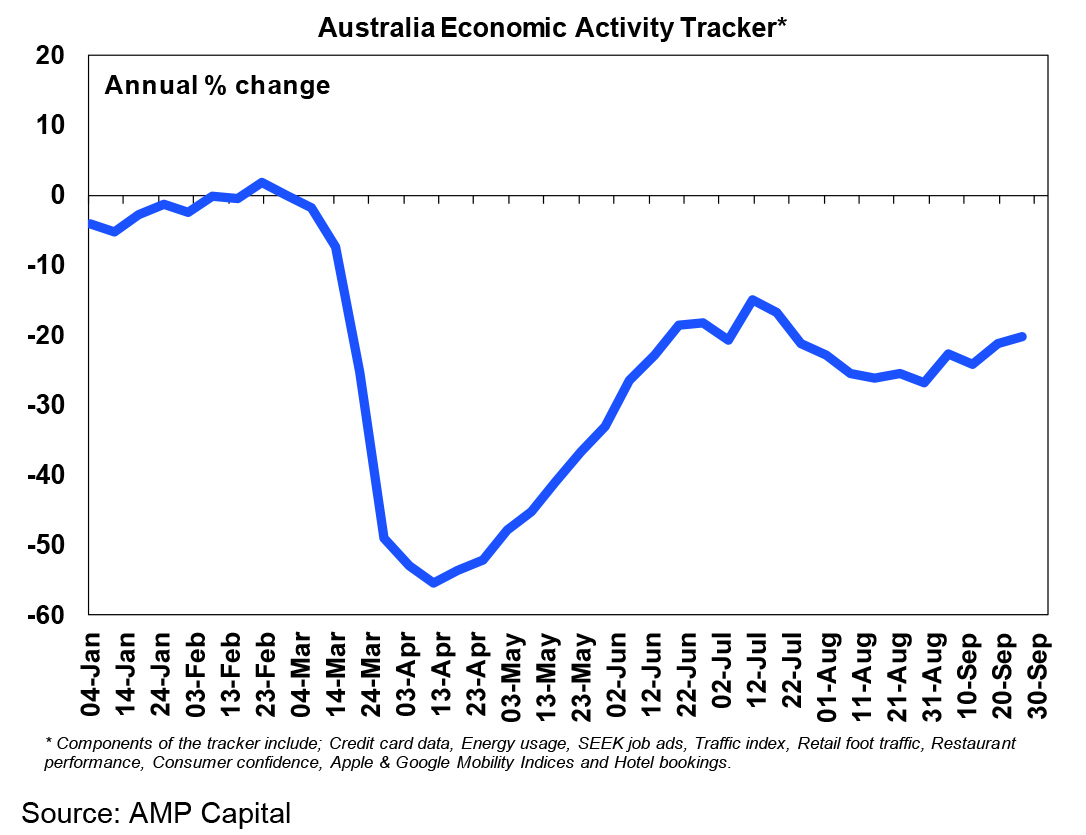

The decline in new cases has seen our Australian Economic Activity Tracker continue to hook up from August lows with gains over the last week in restaurant and hotel bookings, traffic and mobility. Expect the trend to remain up as Victoria reopens a bit more quickly than had been originally flagged and other states continue to recover.

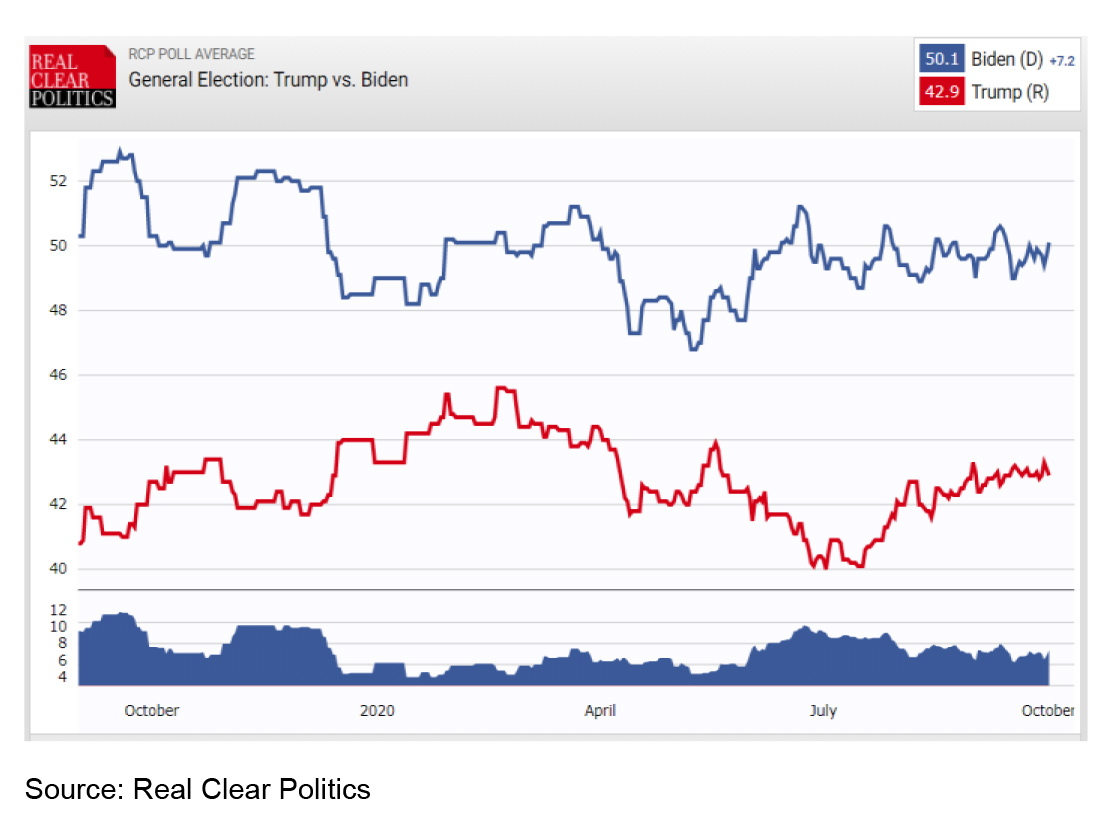

The first presidential debate provided a reminder that the US election is rapidly looming, and that Trump has not lost his penchant for creating chaos. It didn’t provide anything new on the policies offered by both sides. Although I did get a bit (more) concerned by Trump’s “message” if that’s what it was to the Proud Boys to “stand back and stand by”…for what exactly – civil war? Insecure boys with guns always drive me bonkers. For what it’s worth Biden’s lead on the Predict It betting market went from about 12 points to 20 points after the debate but just bear in mind that the “winners” in past debates have not been a good guide to election outcomes. Biden’s average poll lead remains relatively stable at around 7 points, although polls post the debate are somewhat higher.

On the economic policy front, while talks between the US Administration and Democrats made progress towards a new round of fiscal stimulus and the gap between the two has narrowed, it’s still wide with Democrats at $2.2trn and Trump at $1.6trn. Polling suggests that Americans are strongly in favour of more stimulus but with the Democrat controlled House now passing their $2.2trn plan and signalling unified support for stimulus on their part, a failure to reach an agreement on a final deal will weigh more on Trump and GOP Senators (of which 23 are up for re-election on 3rd November versus only 12 Democrat senators) than on Democrats. Meanwhile time is running out as politicians want to get back home to campaign. No deal on stimulus will threaten shares in the short term, but a Democrat clean sweep on 3rd November would then be taken positively by shares as it would clear the way for more stimulus after the election offsetting the worries about tax hikes under Biden.

In Australia, pre budget measures to boost growth continue to roll out with an initial allocation of $1.5bn for the Government to pick manufacturing sector winners (in the areas of resources, food, medical products, recycling & clean energy, defence & space). This is largely motivated by the shortcoming posed through the pandemic to supply chains and the resurgence of nationalist sentiment. Whether “picking winners” works any better than practiced in the past remains to be seen. That said it’s a long long way from full-scale post-war protectionism.

Watching an episode of The Sound (from a few months back) I came across a great Australian band called San Cisco. They have been around for a while but their latest album is worth checking out including On The Line. So, do yourself a favour!

Major global economic events and implications

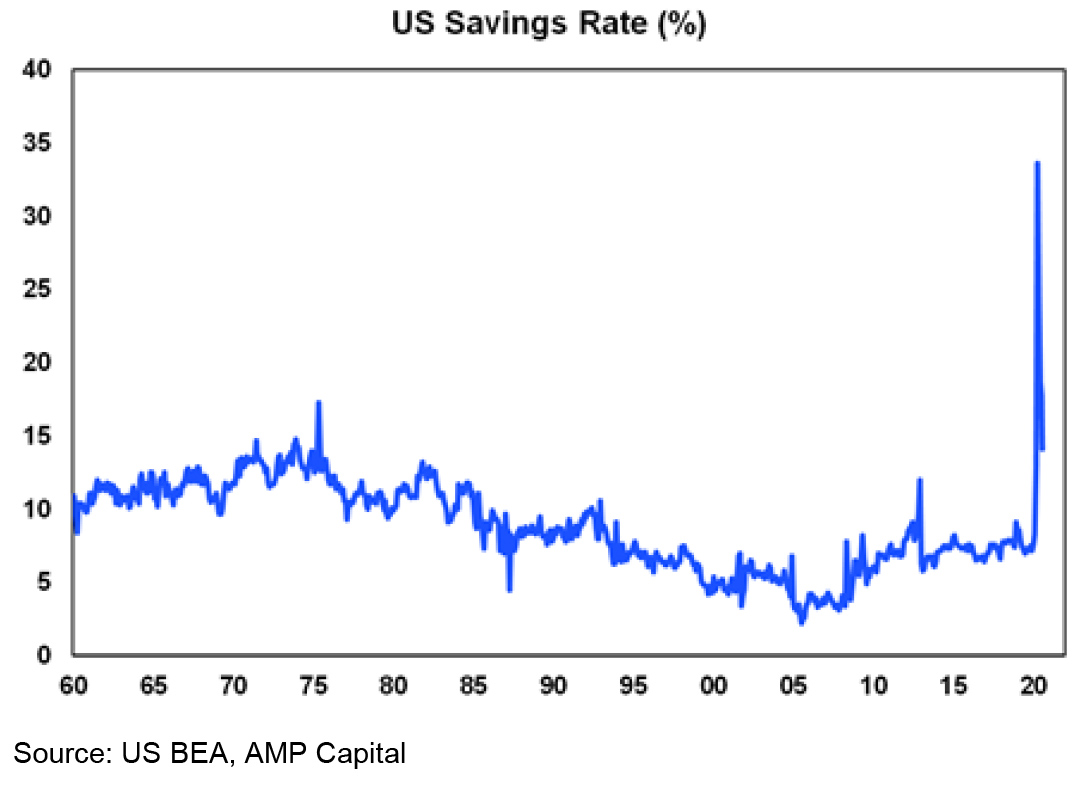

US data remained strong over the past week with the manufacturing conditions ISM for September holding around 56, consumer confidence up, pending home sales surging in August with strong home price gains, construction spending up, jobless claims falling and August personal spending seeing a solid gain despite a fall in income on the back of reduced unemployment benefits with households drawing down the saving rate. The still high personal saving rate of 14% suggests that this will remain a source of support for spending going forward providing confidence improves.

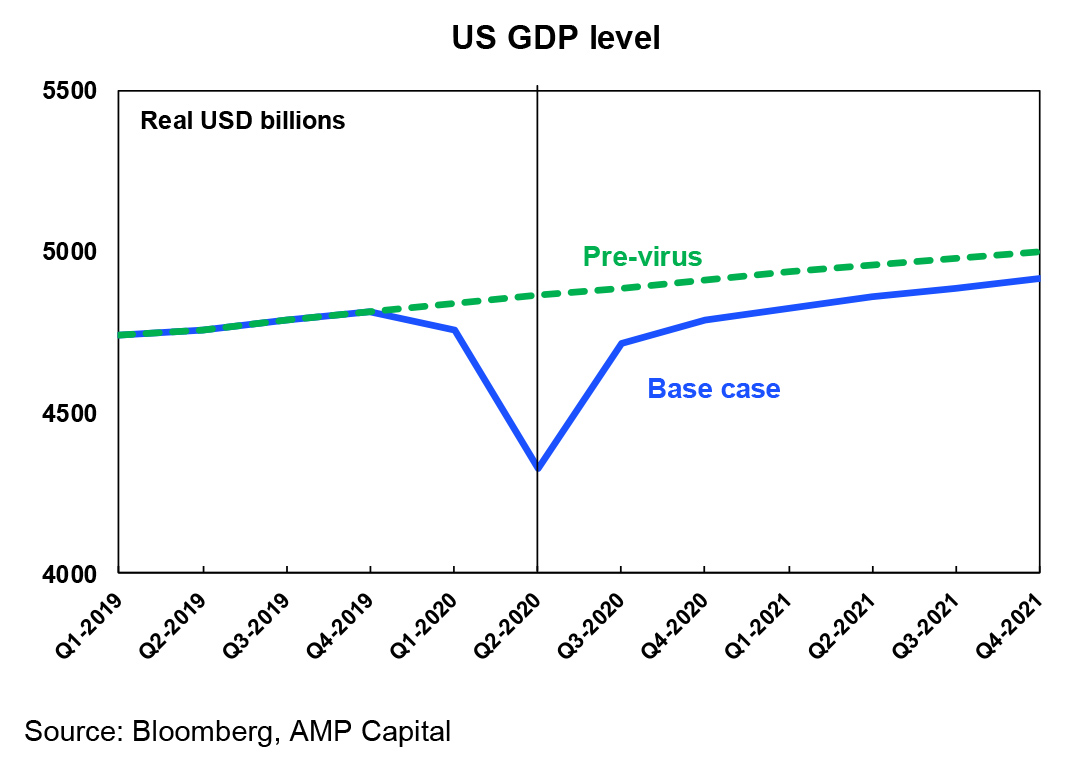

The US remains on track for an initial Deep V recovery with the Atlanta Fed’s GDP Now pointing to a 9% rebound in September quarter GDP based on already released data after a 9% June quarter contraction. Going forward its likely going to be a lot slower consistent with our US Economic Activity Tracker shown earlier in this note. Hence the need for more stimulus. See the next chart.

Eurozone unemployment rose in August to 8.1% but economic sentiment continued to recover.

Japanese industrial production and the Tankan business sentiment survey rose but are still a long way from normal and the ratio of job openings to applicants continued to fall.

Chinese business conditions PMI’s all remained solid in September indicating that China’s expansion is continuing.

Australian economic events and implications

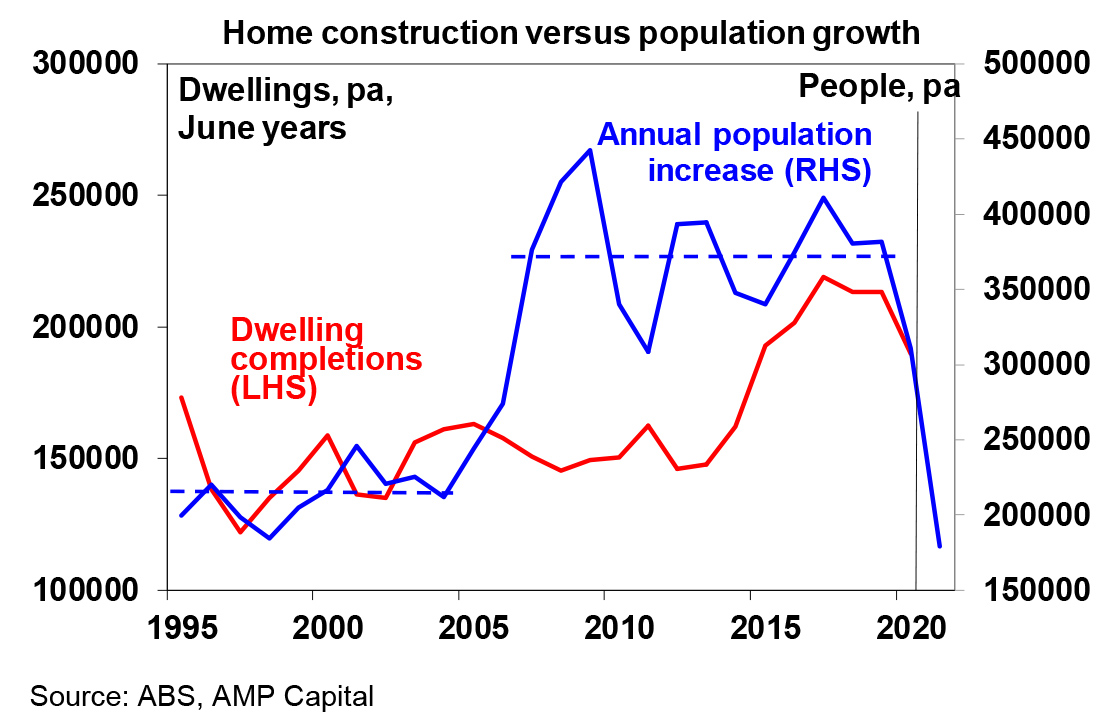

Australian data was mixed with a decline in building approvals, very weak growth in credit but a surge in job vacancies over the three months to August that recovered 80% of the slump in May. The rebound in job vacancies is consistent with various private surveys and points to more jobs growth ahead. HomeBuilder and various housing sector measures should help support building approvals in the months ahead despite the collapse in underlying demand associated with the crash in immigration. Final August retail sales confirmed a 4% decline mainly driven by Victoria but with most states down slightly as pent up demand had been used up and demand had been brought forward.

Meanwhile capital city home prices fell again in September, but the pace of decline has continued to slow and six of the eight cities saw gains. Massive government income support measures and bank payment holidays explain why house prices have only fallen slightly over the last six months despite the biggest hit to the economy since the 1930s. But the artificial nature of the market also makes it hard to work out what this means for the future direction of prices. High unemployment, the collapse in immigration and the hit to the rental market point to more downside. But working against this are continuing government measures to support the property market – with the removal of responsible lending obligations and more measures likely in the Budget – on top of record low interest rates and more rate cuts also in prospect. Reflecting all these cross currents we continue to expect further declines in Victoria reflecting the bigger hit to its economy and maybe Sydney, but other cities seeing modest price gains. Reflecting the “work from home” phenomenon outer suburbs, regions and houses and likely to perform far better than inner city areas and units. The hit to immigration which will take many years to reverse will act as a constrain on medium term house price gains as will work from home which has given many people more flexibility as to where they live.

What to watch over the next week?

In the US, the services conditions ISM index for September (Monday) will likely remain strong, labour market hiring and openings data for August (Tuesday) will be watched closely for further improvement, the minutes from the Fed’s last meeting which confirmed inflation average targeting will be released Wednesday but a speech by Fed Chair Powell (Tuesday) will be more forward looking and will likely be very dovish.

In Australia, the main focus will be on the Government’s 2020-21 Budget on Tuesday which is expected to be big on spending and economic reforms all designed to spur demand and jobs. Reflecting another hit to revenue assumptions along with an extra $30bn in stimulus the budget deficit for this financial year is likely to be around $230bn (up from $184.5bn back in July). The key fiscal measures are expected to be:

- a bring forward of the July 2022 tax cuts to July 2020 or July 2021 (at a cost of around $15bn) and possibly the July 2024 tax cuts to July 2022;

- an investment tax break for all companies;

- an extra $10bn in infrastructure spending to state governments on a “use it or lose it” basis;

- a new wage subsidy tied to increased employment to replace JobKeeper;

- more support for the housing sector – probably via an extension of HomeBuilder and an expansion of the First Home Buyer Deposit scheme;

- $1.5bn in initial funding to help encourage manufacturing in six key areas;

- fringe benefits tax exemptions for businesses for eg retraining workers, supplying laptops & phones to workers;

- more health spending; and

- possibly more stimulus payments for welfare recipients.

More details around how the Government proposes to further its reform agenda around training and education, deregulation and industrial relations are also likely. The Government is also likely to affirm its commitment to not commence budget repair until unemployment is comfortably below 6% and to not raise taxes when it does so.

Just before the Budget on Tuesday the RBA meets with further monetary easing up for consideration. We expect more easing from the RBA for the simple reason that its forecast outlook for inflation and employment is not consistent with its objectives and it has highlighted regularly over the last month or so that its considering options for further easing. Our base case is that the RBA will cut the cash rate, the Term Funding Facility rate and the three year bond yield target to 0.1% on Tuesday so as to present a united “Team Australia” front with fiscal policy on the same day and thereby get a bigger impact. And this is what we think they should do. Why wait? But given the lack of enthusiasm amongst journalists thought to be connected to the RBA for a Tuesday move its close to 50/50 as to whether the cut will come in the week ahead or at the RBA’s November meeting when it will also have a new set of forecasts. Over the next six months we also see the RBA tweaking forward guidance to not raise the cash rate until full employment is reached and inflation is sustainably within the 2-3% target band and adopting a more traditional quantitative easing program extending beyond the three-year bond.

On the data front in Australia, the trade balance for August (Tuesday) is likely to show an increased surplus with imports falling faster than exports, payroll jobs data for 19th September will be released on Wednesday (but have not been the best guide to surveyed jobs growth) and housing finance for August (Friday) is likely to show another rise. The RBA will also release its six-monthly Financial Stability Review on Friday.

Outlook for investment markets

Shares remain vulnerable to further short term setbacks given uncertainties around coronavirus, economic recovery, the US election and US/China tensions. But on a 6 to 12-month view shares are expected to see good total returns helped by a pick-up in economic activity and stimulus.

Low starting point yields are likely to result in low returns from bonds once the dust settles from coronavirus.

Unlisted commercial property and infrastructure are ultimately likely to continue benefitting from a resumption of the search for yield but the hit to economic activity and hence rents from the virus will weigh heavily on near term returns.

Australian home prices at present are being protected by income support measures and bank payment holidays but higher unemployment, a stop to immigration and rent holidays will push prices down by another 5% into next year. Melbourne is particularly at risk on this front as its Stage 4 lockdown has pushed more businesses and households to the brink.

Cash & bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.25%.

Although the $A is vulnerable to bouts of uncertainty about coronavirus, the economic recovery and US/China tensions, a continuing rising trend is likely to around $US0.80 over the next 6-12 months helped by rising commodity prices, the return of a positive bond yield differential versus the US and a cyclical decline in the US dollar.

By Shane Oliver