Weekly market update – week ending 23 October, 2020

Investment markets and key developments over the past week

Global share markets were mixed over the last week being buffeted again by waxing and waning stimulus prospects in the US and ever rising numbers of new coronavirus cases. US and Eurozone shares fell but Japanese and Chinese shares rose slightly. Reflecting the messy global lead Australian shares fell slightly as a rise in bond yields pushed down utilities, telcos and property stocks and materials and consumer staples also fell which offset gains in IT, energy and financial shares. Bond yields rose reversing the declines of the previous week. While the oil price fell slightly, gold, metals and iron ore prices rose helped by a falling US dollar. This also saw the $A rise.

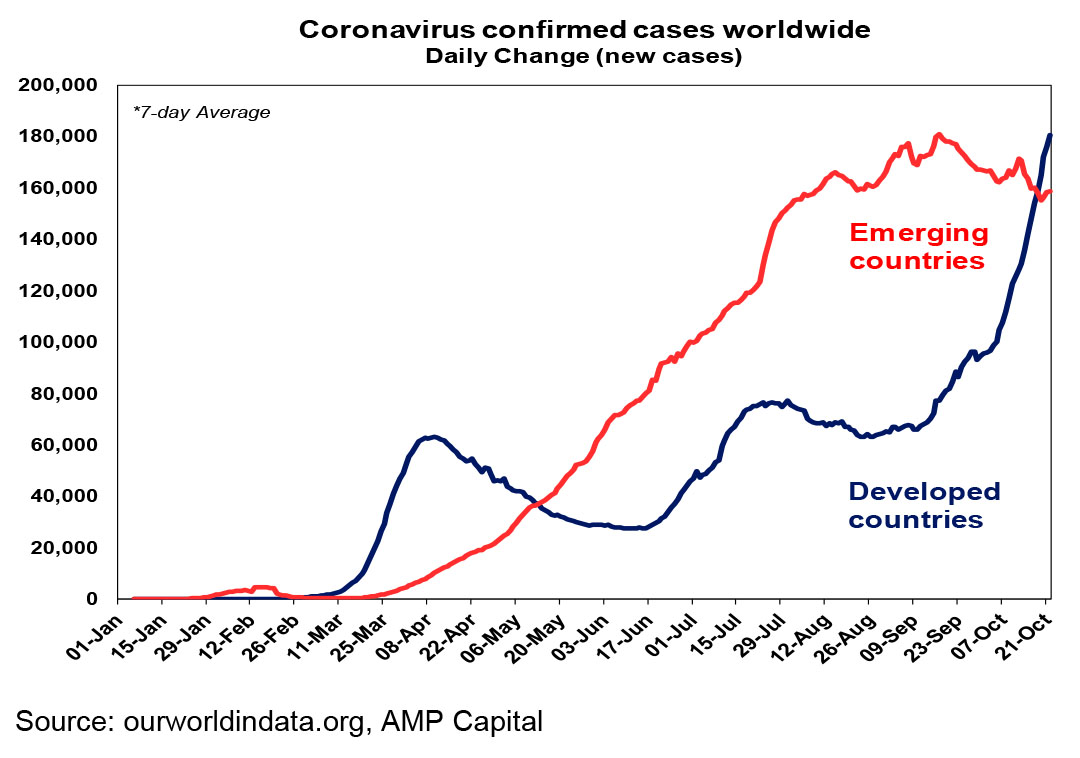

The rising trend in new coronavirus cases continued over the past week. While emerging countries have continued to roll over with a falling trend in India and Brazil, new cases in developed countries continue to surge higher. This is particularly the case in Europe and the UK, and the US is now seeing new cases approach their July high, making it hard to see how President can say its “turned the corner” in the US.

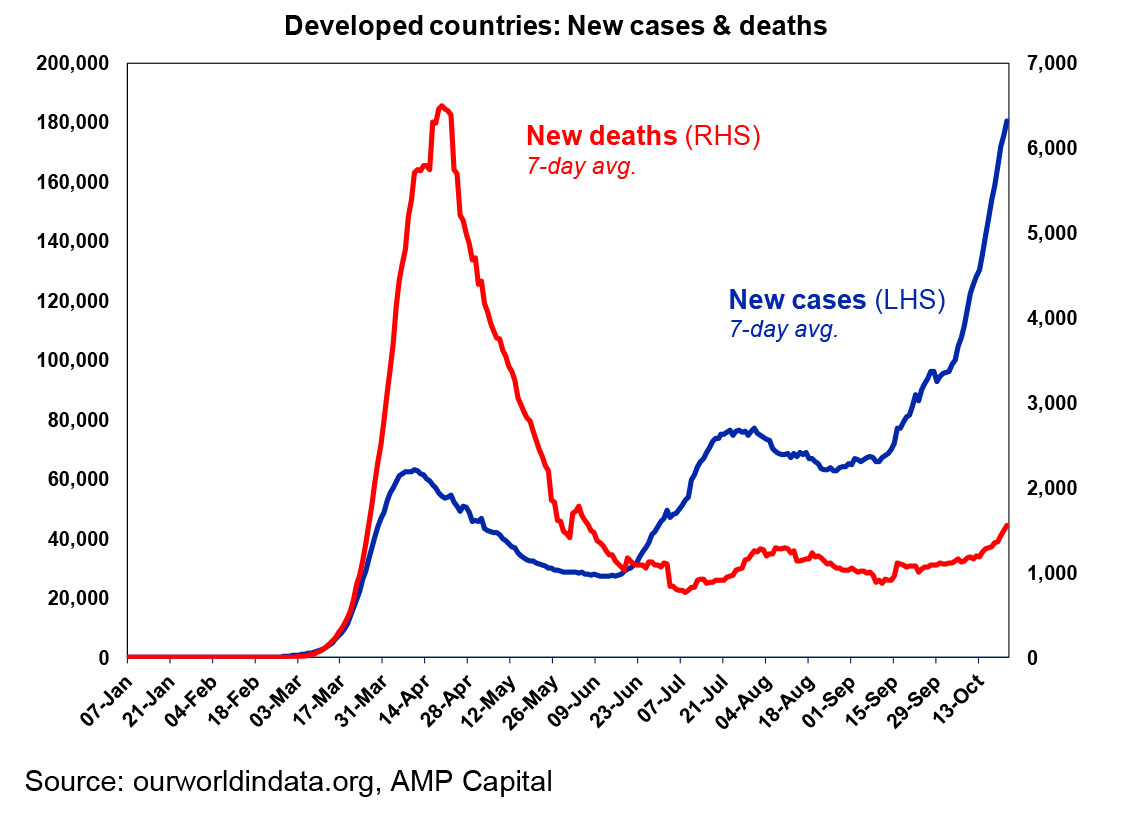

While new deaths in developed countries are starting to edge up they remain well below their April high reflecting more testing which is resulting in more cases in younger people being identified, better treatments and better protections for older people. As long as this remains the case a return to country wide hard lockdowns will likely be avoided in favour of more targeted measures. That said tightening restrictions and self-regulation by consumers risks slowing the recovery and the risk of hard lockdowns is rising in some countries.

Likely reflecting the continuing rise in US cases, our US Economic Activity Tracker has been flat since early September now suggesting the US recovery may be slowing and highlighting the need for more stimulus.

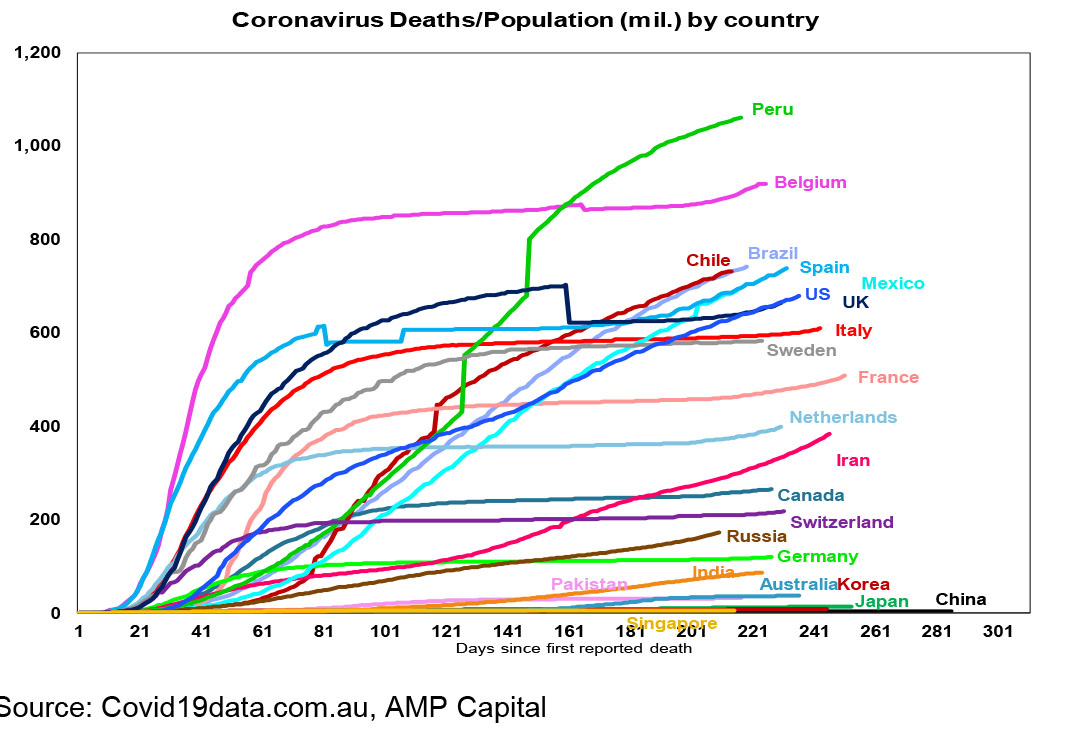

Australia is seeing new local coronavirus cases remaining very low and deaths have fallen sharply. The decline in new cases in Victoria will likely bring forward the reopening of shops. Despite the second wave in Victoria, Australia continues to see coronavirus deaths per capita (of around 36 per million people) run very low compared to countries like the US, UK, Italy, Spain and Sweden (where its been around 600 or more per million). Australia’s better control of coronavirus should contribute to a more confident reopening of the economy which should be positive for Australian assets.

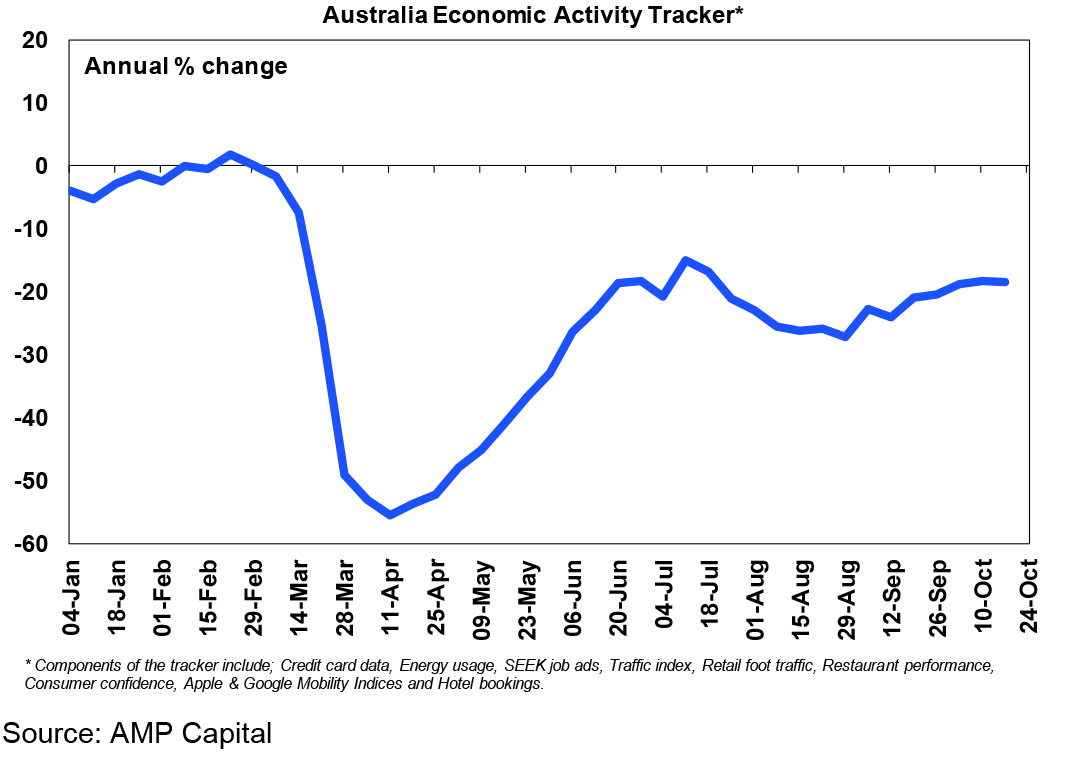

Our Australian Economic Activity Tracker fell slightly over the last week but remains in a rising trend. Expect the trend to remain up as Victoria’s reopening becomes more meaningful economically, as eg shops reopen and more people return to work, and as other states continue to recover.

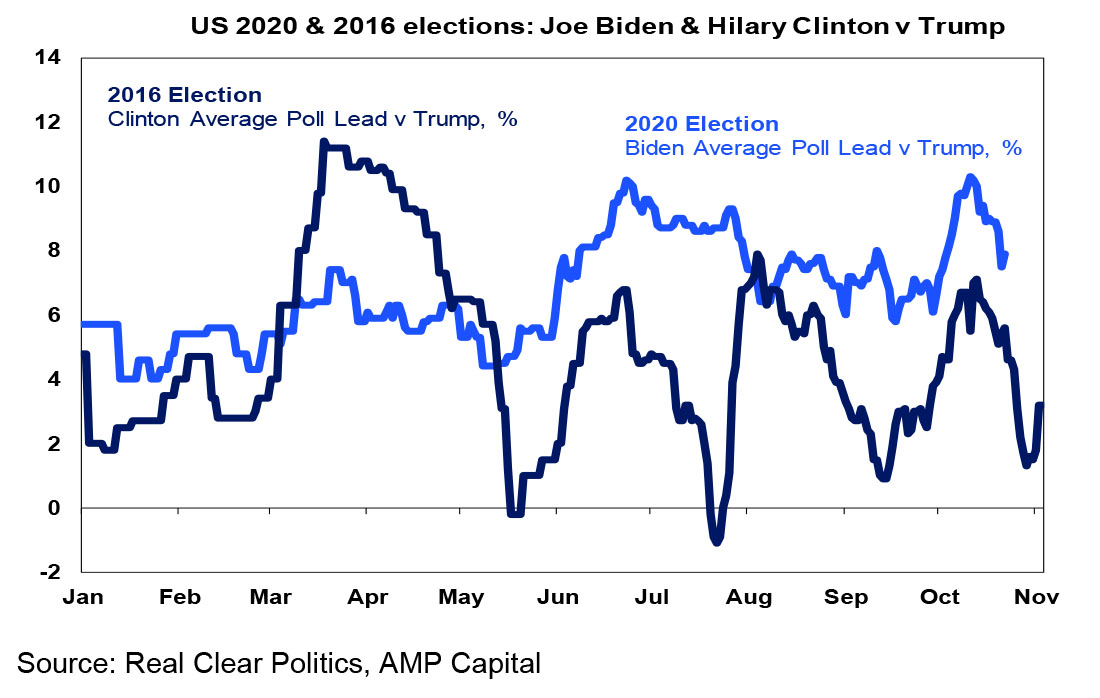

On the election front, the past week has seen Trump claw back some of Biden’s polling lead around 7.9 points. However, it remains in the same 6 to 10% range its been in since June. Meanwhile, Biden’s average poll lead in battleground states is 3.7%, Trump’s approval rating is around 44.5%, the PredictIt betting market puts Biden’s probability of winning at 64% and the probability of a Democrat clean sweep at 54% – both of which are down a bit. The last presidential debate didn’t really add much in terms of what each would do and US futures moved less than 0.1% between the beginning and the end of the debate, but President Trump’s more civil, calm and reasonable approach this time around may work slightly in his favour.

Trump has the benefit of incumbency – as incumbents usually get re-elected, crowds – as his big rallies generate enthusiasm, shy voters, his better rating on the economy and the fear that Biden will take a hard left turn if he wins and there is still more than a week to go.

Working in favour of Biden is the recession, the rising trend in coronavirus cases, a much lower level of undecided (presumably some of whom are shy) voters compared to 2016, record early voting (30 million so far compared to just 6 million at the same point in 2016) suggesting high (likely Democrat) turnout and Biden’s wider more stable poll lead compared to Clinton’s in 2016 (see the next chart). Financial markets are sending mixed signals: a rise in the US share market in the 3 months prior to the election has historically pointed to a victory by the incumbent and vice versa for a fall (with 87% accuracy) and so far its up but the relative performance of US stocks likely to benefit from Biden versus those likely to benefit from Trump is also up according to research house Strategas pointing to a Biden victory.

At a very high level the main issues in the US election of relevance for global investment markets are tax, fiscal stimulus, regulation and trade wars. There are basically three outcomes:

- Trump wins with Democrats retaining the House – taxes and regulation will remain low which may provide a short term knee jerk boost to US shares but trade wars with China and possibly Europe and Japan would likely ramp up again next year which would be relatively bad for global shares (including Australian shares) and good for the $US.

- Biden wins but with the Republicans retaining the Senate – this would mean Biden’s proposed tax hikes won’t pass into law, less fiscal stimulus and periodic fiscal battles but less trade wars and more predictable US policies. This would be neutral for US versus global shares, but historically this combination has been the best outcome for share markets (beyond initial knee jerk reactions).

- Biden wins with a Democratic clean sweep – this will likely mean significantly more fiscal stimulus, less trade wars and more stable US policies but higher corporate tax in the US and more regulation. Global shares would likely benefit more than US shares and the US dollar would likely fall. Historically this has been the second-best outcome for share markets.

Of course, the worst outcome for share markets in the short term would be a contested election, but a clear initial win by either side would head this off. Of course, the record level of early postal votes means that it may take longer to get a result as it takes longer to count them, and counting can’t start till after polls close.

The soap opera around a pre-election fiscal stimulus continued over the last week. While there seems to have been convergence towards the Democrats desire for a $2.2 trillion package, differences still remain and it remains unclear that enough Republican Senators would support it. The main risk is that if its not passed into law prior to the election it would get harder after the election in the event that Biden wins but Republican’s retain control of the Senate (as Republican’s would likely return to fiscal conservatism).

President Trump’s comments over the last week that “people are tired of hearing [coronavirus adviser] Fauci and all these idiots [other health officials]” reminded me yet again of The Pet Shop Boys satirical song from last year “Intelligent people have had their say…Let’s Give Stupidity a Chance.” I know I have given this song a whirl before but perhaps this an anthem for our times. That said, Jacinda Arden’s re-election in New Zealand reminds us that all is not lost. She reminds me of Try A Little Kindness. Such a middle of the road song from 1969 – but the lyrics are so insightful!

Major global economic events and implications

Most US data was good. While the Fed’s Beige book described US economic growth in most districts as “slight to modest” housing data was strong with another surge in existing home sales, home builder conditions at their highest level in over 35 years and another strong rise in permits to build new homes and jobless claims fell.

So far about 25% of US S&P 500 companies have reported September quarter earnings but 84% have surprised on the upside and consensus earnings growth expectations for the quarter have been revised up from a fall of -21%yoy to -18%yoy and this is likely to end up around -12%yoy.

The surge in new coronavirus cases in Europe is weighing with Eurozone consumer confidence and French business confidence down in October.

Brexit trade deal talks seem to be making some progress with the EU’s negotiator indicating that a deal was within reach.

Japanese exports continued to rebound strongly in September consistent with improving global trade.

Chinese September quarter GDP rose a bit less than expected but its up 4.9% from a year ago and consistent with the economy continuing to expand after more than recovering from the coronavirus hit in March. Furthermore, September data for industrial production and retail sales growth continued to accelerate, investment growth remains strong, house prices are rising, and unemployment fell slightly to 5.4%.

Australian economic events and implications

The minutes from the RBA’s last board meeting and a speech by Assistant Governor Kent confirmed the dovish message from Governor Lowe the week before:

- that the RBA is adjusting its forward guidance to focus more on actual as opposed to forecast inflation hitting the inflation target and a return to a tight labour market; and

- that it is considering cutting the cash rate to near zero & buying more government bonds

With the RBA’s updated November economic forecasts likely to show the economy still not meeting its inflation and employment objectives over the next two years we continue to expect a cut in the cash rate, term funding facility lending rate and three year bond yield target to 0.1% and the announcement of a broad based bond buying (QE) program of around $100bn to $150bn spread over the next 12 months. The rate cut will depress variable mortgage rates by around 0.15% (as it will be hard for banks not to pass it on in full given the cheap funding they are getting from the RBA) and the additional bond buying will further depress rates on fixed rate mortgages. It will also keep the $A lower than otherwise would have been the case.

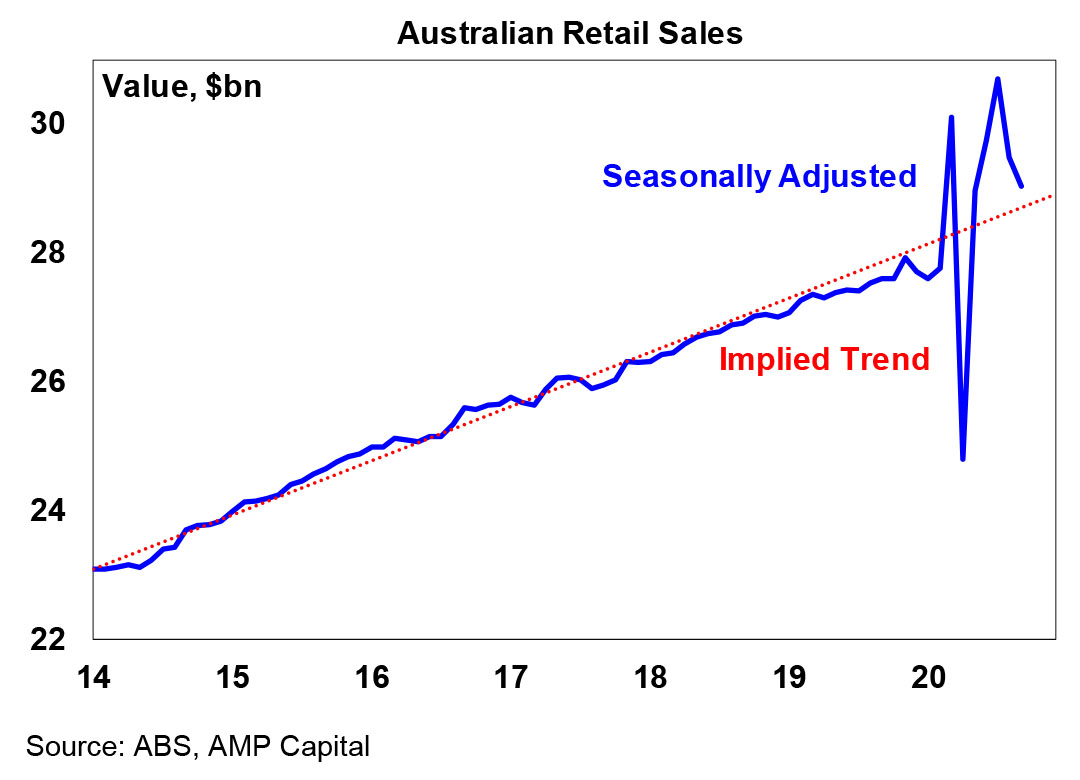

Australian data was mixed, with payroll jobs and retail sales down but the CBA’s October business conditions PMI up on Victoria’s reopening. The decline in payroll jobs should be interpreted with caution as it tends to get revised up. The pull back in retail sales is just returning it to its long-term average after it was boosted around mid year by pent up demand and a diversion of spending from services to goods. Retail sales rose very strongly in the September quarter consistent with some recovery in GDP after the June quarter shutdown driven slump.

What to watch over the next week?

In the US, September quarter GDP (Thursday) is expected to show an annualised 32% rebound as the economy reopened after the -31.4% annualised decline seen in the June quarter. Other data is expected to show continuing strength in new home sales (Monday) and pending home sales (Thursday), a further rise in home prices and durable goods orders but flat consumer confidence (all Tuesday) and weak wages growth and core private final consumption inflation of around 1.7%yoy (both Friday). The flow of September quarter earnings reports will ramp up.

The European Central Bank (Thursday) is expected to leave monetary policy on hold but indicate a strong easing bias in the face of the threat to the recovery posed by rising coronavirus cases. Its expected to increase its QE program in December. Data to be released Friday is expected to show a 9.5% quarter on quarter rebound in September quarter GDP after the -11.8%qoq decline in the June quarter, unemployment is likely to have increased to 8.3% and core CPI inflation for October is likely to have remained at just 0.2%yoy.

The Bank of Japan (Thursday) is expected to leave monetary policy unchanged but with a strong easing bias. September industrial production data is expected to show a further recovery, but underlying jobs data is likely to be weak (both due Friday).

In Australia, September quarter CPI inflation (Wednesday) is expected to rebound by 1.5% quarter on quarter, reflecting the end of free child care and a 7.5% rebound in petrol prices, taking the annual inflation rate to 0.6% year on year. This is after -1.9%qoq and -0.3%yoy in the June quarter. Underlying inflation is expected to remain weak though at 0.2% quarter on quarter and 1.1% year on year. The RBA will of course look through the predictable volatility in headline inflation and remain focussed on the weakness in underlying inflation. Meanwhile, private credit growth (Friday) is likely to have remained soft in September including for housing with the rapid paydown of existing home loans offsetting a rise in new loans. Preliminary trade data will be released Monday.

Outlook for investment markets

Shares remain vulnerable to further short-term volatility given uncertainties around coronavirus, economic recovery, the US election and US/China tensions. But on a 6 to 12-month view shares are expected to see good total returns helped by a pick-up in economic activity and stimulus.

Low starting point yields are likely to result in low returns from bonds once the dust settles from coronavirus.

Unlisted commercial property and infrastructure are ultimately likely to benefit from a resumption of the search for yield but the hit to economic activity and hence rents from the virus will weigh heavily on near term returns.

Australian home prices at present are being protected by income support measures and bank payment holidays but higher unemployment, a stop to immigration and weak rental markets will push prices down by another 5% into next year. Melbourne is particularly at risk on this front as its Stage 4 lockdown has pushed more businesses and households to the brink. Smaller cities and regional areas are in much better shape.

Cash & bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.25%.

Although the $A is vulnerable to bouts of uncertainty about coronavirus, the economic recovery and China tensions and further RBA easing including QE will keep it lower than otherwise, a continuing rising trend is likely to around $US0.80 over the next 12 months helped by rising commodity prices and a cyclical decline in the US dollar.

By Shane Oliver