Weekly market update – week ending 9 October, 2020

Investment markets and key developments over the past week

Share markets rose solidly over the past week on hopes for a stimulus deal in the US, whether before the election or after if there is a Democrat clean sweep. Australian shares benefitted from the positive global lead but also from fiscal stimulus in the Budget with the ASX seeing strong gains across all sectors but particularly in energy, financial, IT, material and consumer discretionary stocks. Reflecting the “risk on” tone bond yields rose, commodity prices rose and the Australian dollar rose as the US dollar fell.

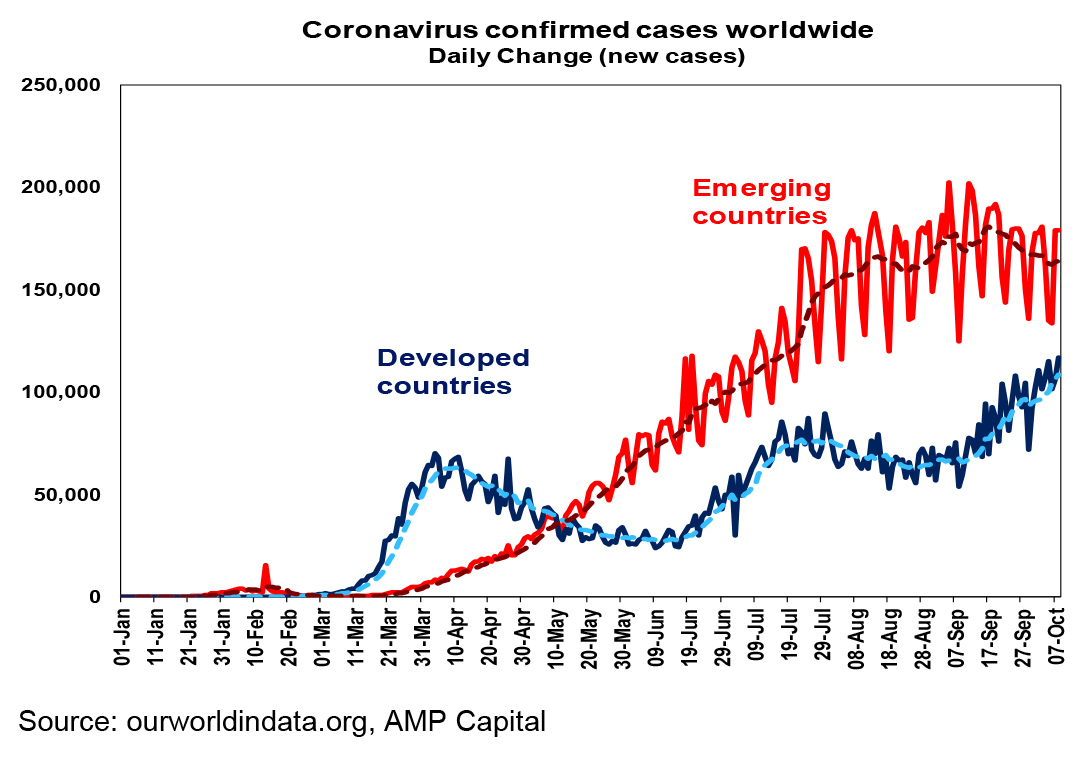

The past week has seen the trend in new global coronavirus cases rise above 300,000 a day, with a downtrend in emerging countries but a continuing rising trend in developed countries.

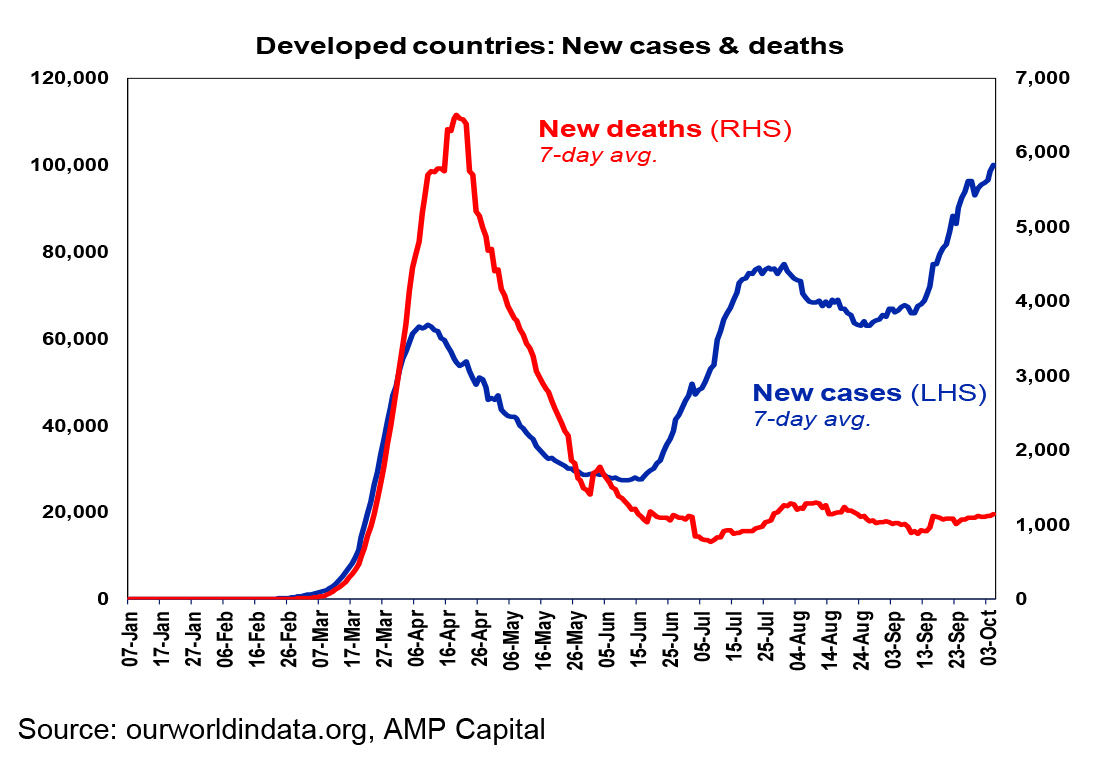

The Eurozone, the UK and Canada are now all seeing strong rising trends in new cases and the US is gradually rising, including in New York again. This is continuing to drive a tightening in restrictions. Fortunately, the number of deaths in developed countries remains well down compared to earlier this year reflecting more testing picking up more younger cases, better treatments (as perhaps seen with President Trump) and better protections for older people and this should help avoid a return to hard lockdowns.

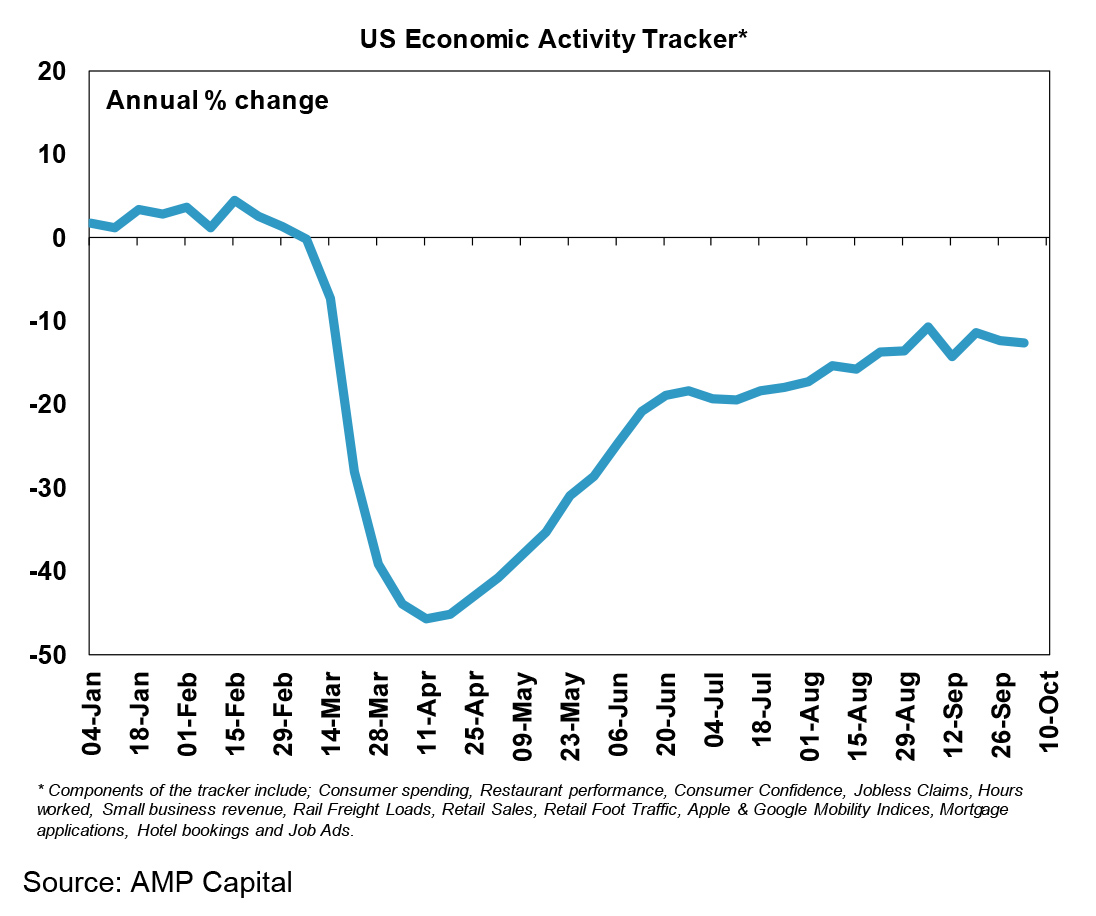

Our US Economic Activity Tracker ticked down again in the last week – with falls in consumer confidence, hours worked, rail freight, and retail traffic – suggesting the US recovery may be stalling again and highlighting the need for additional fiscal stimulus.

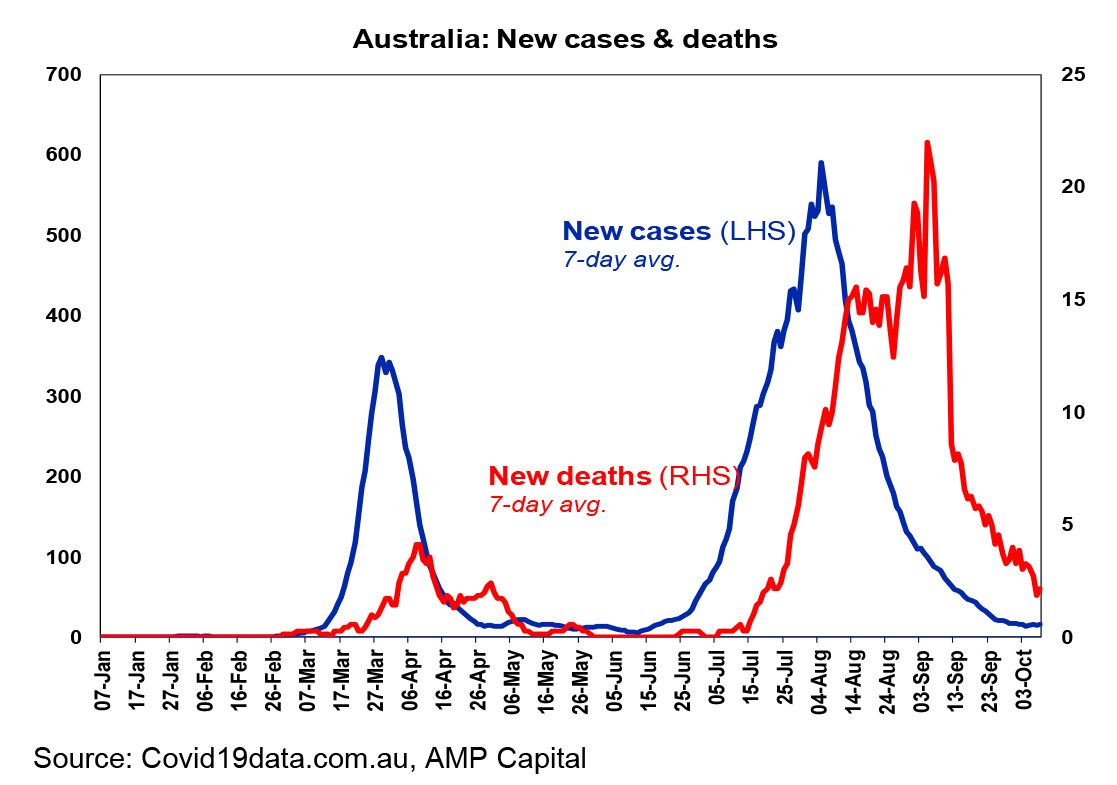

Australia is continuing to see new coronavirus cases remaining low and deaths continuing to fall. Unfortunately, the decline in new cases in Victoria may not be fast enough to see the move to Step Three of the reopening by 19th October. NSW has also seen a spike in new community transmission cases, further delaying a reopening of the Queensland/NSW border.

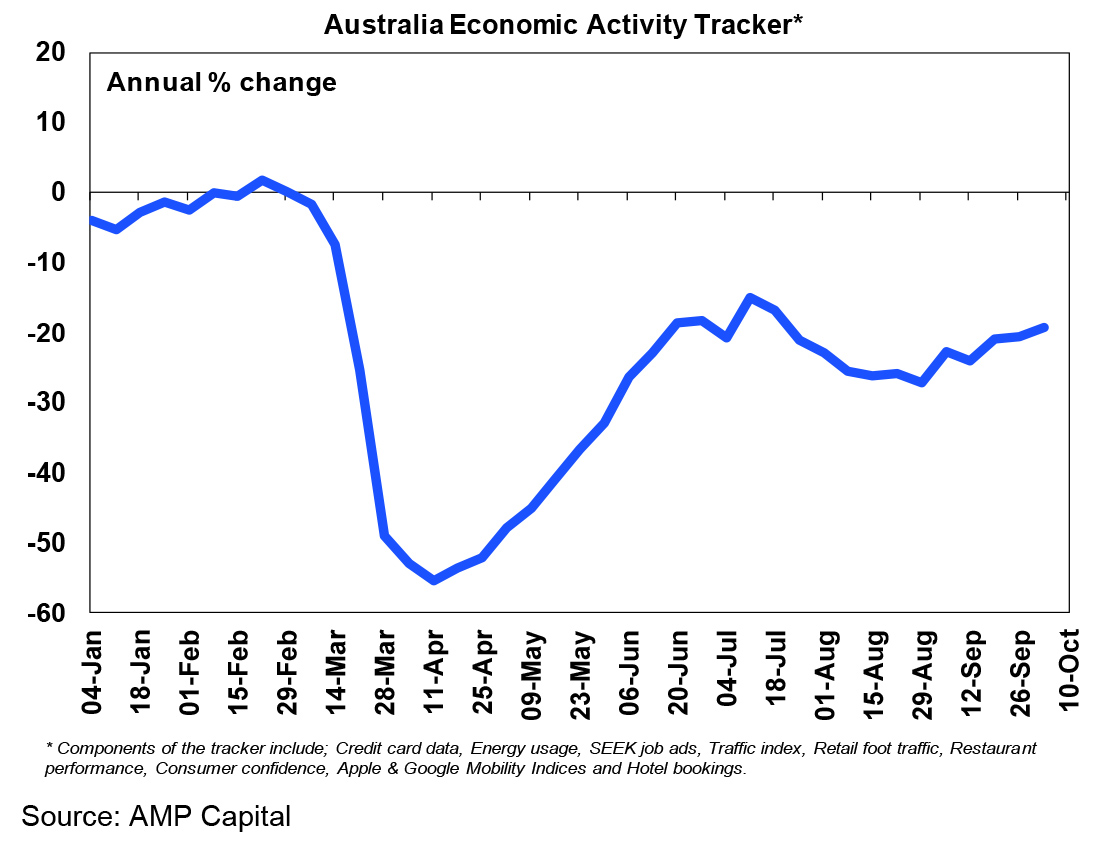

The decline in new cases has seen our Australian Economic Activity Tracker continue to hook up from August lows with gains over the last week in consumer confidence, restaurant bookings, traffic, credit card transactions and mobility. Expect the trend to remain up as Victoria gradually reopens and other states continue to recover.

It might have been hoped that President Trump’s coronavirus infection would lead to a more sensible US response to the virus. Particularly after he said he “learned a lot” about it. But his actions over the last week – the drive-by for fans, the early return to the White House when likely still contagious, the defiant show of removing his mask at the White House balcony, his tweet that coronavirus is less deadly than the flu, etc, at a time when multiple members of his team have become infected – suggest no such thing. And it went crazier when early in the week he tweeted that a fiscal stimulus deal needs to get done, only to then a day later put negotiations on hold till after the election (despite Fed Chair Powell warning of “tragic” risks for the economy) but then do a back flip on the back flip proposing a piecemeal approach (perhaps after some of his team reminded him that he has more to gain from a deal than the Democrats) only to then shift back towards supporting a comprehensive stimulus package after Democrats rejected the piecemeal approach. The trouble is that the two sides remain far apart in terms of how much to spend. So, who knows where this ends up. The good news in all this is that Trump would have been given the absolute best available coronavirus treatments and so his seemingly speedy recovery holds out hope for many others who catch it. It’s interesting that Trump relied on experts (doctors) to fix him rather than some of the things he has advocated over the last six months (like injecting disinfectant)!

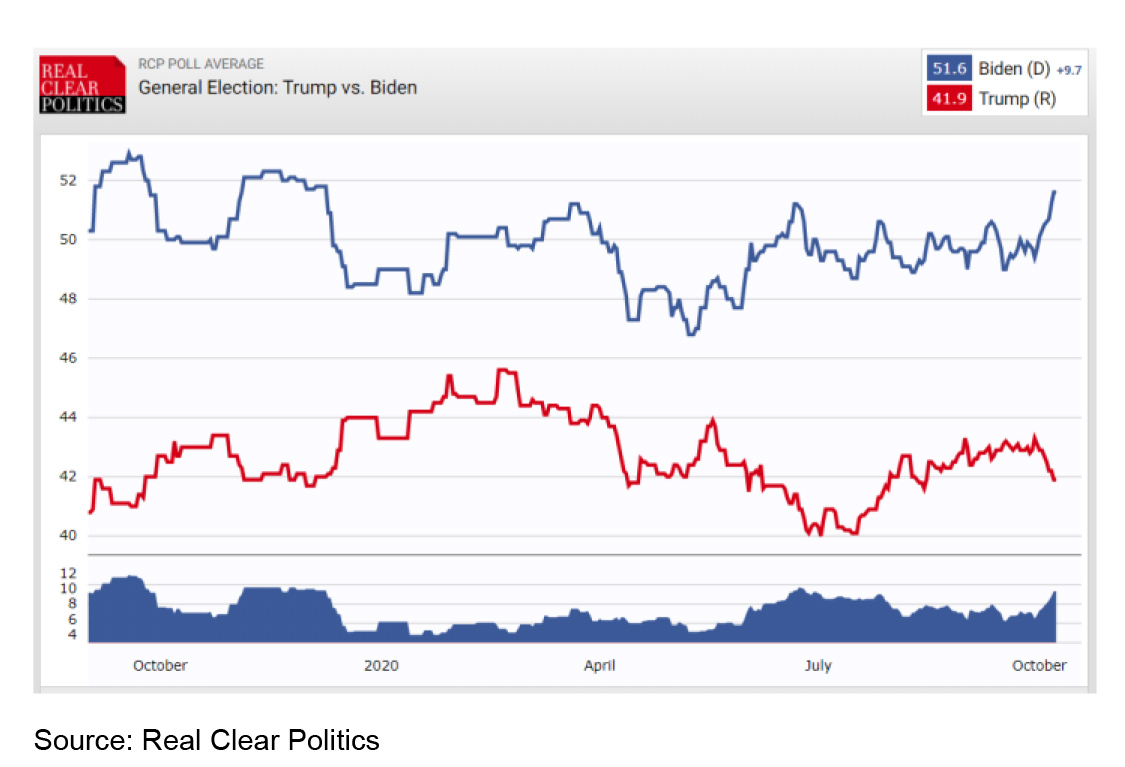

For what it’s worth Trump’s infection doesn’t seem to have provided him with a sympathy boost in the polls. Biden’s average poll lead has risen to 9.7 points, his average poll lead in battleground states has widened to 3.9 points, Trump’s approval rating has fallen over the last week back to 44.4%, and Biden’s lead on the PredictIt betting market is now about 31 points from 12 points before the debate. That said, there are still 3 weeks to go and “shy voters” for Trump could still swing things around.

While a Democrat clean sweep has gone from 50/50 to 60/40 on PredictIt its surprisingly not causing the nervousness in share markets that might have been expected given that it would clear the way for higher taxes and regulation under Biden. This is perhaps because a Democrat clean sweep would also clear the way for more stimulus (after the on again off again mess under Trump) and lead to smoother policy making. Its also worth noting that because new Democrat senators would likely come from conservative states, they would be unlikely to go along with any extreme leftwards policy lurch.

The Australian Budget provides a necessary big further boost to the economy. The Budget provided little in the way of surprise because many of the measures had been pre-announced or leaked. The main criticisms of it were that: it assumes a vaccine next year; the economic assumptions may be too optimistic; that much of the tax cut will be saved; that it exaggerates the actual tax saving for low income earners; that its too focussed on business; and that it will leave too much public debt. No budget is perfect but our response to these is as follows:

- Most forecasters are assuming some sort of vaccine arrives next year and there is a reasonable chance it will. But even the vaccine fails to arrive it doesn’t impact the Government’s decision to provide more stimulus. It would just make it even more important that it did.

- The Government’s economic assumptions are a bit more optimistic than ours but then again, the Budget contained mores stimulus than we were assuming so this could help in achieving the stronger growth forecasts. That said we are of the view that more stimulus will ultimately be required.

- While some of the tax cuts may be saved, because they are permanent they have a greater chance of being spent, even if some is used to pay down debt this will help support future spending and it should be noted that their cost is less than 10% of the overall stimulus of $160bn this financial year.

- While the Government may have exaggerated the size of the tax cuts for those earning $50000 to $90000 (by including last year’s tax cuts in comparisons), they are still getting an extra tax saving of $1080 this year and tax relief has been focussed on this income group in recent years.

- Non-mining investment has been too low for many years now, so it makes sense to provide incentives for business to invest in the interest of boosting spending now and boosting long term growth potential. And the success of the instant asset write-off for tradies shows that such incentives work.

- The budget blow out will add to public debt and its hard to see it being paid down anytime soon but with borrowing rates so low its affordable and not undertaking stimulus spending would have meant a far weaker economy and worse debt problem down the track.

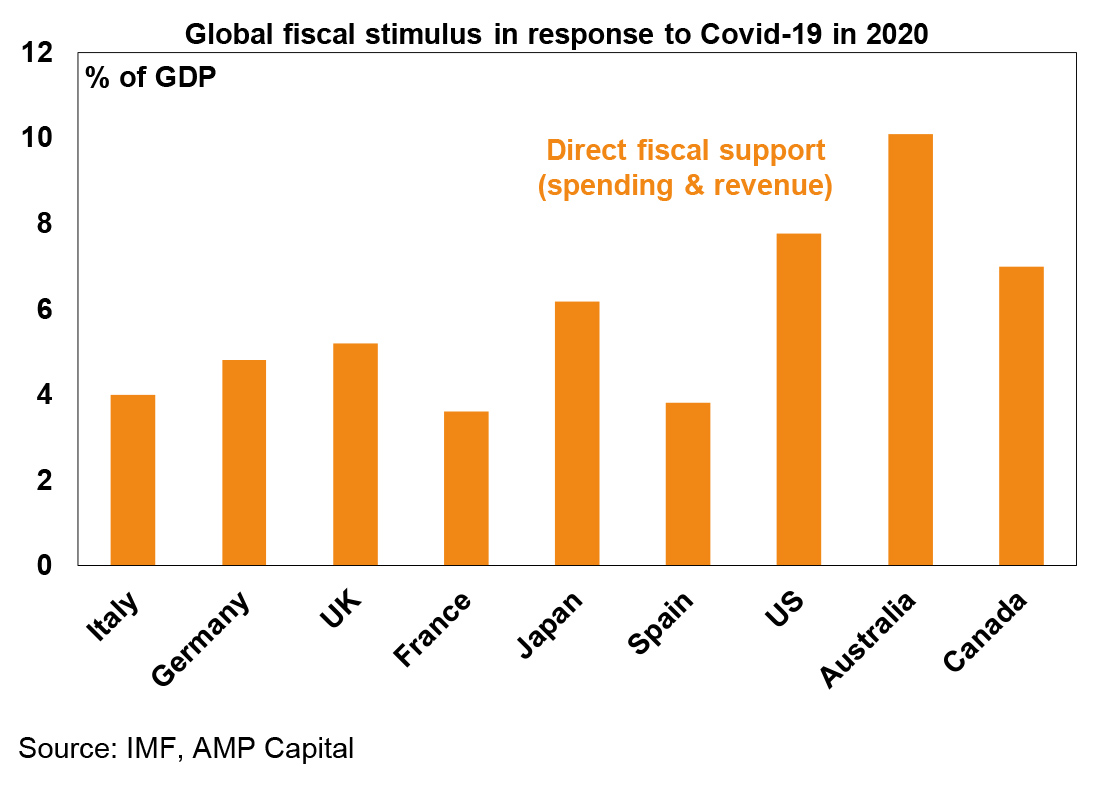

While there is a tendency to get lost in the details of the Budget and each spending measure (often along political lines), the key takeaway from it is that it is actually pumping significantly more stimulus into the economy. This amounts to an extra $41bn (or 2% of GDP) this financial year taking total stimulus this financial year to $160bn. Following the Budget’s further ramping up in stimulus we estimate that total direct fiscal support for the economy this calendar year as a share of GDP is now just above 10%, which is well above that in other comparable countries including the US where extra stimulus has been delayed. This in turn is helping protect the economy and ensuring a faster than otherwise recovery.

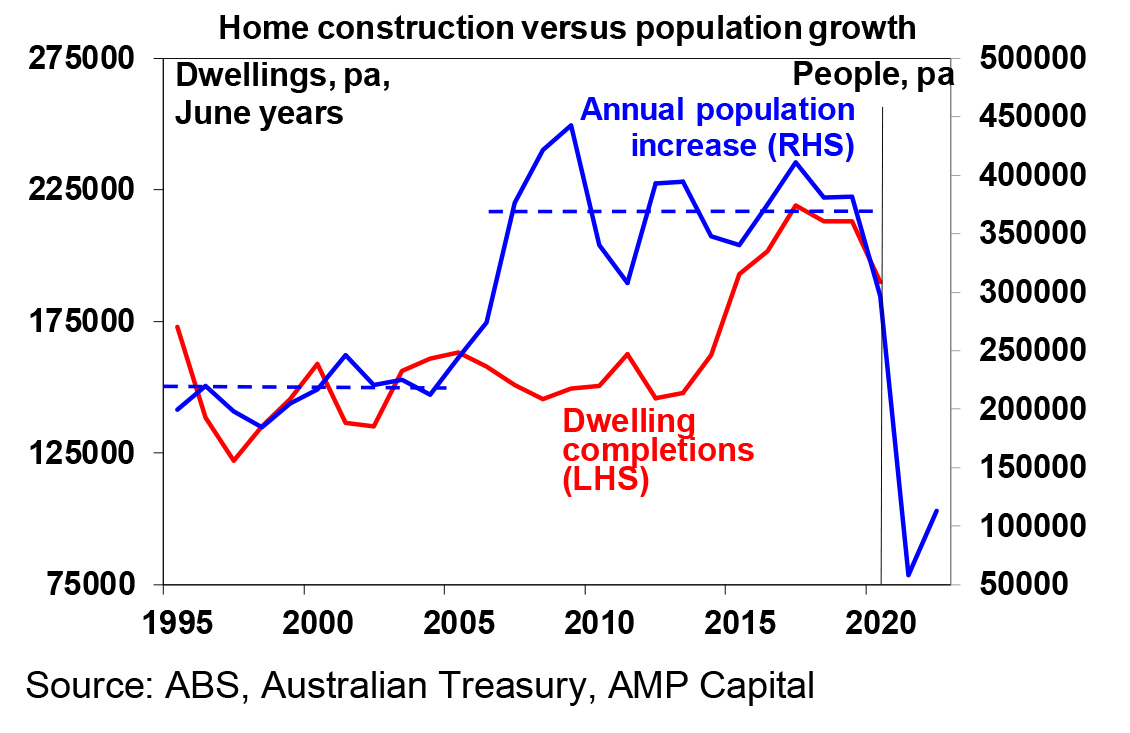

Big hit to housing demand from net immigration going negative. One thing that did surprise us in the Budget is the projection for negative net immigration of -72,000 this year and -22,000 for next year. While I get there won’t be many immigrants coming here it’s a bit hard to understand why the Government now projects a net outflow – particularly given Australia’s far better control of coronavirus than most countries and it being a better place to be in a lockdown. Be that as it may, if the projections are correct it implies that underlying demand for housing this year will be down by just over 100,000 dwellings and it will be down by another 87,000 dwellings next year. This is a bigger hit than I have been assuming. With the Government keen to support housing construction the risk is that we go from years of having a housing supply shortfall to an oversupply which will mean downwards pressure on rents and home prices – particularly in Melbourne and Sydney which are more dependent on immigration. While the Government projects a return to net immigration of 201,000 in 2023-24 its hard to see this happening in the face of still high unemployment.

With the death of Eddie Van Halen I can’t go past Jump this week. I got to Van Halen via David Lee Roth’s cover of The Beach Boys’ California Girls (where you can hear Carl Wilson on backing vocals). Also worth checking out is James Corden’s “cover” of Paul McCartney’s Maybe I’m Amazed (or Immune).

Major global economic events and implications

US data was mixed with a decline in job openings and flat initial jobless claims, but an ongoing decline in continuing jobless claims and an unexpected rise in the services conditions ISM index to a strong 57.8. Meanwhile, the minutes from the Fed’s last meeting hinted that it may be heading towards firmer guidance in relation to its QE program. Ramped up QE would likely be necessary if there is no agreement on further stimulus in the US.

ECB President Lagarde highlighted the shakiness of the recovery and reiterated that the ECB is prepared to use all tools to support growth. Looks like more easing coming.

The UK warned that it would quit Brexit talks unless a clear deal is in sight next week. This could just be bluffing but who knows. Don’t forget there is far less at stake in this for the EU for which only 5-10% of its exports go to the UK and which has become more united through the coronavirus crisis than the UK for which nearly 50% of its exports go to the EU.

Japanese wages continued to fall in August and household spending remained weak but the Economy Watchers survey for September showed a continuing recovery in household and corporate conditions.

Australian economic events and implications

Australian data was mostly good. While the trade surplus surprisingly weakened in August this reflected a fall in exports due to a sharp fall in gold exports which can be volatile and a recovery in imports which is consistent with stronger demand in the economy. Meanwhile business conditions and confidence improved in September according to the NAB business survey, job ads rose again in September and payroll jobs rose over the two weeks to 19th September suggesting the payroll jobs recovery may be resuming after a flat period since July due largely to Victoria.

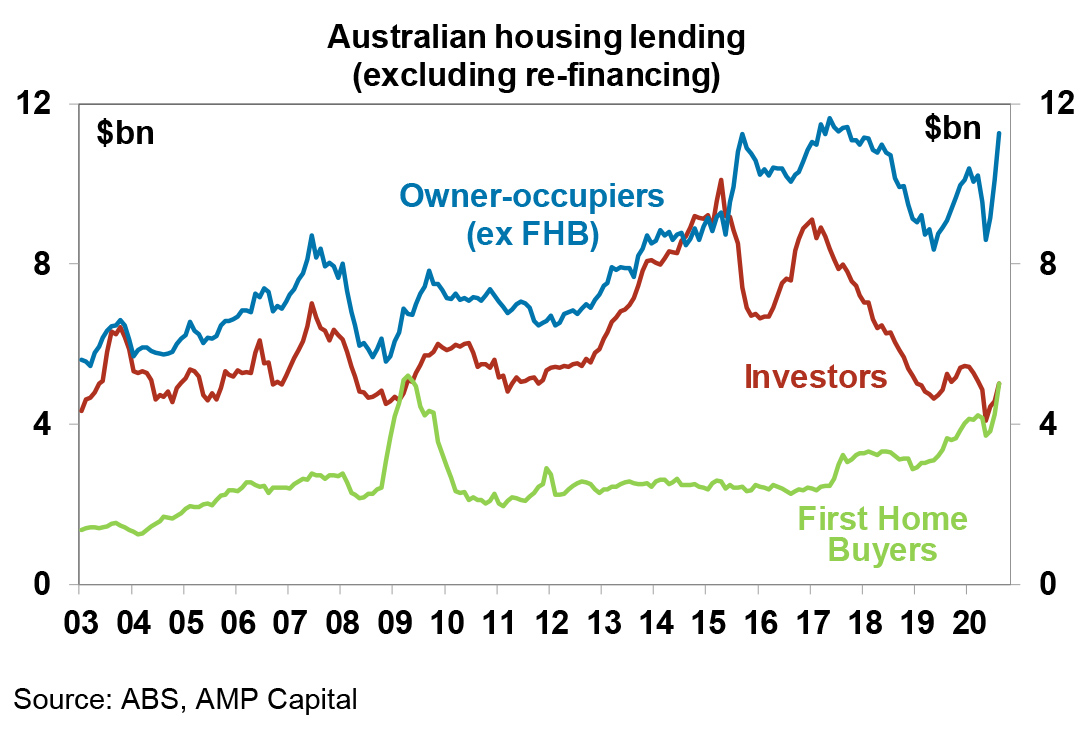

Housing finance commitments surged another 12.5% in August with owner occupiers and investors seeing strong increases and an 18% rise in finance for first home buyers. The surge in housing finance partly reflects a catchup to the low processing of loans in April and May but is also being driven by record low rates and various incentive schemes and is occurring before the removal of responsible lending rules. The surge in housing finance taken in isolation points to a potential surge in house prices. Working against this though are a likely increase in distressed sales as bank payment holidays and various income support measures end and the huge reduction in underlying demand flowing from the collapse in immigration.

The RBA’s latest Financial Stability Review noted that the Australian financial system can withstand the downturn and support the recovery, but that “business failures will rise substantially” as loan deferrals and income support end and that while the finances of most households are faring well “the number of households in financial stress has increased and will increase further.”

Meanwhile the Melbourne Institute’s Inflation Gauge for September saw underlying inflation falling to just 0.1%yoy, pointing to a further fall in underlying inflation in the September quarter to around 0.3%yoy.

While the RBA left the cash rate on hold at its October meeting it strongly hinted at further easing to come by noting that it “continues to consider how further monetary measures could support jobs as the economy opens up further.” Our base case remains that the RBA will cut the cash rate, the Term Funding Facility rate and the three year bond yield target to 0.1% and will likely do this at its November meeting after it has updated its forecasts which will likely show that its employment and inflation objectives are still not going to be met over the next two years at least. Over the next six months we also see the RBA moving towards inflation average targeting and therefore tweaking its forward guidance to say that it won’t raise the cash rate until full employment is reached and inflation is sustainably within the 2-3% target band. And we also see it adopting a more traditional quantitative easing program extending bond buying beyond the three-year bond.

What to watch over the next week?

In the US, expect to see continued strength in the NFIB small business survey (Tuesday) and in NY and Philadelphia regional manufacturing conditions indexes for October (Thursday) and solid gains in September retail sales and industrial production (Friday). Expect to see a 0.2% rise in core CPI inflation (Tuesday) taking the annual rate to 1.8%yoy, which suggests core private consumption deflator inflation of around 1.5%yoy. September quarter earnings reports will start to flow with consensus expectations for earnings to fall by -22% year on year, up from -32%yoy in the June quarter.

Chinese data is expected to show export growth running around 9.5%yoy but imports about flat (Tuesday), a fall in headline inflation (Thursday) to around 2%yoy and continuing solid growth in credit.

In Australia, expect a rise in consumer confidence (Wednesday) on the back of the tax cuts and extra stimulus in the Budget and October jobs data (Thursday) to show a flat employment and unemployment rising to 7% reflecting a further recovery in participation. A speech by RBA Governor Lowe (Thursday) will be watched closely for any clues regarding further monetary easing.

Outlook for investment markets

Shares remain vulnerable to further short-term volatility given uncertainties around coronavirus, economic recovery, the US election and US/China tensions. But on a 6 to 12-month view shares are expected to see good total returns helped by a pick-up in economic activity and stimulus.

Low starting point yields are likely to result in low returns from bonds once the dust settles from coronavirus.

Unlisted commercial property and infrastructure are ultimately likely to benefit from a resumption of the search for yield but the hit to economic activity and hence rents from the virus will weigh heavily on near term returns.

Australian home prices at present are being protected by income support measures and bank payment holidays but higher unemployment, a stop to immigration and rent holidays will push prices down by another 5% into next year. Melbourne is particularly at risk on this front as its Stage 4 lockdown has pushed more businesses and households to the brink.

Cash & bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.25%.

Although the $A is vulnerable to bouts of uncertainty about coronavirus, the economic recovery and US/China tensions, a continuing rising trend is likely to around $US0.80 over the next 6-12 months helped by rising commodity prices and a cyclical decline in the US dollar.

By Shane Oliver