Weekly market update – week ending 4 December, 2020

Investment markets and key developments over the past week

Global share markets mostly pushed higher again over the last week helped by reasonably good economic data, renewed stimulus talk in the US and ongoing vaccine optimism. Eurozone shares slipped a bit, but other major markets rose with US shares reaching a new record high. Reflecting the strong global lead, stronger than expected Australian economic data and a surging iron ore price the Australian share market rose again for the fifth week in a row with gains being led by resources, IT, property and consumer staple stocks. Bond yields mostly rose consistent with “risk on” sentiment as did prices for oil (helped by an OPEC agreement to more gradually ease production cuts), metals and iron ore and the $A rose to its highest since mid-2018 against a falling $US.

After huge gains shares remain overbought and at risk of a short-term pause. However, more upside is likely as momentum is very strong, the Santa Claus seasonal rally normally gets underway from mid-December and investors are yet to fully discount the potential for a very strong economic and profit recovery next year as stimulus combines with vaccines. Cyclical recovery shares like resources, industrials and financials are likely to be relative outperformers as they have been laggards through the pandemic, and this should benefit the Australian share market over US shares. More upbeat comments and upgrades than normal through the recent Australian AGM season are also bullish for the Australian share market. With the $A now having broken through resistance at around $US0.74, its likely on its way to around $US0.80 over the year ahead on the back of rising commodity prices and a falling US dollar. RBA quantitative easing may be able to slow the $A’s ascent but its unlikely to be able to stop it.

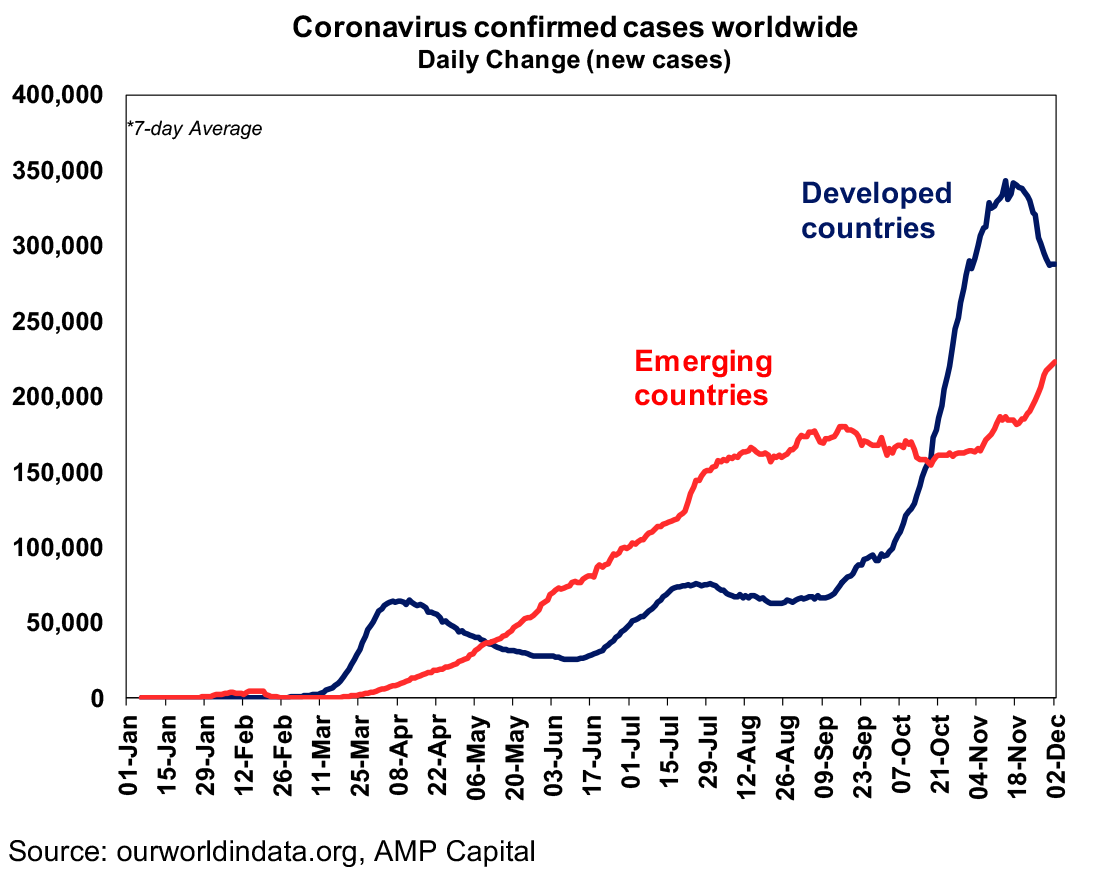

The flow of new global coronavirus cases remained stable over the last week with a rising trend in emerging countries offset by a declining trend in developed countries. Europe and the UK are continuing to see a sharp decline in new cases as lockdowns impact and the US may also be starting to roll over, although testing delays associated with the Thanksgiving holiday may be impacting and pressure on its hospital system indicates a high risk of more lockdowns. Japan and Canada remain in uptrends, with Japan at risk of another lockdown.

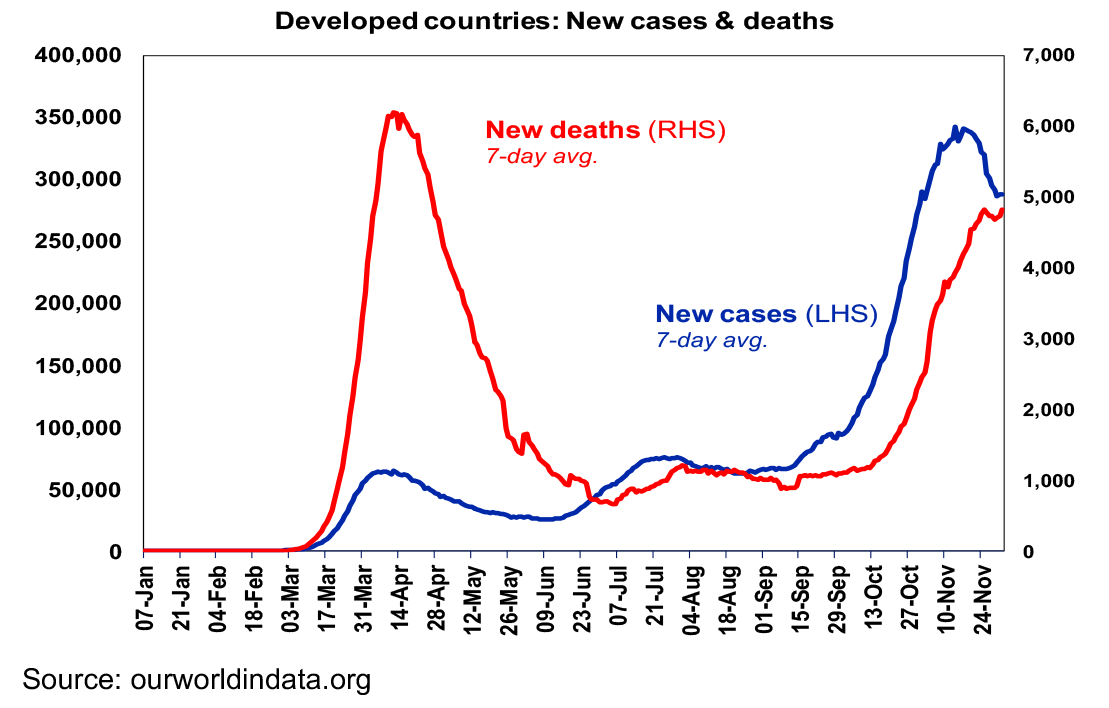

The decline in new cases in developed countries, led by Europe, is starting to see deaths peak. The US bears watching here though.

The deployment of vaccines is getting closer with the UK approving the Pfizer vaccine for emergency use and other countries and vaccines likely to follow rapidly. Allowing for production plans (including somewhat slower production from Pfizer this year) and those who have already had the virus (which is likely to be far above the 65 million officially reported) there is a good chance of reaching herd immunity globally by the end of 2021 or early 2022. This is continuing to help share markets look through the current problems with the virus and its economic impact.

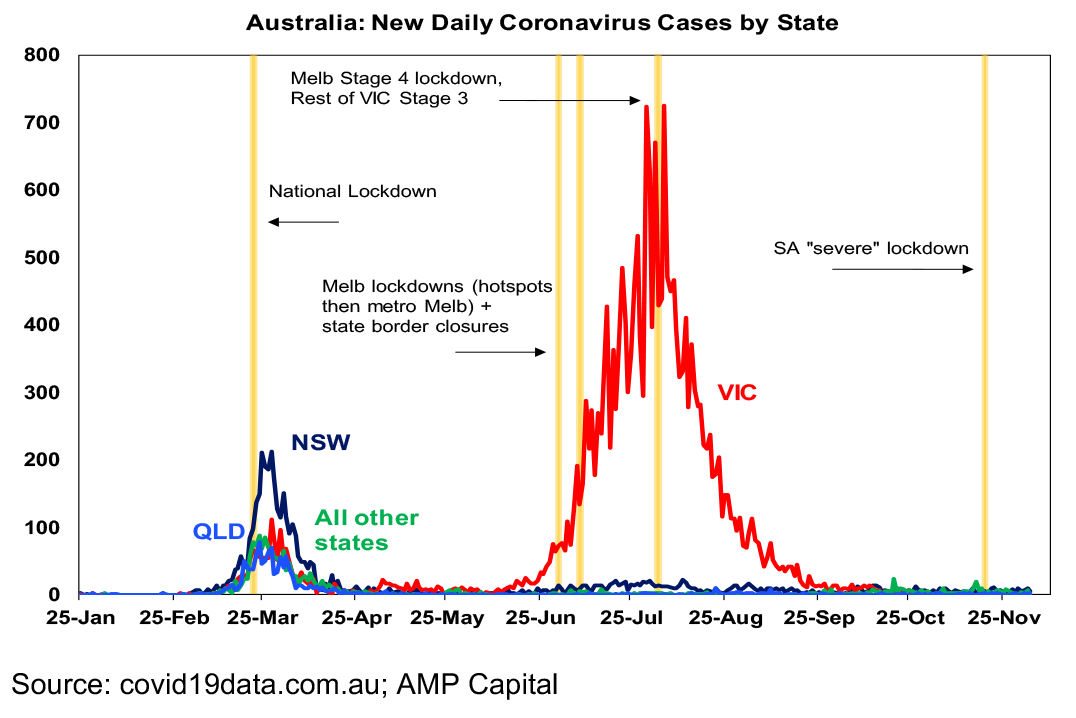

Australia is continuing to report a low level of new covid cases – with Victoria going 35 days without a case, SA appearing to get its cluster under control but NSW seeing concern around an infected hotel quarantine worker.

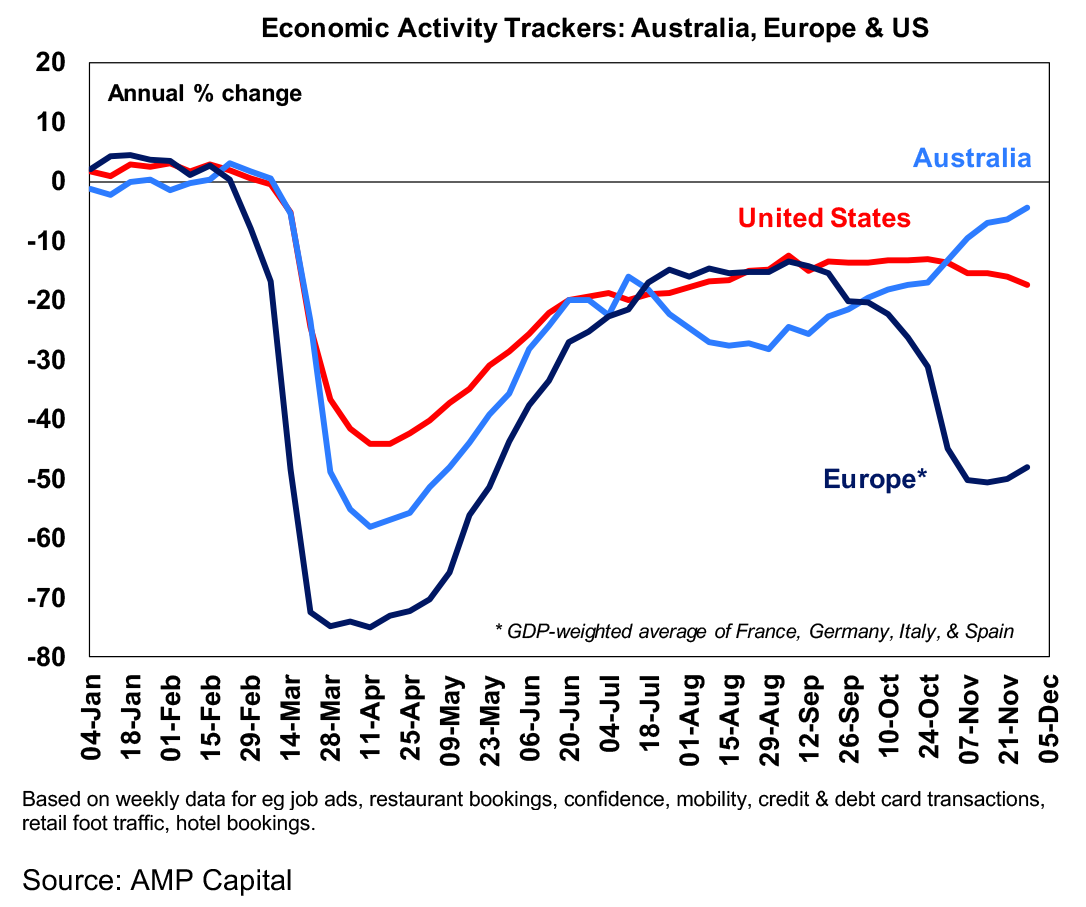

Our weekly Economic Activity Trackers remain divergent. In Europe they have started to edge up a bit after a sharp fall driven by lockdowns and may start to improve more significantly in the next month or two if lockdowns are eased. Our US tracker is edging down suggesting a slight negative economic impact from the resurgence of coronavirus but nothing like that seen in Europe due to the absence of a hard lockdown in the US. By contrast our Australian Economic Activity Tracker is continuing to edge up consistent with the control of coronavirus in Australia and the reopening of the economy – notably in Victoria but also with relaxing distancing requirements in other states and border re-openings. In fact, it’s now down just 4.5% from a year ago which is a huge improvement from being down 58% at its low point in April. This all suggests that Australia will see continuing solid economic recovery this quarter, while the US may be slower, and Europe will see a contraction. All things being equal this should be relatively positive for the Australian share market and the $A.

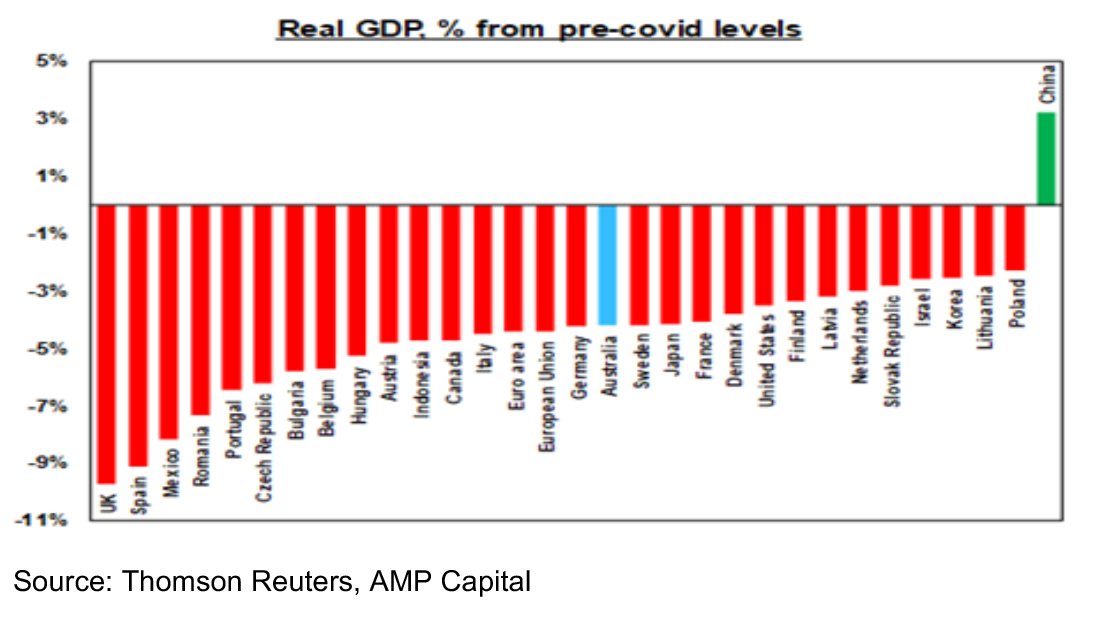

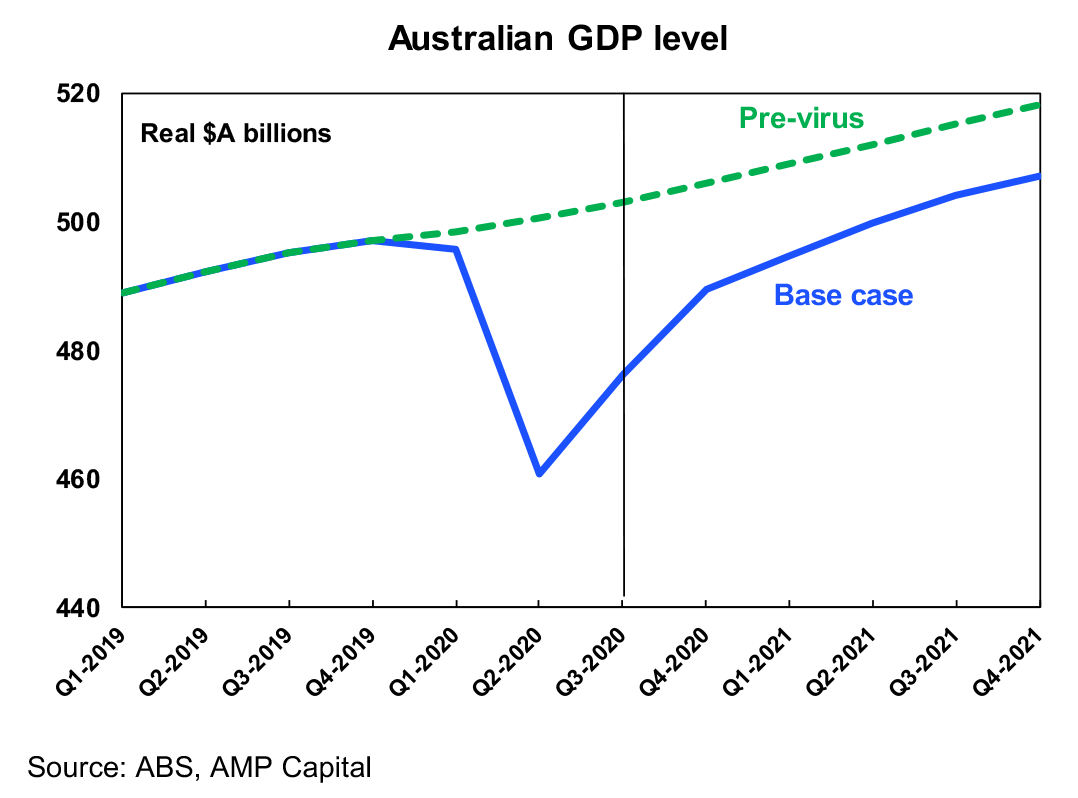

The Australian economy still has a way to go to a full recovery from the covid hit, but at least September quarter GDP data showed that the recession is over and its heading in the right direction. The bad news is that GDP is still down 4.2% from its pre-covid level which still exceeds the biggest slumps since the end of WW2. The good news though is that September GDP rose by a stronger than expected 3.3% indicating that the economy is recovering, were it not for the lockdown in Victoria it would have rebounded by around 5.3%, the household saving rate remains very high at 18.9% suggesting a lot of pent up demand remains that can be unleashed as confidence improves and Victoria is reopened and more timely data reflected in our Australian Economic Activity Tracker points to a continued strong recovery this quarter.

While Australia’s September quarter GDP rebound was less than that seen in the US (+7.4%), the Eurozone (+12.6%) and the UK (+15.5%) this reflected a much smaller first half contraction, a more cautious and covid safe reopening and Victoria’s lockdown. Looking forward, better virus control should augur well for continued recovery in contrast to Europe which is likely to contract this quarter and the US which may slow.

Our rough estimate is that Australian GDP growth in the current quarter will be around 2.8% with much of that coming from Victoria, and that GDP will be back to its December quarter 2019 pre-covid level by mid next year. We have now revised our 2020 growth forecast to -2.5% (up from -3.5%) and see 2021 growth of 4.5% and 2022 growth of 3%.

RBA on hold, but further easing via QE remains likely. While September quarter GDP growth was stronger than expected, the recovery will still be “uneven and bumpy” (in the words of Governor Lowe) with lots of “spare capacity” in the form of unemployment and underemployment for some years to come. So we agree with the RBA that a cash rate hike remains unlikely for three years at least, and with negative rates remaining “extraordinarily unlikely” an expansion in the RBA’s bond buying program is likely at some point in the first half of next year, particularly to provide a brake on the ascent of the Australian dollar which we see rising to around $US0.80 over the next 12 months.

What about the tensions between Australia and China? So far these are having a big impact on affected goods exporters – mainly in agriculture, but the macro economic impact is minor as they only relate to around 0.3% of GDP and they are not stopping a recovery in the economy which is due to reopening of domestic activity. If things remain as they stand the tensions might knock 0.25% of GDP growth in the years ahead. However, a bigger impact will occur if the tensions start impacting bulk commodities which are around $114bn annually or 6% of GDP of which iron ore is around $85bn. But this would also involve a bigger hit to China’s economy – as Australia accounts for 50% of iron ore exports globally so it would not be possible for China to replace all its Australian iron ore imports from other sources. But it’s a key risk for next year. Both sides seem to have gripes with each other – the key is to sit down together at a high level and talk it though. Hopefully this should be easier as the US moves under Joe Biden to a more diplomatic approach to resolving its issues with China. Note that tensions between China and Japan have flared up for periods in recent years only to die down again and in the 1980s and 1990s Australia often had tensions with Singapore and Malaysia only to see it resolved after a while.

Turning to the US, “Squattergate” is now into its fifth week, but attention is now shifting to Biden as it should be. Trump’s quixotic bid to declare votes for Biden illegal continues to flounder. Attorney General Barr – one of Trump’s biggest allies – has said that the Justice Department has not uncovered significant fraud that would alter the election outcome. Trump is actually correct in his comment a few days back that “I know one thing, Biden did not get 80 million votes.” In fact, he now has more than 81 million votes, which is nearly 7 million more than Trump. And despite various recounts and challenges his lead in the key battleground states that he won ranges from 10,500 in Arizona to 154,000 in Pennsylvania. Trump only has 47 days left but could still throw hand grenades between now and January 20.

Meanwhile, progress appears to be starting up again towards a new stimulus package in the US. Biden has indicated a desire for stimulus prior to his taking office and this has given cover for House Speaker Pelosi to back down from her $2.4bn proposal. Something closer to $908bn – as proposed by a bipartisan group of Senators – is looking more likely for now given Senate Republican’s opposition to another huge package. A bigger stimulus is possible next year – particularly if Democrats win control of the Senate via the two special elections in Georgia (which is possible particularly if Trump keeps stirring up trouble in Georgia, but not probable…betting odds are currently around 40%). In other policy comments Biden has said: he still wants to raise taxes in mid-2021 (but in the absence of winning both Georgia Senate seats this will only occur if some sort of deal is cut with Senate leader McConnell); he is ready to go back to the Iran nuclear deal which would mean increased global oil supply (suggesting little impact from last week’s assassination of a top Iranian nuclear scientist); and he won’t remove tariffs straight away on China (this is no surprise and suggests they will be used as a bargaining tool – and he may remove tariffs on other countries).

A year ago, Christmas was marred by the horrible bush fires in Australia and it ushered in a year that many would rather forget. But coming into this Christmas there are some reasons for cheer with light at the end of the covid tunnel, more thoughtful and respect leadership returning to the US, Australia has done an excellent job in protecting its people and economy from the virus and most of Australia has exited the drought (eg Sydney dam levels are around 93% which is around double year ago levels). There used to be a time when pop singers did Christmas songs it was just another soppy cover of old Christmas standards…but The Beach Boys changed all that with Little Saint Nick. For the purists Elvis’ Merry Christmas Baby from 1971 is also a classic.

Major global economic events and implications

US data was mostly good with strong business conditions ISM readings for November, a strong rise in construction and solid home sales but mixed jobs indicators.

Eurozone unemployment fell slightly to 8.4% in October from 8.5%, but core CPI inflation remained weak at 0.2%yoy.

Japanese industrial production recovered more than expected in October and the ratio of job openings to applicants improved for the first time since April last year.

Chinese business conditions PMIs for November improved further and are all at solid levels consistent with an ongoing solid economic expansion.

Australian economic events and implications

Apart from the stronger than expected GDP rebound most other data releases in Australia were solid with building approvals up again in October helped by HomeBuilder which has now been extended and housing finance rising to a new record high, CoreLogic showing a return to solid growth in home prices in November, mostly solid PMI readings, the trade surplus rebounding in October on the back of a strong iron ore exports, car sales rebounding to be well up on a year ago and final retail sales confirming solid growth in November. Credit growth remains soft though as homeowners continue to pay down existing loans faster than normal and the MI Inflation Gauge points to continuing low inflation.

Its now clear that the combination of reopening, government incentives, easing lending standards and ultra-low rates are more than dominating the drags of reduced underlying housing demand from the hit to immigration, weak rental markets and higher unemployment and underemployment and for most areas this will drive further price gains next year. Inner city Melbourne and Sydney are the most vulnerable to the hit to immigration, whereas outer suburban areas and houses, other cities and regional centres are likely to continue to perform well.

At present, the rebound in house prices is not a concern for the RBA as its more focussed on reducing unemployment. But it may become more of an issue later next year if house price gains gather pace, debt starts to rise more rapidly and if lending standards start to slacken raising concerns about financial stability. In the first instance this should drive a wind back of government home buyer incentives, but, if this is not enough, pressure on the RBA and APRA to re-tighten lending standards may become apparent in the absence of an ability to raise interest rates.

What to watch over the next week?

In the US, expect small business optimism for November (Tuesday) to have remained solid and core CPI inflation to have slowed to 1.5% year on year. US Government funding runs out on Friday 11th December, but a shutdown is likely to be averted.

The European Central Bank (Thursday) is expected to extend its quantitative easing and cheap bank lending programs to combat the likely set back in the recovery as a result of recent lockdowns.

Chinese trade data (Monday) is expected to show continuing strength in exports and an acceleration in imports and CPI inflation (Wednesday) is expected to show a further fall in inflation to zero on the back of falling food prices. Credit data will also be released.

In Australia expect business confidence as measured by the NAB survey (Tuesday) and consumer confidence as measured by the Westpac/MI survey (Wednesday) to be buoyed by the recent flow of good news including around vaccines and ABS data to show a 1.5% fall in September quarter home prices (Tuesday) consistent with private house price indexes that have already been released. A speech by RBA Governor Lowe is unlikely to add anything new on the monetary policy front.

Outlook for investment markets

Shares could see a short term pause after recent strong gains. But we are now into a seasonally strong period of the year for shares (particularly from mid-December) and on a 6 to 12-month view shares are expected to see good total returns on the back of ultra-low interest rates and a strong pick-up in economic activity helped by stimulus and likely vaccines.

Low starting point yields are likely to result in low returns from bonds as the dust settles from coronavirus.

Unlisted commercial property and infrastructure are ultimately likely to benefit from a resumption of the search for yield but the hit to economic activity and hence rents from the virus will weigh heavily on near term returns.

Australian home prices are being boosted by ever lower interest rates, government home buyer incentives, income support measures and bank payment holidays but high unemployment, a stop to immigration and weak rental markets will likely weigh on inner city areas and units in Melbourne and Sydney into next year. Outer suburbs, houses, smaller cities and regional areas are in much better shape and will see stronger gains in 2021.

Cash & bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.25%.

Although the $A is vulnerable to bouts of uncertainty about coronavirus, the economic recovery and China tensions and RBA bond buying will keep it lower than otherwise, a continuing rising trend is likely to around $US0.80 over the next 12 months helped by rising commodity prices and a cyclical decline in the US dollar.

By Shane Oliver