The Australian economy entered recession in the March quarter for the first time in 28 years – impacted by the COVID-19 coronavirus as well as drought, bushfires and storms.

In the June quarter, the economy contracted by 7 per cent – the biggest fall in activity since the end of World War II. The Australian economy contracted by 0.3 per cent in 2019/20.

But the recovery is underway with the economy growing by 3.3 per cent in the September quarter – the biggest lift since March 1976.

The Australian economy is recovering due to our relative success in suppressing the COVID-19 virus as well as the speed and size of economic stimulus and support supplied by all levels of government and the Reserve Bank.

The cash rate currently stands at a record low 0.1 per cent; Aussie dollar is near US74.3 cents; unemployment stands at 7.0 per cent; annual inflation is 0.7 per cent; the S&P/All Ordinaries is near 6,930 points; and the S&P/ASX 200 index is near 6,700 points.

The year ahead: 2021

As we enter 2021, it is clear that COVID-19 still dominates the landscape. The bad news is that Europe and the US are experiencing second waves of the virus, driving case numbers to record highs and necessitating fresh lockdowns. The good news is that effective vaccines are set to be distributed across the globe with doses already being rolled out in the UK.

The economic outlook will clearly be dictated by the virus and how quickly the vaccines can stem case numbers and allow economies to start repairing.

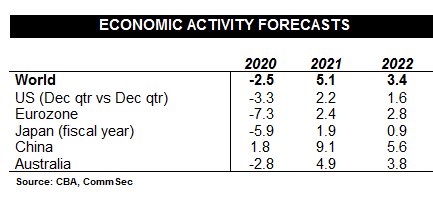

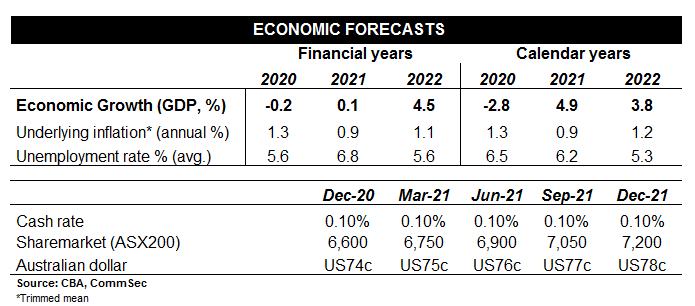

After contracting an estimated 2.5 per cent in 2020, the global economy is tipped to rebound by 5.1 per cent in 2021. On the same basis, the Australian economy is tipped to grow by 4.9 per cent in 2021 after contracting 2.8 per cent in calendar 2020.

The Reserve Bank Governor has committed to leave the cash rate at 0.1 per cent (or even lower?) for three years. Bond purchases are being employed with the hope of reducing longer-term yields.

Underlying inflation is expected to broadly hold near 1-1.5 per cent over 2021.

Unemployment is the focal point of all monetary and fiscal policy actions. Commonwealth Bank Group economists expect that the jobless rate has peaked at 7.5 per cent. The unemployment rate is expected to ease to 5.75 per cent by the end of 2021 and ease further to 5.0 per cent by the end of 2022.

Interest rates

The cash rate was reduced from 0.75 per cent to 0.10 per cent in 2020 with 25 basis point rate cuts on March 3 and March 19 and a further rate cut of 15 basis points on November 3.

On March 19 the Reserve Bank (RBA) introduced a target rate for 3-year Australian Government bonds of around 0.25 percent. It reduced the target rate to 0.10 per cent on November 3.

On March 19 the RBA introduced a term funding facility for the banking system. On September 1 the Reserve Bank decided to increase the size of the Term Funding Facility and make the facility available for longer.

On March 19 the RBA said Exchange Settlement balances at the Reserve Bank will be remunerated at 10 basis points.

On November 3 the RBA announced:

a reduction in the interest rate on new drawings under the Term Funding Facility to 0.1 per cent

a reduction in the interest rate on Exchange Settlement balances to zero

and the purchase of $100 billion of government bonds of maturities (also known as Quantitative Easing) of around 5 to 10 years over the next six months.

The market-determined 90-day bank bill rate fell from highs near 0.92 per cent in January to record lows of 0.02 per cent and is ending the year near the lows. Yields on the long bond – 10-year government bond – fell from highs of 1.37 per cent in January to lows of 0.62 per cent on March 9; lifted to highs near 1.50 per cent on March 19; and is ending the year near 1.03 per cent.

Exchange rates

The Aussie dollar has risen around 6.2 per cent against the greenback over 2020. The Aussie started the year around US70 cents and is ending the year near US74 cents. The Aussie hit highs (30-month highs) of US74.85 cents in December, while the low (17½-year lows) of US55.06 cents was set in on March 19. The 19.8 cent range for the Aussie over the year was the biggest in a decade.

The Aussie has gradually trended higher since mid-October against a weaker greenback. Reduced interest rate differentials, a rapid rise in iron ore prices and improved risk sentiment have pushed the Aussie up 33 per cent since the March low.

Over 2020 the Aussie has lifted against pound sterling (+4.9 per cent); the Japanese yen (1.5 per cent); and the NZ dollar (+1.2 per cent). The Aussie has fallen against the Swiss Franc (-2.6 per cent); Euro (-2 per cent); and Chinese yuan (-0.5 per cent).

Sharemarkets

At the start of 2020, the Australian All Ordinaries index stood at 6802.4 with the ASX 200 at 6684.1. The two indexes are respectively near 6930 and 6700 points in late 2020. The All Ords is up around 2.4 per cent on the year with the ASX 200 up 0.7 per cent.

Focussing on the ASX 200, the index hit record highs (together with the All Ords) on February 20 at 7162.5 points. The ASX 200 then fell 37.5 per cent over the next 22 days before lifting 21 per cent over the next 16 days.

Movements of other key markets over 2020 so far: US Dow Jones (+5.4 per cent); US S&P500 (+13.7 per cent); US Nasdaq (+37.5 per cent); Japan Nikkei (+13.4 per cent); UK FTSE (-13 per cent); German Dax (+0.7 per cent).

The world index (MSCI) excluding Australia in US dollar terms is up 12.2 per cent in 2020.

Key US sharemarket indexes set fresh record highs over the month of December 2020.

Australia sharemarket sectors and asset returns

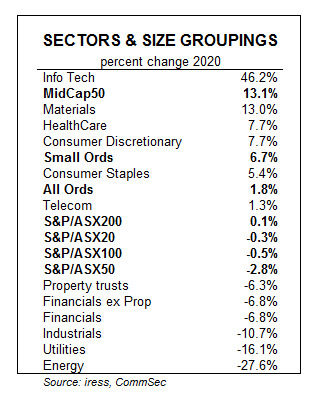

Australia’s relatively small Information Technology sector has out-performed so far in 2020. The Info Tech sector has lifted 46.2 per cent over 2020, ahead of Materials (+13 per cent) and the HealthCare and Consumer Discretionary sectors (both +7.7 per cent).

At the other end of the scale, Energy has fallen 27.6 per cent, from Utilities (-16.1 per cent) and Industrials (-10.7 per cent).

Of the size groupings, the MidCap50 (+13.1 per cent) out-performed the Small Ordinaries (+6.7 per cent). The S&P/ASX50 is down 2.8 per cent.

Total returns on Australian shares (All Ords Accumulation index) have lifted 4.6 per cent over 2020. Cash is currently yielding 0.1 per cent with bond returns (Bloomberg AusBond Govt 0+ Yr index) up 4.2 per cent. And residential property (CoreLogic Home Value index) has returned 6.6 per cent in the year to November.

Commodity prices

The CommSec daily commodity index has lifted 30 per cent so far in 2020 in US dollar terms. Over the same period the Aussie dollar has risen by around 6 per cent.

The Reserve Bank commodity index in US dollar terms (using spot prices for bulk commodities) was up 6.9 per cent in the 11 months to November. Prices for iron ore, coal and natural gas have since lifted sharply in December.

In contrast, the CRB futures commodity index has fallen by 14.7 per cent over 2020.

One of the stand-out gains from an Australian perspective has been the iron ore price (up 63.9 per cent), followed by natural gas (up 58.8 per cent), coking coal (26.3 per cent), gold (up 23 per cent) and thermal coal (up 13.9 per cent).

At the other end of the scale, oil has fallen 25.5 per cent with beef down 19.4 per cent.

Outlook 2021

The 2020 calendar year was a year of unprecedented challenges. The last time there was a pandemic of global significance was just over a century ago. And unfortunately our ancestors didn’t leave us with a playbook – each country and region have had to make their own choices about the ‘right’ way to respond.

While there were some hiccups with virus case numbers in Australia, we are exiting 2020 as a nation with plenty of optimism. A monthly consumer sentiment index is at decade highs while business confidence is at 31-month highs.

The success in suppressing the virus has enabled our states and territories to ‘re-open’ their economies. Governments, the Reserve Bank, commercial banks and regulators have provided all the necessary support and stimulus to ensure as many businesses as possible to stay in business and workers hold onto jobs. Borrowing costs for businesses, households and governments are at ‘rock bottom’.

The additional boost to confidence and future prospects comes from the prospect of a vaccine – already starting to be distributed in the UK.

Stimulus measures will need to stay in place through the first quarter of 2021. The hard decisions lie ahead about how and when to phase out fiscal measures like JobKeeper and JobSeeker. If you remove the support too quickly, you risk a loss of economic momentum. But leave the support in place too long and businesses and consumers lose the desire to take charge of their own destinies.

Overall we expect the Australian to rebound by 4.9 per cent after contracting 2.8 per cent in 2020. Risks to the forecasts include ‘second’ or ‘third’ waves of virus cases; setbacks with vaccines; policy mistakes on the removal of support measures; and an extended delay in the re-opening of foreign borders.

We believe that the jobless rate peaked at 7.5 per cent. The jobless rate could fall to the 5.75-6.00 per cent region by end year.

But make no mistake the job market will dominate attention over 2021. No longer is the Reserve Bank directed solely by inflation but by reducing unemployment – an “important national priority”.

The Reserve Bank is committed to leave the cash rate at 0.10 per cent through to late 2023. The big question is what happens if unemployment surprises on the downside and inflation surprises on the upside over 2021.

Home prices could grow by 3-5 per cent in 2021. Low interest rates and government grants will support buying and building of homes. But demand will be constrained by the absence of migrant demand. Should the property market show signs of overheating the banking regulator APRA may act through macro prudential policies.

We expect the Australian sharemarket to return to record highs by the end of the year. An earlier return to highs is possible given the fast progress with vaccine approval and distribution in many countries. Also other advanced economies are expected to follow China’s lead with infrastructure-led growth, supporting Australia’s mining and energy sectors.

While the relative outperformance of the Aussie sharemarket may continue over the summer months, the ASX 200 is ‘expensive’ valuation-wise and is less cyclical in composition relative to offshore peers.

The global economy is expected to lift 5.1 per cent in 2021, further underpinning demand for metals and ores and driving the Aussie dollar higher.

The Aussie dollar is expected to rise over 2021 to reach US78 cents by the December quarter. A stronger Aussie could see the Reserve Bank extend its bond purchasing program with the Board reluctant to cut the cash rate further or introduce negative interest policy.

Introduction Why do financially secure retirees still hesitate to spend, or commit to strategies that would clearly improve their outcomes? This article sets out the Two-Chapter Retirement framework, a new [...]

China’s economic trajectory is shifting, but not in the way many had once expected. Consumption-led rebalancing has not materialised. Instead, economic policy continues to emphasise industrial modernisation, aligned with a [...]

In financial advice, acting in a client’s best interest isn’t just a regulatory rule, it’s the foundation of a trusting, successful partnership. This article, proudly sponsored by GSFM, examines the [...]

Few themes rival the scale, urgency and long-term significance of climate change. Consequently, regions, countries, companies and individuals are taking positive action to decarbonise the planet and work toward net [...]

Introduction In February 2026, the Australian Financial Complaints Authority (AFCA), reached a significant milestone when it issued its 1,000th Dixon Advisory determination[1]. Up until that point, this represented the single [...]