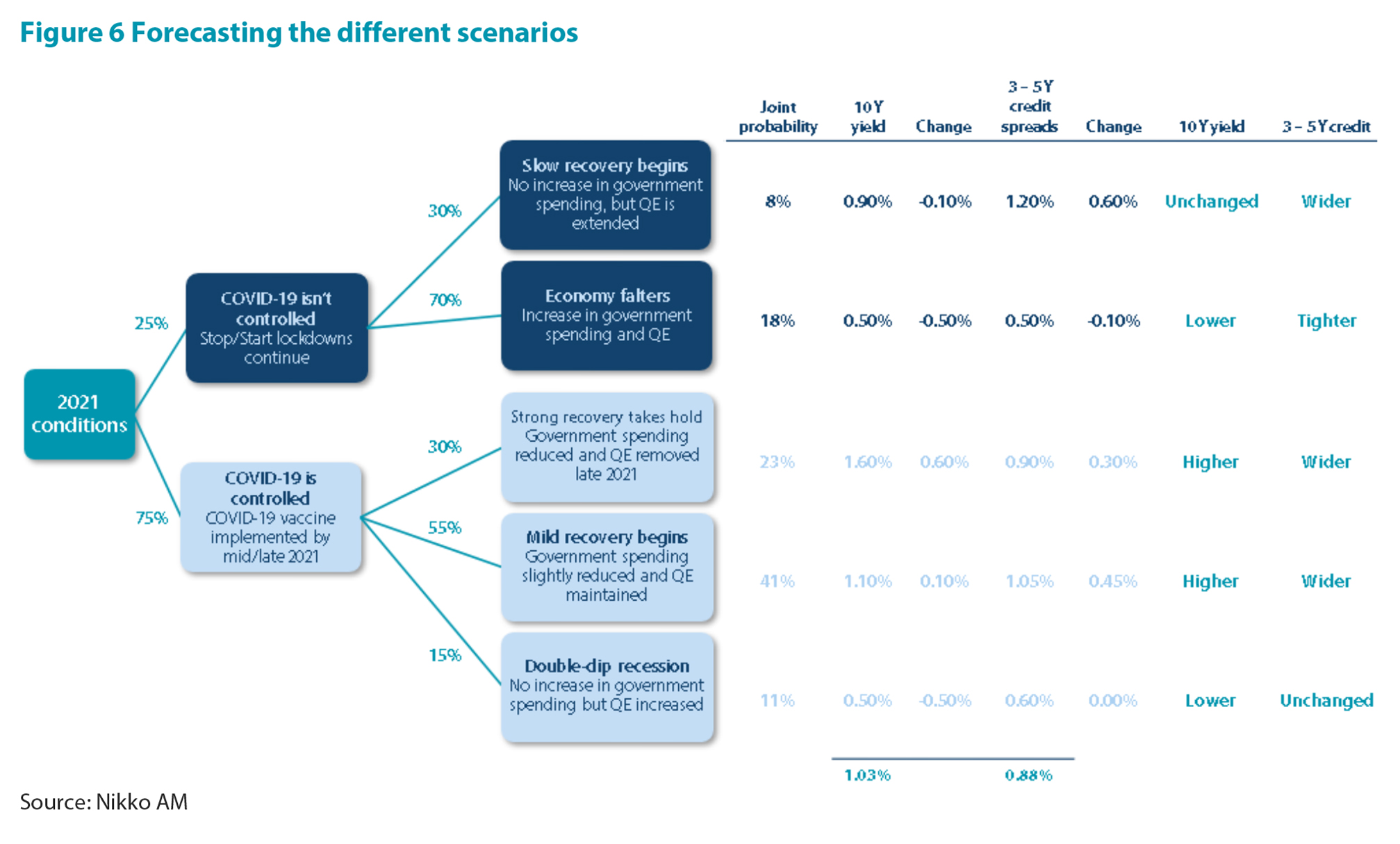

Use a decision tree to try to establish the range interest rates could fall into and what the most likely outcomes could be.

Forecasting outcomes for the year ahead is challenging in the best of times, let alone during a global pandemic. This year, Chris Rands adopted an alternative strategy for determining where interest rates could land in 2021 and what that could mean for fixed income performance.

“What if?” scenarios

Typically when creating our fixed income outlook for the year ahead we focus on the most likely scenarios, figuring out how interest rates could move in those environments. This year, however, the range of possible outcomes is far too wide to focus only on what is expected to occur, which makes forecasting particularly difficult. As a simple example, it is not impossible to forecast a world where COVID-19 continues to spread through countries and the global economy sees intermittent shutdowns aimed at controlling the disease. It is also not far-fetched to forecast a world that has a working vaccine and trillions of dollars in government support to drive an economic recovery.

As such, this year’s outlook will use a decision tree to try to establish the range interest rates could fall into and what the most likely outcomes could be. This will involve stepping through the branches of the decision tree to determine the probability of different events:

- Branch 1: Will COVID-19 be controlled in 2021?

- Branch 2: How will the economy perform if COVID-19 cannot be controlled?

- Branch 3: How will the economy perform if COVID-19 is controlled?

The result of this process will be a decision tree that estimates different outcomes occurring in the economy. Once we have determined what the potential scenarios entail, we will then assign fixed income forecasts to each environment.

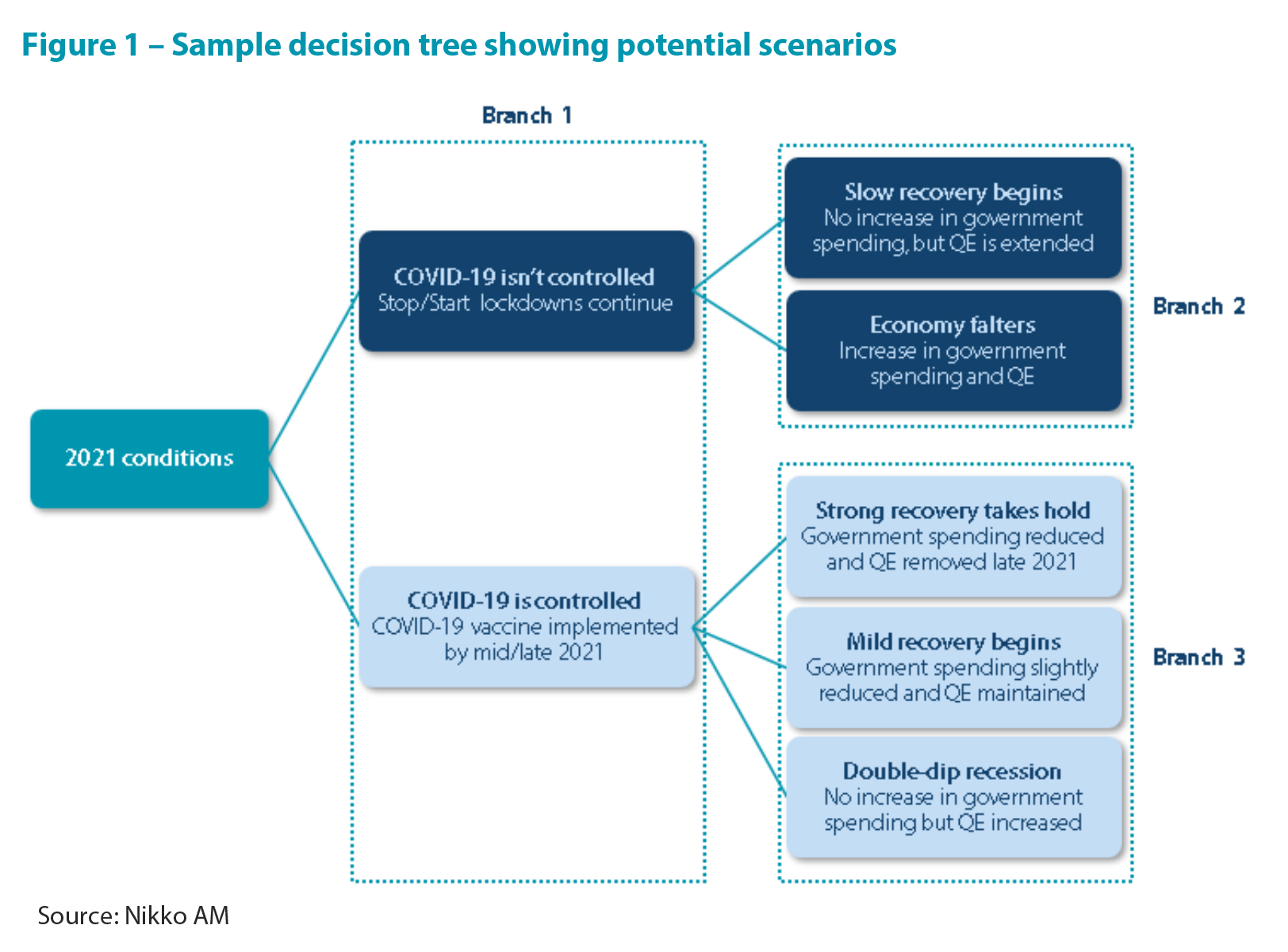

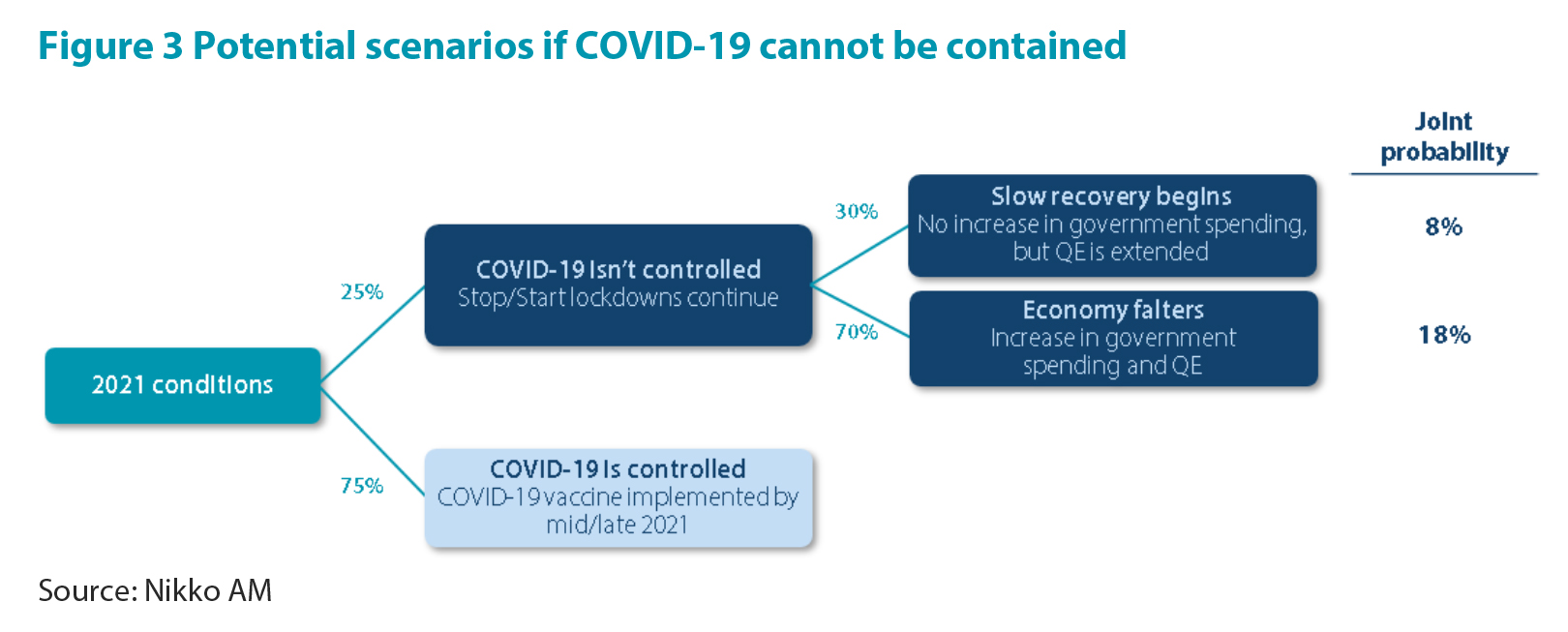

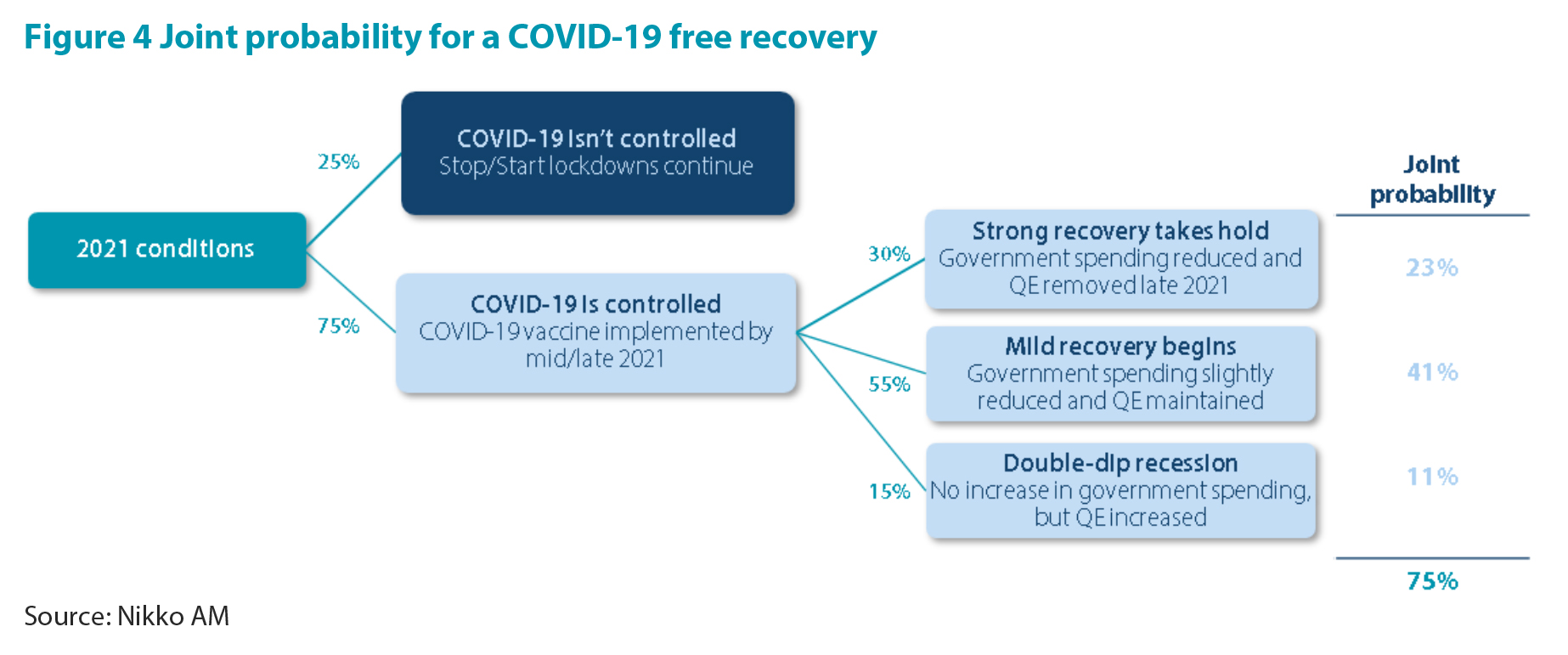

A sample of this decision tree is shown below (excluding any assigned probabilities). The first branch in the decision tree considers the status of COVID-19 before branching out into how the economy could perform under that environment.[1]

Branch 1: Will COVID-19 be controlled in 2021?

The starting point for determining the outlook in 2021 is whether COVID-19 will be controlled. This question is extremely important for the outlook as completely different outcomes are expected if the disease is controlled.

To help define what ‘controlled’ means, we can refer to the Northern Beaches COVID-19 outbreak in Sydney in December 2020. This outbreak quickly led to the Northern Beaches entering lock down, before wider restrictions on gathering sizes and state border closures where enacted. This scenario represents ‘COVID-19 isn’t controlled’ above, with stop/start lockdowns continuing throughout 2021.

An example of ‘controlled’ is where an outbreak such as the Northern Beaches

episode occurs but requires no widespread action to stop community infection. This doesn’t necessarily mean there are zero cases, but rather we no longer need to lock down the economy at the first sign of an outbreak.

Whether COVID-19 is controlled will have big implications for our outlook. For example, if it is not controlled then it is foreseeable that certain parts (or states/territories) of the Australian economy will need to be shut down or quarantined, which will result in a loss in output and increased pressure on tourism. However, if COVID-19 is controlled, businesses will be able to start making investment decisions again, the employment outlook should improve and uncertainty around economic conditions will improve.

This means our most important question becomes: What is the probability that COVID-19 is controlled in 2021?

Rolling out the vaccine

The most recent news in respect to this question is obviously positive. At the time of writing, trials of the vaccine were proven effective and are being approved and rolled out in different parts of the world. In November 2020, Pfizer BioNTech announced a COVID-19 vaccine efficacy rate of 95 percent. Subsequently, it was rapidly approved across countries, with the UK the first to approve the vaccine for use in December 2020.

The Australian timetable for vaccine use and approval is slightly slower, with the Australian Government recently announcing that they expect vaccines to begin in February with potentially four million people vaccinated by March.

On the production side, currently CSL is producing 30 million doses of the AstraZeneca vaccine with the hopes of a fast rollout should the vaccine be approved. Considering that children will be vaccinated last, this could see a considerable percentage of the adult population vaccinated by June. Given the effectiveness of the vaccines in the trials, the rapid pace at which other countries have been approving them, and the fact that the Australian Government has been quick at curtailing any signs on the disease post the second Victorian lockdown, there is a high probability for the potential of COVID-19 to be controlled in Australia in 2021.

Will it work?

While there has been a lot of positive news surrounding the pace with which vaccines could be produced, there are still some lingering questions on whether this will control the virus. The types of questions that are worth posing are:

- How long does the vaccine offer protection?

- Will enough people take it?

- How soon can the vaccine be made available offshore (particularly emerging markets)?

- Are there any longer-term side effects?

- Will the vaccine prove ineffective as the disease mutates (such as the new strains being reported in the UK and South Africa)?

- How long will it take to vaccinate a majority of the population?

While we currently do not have answers to these questions, the lack of information on this front tempers some of the positivity that we cover under Rolling out the vaccine earlier in this paper. Increasingly we are also becoming more concerned that the more contagious strains, such as the UK strain, could see case growth increase considerably and lead to more lockdowns should it become prevalent in the economy. There is also the possibility of complications that see the vaccine rollout timeline delayed to the back end of 2021.

Estimating the probabilities

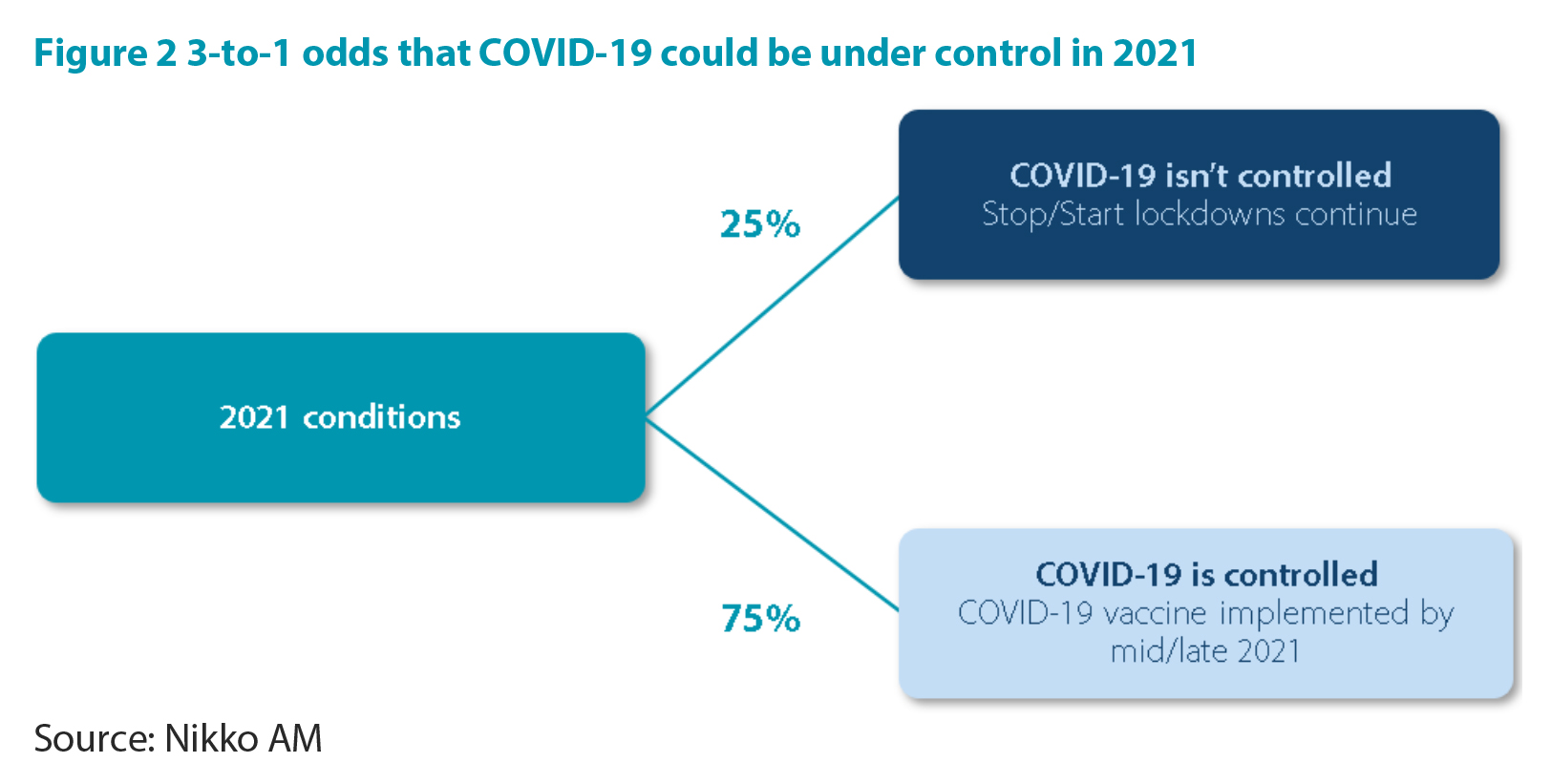

We believe this information is pointing towards ~75% probability that COVID-19 could be under control in Australia in 2021. As a reminder, in this scenario we do not need COVID-19 to be eradicated, but rather have enough people vaccinated that a Northern Beaches style outbreak does not lead to lockdowns in the economy, but something closer to business as usual.

There are obviously still obstacles and risks to this occurring (and maybe this is an optimistic probability), however, the positive news flow and speed with which the vaccines are being approved point to a strong chance of this occurring. As such, 3-to-1 odds feels about right at this point in time and gives us our first branch of the decision tree.

Given these probabilities, we can now try to determine how the economy could perform in each environment. We start first with what the economy could look like if lockdowns need to continue.

Branch 2 – Outlook if COVID-19 is not controlled and the stop/start economy continues (25% probability)

In our opinion, there are two key economic pathways that could occur in this environment: a slow recovery or a mild fall in growth. The more extreme outcome of a deeper recession is not assumed as both the central bank and federal government have shown they are willing to throw immense financial support at the problem and will isolate a single state (e.g. Victoria) to stop the spread of the disease.

In the interests of simplicity, we have removed the extreme negative outcome from the process. A small probability could be assigned for a more complete forecast, but we will instead focus on whether the economy recovers or falters.

Slow recovery or economy falters?

The starting point of this question is a little more complex than the past six months would have you believe. There is a valid point to be made that the Australian economy has performed well over the past three months despite COVID-19 keeping us in lockdown. This implies the recovery should continue. While this may be true, a continuation of the crisis throughout 2021 poses some tough problems for the economy.

The first of those relates to JobKeeper and JobSeeker potentially ending in March of 2021. In the event that COVID-19 is prolonged, these income support measures will be set at January’s lower rate. This has important flow on effects for the economy, as part of the reason that the economy was able to bounce back quickly from its lows was that over three million Australians were receiving income support.

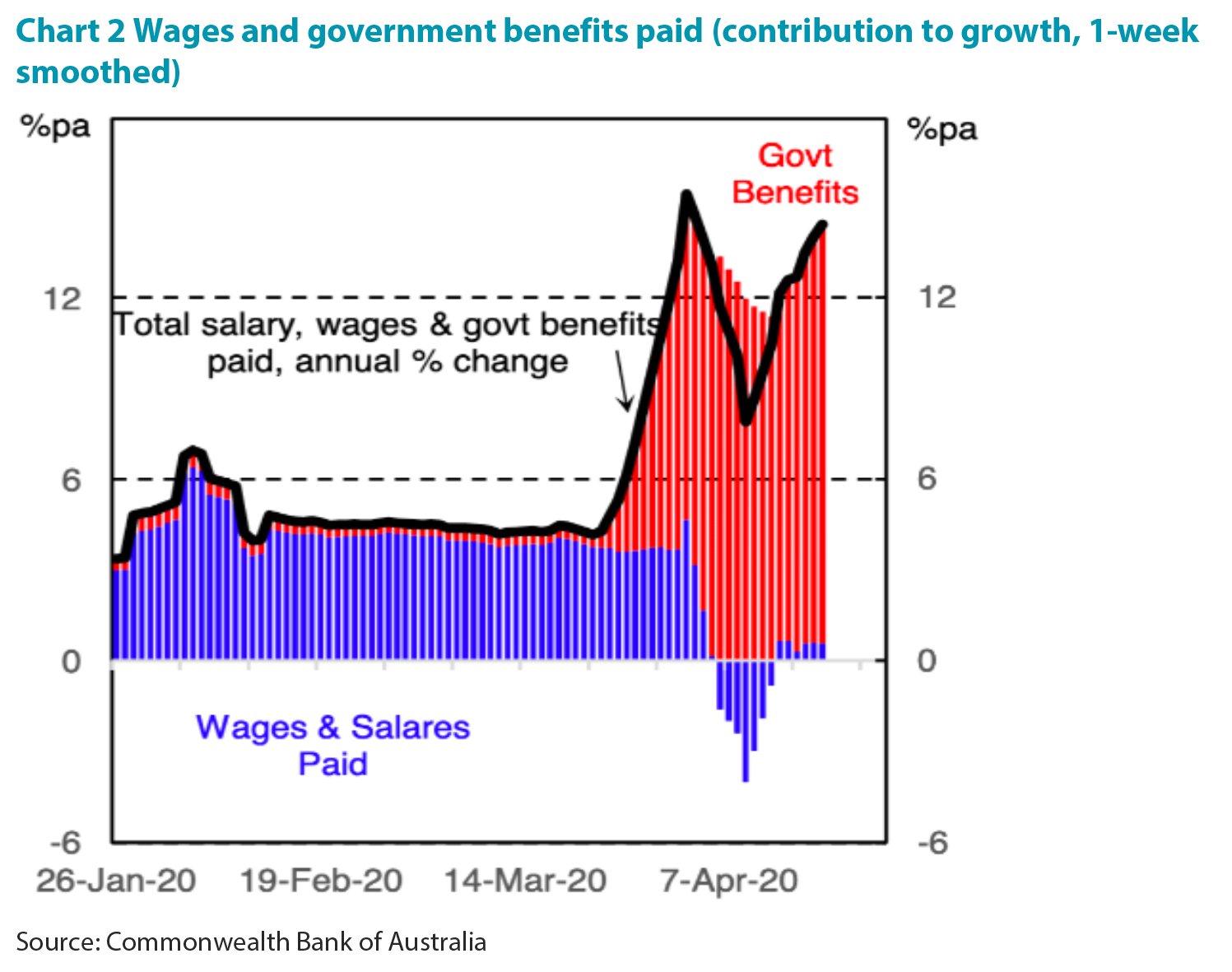

Interestingly, the 2020 COVID-19 recession was not like other recessions in terms of the impact on households. Disposable income growth actually rose at its fastest pace in a decade. Rather than losing income through the recession, households had more to spend.

Research from Commonwealth Bank shows just how important government support measures were throughout this period. Chart 2 shows how total salaries, wages and benefits jumped almost 20% in June 2020 period. This was driven entirely by the red bars; government benefits. Actual wages paid have been going sideways. Hence, in an environment where income support continues to unwind and the economy is still exposed to COVID-19, a drop in household income would be expected.

The second problem is that small businesses—those hit hardest by the COVID-19 crisis—will need to start making real business decisions should the economy remain in a stop/start nature. The RBA’s October 2020 Financial Stability Review stated that “Survey evidence indicates that about one-quarter of small businesses currently receiving income support would close if the support measures were removed now, before an improvement in trading conditions”.

As JobKeeper rolls back, small businesses are starting to lay people off and small business employment has dropped back to levels similar to April. Larger companies that have better access to finance have seen a stable improvement in their employment conditions. This has seen big businesses performing well, but the same cannot be said for smaller ones.

This precarious business position, coupled with no international students, a potential trade war with China, a weak commercial property market and the risk of having to shut down major cities, all pose significant risk that the economy would falter in an environment where COVID-19 is not contained.

Given this information, what are the positives that show a recovery could take hold? There are a number of economic data points that have begun to turn positive, pointing to more optimism for the economy.

The first of those comes from the housing outlook, as the low interest rate environment has improved demand for housing. This typically leads to new construction of residential dwellings and would be a positive for both construction employment and growth. The Australian Industry Group (Ai Group) Performance of Construction survey bears this out with a jump occurring in new orders over the past few months, which will bode well for the construction outlook in 2021.

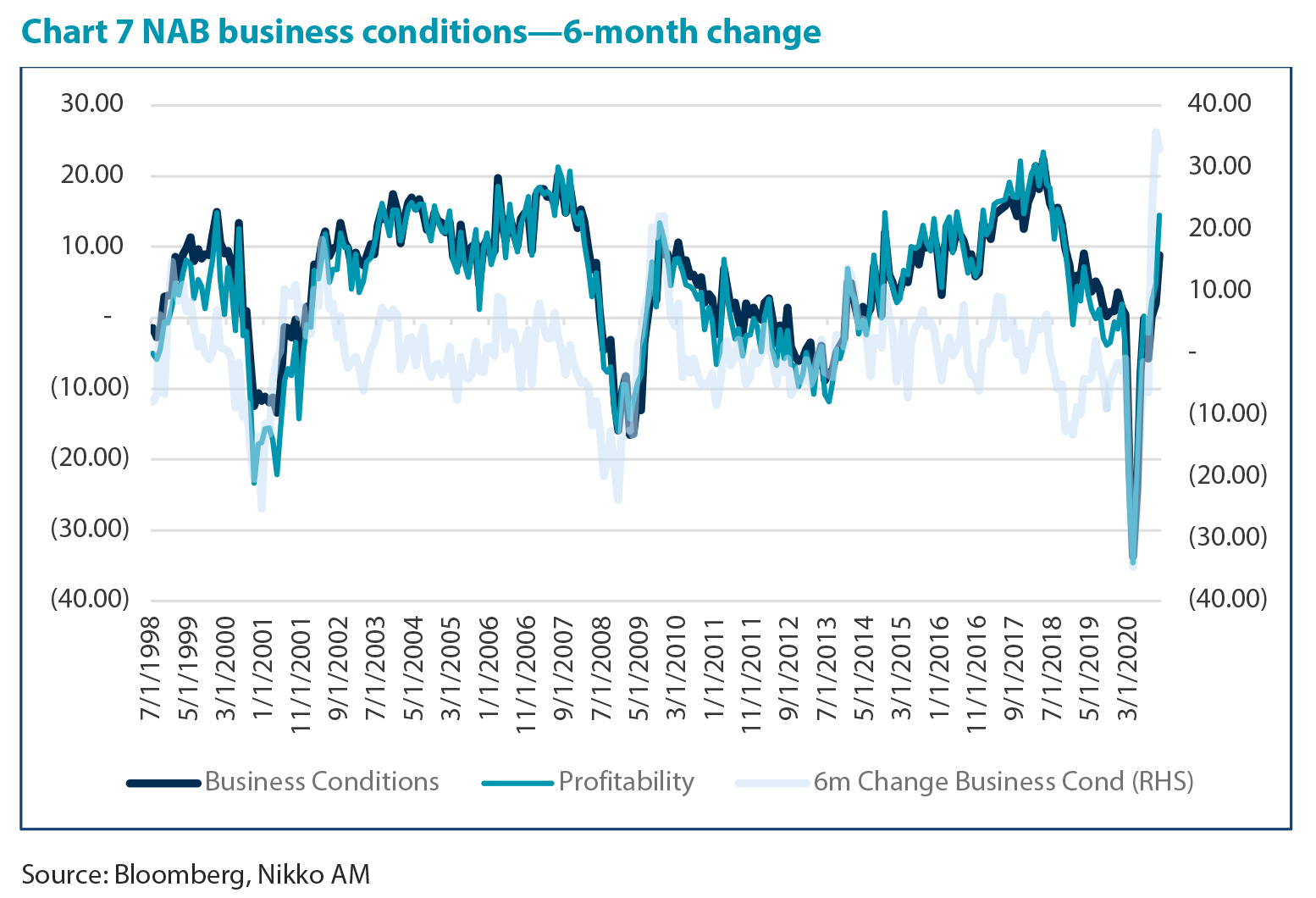

Secondly, business optimism has begun to substantially improve, which will mean that the rise in unemployment should not be as great as first feared. Typically, NAB business conditions lead the change in the unemployment rate, with the current conditions suggesting the unemployment should at least be stabilising and move lower from here.

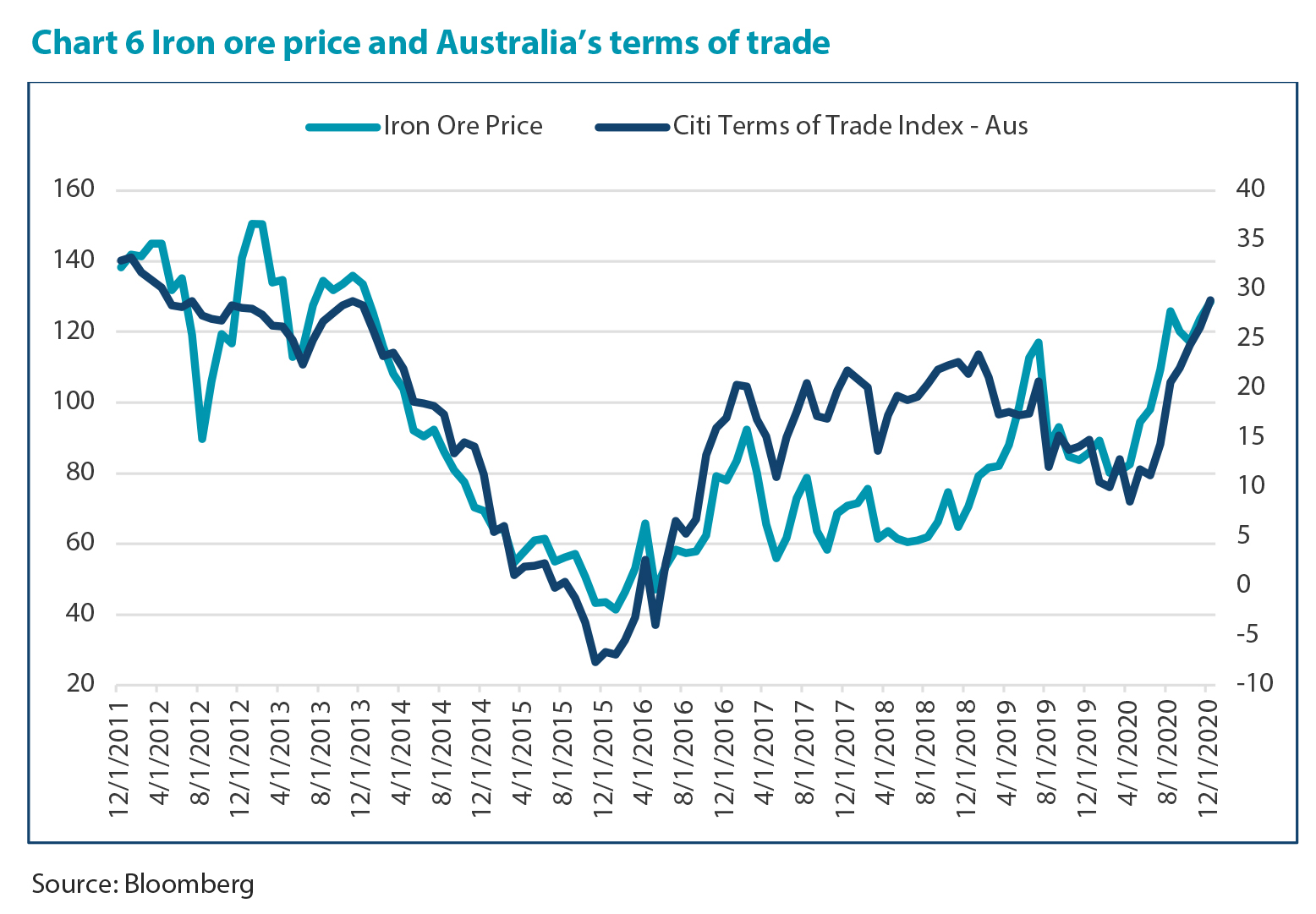

Thirdly, commodity prices have been rising, particularly iron ore, which at the time of writing, was priced at over $130 a ton—the highest level in six years. While there is a risk that the confrontation with China continues to deteriorate and this torpedoes some of our export growth, the commodity price outlook is favorable, which will benefit Australia’s terms of trade.

Finally, if COVID-19 is not controlled in 2021 then the RBA will likely continue its quantitative easing (QE) program and the large fiscal support from the government should help the economy back on its feet.

Putting the odds together

While there are a number of positives to look forward to in the economic data, we think that another year of an economy that remains constrained due to COVID-19 would eventually weigh on business sentiment and profitability. In these circumstances, we would expect government support to continue, but eventually many small businesses will fold under the pressure of strained operating conditions. As such, we have assigned a probability of 70% that the economy would falter (with a simple estimate of 0% growth) if the disease cannot be contained, creating the below outcomes in our decision tree.

Branch 3 – What would a vaccine do for the economy? (75% probability)

The second, and more positive, question to ask is: “What happens to the economy if COVID-19 is controlled in 2021?” In this instance, the most likely set of outcomes focus on whether the economy would see a mild or strong recovery. This would be followed by asking the question: “What would cause a double dip recession?”

Mild or strong?

The most likely set of outcomes in this instance relate to whether the economy bounces back from its 2020 shock in a mild or strong way. This may seem like splitting hairs, but it will be important in determining how the RBA reacts with monetary policy and therefore our interest rate outlook.

As described above, there are a number of factors that are pointing to a strong rebound in 2021, which would be even more impactful if we had certainty on the containment of COVID-19. One of the most important of these indicators is the NAB business conditions, which have staged a remarkable bounce.

The six month change in business conditions is the strongest it has been in the series history and both conditions and profitability are hitting levels associated with a robust expansion.

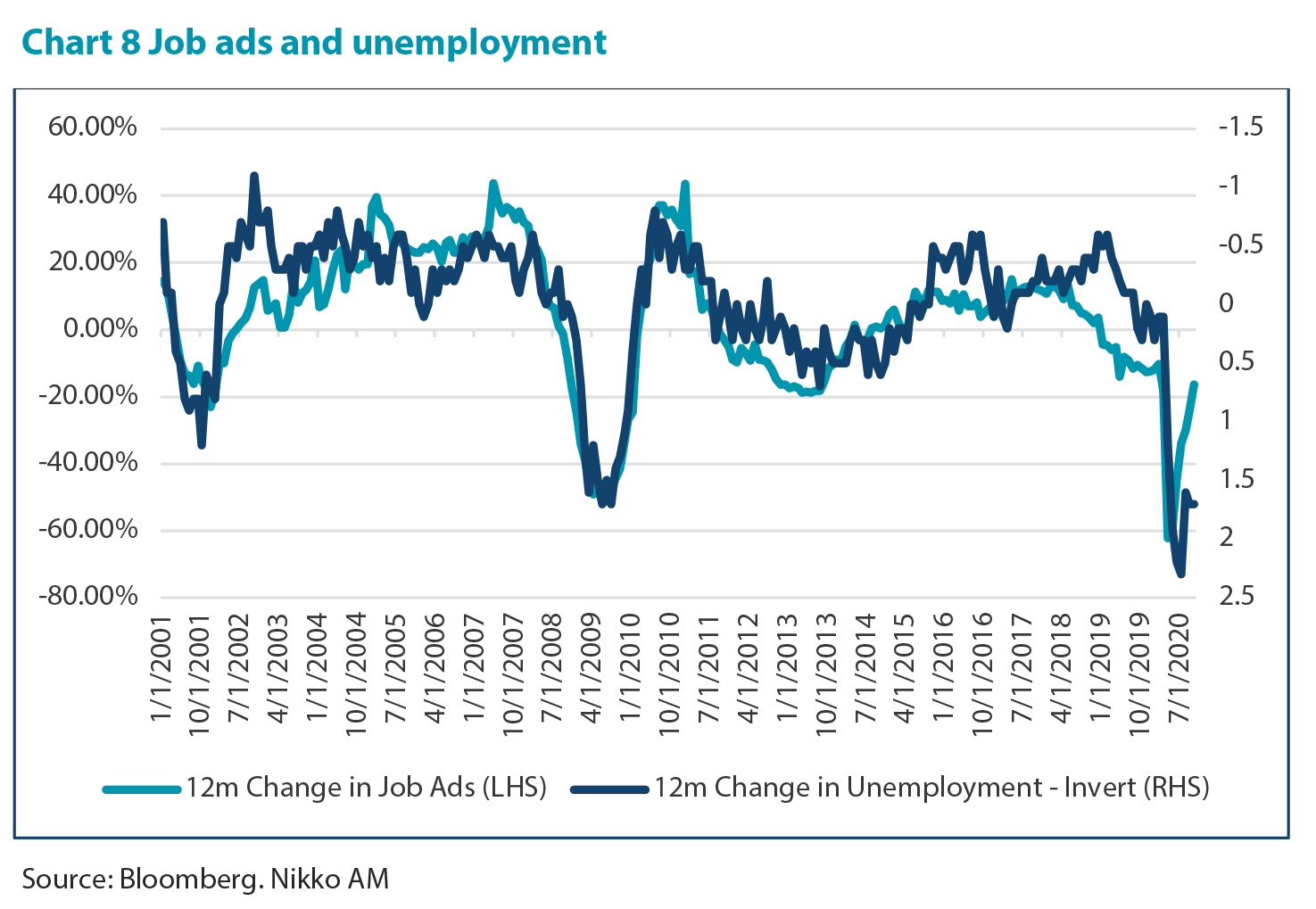

Improved profitability and operating conditions should set the scene for businesses to start hiring again, which is currently being reflected in job advertisements quickly rebounding from their decline.

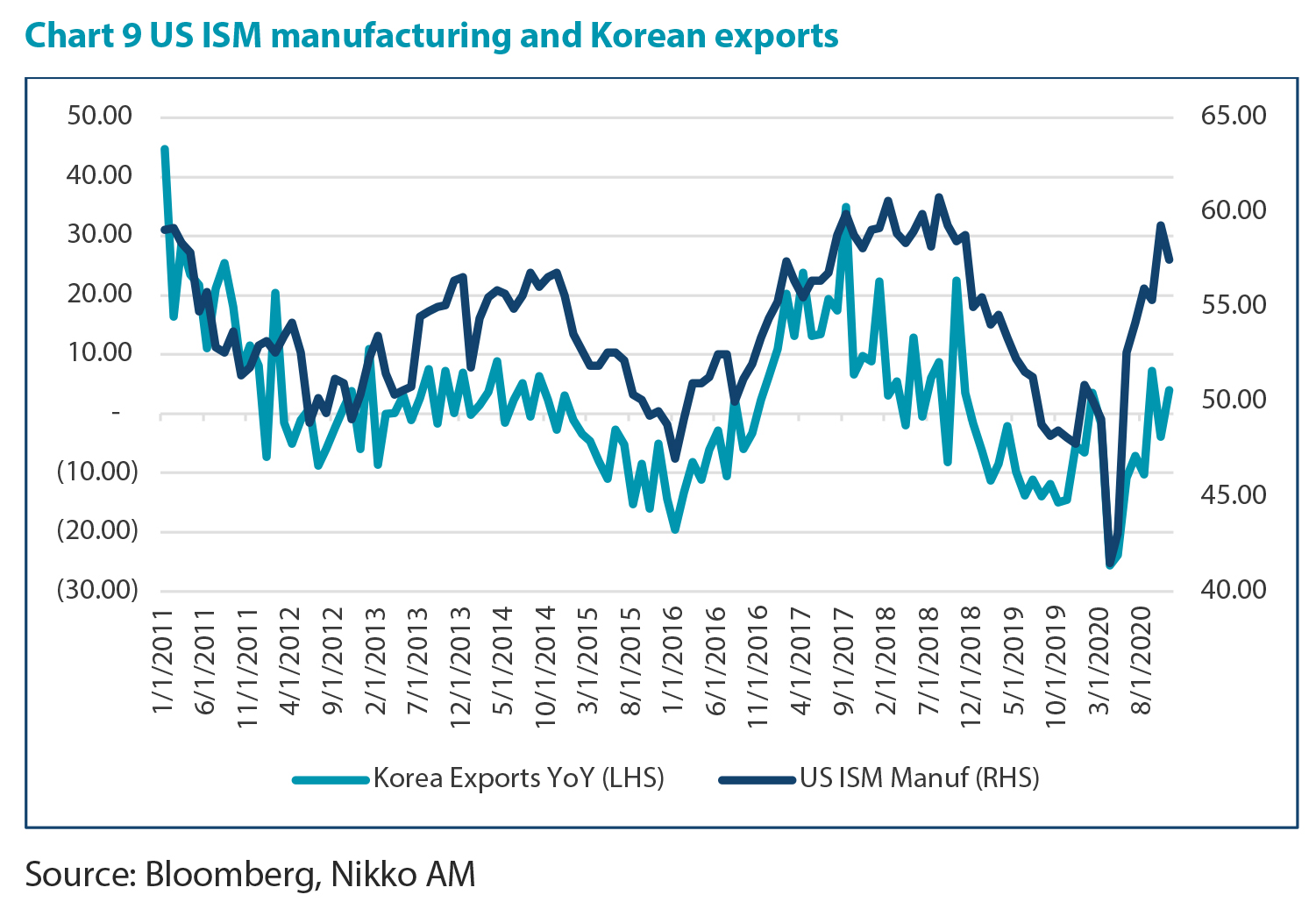

Furthermore, the global Purchasing Managers’ Index (PMI) has reached highly expansionary levels and this typically bodes well for Asian economies. Chart 9 shows that Korean exports typically move higher with the global PMI, and this is similar across other Asian exporters, such as China and Taiwan. Given the extreme volume of global stimulus, there is a good reason to believe that Asia could see strong growth in 2021.

Rising exports to China is also a positive for Australian corporates, whose profitability often moves in a similar direction to the trade situation in China. Note that in 2020 the series deviated as the JobKeeper payments distorted the corporate profits figure. As such, a rebound in the Asian region is going to serve Australian corporates well, provided the trade dispute does not continue to escalate.

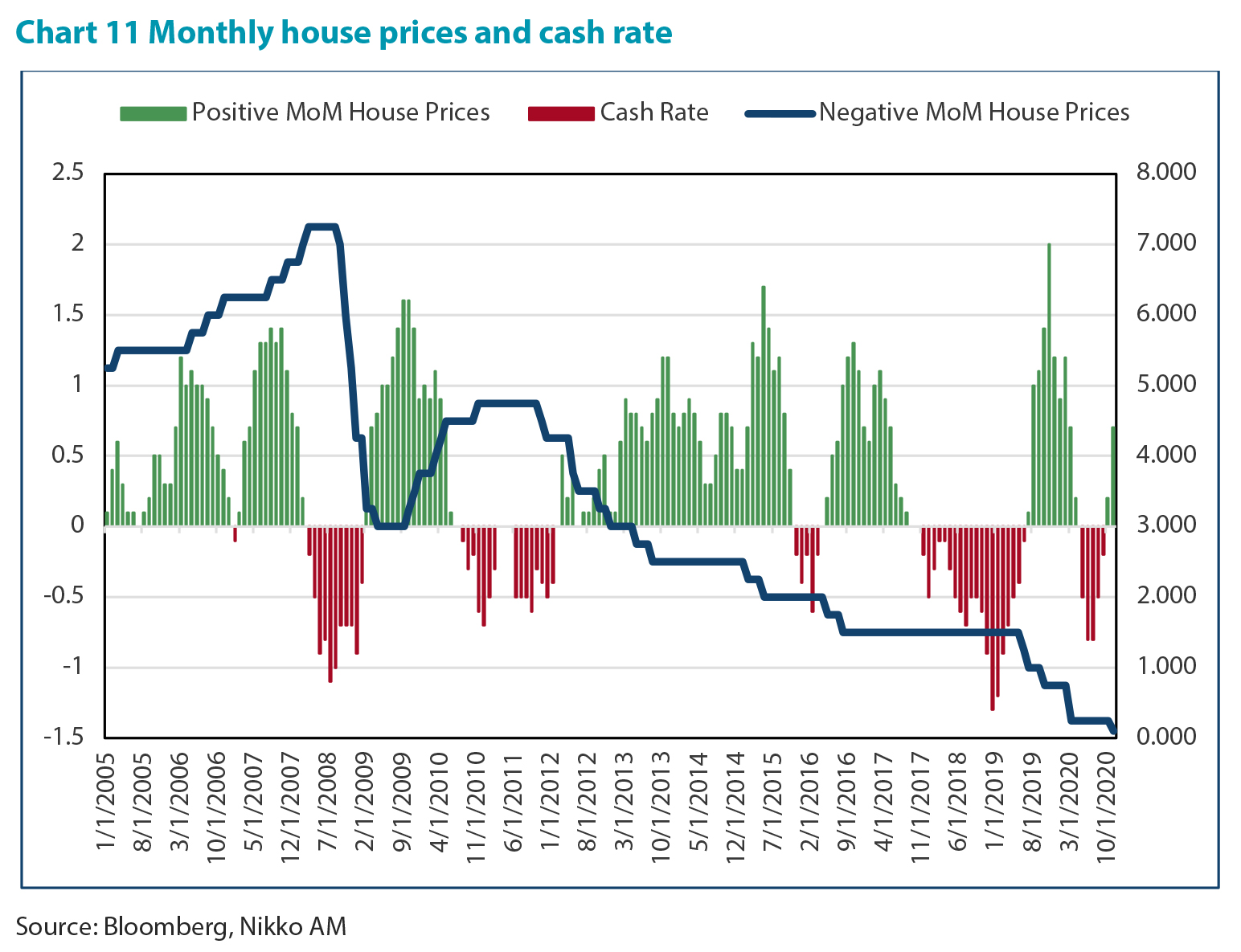

The final area worth pointing out is housing, which is showing just how interest rate sensitive this area of the economy is. The price outlook was disturbing in 2020 as the usual explanations for high Australian house prices where pointing to trouble. This included rising unemployment, falling population growth, wage freezes, falling rents, excess supply, and economic uncertainty. However, the sector has shown that the key driver is not necessarily these factors, but rather the march lower in interest rates.

Over the past 10 years, whenever housing slowed the RBA has cut rates, which has been followed by 12 – 18 months of house price appreciation. This can be seen in Chart 11: see 2011, 2016 and 2019. When the monthly performance of the housing market turns negative, the RBA has been quick to act, which leads to multiple months of price appreciation.

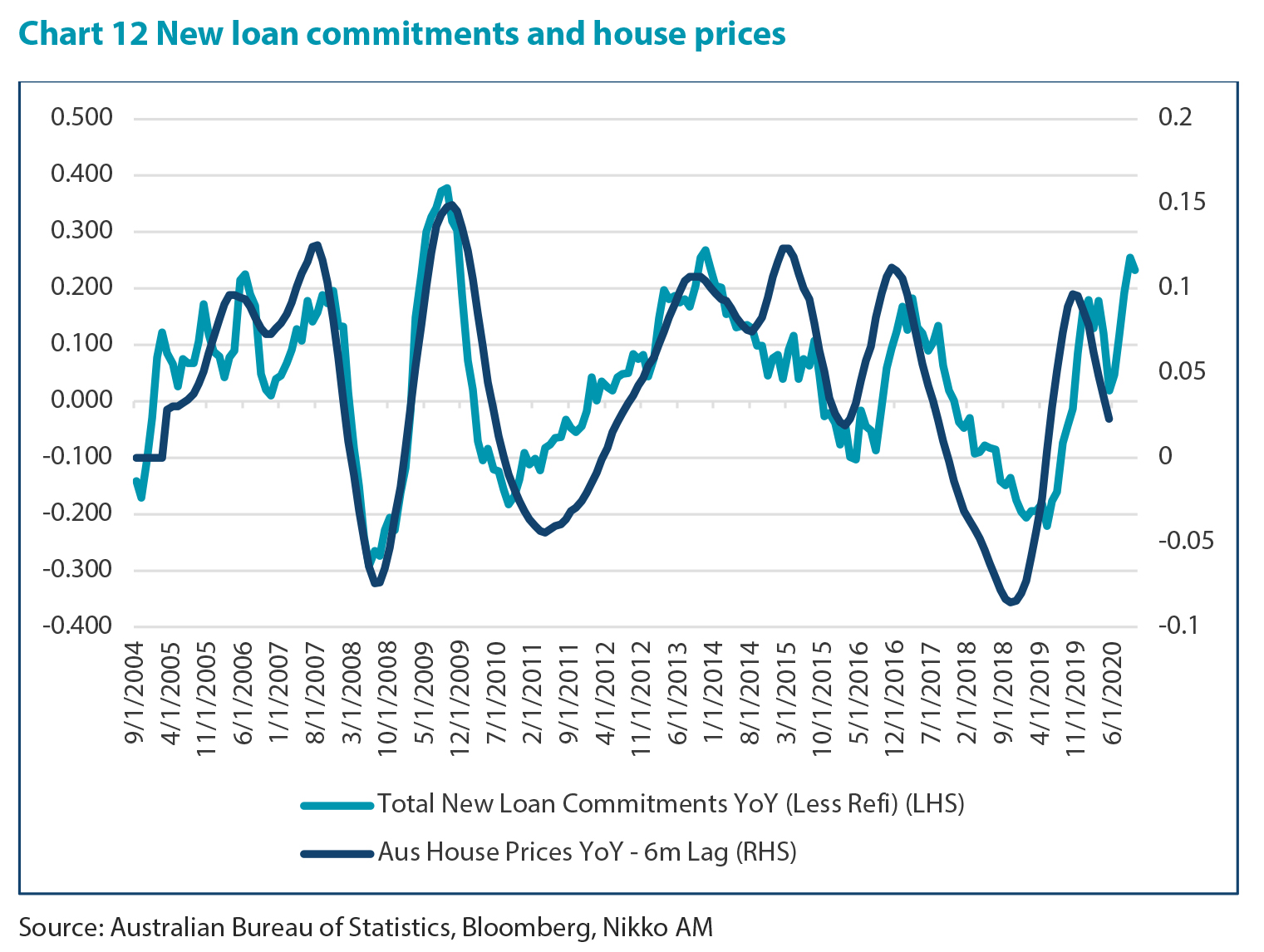

A simple debt service calculation tells us that households will be able to expand household debt by approximately 15% while keeping serviceability stable, thanks to the interest rate cuts in throughout 2020.

As mentioned above, while there has been a myriad of risks, owner occupiers have taken the signal and used the lower rates to borrow more and buy housing. While we can guess what this might mean for household debt and the future ability for the RBA to raise rates, the relationship between loan commitments and house prices implies there should be strong upside for house prices in 2021, in the 10 – 15% range.

This brings us back to our question: ”Will the economic recovery be mild or strong?” The available evidence seems to suggest that if COVID-19 is controlled, the bulk of the probability distribution will be between these two outcomes. Almost all the lead indicators that we observe have now turned positive: business conditions, global PMI, employment indicators, lending statistics, retail sales, house prices, commodity prices, and equity prices.

However, while the economic information displayed above looks promising, there are still a number of unknowns that make us lean into the mild recovery scenario, including:

- Would APRA step in with macro-prudential policy to slow housing?

- Will the trade war intensify and slow down Australian exports and corporate profits?

- Will job ads continue to bounce as JobKeeper is unwound in 2021?

- Will the RBA/Government withdraw stimulus too quickly if things look very positive?

None of these questions alone would likely be enough to derail a recovery that is taking hold as COVID-19 is controlled, but it would reduce the potential for a strong outcome. As such, we assign a 55% probability to a mild expansion and 30% probability of a strong expansion.

Is a double dip recession on the cards?

The final question that is worth exploring is: “What are the odds that the economy enters a double dip recession?” This could be similar to 2011, where the global economy veered towards recession after a rebound from the GFC.

In this respect, there is very little economic data that is pointing at the possibility at the moment. All the above lead indicators are strong. But that does not mean that it is a zero per cent probability. There are still a number of hurdles that the economy must overcome even if COVID-19 is controlled:

- What will happen to income/spending when JobKeeper ends in March?

- Will small businesses fail when government support is reduced?

- When will international travel resume, since developing economies will not have access to vaccines as early as the developed world?

- Have households/government/businesses taken on too much debt?

In an environment where COVID-19 is controlled, we would think that the economy can grow even with these questions. However, the fact that the world economy teetered lower with the European debt crisis in 2011—just after the GFC—gives some pause for thought. As such, we assign this a 15% probability. A one-in-seven chance seems about right given that history shows the year after a recession the economy typically bounces back.

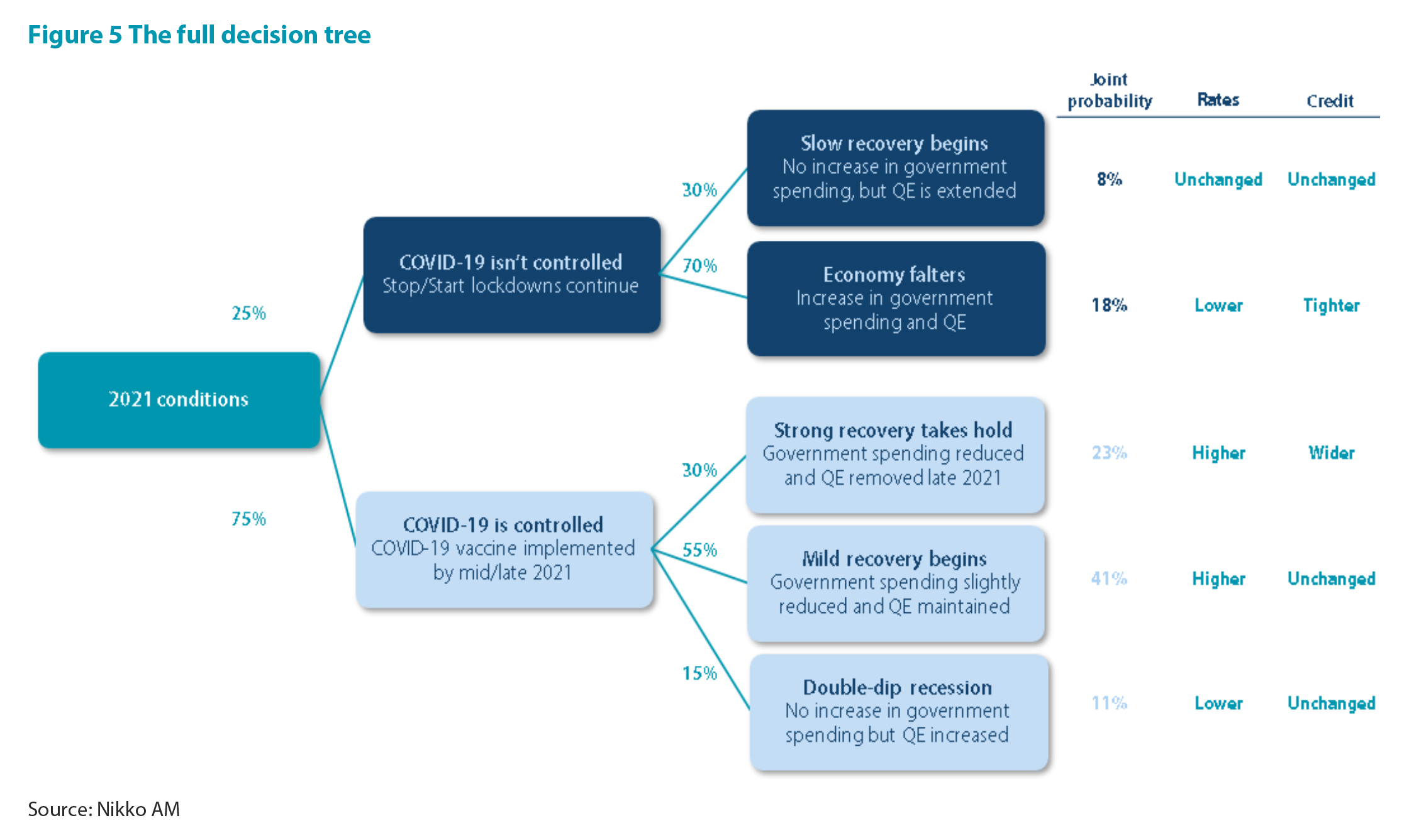

The decision tree

Those probabilities give the following decision tree and joint probabilities for a COVID-19 free recovery.

Assigning rates and credit outcomes

Our final task in our rates outlook is to assign expected interest rate and credit outcomes to each of our decision tree points. Doing so allows us to see a range and expected outcome for fixed income in 2021.

Interest rate ranges

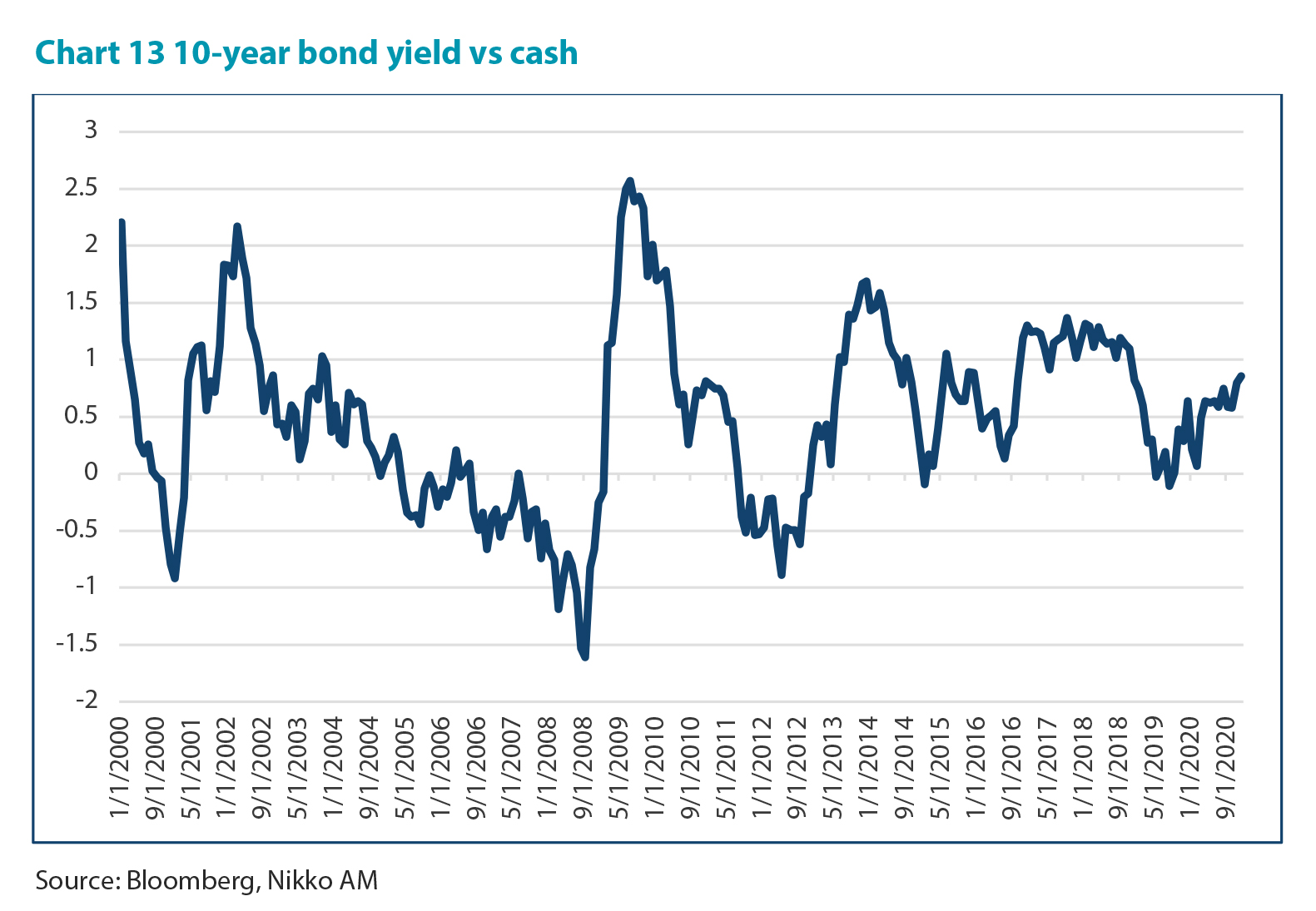

When assigning our interest rate forecasts, we use the spread between 10-year bonds and the cash rate to guide our thinking. This is a good way to derive our forecasts, as the spread to cash for 10-year bonds has been relatively stable, as Chart 13 shows—covering a 20-year history. Furthermore, since the cash rate likely won’t move next year, then this spread gives a strong indication of outright yield levels will be, by simply adding the expected spread to the current 0.1% cash level. As such, these ranges should give a reliable forecast for yields.

Using this range, we can make a number of observations about the interest rate outlook.

- Should the economy improve next year, then bonds should move back up towards the maximum of the range (+100 to +150bps) as the RBA‘s commitment to easy policy into the future will slowly be questioned. The stronger the outlook, the greater this should pressure the range. A good example is the 2013 period for a strong recovery and 2017 for a mild recovery.

- We do not think that the +200bps range of 2001 and 2010 will occur again in 2021. This is because those years came prior to RBA hikes—an outcome we don’t think likely to occur over the next 24 months. As such, we use 2013 and 2017 as the likely outcomes through a strong economy.

- Should the economy falter, then the potential for additional easing from the RBA will be priced by the market. This should see bonds drop towards the middle or bottom of the range (+0 to +50).

For our strong economic forecasts, we use a bond range of +100 to +150 basis points over cash (depending on the strength of the recovery), and for our weak economic forecasts, we use a +0 to +50 basis point spread to cash.

Credit ranges

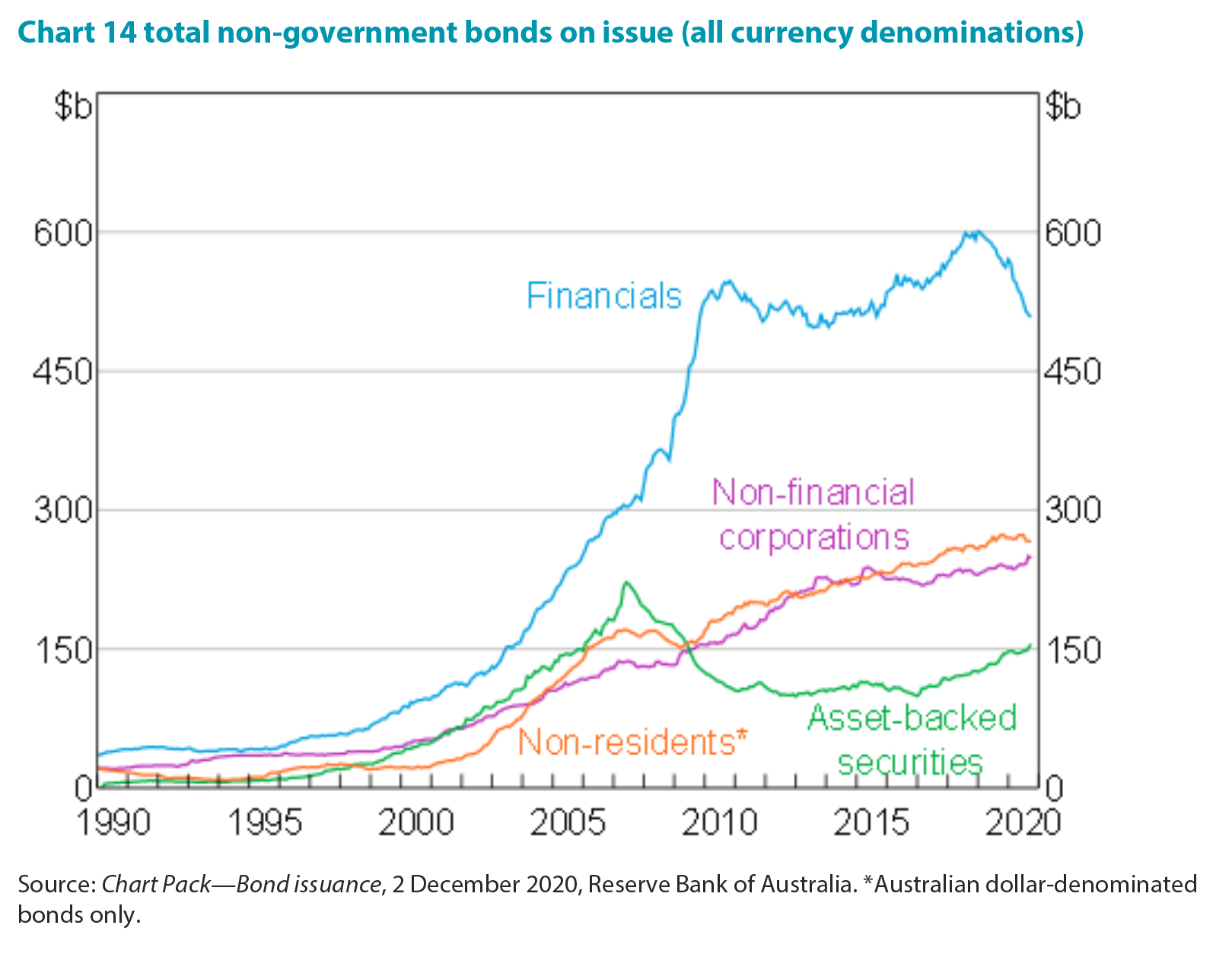

For credit, we need to take a short deviation to explain our ranges, as the credit environment isn’t behaving like its usual self. Typically, in a strong economic environment, the expectation is that credit spreads should tighten and then widen during economic weakness. However, credit spreads currently have reached levels which are, for some maturities, inside their pre-GFC lows. This has been driven by the RBA’s Term Funding Facility (TFF).

The reason for this is that the major banks are the largest issuers in the Australian bond market. By giving them access to 3-year funding at 0.1%, it means there has been almost no bank bonds issued over the past six months. This has caused the market to scramble to buy assets. Chart 14 shows that the volume of financial sector bonds outstanding in the Australian market has fallen by about AUD 100bn over the past 12 months.

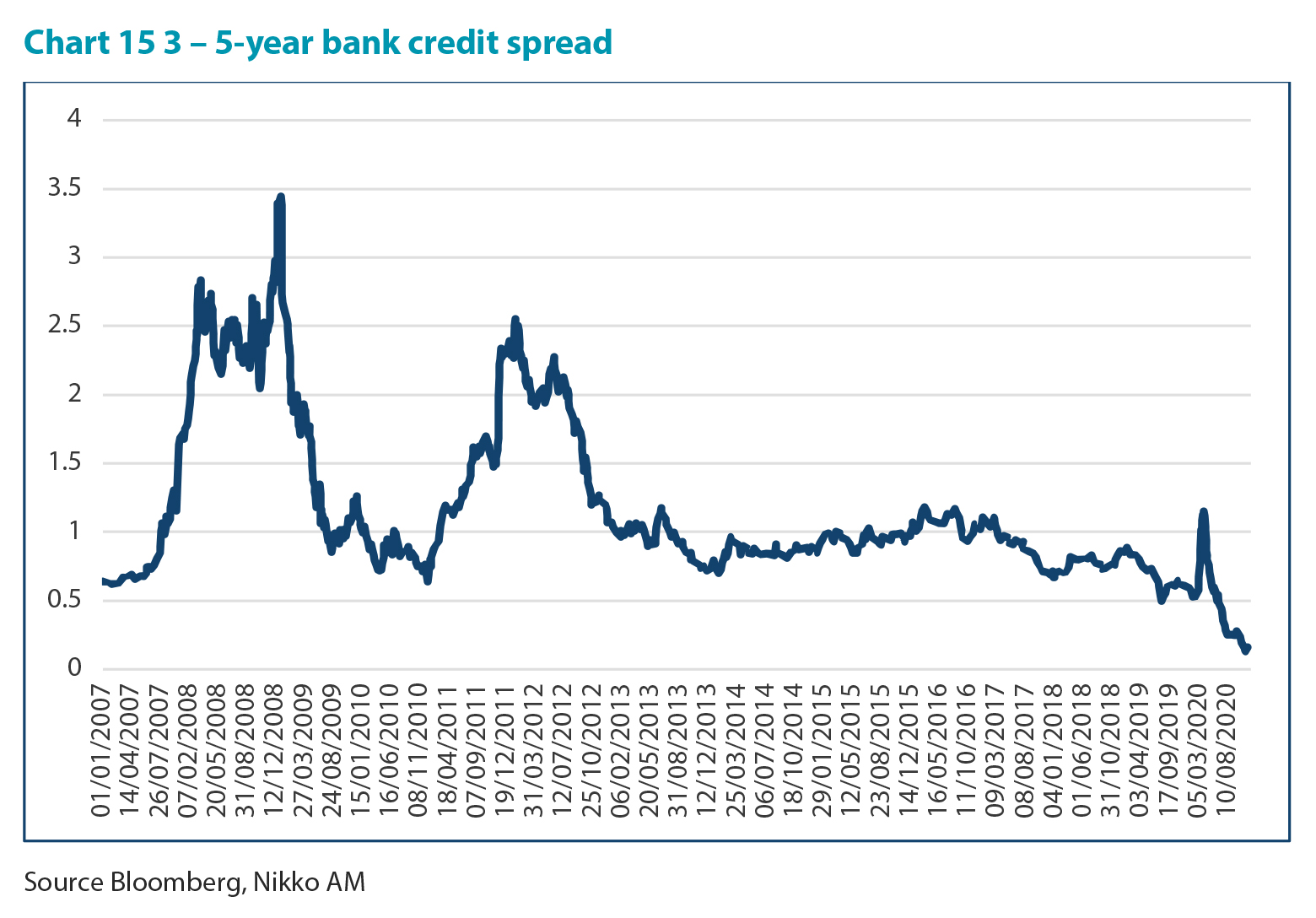

This has meant credit has been extremely well bid compared to the levels of supply. Major bank spreads have reached levels inside the 2007 pre-GFC tights and are offering very little compensation for credit risk. At around 20 basis points of yield pickup versus government bonds, spreads have become extremely tight.

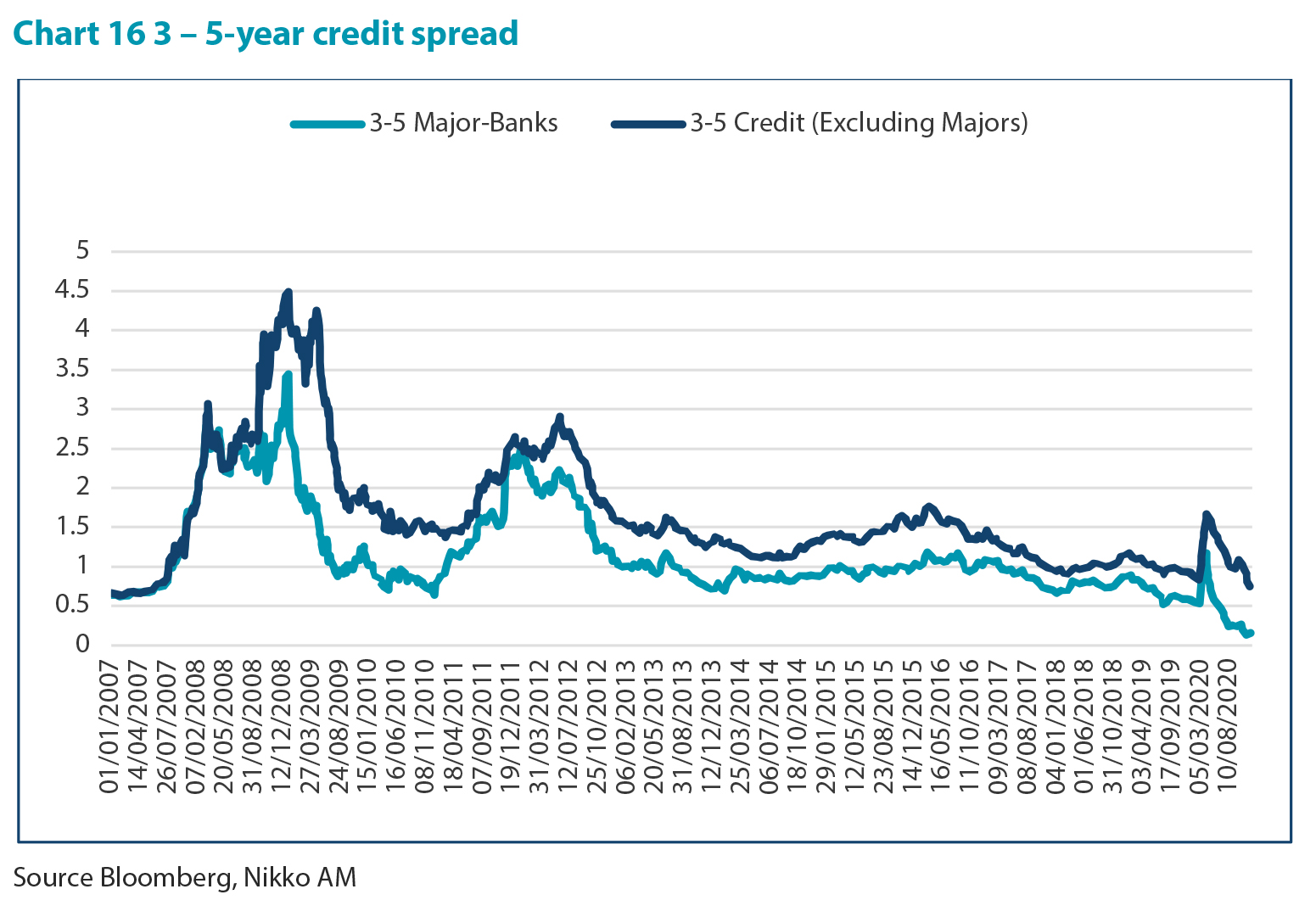

This lack of supply has also driven the rest of the credit market with it, with 0 – 5 year maturities now trading at close to GFC lows in terms of spread for corporate issuers. Considering the uncertain nature of the economy, and the amount of debt taken on over the past six months, this tells us that either the market believes there is no default risk, that QE works, or that supply has been an issue. We believe the last two are the correct interpretations.

Therefore, when we are forecasting credit spreads, we also need to make an assumption on what the RBA will do with its TFF. If the economy recovers strongly, then the RBA will likely remove the TFF policy and, perversely, this will likely see spreads back up. In this environment where the economy is strong, spreads should back up around 30 – 35 basis points— taking spreads in line with the outcomes of 2013 or 2017 economic periods.

However, if the economy is weak, then the TFF policy would likely be continued; keeping supply out of the market and spreads tight at their current levels. In this instance, the non-major bank issuers will have some compression left, but there will be little ability for major bank spreads to compress as there is no argument to be made that they should trade under government bonds.

This is the opposite of how credit spreads typically trade, making for somewhat unusual forecasts.

Forecasts

Using the above ranges, we make the following forecasts under each economic environment. It should be noted that the credit forecasts in the weaker economic environment are the only ones that we feel conflicted with, because despite supply being lower in those environments and the TFF likely extended, there is the very real risk of corporate defaults occurring if poor economic conditions continue for another 12 months.

The reason we have put lower spread forecasts in these environments is due to the fact that central banks globally have shown they will defend credit markets and corporates if required. As such, while we think an argument can be made for far wider spreads, at the moment we have forecasted it lower on the central bank support assumption.

Summarising our forecasts

The most likely outcomes

From our decision tree, the most likely outcome is that COVID-19 is controlled and that a mild (41%) or strong (23%) recovery occurs. This captures around two-thirds of the distribution. As such, the most likely outcome from this perspective is that interest rates rise in 2021 by about 20 to 60 basis points and credit spreads widen by about 30 to 40 basis points.

The sum product

This gives us a weighted average outcome. For interest rates, this currently sits at 1.03%, which is about 10 basis points lower than market pricing. Given the bulk of our distribution shows the economy recovering in 2021, in a normal year this would probably be higher. The weighted average sits at 1.03% as while our expected mean outcome for the economy is to recover, in the event that this is wrong rates would rally aggressively. As such, market pricing at the moment seems to reflect the view we have described above; cautiously pricing in an upbeat scenario that remains tenuous.

For credit, this sits at 0.90%, which is currently about 30 basis points higher than market pricing. For the credit outcome, this higher spread outcome makes intuitive sense as policy support should back away slightly. However, it would not be expected to occur until after the removal of the TFF. If the RBA extended this policy, we would forecast lower spreads.

The range

For interest rates, the range is relatively large, sitting between 0.5% and 1.60%. While the range of outcomes for the economy feels extremely wide at the moment, this range was not as wide as we would have expected coming into this process. This is because to get below 0.5%, we believe the RBA would need to institute negative rates, which they in no way look ready to do.

Alternatively, we believe to get above 1.60%, the market would need to start thinking about interest rate hikes. Again, not something the RBA seems ready to do. As such, the expected stability of the cash rate gives strong anchor for the yield outcomes in 2021, creating a range of 10-year yields which are tighter than the dispersed economic outcomes that are foreseeable.

For credit spreads, the range is relatively tight, between 0.5% and 1.20%. This reflects the fact that even if the economy improves, there is likely still going to be large central bank and federal government support in markets. This should cap some of the downside risks.

The simple distribution

Table 1 shows a simple distribution of the direction of rates and credit based on our probabilities. From this we can see that our expectations are that interest rates will rise slightly in 2021 and credit spreads will widen. The lower rates outcome of 29% seems broadly in line with how we felt about rates heading into this, i.e. it could go lower but the economic conditions are not pointing towards that outcome at the moment.

Conclusion

The most likely outcome from our perspective now looks to be that the economy begins to heal and with that comes a mild sell-off in interest rates and credit spreads. For a continued rally to occur, we believe that the economic situation would need to deteriorate or the vaccine prove ineffective—neither of which currently look evident.

By Chris Rand

————