Understanding the differences between ETFs, LICs and Unlisted Funds

What are the differences between ETFs, LICs and Unlisted Managed Funds?

Exchange Traded Funds (ETFs), Listed Investment Companies (LICs) and Unlisted Managed Funds are all popular vehicle structures amongst investment managers to deliver portfolios to their clients. While there are similarities between each structure, there are also a number of key differences that clients must be aware of, as these differences ultimately determine the most suitable vehicle structure for their specific needs.

What are ETFs and how do they work?

An ETF is a registered managed investment – a type of ‘unit trust’ – that trades on a stock exchange in the same way that a share in a listed-company does. Through a single tradeable security, unit holders gain exposure to a portfolio of securities without having to individually trade and hold these securities themselves. This gives them access to a diversified portfolio of investments through one single trade.

Although they share the same trading process, ETFs are priced differently to listed shares on an exchange. The share price of an ETF is based on the Net Asset Value of the Fund’s underlying holdings, similar to an unlisted unit trust. Their intraday price is referred to as the iNAV (intraday Net Asset Value), which aims to reflect the value of the portfolio’s underlying assets. As ETFs are priced based on their iNAV, they do not experience discounts or premia in the same way that market-priced securities do.

Like any share on an exchange, investors can buy or sell units in an ETF on the secondary market via their broker. They are open ended, meaning the number of units on issue can be increased or decreased in response to demand from investors. This helps ensure that the market price stays at or very close to the NAV. They trade intraday between buyers and sellers through a designated Market Maker. The Market Maker’s role is to provide liquidity to the market by quoting ongoing buy and sell prices throughout the trading day, which is referred to as the buy/sell or bid/ask spread. They place this spread around the iNAV and update it frequently throughout the day as the value of the Fund’s underlying assets change.

Passive ETFs

Due to their ability to track a portfolio’s net asset value, ETFs have become the first-choice vehicle for clients seeking passive investment strategies. Passive ETFs have existed since 1993 when State Street launched the SPDR S&P 500 ETF in the US. Clients now have access to a vast range of passive ETFs that track the indexes of markets, sectors, currencies, commodities and a plethora of themes and trends around the world.

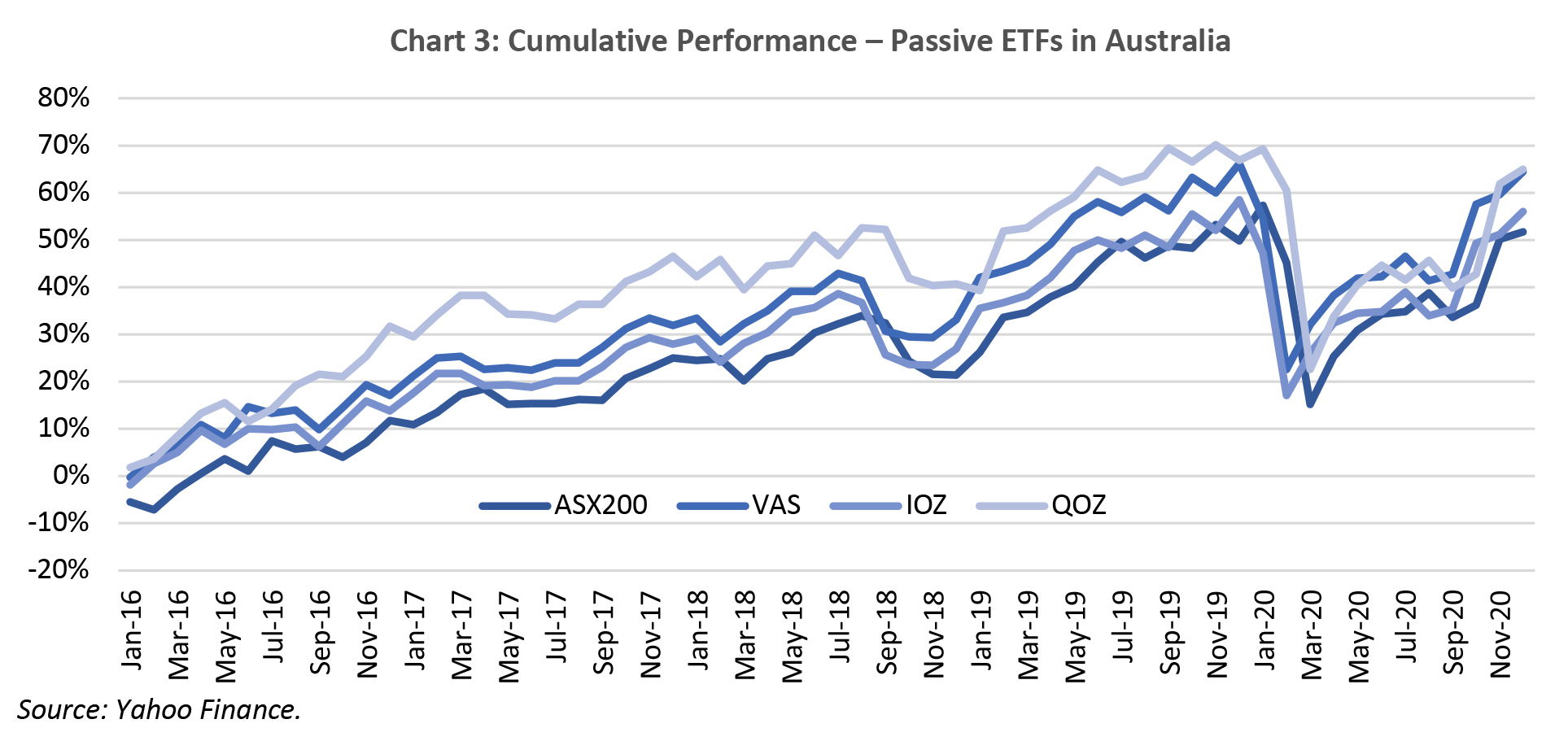

For clients who are not believers in active management, passive ETFs can offer broad Beta strategies with total costs typically around 40 bps. See below a fee breakdown of some popular passive ETFs providing broad exposure to the Australian market

These low all-in fees are reflected in the cumulative returns of each ETF shown below. The slightly different returns of each ETF are explained by the differences in their mandates. Over time, however, these passive ETFs provide clients with relatively similar returns.

Active ETFs

Although passive ETFs account for the majority of the market, active ETFs have seen a surge in popularity in recent times. In Australia, active ETF issuance started to evolve in early 2015 when issuers and regulators agreed on a portfolio disclosure regime that balanced the needs of clients who want to know what they are investing in with the protection of the investment manager’s intellectual property (its portfolio holdings and active portfolio decisions).

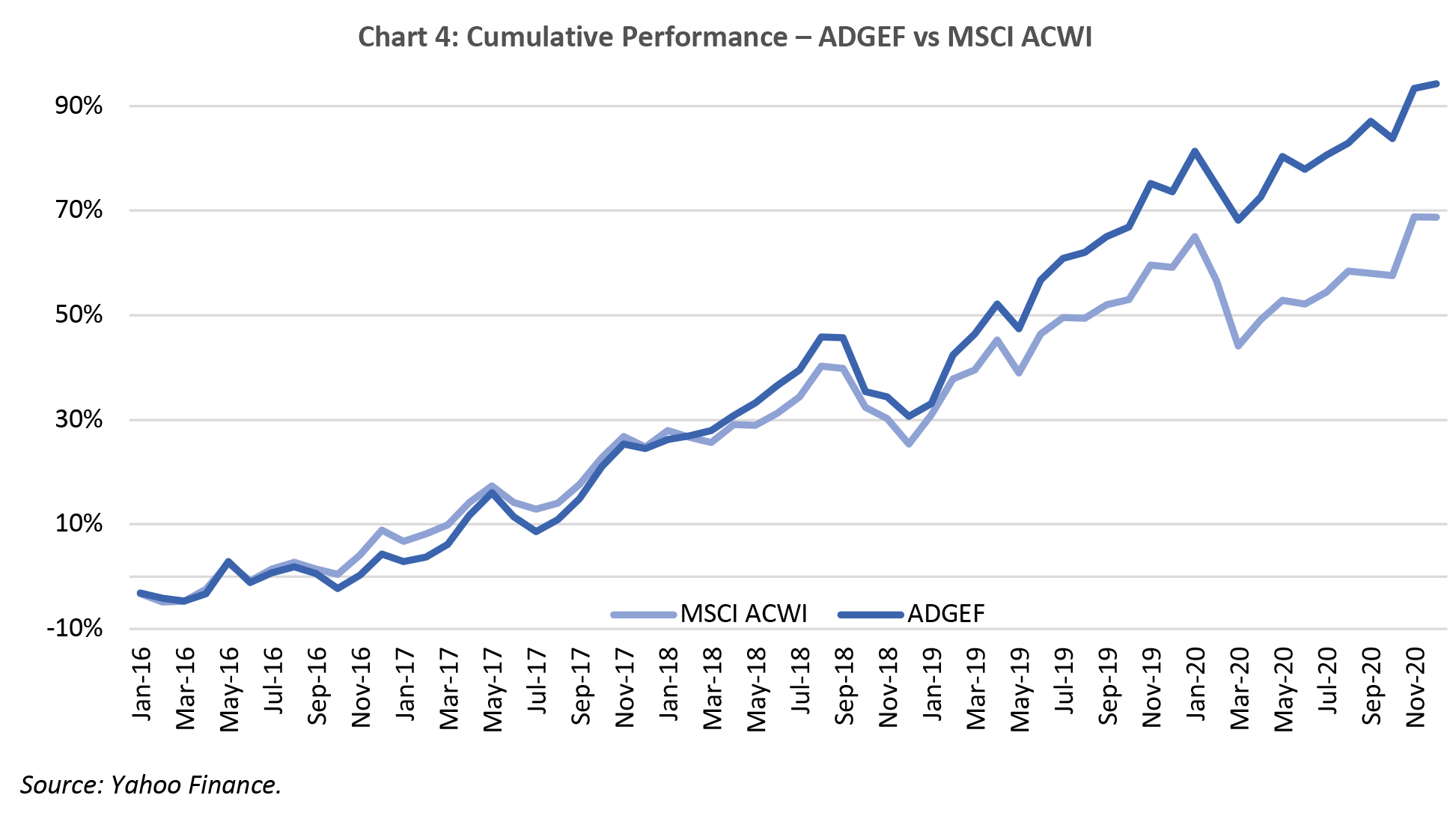

Whilst active products charge higher fees than passive products, the costs of active ETFs are coming down as more participants enter the market. The Apostle Dundas Global Equity Fund ETF (ADGEF), for example, will be coming to market with an all-in management fee of 0.9% p.a and no performance fee. This is expected to launch to market in late February. For clients who are believers that active management can deliver outperformance relative to the market over time, these slightly higher management fees are more than offset by superior performance. This is demonstrated by the Fund’s significant outperformance against the MSCI All Country World Index (ACWI), shown below.

What are LICs and how do they work?

An LIC is a closed-ended, exchange-traded vehicle that is unique to the Australian market. Unlike other investment vehicles, LIC unit holders do not hold a portfolio of assets. Rather, they hold units in an incorporated company, meaning the value of their investment is determined by market pricing rather than net asset value.

A key feature of LICs is the investment management agreement (IMA) they have with the underlying investment manager. These agreements are structured between 5 and 10 years, with the manager receiving locked-in fees for the duration of this agreement. Whilst this structure can be highly beneficial to investment managers, there are various features that are disadvantageous to clients, such as distributions. Unlike other investment vehicles that pass on all of their underlying assets’ dividends to clients, LICs have no distribution obligations. Rather, the LIC’s board of directors determines whether or not the company will pay a dividend and, if so, how large that dividend will be. For clients seeking income alongside capital appreciation, LICs are unlikely to be suitable investments.

Another disadvantage of LICs is that both investment managers and clients incur high costs relative to other structures. Firstly, managers incur high operating costs due to the incorporated company structure, which is consequently reflected in the fees charged to clients. Additionally, clients incur price costs due to the tendency of LICs to trade at a discount to their underlying net asset value.

A significant difference between LICs and other investment vehicles which clients should be aware of is their performance reporting. Whilst LICs report on the performance of their underlying portfolios like any other investment vehicle, this is not actually reflective of a client’s investment performance. Rather, LIC capital appreciation is determined by the securities price return, which is not disclosed in reporting. Although this can be easily calculated using historical prices, it is essential that clients understand the distinction between the performance reported by LICs and the actual performance of their investment. Additionally, LICs are only required to report gross returns when disclosing the performance of their underlying portfolios, whereas other investment vehicles are required to report both gross and net returns. This is also important for clients to understand as net returns reflect their realized investment performance.

What is an Unlisted Managed Fund and how does it work?

An Unlisted Managed Fund is a unit trust that can only be accessed through the Fund’s Investment Manager. Whilst their underlying portfolios are similar to those of exchange traded products, the key differences lie in the ease with which a client can make an investment in the Fund. They require a greater amount of administrative work than investments in a listed product due to the lack of a third-party administrative framework that public exchanges provide. The consequence of these greater administrative requirements is that clients cannot invest and withdraw their funds as quickly as they can on an exchange.

The terms of investment offered by unlisted fund managers can vary greatly between different funds. For example, whilst some funds offer daily pricing and daily liquidity, other funds may offer highly illiquid terms and can have lock-up clauses spanning multiple years. Although nuances such as this make unlisted funds less suitable for clients with minimal investment knowledge, they also provide a greater opportunity set than listed investment vehicles as they have access to a wider range of asset classes and investment styles. For example, whilst ETFs are required to limit their portfolio holdings to liquid assets, unlisted funds are unrestricted in the assets they can hold, which gives them a greater ability to provide niche strategies for specific client needs.

A less beneficial nuance of unlisted funds that clients should be aware of is that they have less stringent transparency requirements. Whilst all unlisted funds are registered under the Investment Company Act of 1940 and, consequently, must provide regular SEC filings, their disclosures are not made as publicly available as listed funds. For example, while listed funds have their portfolio holdings disclosures published quarterly on the ASX or Chi-X, unlisted funds are not required to make their disclosures publicly available, so long as they have been disclosed to the relevant regulatory bodies. Whilst this can be beneficial to managers seeking to protect their intellectual property, it has consequences for clients by making it more difficult to assess investment opportunities.

Comparison

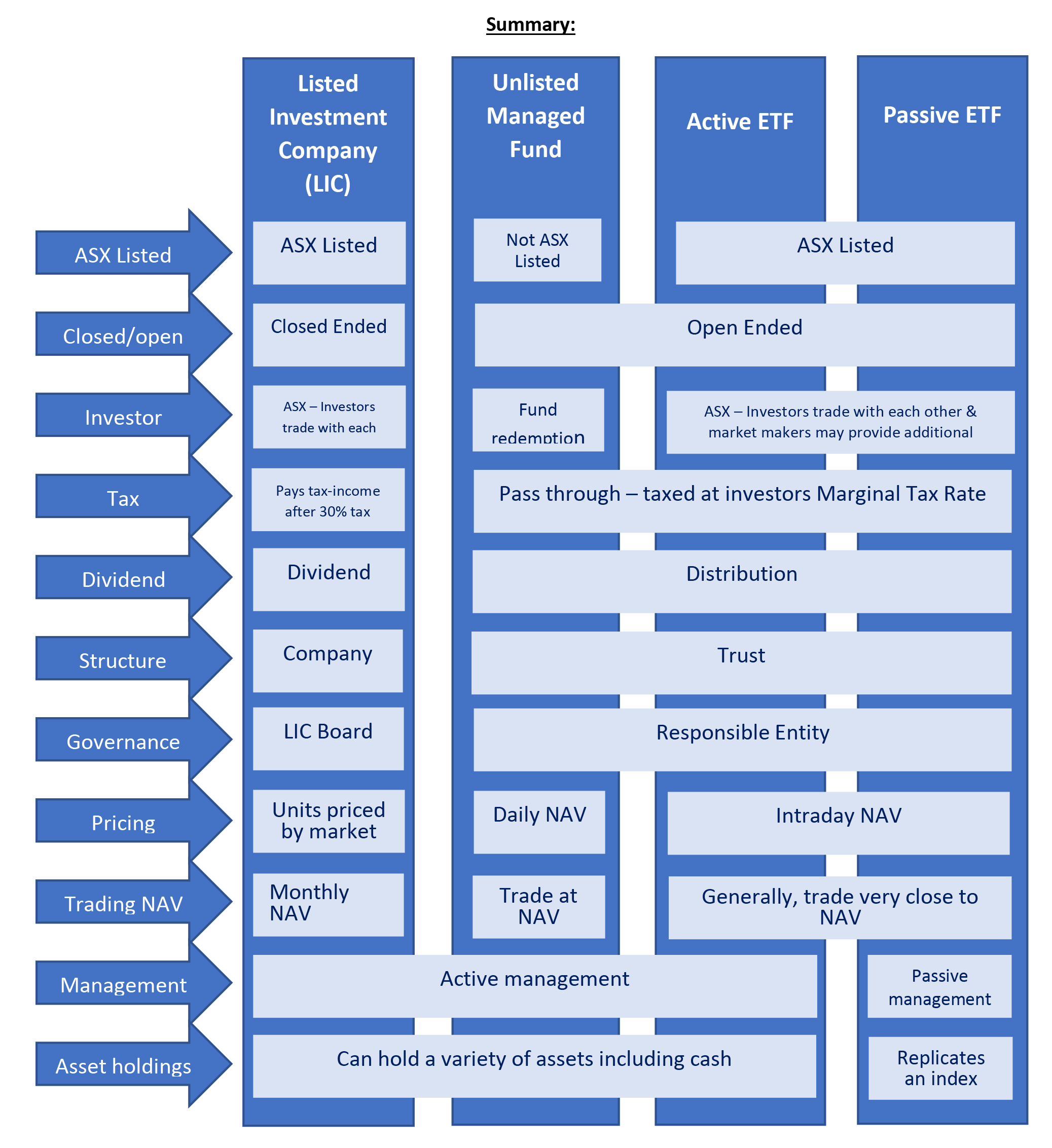

Structure

- ETFs are open ended, meaning the manager can issue or redeem units. Clients buy units in a Fund, meaning they gain access to the Fund’s underlying assets.

- LICs are closed-ended, meaning there is a fixed number of units on issue. Clients buy units in a company as opposed to a Fund.

- Unlisted funds can be both closed-ended and open-ended. Like ETFs, clients buy units in a Fund, meaning they gain access to the Fund’s underlying assets.

Unit pricing

- ETFs trade at iNAV, so client returns are in line with those of the underlying portfolio.

- LICs are priced by the market and can therefore be priced at a discount or premium to the underlying assets of the investment company.

- Unlisted funds trade at Net Asset Value. This is different to iNAV as it is priced periodically (i.e daily) as opposed to intra-daily.

Income

- ETF pass on all distributions from underlying assets to their unit holders.

- LIC managers have no obligation to pass on the dividends of their underlying assets to unitholders. The board of directors will determine the dividend payment each financial year, if they choose to pay a dividend at all.

- Unlisted funds pass on all distributions from underlying assets to their unit holders.

Fees

- ETFs tend to charge their clients relatively low management fees, but clients will incur brokerage fees every time they trade an ETF unit.

- LICs generally incur higher operating costs than other vehicles and, thus, charge their clients higher fees. A larger portion of LICs have active managers than ETFs, which in turn leads to higher management fees.

- Unlisted Funds vary in their management fees depending on multiple factors, such as capacity constraints and asset class. However, most unlisted funds are actively managed, leading to higher management fees than those in the predominantly-passive ETF market.

Liquidity

- ETFs have intraday liquidity, meaning clients can buy or sell their units quickly and easily via their brokers on the ASX or Chi-X.

- LICs also have intraday liquidity available, but their lack of a designated market maker means that liquidity is determined by market supply and demand.

- Unlisted funds have varying liquidity. The most liquid of these funds can provide clients with the ability to invest or withdraw capital in a matter of days.

Tax

- ETFs do not pay income tax as they pass on all income to unit holders. Clients are taxed at their marginal tax rate.

- LICs pay 30% income tax

- Unlisted funds do not pay income tax as they pass on all income to unit holders. Clients are taxed at their marginal tax rate.

Administrative ease

- ETFs are traded easily on an exchange through a broker.

- LICs are also traded easily on an exchange through a broker.

- Unlisted funds require greater administrative work due to the lack of a third-party administrative framework (such as an exchange). This is typically a T+2 confirmation process.

Consolidated reporting

- ETFs are required to disclose their gross and net returns monthly, as well as their portfolio holdings quarterly. These disclosures are publicly available on the ASX or Chi-X.

- LICs are required to report the gross return of their underlying portfolio. They are not required to report net performance, nor their unit price return.

- Unlisted funds must disclose their gross and net returns monthly, as well as their portfolio holdings quarterly, but are not required to make them publicly available.

Business approach to the Listed Markets

Apostle Funds Management currently manages A$1bn using Dundas Global Investors as the underlying global equity manager of an unlisted Trust.

Due to significant market demand and feedback, many of our clients have shown interest in a listed vehicle. We had the option of choosing between an ETF and a LIC. Weighing up the pros and cons as outlined above, we determined that an ETF option would suit our client’s needs best.

Many IFAs and brokers prefer the ETF structure to manage their clients’ equity holdings through CHESS. They see great value in the ETF model due to features such as intraday pricing and liquidity, which are not provided by unlisted funds. We view the addition of an ETF as providing multiple access points to one underlying portfolio to provide choice to the market.

Why ETF over LIC?

Clients will find an ETF to be more suitable than an LIC for two reasons:

- Pricing is determined by the underlying value (NAV) of the portfolio and do not trade at a premium or discount. LICs are likely to trade at a discount to NAV, so clients may not receive the full return provided by Dundas’ outperformance.

- Clients will also favour the ETF structure as unitholders will receive all distributions from the Fund’s underlying holdings. LICs are not required to pay these distributions.

Financial planners would need to explain why an LIC’s portfolio underperforms to the market when it is trading at a discount, which can be complicated and frustrating for clients.

———