Understanding greenhouse gas emissions and fossil-fuel reserve data is an essential element for advisers to understand when assessing ESG investment vehicles.

Discussions on carbon metrics are fast becoming a popular topic in investment circles. Carbon exposure is typically seen as a proxy for transition risk. Transition risk is a subset of climate risk associated with systematic shifts in regulation and consumption due to climate change.[1] Institutional investors, risk professionals and fund managers are increasingly looking to assess the exposure of their investments to carbon in order to manage transition risk, meet emerging regulatory standards, earn abnormal returns, or ensure that their values are reflected in their portfolios. This is Part 1 of the Climate Change and Investment Portfolios series.

Before developing and managing an investment strategy incorporating carbon exposure, it is crucial that advisers understand carbon metrics – that is, how carbon exposures are measured and calculated. Understanding the metrics used to manage portfolio carbon exposure allows an adviser and investor to better understand the channels of transition risk and make better evaluations of whether they believe securities are fairly priced. Furthermore, values-motivated investors may prefer some metrics over others due to subtle differences in their meaning.

This article provides more details on what carbon exposures are and how they are measured within the industry. We explain the difference between greenhouse gas (GHG) emissions and fossil fuel reserves, and how advisers and investors can calculate their portfolio’s exposure to each. We also discuss data providers in this space, and best practice for reporting on portfolio exposures. In Part 2 of the Climate Change and Investment Portfolios series, we will discuss various implementation considerations for investors considering taking the step to reduce the carbon footprint of their equity portfolios.

There are two primary categories of metrics used to measure separate types of carbon exposure. The first category is GHG emissions, and the second fossil-fuel reserves. We discuss what each of these are and how they are typical measured in the following sections.

Greenhouse gas emissions (GHG)

Carbon emissions are the releases of GHGs into the atmosphere through economic production or consumption. GHGs are typically expressed in CO2 equivalent units (CO2e) to allow for comparability between the different types of gases. In this section, we highlight how carbon emissions are classified, compared, and then aggregated into a portfolio-level metric.

Definition of emission scopes

Carbon emissions may be released at various points in the supply chain depending on the industry. Investors must determine which emissions are relevant to them, or “where the carbon buck stops”.[2] This distinction is captured by disaggregating the types of emissions into three separate ‘scopes’.[3] Scope 1 emissions are considered ‘direct’, while scopes 2 and 3 are ‘indirect’.

- Scope 1 refers to direct emissions generated as a result of industrial activity. These are emissions from sources owned or controlled by the entity. Typical examples include emissions produced from in-house manufacturing activity.

- Scope 2 emissions are those that are generated by the electricity, steam, heat and cooling that a company has purchased or consumed. Power generation is the largest source of emissions for many companies. The scope 2 emissions of one company are the scope 1 emissions of another.

- Scope 3 refers to all other indirect emissions not captured in scope 2, including both upstream and downstream emissions. This includes emissions produced by the inputs to the product or to get that product in the hands of consumers. Scope 3 captures the widest range of activity and leads to emissions being counted many times, since one company’s upstream scope 3 emission is often another company’s direct scope 1 emission.

Figure 1 illustrates an example of these scopes.

While there are different calculation methodologies in use, scope 1 and 2 emissions are widely calculated and increasingly audited. These are more-reliably measured and more-clearly defined than scope 3. Because of the sheer scale of scope 3 emissions, reporting, comparability, and reliability is limited. Some entities only report a subset of their upstream or downstream activities, and heavy amounts of estimation is often required. There are also concerns around double counting scope 3 emissions. Furthermore, because of limited disclosure, excluding or underweighting companies based on their scope 3 emissions is likely to penalise the first movers in this field. As a result, scopes 1 and 2 are the currently most used measures for estimating GHG emissions, although there are significant initiatives underway to increase scope 3 standards and usage.[4]

GHG exposure at a company level

Aggregation by gas

In the next step, the different emissions made by the same company are aggregated into one single variable. Currently, most carbon data providers offer aggregated emissions; this section provides information on how this is conducted.

There are many different GHGs that contribute to climate change with varying impacts. When investors use the word ‘carbon’ to refer to GHG emissions, they typically refer to all GHGs emitted expressed in a common unit – the carbon dioxide equivalent (CO2e). For example, 1kg of emitted methane (CH4) can be expressed as 25kg of CO2e, indicating that methane’s global-warming potential is 25 times that of carbon dioxide.

The CO2e for Kyoto gases are presented in table 1 below.[5]

Absolute vs standardised emissions

Investors may then choose to standardise GHG emissions for comparability across scale. Standardisation accounts for the fact that firms with larger revenues or assets are likelier to pollute more. Standardisation reflects a desire of the investor to measure their exposure to emissions efficiency over absolute emissions.

Non-standardised emissions are generally referred to as absolute emissions, whereas standardised emissions are referred to as carbon intensity. When carbon intensity is used instead of absolute emissions, an investor must choose which variable to use for standardisation. The most common method is firm revenue, but other options include enterprise value or units produced.

GHG exposure at a portfolio level

The resulting company-level CO2e is then weighted and aggregated in order to measure portfolio-level exposures to GHG emissions.

There are two types of approaches for weighting the GHG emissions of constituent securities (either in absolute or standardised terms); by portfolio weight or by ownership weight.

Portfolio weights are relatively straightforward, as CO2e is weighted by the exposure the investor has to that security relative to the entire portfolio. This is identical to how other investment metrics, such as valuation multiples or factor betas, are weighted when aggregated to the portfolio level.

Ownership weights involve allocating weights based on the size of an investor’s holdings as a percentage of the market capitalisation of the company. To illustrate, if an investor owns 5% of a company, then the investor also owns 5% of its emissions.

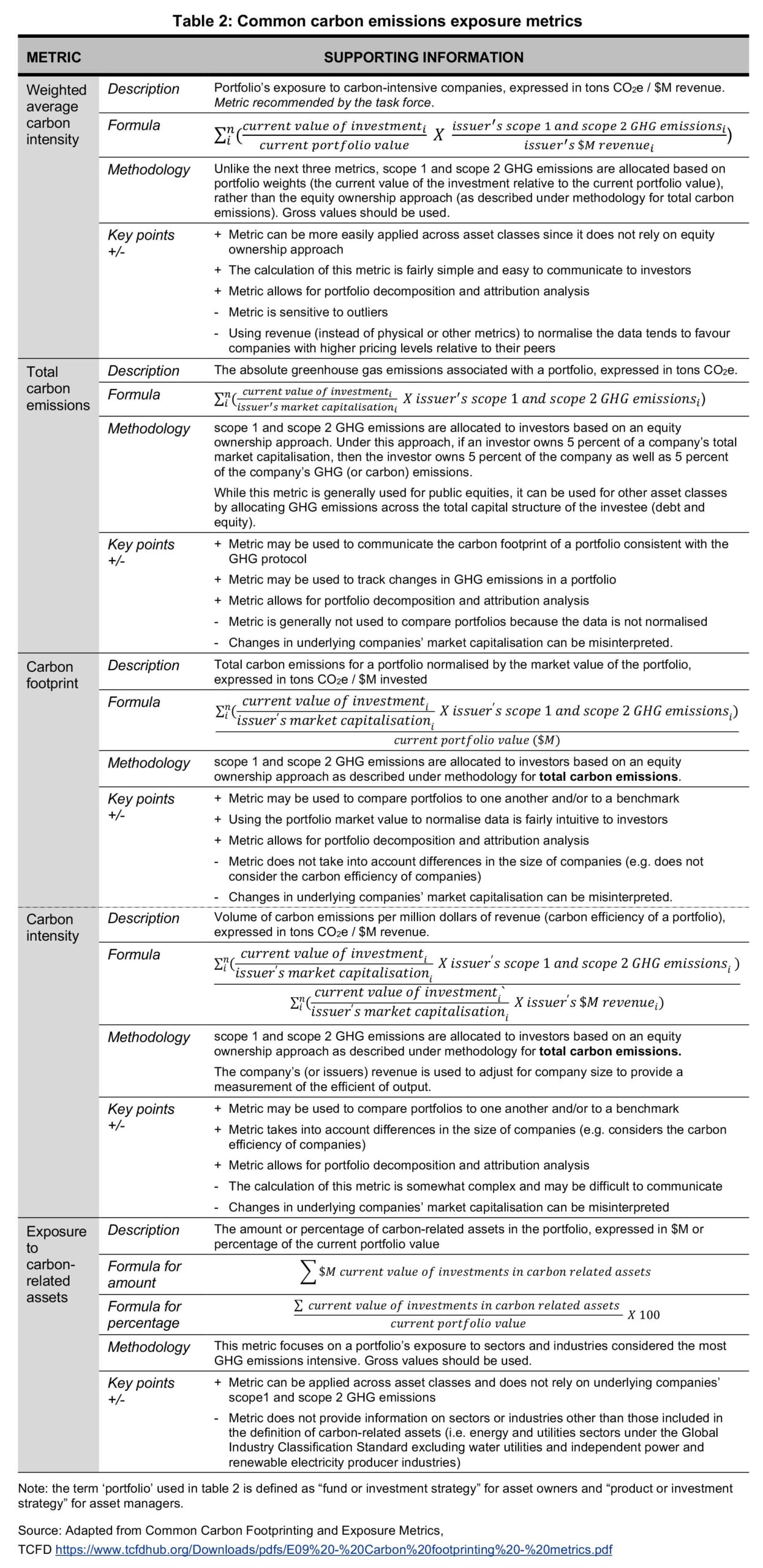

In table 2, we highlight an excerpt from the Task Force on Climate-related Financial Disclosures (TCFD)[6] Recommendations which provides a summary of popular GHG emissions metrics using both portfolio and ownership weights. The portfolio-weighted approach is used by the TCFD when calculating weighted average carbon intensity (WACI). Ownership-weights are used by the TCFD to calculate the portfolio metrics defined as ‘total carbon emissions’, ‘carbon footprint’, or ‘carbon intensity’.[7]

Weighted average carbon intensity

WACI is arguably the most popular of the carbon emissions metrics listed in table 2. WACI is useful from a risk perspective, as it provides a portfolio-weighted exposure to emissions in a manner like other measures of investment risk, such as market beta. When calculated using revenue standardisation, WACI has the advantage of proxying for the risk of carbon pricing. Revenue as a standardisation also has the benefit of matching two flow variables to one another (emissions over a year and revenues over a year). WACI is relatively simple to calculate and requires fewer variables compared to calculating ownership-weighted metrics (i.e., market capitalisation is not needed). However, WACI is sensitive to market movements; holding all else constant, a change in the price of a security will cause WACI to also change.

Total carbon emissions

Total carbon emissions is the simplest ownership-weighted carbon exposure metric listed in table 2. An advantage of this metric is it is unaffected by changes in company valuation, as changes in security price and market capitalisation cancel out. However, because GHG emissions are not standardised by revenue, the metric does not provide any information about how carbon-efficient the companies in the portfolio are. Furthermore, due to the ownership-weighted approach, for two portfolios with identical security allocations, the larger portfolio (in terms of dollars invested) will have a greater total carbon emissions score.

Carbon footprint

Carbon footprint is the total carbon emissions metric divided by the portfolio value. This standardisation allows for portfolios of differing sizes to be compared against one another. As a result, two investors with identical security allocations but differing portfolio sizes will still have the same carbon footprint. The other advantages and disadvantages of the total carbon emissions metric are also applicable to the carbon footprint metric.

Carbon intensity

The carbon intensity formula is a standardised, ownership-weighted metric. By dividing the total carbon emissions metric by the sum of ownership-weighted revenues of securities in the portfolio, the resulting metric represents ownership weighted exposures to emissions intensities. As a result of this standardisation, the metric also becomes comparable across portfolios of differing sizes. Due to the relatively complex calculation of this metric, carbon intensity may be relatively more difficult to communicate. Of the metrics listed in table 2, carbon intensity requires the most data for calculation.

Exposure to carbon related assets

Exposure to carbon related assets is the easiest metric to calculate and communicate in table 2, as it is simply the proportion of securities in the portfolio that meet whatever criteria is selected for defining carbon related assets. Despite its simplicity, the metric is not as informative as the others as it does not communicate to what extent the portfolio has exposure to carbon. Two portfolios could have the same exposure to carbon related assets but vastly different WACI or carbon intensity scores.

What is a good default metric?

We are of the view that WACI is reliable as a first-choice metric as it is simple to calculate and widely used. We recommend the use of WACI as it is the metric recommended by the TCFD, is used to create many decarbonised indices, and for its advantageous properties of comparability. Specifically, we prefer the calculation of carbon exposure through revenue standardisation and portfolio weights. Russell Investments uses the WACI metric to calculate the carbon exposure of its Low Carbon Global Shares fund.

However, it would be an overstatement to say there is a clear consensus on the use of WACI; the alternatives outlined in table 2 are all viable options that suit different purposes. For example, while the EU Technical Expert Group on Sustainable Finance (TEG) recommends using the WACI, it uses enterprise value to standardise emissions rather than the revenue-based calculation described above.

Forward-looking emissions

Reported carbon emissions are backward looking, which is an often-cited criticism. Incorporating whether emissions are upward or downward trending is likely to provide a better view of a company’s direction of travel. For investors who aim to manage risk, a metric which incorporates forward-looking trends in emissions may prove insightful. Such a metric may also match the preferences of a ‘values’-motivated investor.

While there is an increasing desire to use forward-looking metrics, there is no clear consensus around what constitutes a reliable forward-looking metric. We do not find that adjusting for trends in carbon emission metrics is common amongst low carbon strategies. Some quantitative interpretations may include green revenues or energy efficiencies (discussed later), however many forward-looking measures are qualitative and subjective, such as evaluating the quality of carbon-reduction targets. These measures are not easily comparable across companies, and actual progress towards targets can vary substantially

Maintaining data integrity is a critical component of any carbon management strategy; considerations of forward-looking measures should be balanced against the quality of that information.

Fossil-fuel reserves

Fossil-fuel reserves (sometimes referred to as carbon reserves or potential emissions) are another commonly used metric used in carbon management strategies and reporting.

Not all companies hold fossil-fuel reserves (only approximately 5% of the global large capitalisation index, by market capitalisation, own reserves), and as a result ‘full coverage’ of reserves is relevant to a smaller number of firms than that of emissions.

The following alternative approaches can be used to measure exposure to fossil-fuel reserves:

Percent of companies in the portfolio holding fossil-fuel reserves

A binary measure of whether a company has a claim on reserves or not. The results can then be aggregated at a portfolio level. It is likely that a materiality threshold would need to be employed above which a company is considered to have a claim on reserves.

This is a simple, unsophisticated approach that ignores the magnitude of reserves held by companies.

Potential emissions from fossil-fuel reserves

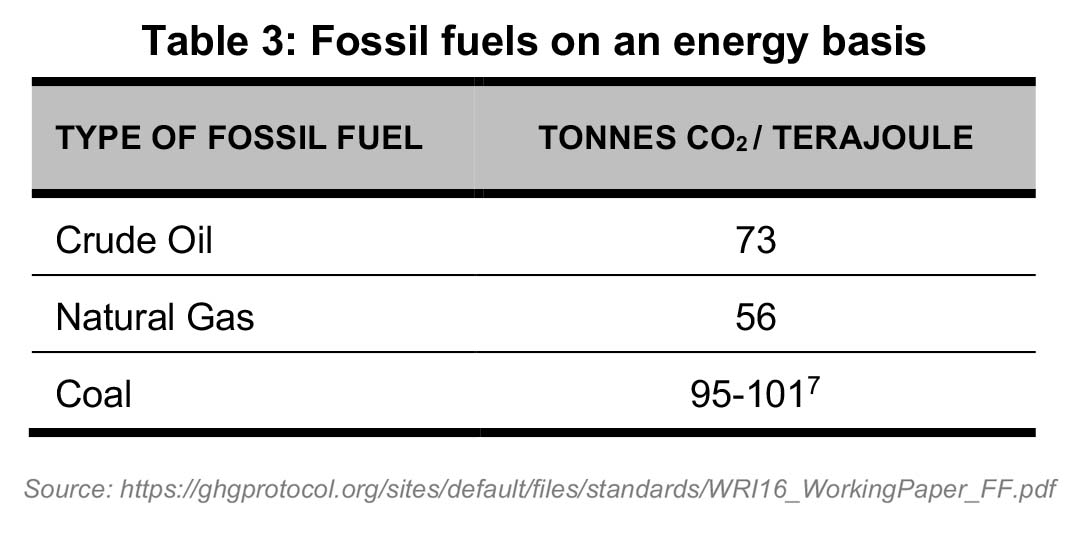

Coal, oil, and natural gas reserves are each converted into potential CO2e and then added together. Methods for converting fossil-fuel reserves into potential CO2e include:

- the energy basis, which looks at emissions per unit of energy

- the mass basis, which measures emissions per unit of weight

- the volume basis, which measures emissions per unit of reserve size

We provide an example of the energy basis method of aggregating fossil-fuel reserves in table 3. Similar to the CO2e aggregation, an investor can purchase this information already converted into potential emissions rather than needed to perform the calculation.

Similar to the CO2e calculation for GHG emissions, fossil-fuel reserves can be converted into standard units and added together. This measure can also be standardised; in contrast to GHG emissions, our preferred approach for standardising fossil-fuel reserves is to use total assets.[9] This standardised metric may be defined as a weighted average potential emissions intensity.[10]

Excluding or reducing exposure to fossil fuels is a common approach to reducing overall carbon exposure. Companies with fossil-fuel exposure are often defined using either a revenue threshold (e.g., deriving 10% or more from extraction or production of fossil fuels) or absolute exposure threshold (e.g., companies that hold proven or probable reserves). Once identified, these exposures can be managed on a spectrum, the same as GHG emissions.

Within fossil-fuel reserves there is a particular emphasis on exposure to coal companies. The most common outright fossil-fuel exclusion is on thermal coal.

Additional considerations

Non-corporate securities

Discussion around GHG emissions and fossil-fuel reserves is most developed around corporate debt and equity exposures. However, this excludes other asset classes – in particular, sovereign debt and private assets, which may be material. Within sovereign debt it is possible to look at country-level exposure to fossil-fuel reserves and GHG emissions, as well as investment in renewable technologies. These can include factors such as assessing sovereign dependency on fossil-fuel revenues and vulnerability to environmental risks.

Physical assets are also particularly vulnerable to climate risks, making this an important consideration in private infrastructure and real estate investments. However, data availability in these asset classes currently lag that of corporate debt and equity asset classes.

Portfolio scenario analysis and stress testing

In addition to understanding carbon exposure through the use of particular metrics, there is also increasing pressure on asset owners to consider the use of scenario analyses. The traditional risk tools of scenario analysis and stress testing can be used to understand a portfolio’s resiliency to a range of future states. A range of climate scenarios can be tested including ones that align with ‘business as usual’ or ‘2-degrees or lower’ scenarios.[11]

Non-carbon environmental metrics

We have focused primarily on carbon-related metrics but for many companies other forms of environmental exposures are also material. Besides carbon, the area with perhaps the most extensive reporting is water-related exposures, and in particular water withdrawal and/or water consumption as well as exposure to high-stress regions. Water is recognised as a material climate-related risk for many companies in industries such as food and agriculture, metals and mining, and energy production. Other areas of focus include biodiversity and waste management.

Climate-related opportunities

Since carbon-intensive activities are concentrated in a handful of industries, reducing carbon exposure by underweighting those industries is relatively simple in that it can be done without introducing significant active risk into the portfolio. However, this approach is increasingly being considered a form of greenwashing as it does not address the re-allocation of capital towards solutions for the transition to a low-carbon economy.[12] As a result, there is an expectation by some stakeholders that investor exposure to the clean-energy sector, green revenues or renewable energy be part of a low-carbon solution.

From a ‘value’ perspective, carbon exposures are a proxy for an investment’s exposure to transition risk, while climate-related opportunities measure the same factor albeit in the opposite direction. From a ‘values’ perspective, exposure to climate-opportunities may fit with an investor’s desire to be involved in the low-carbon transition.

Because climate-related opportunities are broad in definition, there is no consensus on a universal set of metrics that should be used for measurement and comparison. Furthermore, data on these metrics are still developing. Looking at the percent of company revenues classified as ‘green’ is one commonly-used metric. Another metric is exposure to renewable energy production.

The EU taxonomy for sustainable activities is a classification system designed to provide a common language around activities deemed ‘sustainable’. This new piece of regulation is set to come into effect in 2021.

Percent of portfolio invested in high-stakes sectors

As mentioned above, it is relatively straightforward to decarbonise by reducing exposure to high-stakes sectors, but given the level of investment required to fund an energy transition, this shift of capital out of these sectors arguably damages rather than facilitates a low-carbon transition. As a result, some new proposals require that these sector weights be maintained at benchmark levels, and shift the investments from the most carbon exposed companies within a given sector. In addition, having opportunities-related data, such as renewable energy exposure, can be a useful tool in identifying the best-in-class companies in sectors that are repositioning their business for the energy transition.

Measuring “Impact”

Some stakeholders may also be interested in understanding not only exposure to financial risks and opportunities but also how the portfolio contributes more pro-actively to real-world outcomes. For example, did an investment contribute to an outcome associated with the United Nations Sustainable Development Goals (UN SDGs)?[13] Frameworks for measuring impact are still developing and there is no clear consensus. An example of an impact framework is the Cambridge Sustainable Investment Framework.[14]

Data providers

Currently, data providers offer carbon metrics at both security and portfolio levels. Once an investor has access to carbon data and security information (i.e., weights / revenue / enterprise value / market capitalisation), the required metrics become easy to calculate and can be incorporated into a standard reporting workflow.

Our analysis of two flagship carbon data providers suggests a high degree of commonality between reported GHG emission data. However, differences are the most common where the data has been estimated by the provider rather than reported by the company. In our experience, these differences are larger for small-cap companies.

Table 4 shows the differences in the reported metrics of two flagship carbon-data providers based on a sample of data from 2017. The security-level coverage of data providers is variable. For example, while provider 1 covered 91% of the Russell 2000 index, provider 2 only covered 15% of that index in 2017. When coverage is low (i.e., 15%) then the weighted average carbon intensity score of the covered universe is sensitive to outliers and other small-sample biases. Despite this, the correlation of carbon intensity scores for overlapping securities between these providers is reasonably high (i.e., above 80%), suggesting that carbon data are consistent across these two providers and providing confidence in data quality.[15]

In figure 2 we illustrate the differences between GHG emissions data reported by the same two flagship data providers by plotting the absolute differences in reported emissions at the company level. The plotted line illustrates on the x-axis the number of companies that have differences in reported emissions equal to or greater than the number on the y-axis.

There are a handful of companies where the differences in reported carbon intensity between the flagship data providers are substantial. These tend to be companies for which the providers apply estimation algorithms due to the lack of self-disclosed data from the company.

Reporting

While several frameworks exist, there is no clear consensus for climate-related reporting since reporting is tailored to the climate-related objectives and targets, which vary by investor. If a portfolio is managed to a specific climate-related objective, reporting will often be aligned. Investors often disclose to stakeholders the same carbon metrics to which the portfolio is managed. Typically, an investor reports the relevant carbon metrics at the benchmark level as well as the actual portfolio level, along with any long-term climate-related goals for the portfolio.

Carbon exposure reports vary by region. In regions where regulation dictates what and how often asset managers should report, there is little flexibility in choosing a reporting frequency or metrics. External stakeholder pressures may also necessitate a greater frequency of reporting. Some entities are making carbon exposures part of their standard reporting, but it is common for climate-related reporting to take place annually.

As mentioned above, there is no clear consensus on what climate-related reporting needs to look like, there are several key frameworks, most notably the TCFD Recommendations. The TCFD reporting framework provides guidance for asset owners on both climate metrics, along with more static disclosures that illustrate the investor’s overall carbon management strategy. These include other components linked to carbon-related governance, climate strategy and risk management.[16]

Conclusion

Carbon metrics are an essential part of implementing a successful carbon-management policy. The difficulty in calculating a full measure of company carbon emissions (i.e. including scope 3) along with greater coverage of securities and asset classes on a forward-looking basis highlight that there is still work to do for the industry. Nevertheless, if investors are worried about the exposure of their portfolio to climate transition risks or want to match their investments with their values, understanding carbon metrics and their nuances is a crucial first step.

In this paper, we highlight how GHG emissions and fossil-fuel reserve data can be used to estimate carbon exposures, along with popular metrics recommended by the TCFD. We also discuss related considerations around assessing carbon exposure, such as forward-looking emissions and exposures to assets funding the low-carbon transition.

By Mihir Tirodkar, PhD, CFA, Senior Analyst and Emily Steinbarth, CFA, Senior Quantitative Research Analyst

———