The benefit to investors of buying real assets through fractional investment

For those retirees with reduced income potential and diminishing super savings, the family home may be their saving grace.

Covid highlights the retiree dilemma

If you are looking for one word to describe 2020, volatility would seem to fit the bill. Every aspect of our lives, whether it be financially, socially, or work, was like a roller coaster ride. Into lockdown, out of lockdown, especially in Victoria. Often isolated from family or close friends. And then coping with investment markets still giving a good imitation of a yo-yo.

COVID drove us indoors, suspended our social lives and devastated businesses and personal incomes. That quaint phrase all those years ago by the Queen, when she described 1992 as her “annus horribilis”, comes to mind.

Many people either received JobKeeper (now officially ended) or higher JobSeeker payments to tide them over, but others haven’t been so lucky, with senior Australians certainly in this category receiving very little financial help to bridge the gap between what they receive and what they need.

At the same time, many of these retirees are finding that the traditional asset allocation split between equities, property, bonds and cash is not necessarily doing them any favours in the current environment. Dividend income is under pressure, property faces several issues around rental income, interest rates remain at record lows, as well as bond yields. In short, a bleak outlook.

It’s time to think outside the square, to examine emerging sub-classes of assets that could provide better income and capital growth. And these investment options can come with other benefits such as diversification and social responsibility without sacrificing liquidity or sharply increasing risk.

Syndication or fractional investment puts another option on the table, allowing retirees (and other investors) to invest in these assets at a lower entry price, as well as offering the opportunity to deliver diversification, minimise risk and increase returns.

Equity release

Enter the family home. For those retirees with reduced income potential and diminishing super savings, the family home may be their saving grace.

And for investors, with property tipped to increase dramatically, it could be a boon with the addition of a guaranteed rental return, no tenancy risk (seniors stay in their property and only pay rent on the percentage of the equity they sell), a secondary market to exit and a long-term time horizon.

A key pillar of Australia’s future retirement income policy must be the family home (although the Government still must figure out how), with the parlous state of the economy and volatile markets almost making this inevitable.

For this to happen it will become imperative for financial advisers to be involved in providing the necessary planning for our aging population, many of whom are vulnerable, potentially open to elder abuse and possibly not armed with the necessary knowledge to make informed decisions.

Whilst downsizing is an option there are several considerations, among them, the social and lifestyle impact of moving and the cost of selling, repurchasing and moving. Downsizing could be a consideration if using some of the proceeds top up super is an objective.

If staying or aging in place is a key objective, there are only four avenues for home equity release from only seven providers for a very large demographic that will require access to their home equity over the coming years. They are:

- Government Pension Loan Scheme – a prescriptive Government funded home equity release solution linked to the Aged pension with a limited pension payment option only. Repaid upon sale of the property.

- Reverse Mortgage – four providers – funded by lending markets, similar to a home loan but with no regular repayments required. The capital and interest is repaid upon sale of the property. Residual equity uncertain.

- Home Reversion – one provider only. Postcodes where this is available are very limited. Residual equity uncertain.

- Equity Release Agreement – one provider – can be funded by family, friends, individual investors or institutions. Fixed costs. Residual equity more predictable.

There is also the potential for seniors to make downsizer contributions under the legislation from their home equity. This can occur in one of two ways. The first is to sell the family home, downsize to a cheaper home and top up super from the proceeds, up to $300,000 per spouse. There are some rules around this, among them, how long the home has been held, the age of the members and when the contribution is made in relation to the settlement.

The second is to enter an equity release agreement to sell a fraction of their family home, stay put and use the sale proceeds, again up to $300,000 per spouse to top up super to increase income. There is only one Fund that can do this at this time, the DomaCom Fund.

The time is here and now for advisers to get up to speed in this sector, to engage the seniors market, and their families where this is appropriate, and provide the solution most suitable for each individual or couple needing equity release to provide for a financially fulfilling retirement.

With a new fractional debt-free senior equity release product guaranteeing long-term rental income and a share of the future capital value of a wide range of residential property, advisers can control both ends of the transaction. This can be helpful where investors in a senior’s property are related parties.

The long-term nature of seniors’ equity release properties is ideal for SMSFs which, by their nature, have a long-term outlook in the accumulation stage. It also dovetails with the financial needs of many seniors who similarly have a long-term horizon regarding their retirement funding.

The release of the new fractional model that comes under the Equity Release Agreement[1] enables this to occur because the fractional model is the only financial product in the equity release space.

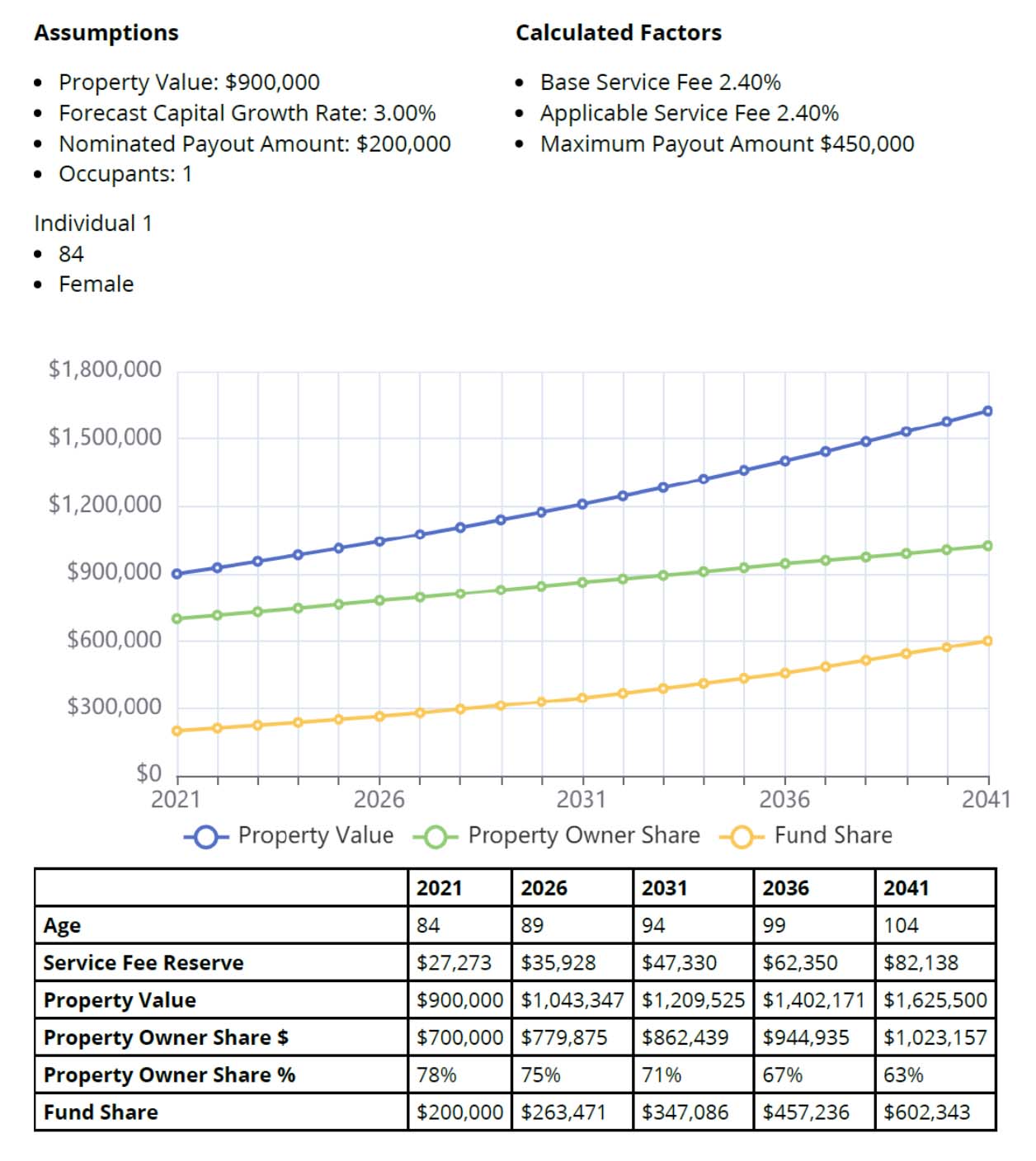

Case study on equity release

- Gwen is 84 and owns a mortgage free property worth $900,000

- She needs $200,000 for a more comfortable retirement

- Her 4 children have shown a desire to help their mother in retirement

- Funding options under consideration include:

- Personal loans from the siblings to Gwen

- Reverse Mortgage

- Government Pension Loan Scheme – no lump sum

- Home Reversion Scheme

- Senior Equity Release – funded by children

- Because the Senior Equity Release the vendor (Gwen) must receive financial advice and it is recommended that siblings are also involved and receive financial advice (a possible client generation opportunity)

- Senior Equity Release has a calculator to model and illustrate the outcome

Considerations:

- Centrelink entitlements need to be considered when deciding on the settlement outcome i.e. lump sum vs flexible monthly payments

- The children can agree to any rental income between 0% and 3% the life of her equity

Benefits:

- Gwen is able to remain in situ

- She can ‘bequeath’ part of the children’s inheritance whilst still alive

- She can choose to receive a lump sum or a flexible monthly payment

- If necessary she move into an Aged Care facility and lease out her house and keep the rent (which could be used to pay her daily room charge)

- The DomaCom Fund provides a third-party structure with independent Trustee and Custodian to avoid any possible family disputes

- There is a liquidity facility (secondary market) that enables individual siblings to exit the investment if required

- The children will receive investment returns (capital and agreed income)

- Following confirmation from the ATO, Gwen may also contribute the $200,000 released into Super if she wishes under ‘Downsizer’

Property assets with income and growth potential

There are other models open to investors such as the property savers market. Saving for a deposit traditionally meant piling money into a bank account where the return tracked interest rates and, when you had sufficient capital, it became a property deposit.

Today, this approach means almost zero interest will be paid on any bank savings. But there is an option that allows a small investment to grow with the property market: a simple residential fractional property syndicate where buyers can invest via a syndicate in an area where they want to live. For example, if you want to live in Carlton or Balmain you can invest in a property in those areas with, but independently of, other like-minded investors.

One fractional model seeks out developer discounts by buying several properties in a single tranche then splitting the discount (which can be from 10% to 20%) between investors and tenants.

Discounts come from developer savings on sales commissions and marketing and are passed on to investors and tenants resulting in an immediate uplift in capital value. It’s like bulk buying for investors.

Investors, whether they are saving for their own home or investing for the longer term, also get less tenancy risk as the tenants earn equity over the period of their tenure.

The beauty of this innovative model is that the savers can also be the tenants and get an extra lift in their savings if the property is where they want to live.

Indicative capital growth for this investment model is about 5% with additional estimated yields of 3 being a fair indication of the broader market

Investing that helps others

Disability and affordable housing are in high demand and can’t be built quickly enough to satisfy the demand. Investors stand to benefit from Government subsidised housing in the form of very low interest rates (2.5%) and/or subsidised rent payments to owners.

Where this model is used in the affordable housing space for essential workers, the “bulk-buying” discount from developers also applies as does the tenant share of discount. Indicative growth in the affordable housing space is around 8% to 10, owing to the geared nature of the investment.

In both models, tenants having equity also provides market depth for investors as they will soak up equity from others as and when they can do so from their savings and income.

Both models are well worth understanding if advisers want to offer better income and growth prospects to clients.

Renewable energy and “future” investments

For income, renewable energy projects are another way to go. Low on capital growth but high on the income side with a depreciable asset, renewable energy is here to stay.

For those clients with a longer-term time horizon, land banking might be their cup of tea if they think rezoning for future use will increase values.

Another area that has done well for many investors is rural farmland, a commodity that has appreciated well over the past few decades and one that attracts better rental income than many capital city residential properties. It’s also a “green” investment, as well as assisting our next generation of farmers to work the land without the pressure of large mortgages, allowing them to sow their capital more productively.

Rental returns are usually in the 4% to 5% range and passive non-farm income is also possible. Growth figures are positive with an estimated 6% plus average annual growth

The fractional investment model gives investors the ability to syndicate into loan or individual mortgage sub-funds to lend to specific properties or developments with first mortgage security and, typically, earn 5% p.a. plus. Where developments are concerned this is cheap settlement insurance.

Advisers are in the box seat with most of these investment models as they can structure both sides of many of the transactions between retired income clients and wealth accumulator growth clients. Advisers can also assist liquidity by matching various client needs internally via their client bases.

The shape of investing is changing in many ways, providing financial advisers and their clients with multiple avenues to achieve financial goals beyond the traditional equity, property, cash and bond markets.

———-