Weekly market update – week ending 30 April, 2020

Investment markets and key developments over the past week

Share markets were mixed over the last week with US shares rising to new record highs helped by good economic data, strong earnings and more stimulus and Chinese shares rising but European and Japanese shares fell. Australian shares also fell back slightly as the local market continues to work off technically overbought conditions after its early April surge. Weakness in retailers, IT, health and telco stocks particularly weighed on the Australian share market over the last week. Bond yields rose in most major countries. Oil and metal prices rose but iron ore prices were flat at near record levels. The $A rose as the $US fell further.

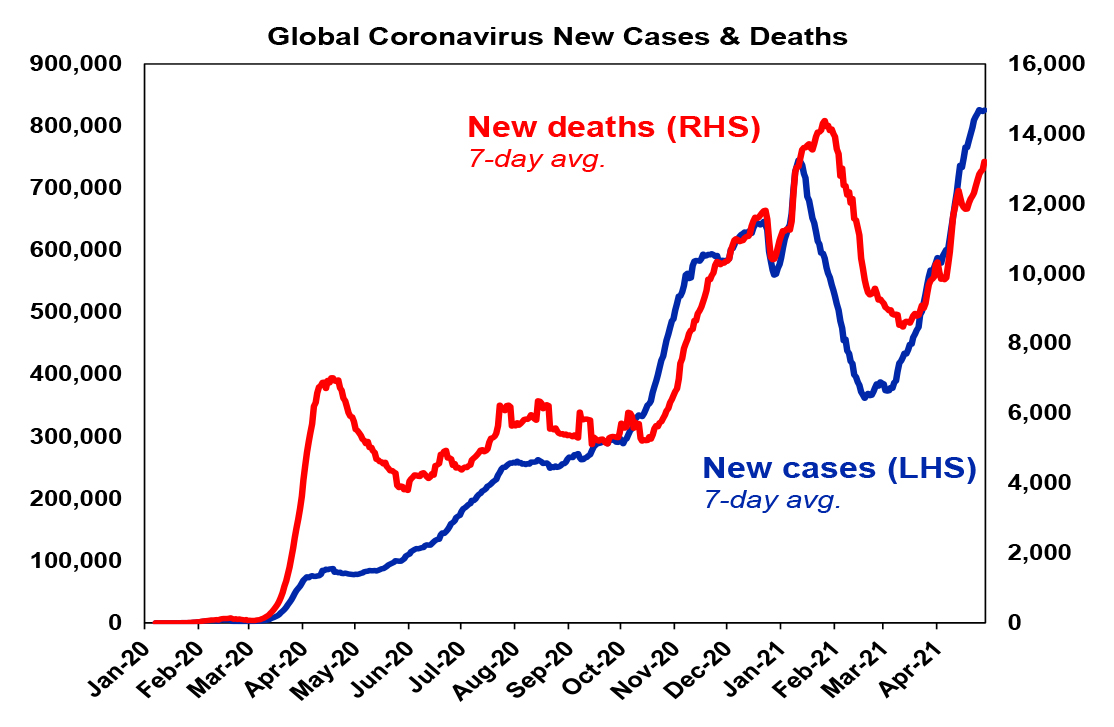

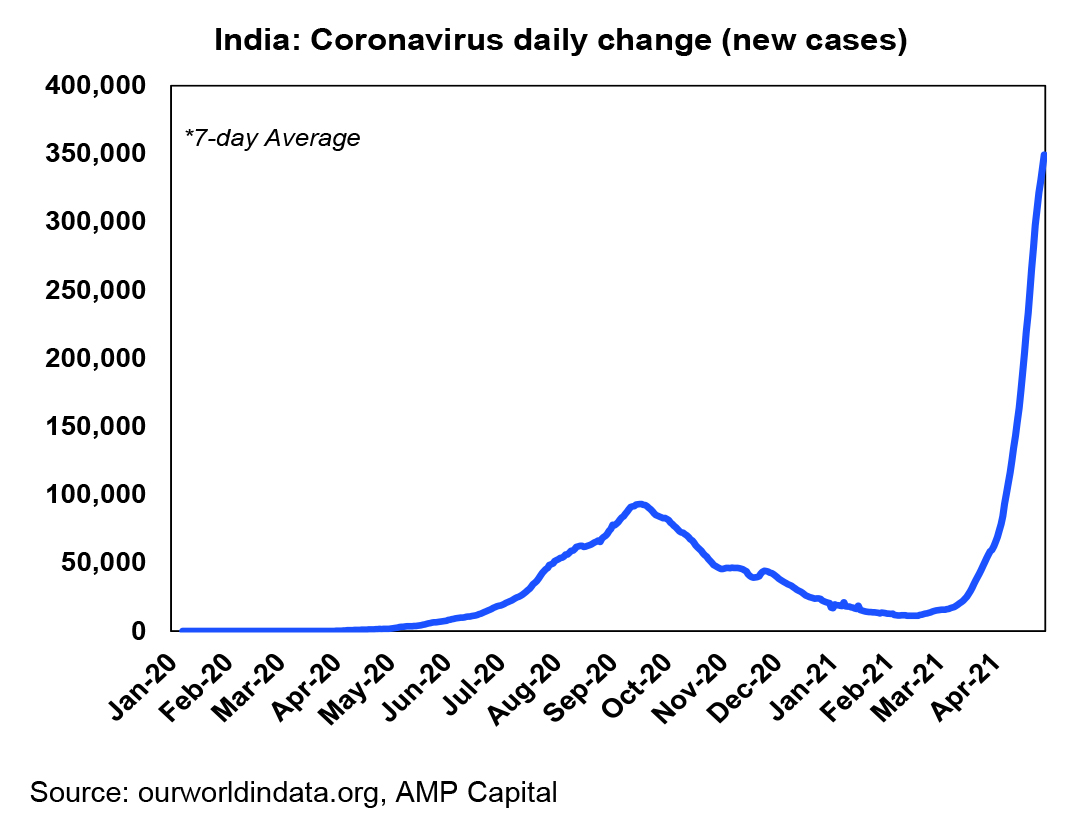

First the bad news. The latest rise in new global coronavirus cases and deaths continued over the last week, with India accounting for over 40% of new cases. New cases and deaths are declining in developed countries – with the US trending down and Europe slowing again, although Japan still has a problem and has announced a third state of emergency.

Fortunately, new cases in Australia remain low and due to returned travellers and the snap lockdown in Perth worked in limiting another breakout from the quarantine system.

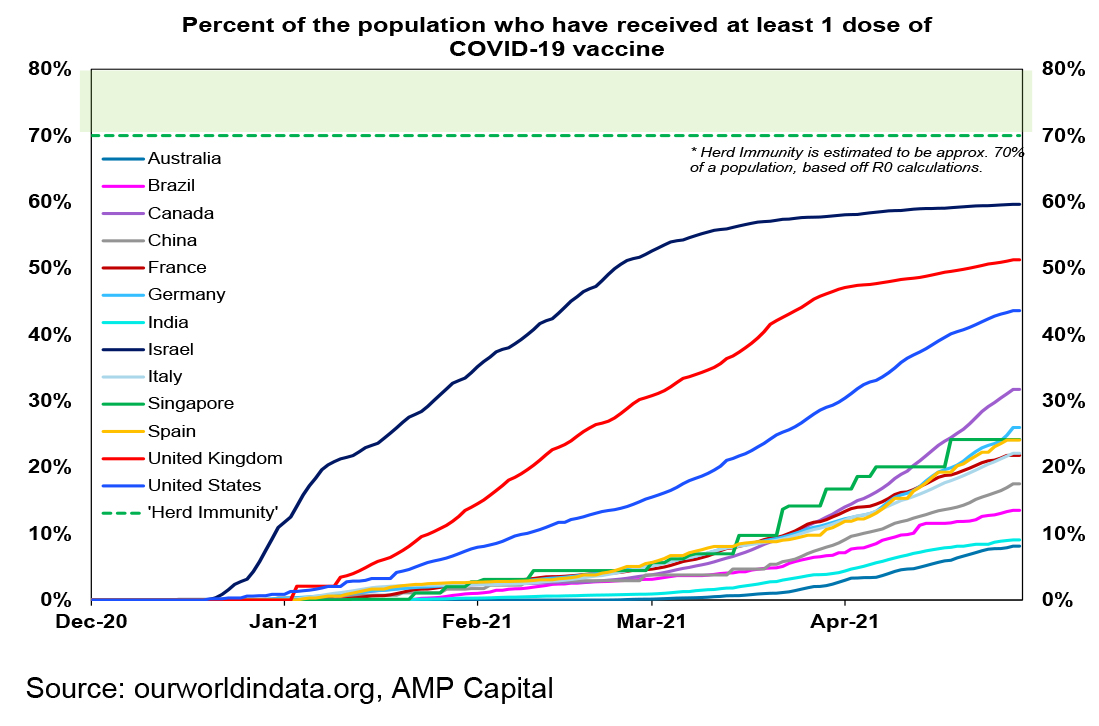

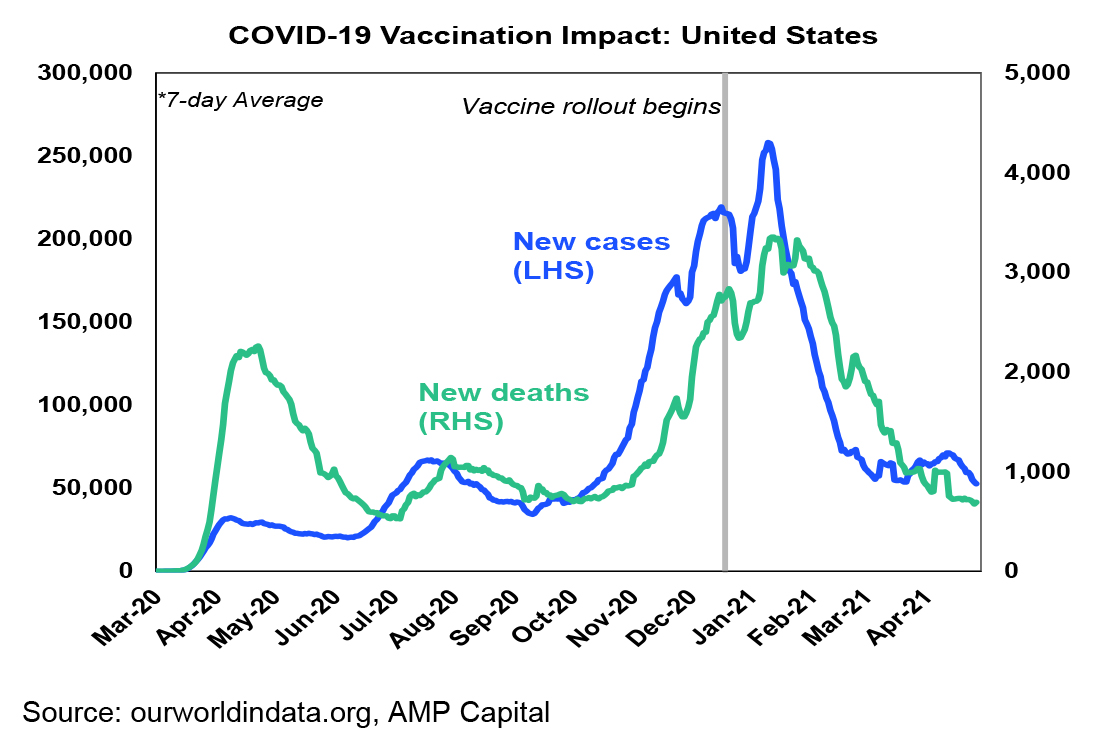

More broadly, the good news continues to dominate globally. First, the vaccination rollout is continuing – and they work. So far around 8% of the global population has now received one dose of vaccine – with 44% in advanced countries and 6% in emerging countries. Within developed countries the UK is leading the charge at 51%, the US is at 44%, Europe is at 23% with Australia well behind at around 8% (but picking up).

In developed countries the main risks relate to reopening before herd immunity is reached and hesitant take-up (following the bad headlines around the vaccines). The damage from the former is being minimised by vaccinating older/at risk groups and the issue of take up can be resolved by “vaccine passports” – with, eg, the EU talking of allowing American tourists back if they are vaccinated. Meanwhile, surging vaccine production will see vaccination in emerging countries accelerate.

Second, stimulus continues. President Biden confirmed his American Families Plan with an extra $1.8 trillion in spending over 10 years on childcare, education and paid leave partly funded by tax hikes including an increase in the top income tax rate rate, an increased capital gains tax for very high income earners (just 0.3% of taxpayers) and increased auditing of high income earners. As with the proposed increase in the corporate tax under the American Jobs Plan, the increase in top personal and capital gains tax rates will likely be watered down by Congress and there is an offsetting boost to spending which given that its focussed on lower income earners should boost corporate revenue. So, the US share market reaction was positive. Bear in mind though that both the $2.25trn American Jobs Plan and the $1.8trn American Families Plan are both spread out over a decade or so and won’t start till next year so the additional stimulus is minor compared to the $5trn paid out in relation to the pandemic stimulus. And both plans face challenges in getting through Congress.

Meanwhile, also in the US the Fed remains very dovish. While it was more upbeat on the economy and noted that inflation has risen it still sees the latter as “transitory” with Fed Chair Powell indicating there is still significant slack in the economy, “it will take some time before substantial further progress” is made towards its goals and so its too early to be “talking about tapering” its bond buying. We expect the taper talk at the Fed to start around September though.

Thirdly, economic data remains consistent with global recovery. US GDP surged 6.4% at an annualised rate in the March quarter and Eurozone economic sentiment surged to historically high levels in April pointing to a strong recovery once covid settles.

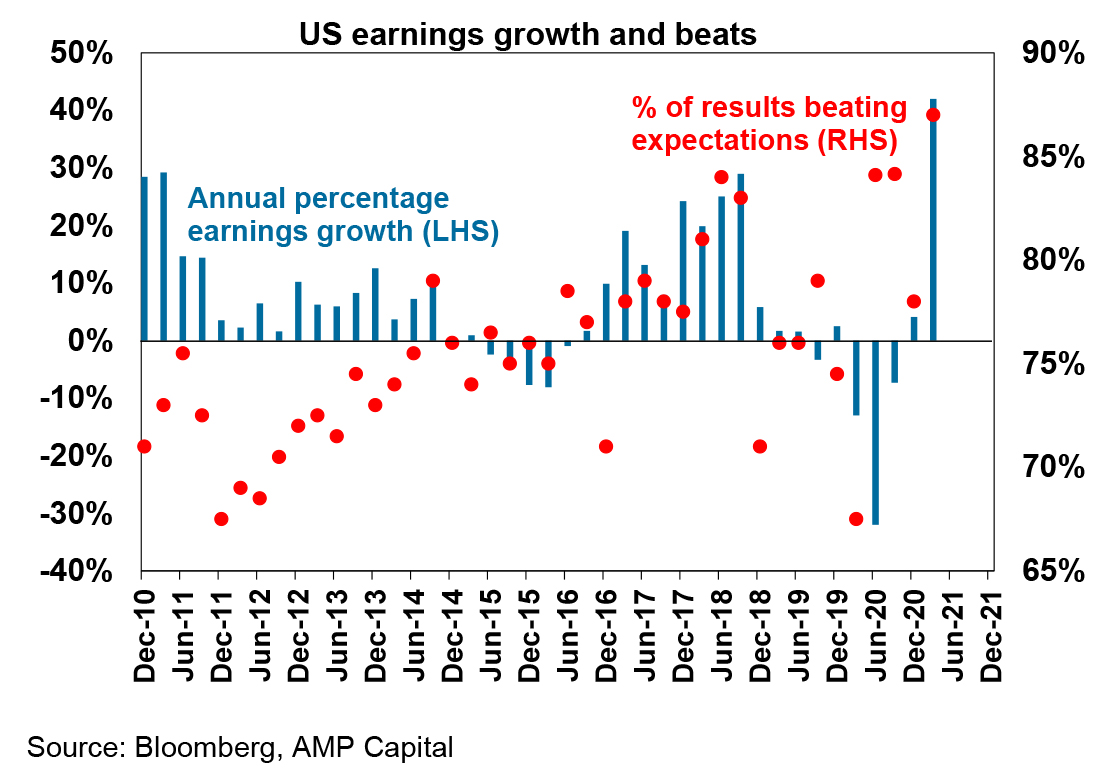

Finally, consistent with this, profits are continuing to surprise on the upside. This is most evident in the US where consensus expectations for March quarter earnings per share growth have jumped from 21%yoy at the start of the current earnings reporting season to +42%yoy now.

Given all this, our assessment remains that share markets will head even higher this year as recovery continues and this boosts earnings. However, investor sentiment is very bullish which is negative from a contrarian perspective and we are coming into a seasonally softer period of the year for shares as the old saying “sell in May and go away…” reminds us. A resumption of the bond tantrum, US tax hike concerns if Congress does not pare back some of Biden’s tax hikes, coronavirus setbacks and geopolitical risks (around US/China tensions, Russia and Iran) could all provide a trigger for a correction. It would likely be just another correction though. Our ASX 200 forecast for year-end remains 7200.

In Australia, going by a speech by Treasurer Josh Frydenberg in the past week, the Budget on May 11 is likely to see a continuing focus on supporting recovery – prioritising job creation to push unemployment below 5% – to help drive the budget deficit lower rather than adopting fiscal austerity. Key elements are likely to include:

- an upgrade to growth forecasts;

- an extra $2.5bn a year in aged care spending;

- measures to help boost women’s economic security including changes to help women bolster their superannuation balances;

- possibly increased childcare rebates (although this could be delayed until closer to the next election);

- more targeted industry support measures;

- extra spending on mental health, disability services, climate, infrastructure and skills;

- some possible tax reforms and deregulation;

- a possible lifting of the home price caps for the First Home Loan Deposit Scheme;

- an extension of the Low and Middle Income Tax Offset (LMITO) to cover the next financial year; and

- much lower budget deficits of $150bn this financial year and $50bn next financial year. The faster than expected economic recovery which means lower than expected welfare spending and increased revenue along with the higher iron ore price (which has the potential to slice $20bn alone of this year’s deficit) means that the starting point for the budget deficit this year could be as low as $125bn (down from $214bn projected in the October Budget last year and $198bn in MYEFO) and $40bn next financial year (down from $112bn in the last Budget). However, we are assuming more conservative Government forecasts, extra spending, and a desire to leave some scope for surprise in the bag will see deficits of $150bn and $50bn reported on Budget night. The key though is that it’s possible that a return to surplus could be on the cards in five years or so (assuming no new shocks along the way).

As to where the non-accelerating inflation rate of unemployment (the so-called NAIRU) sits in Australia – new Treasury research suggests its around 4.5% to 5%, the RBA prior to the pandemic suggested it was around 4.5% and Governor Lowe has agreed it could be below 4%. So it’s a bit of a guessing game – which is complicated further by a still high pool of underemployed. To get wages growth above the 3.5% necessary to sustain inflation around 2-3% will probably require labour underutilisation of around 10% or less which given that its currently at 13.5% means we still have a long way to go.

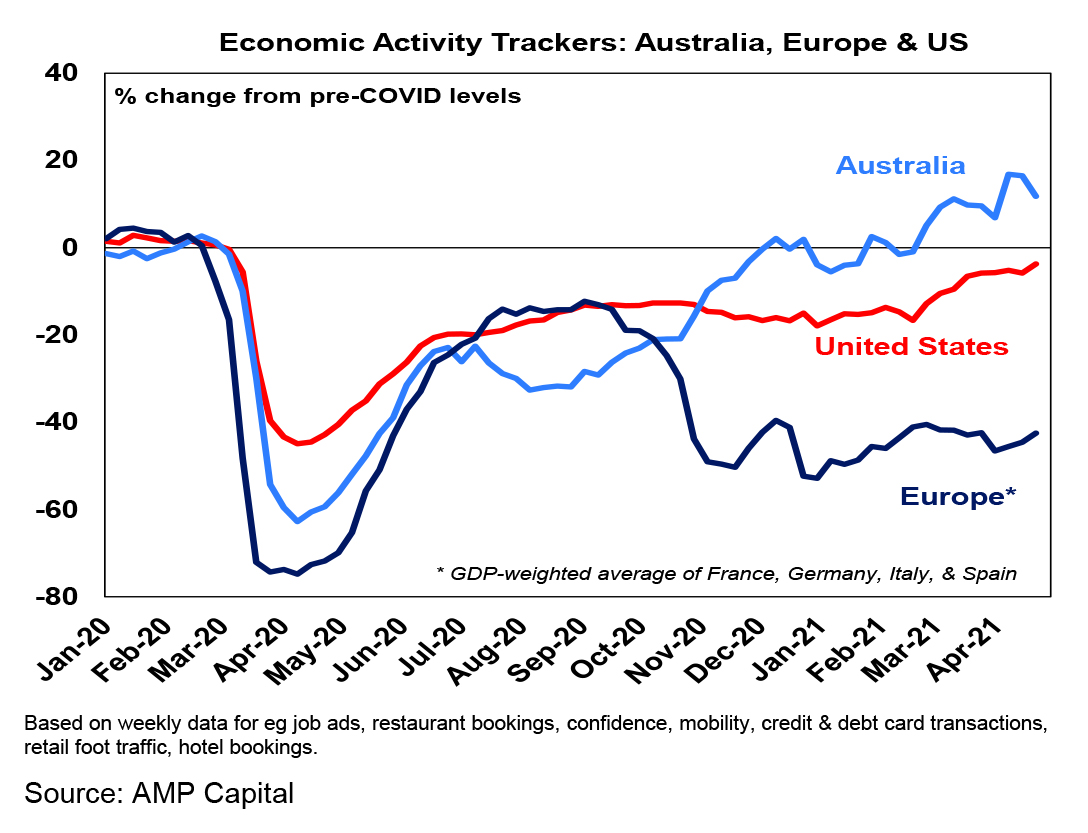

Our Australian Economic Activity Tracker fell over the last week but remains very strong suggesting that economic recovery remains on track. Our US Economic Activity Tracker resumed its recovery but still remains down on pre coronavirus levels and our European tracker rose but remains very weak not helped by lockdowns.

Back in the 1960s/early 70s Detroit didn’t just make great cars (over a few years at one stage I had four of them) but it also made great music, particularly that from Motown. Amongst the best at Motown were The Supremes with a string of hits including Baby Love, Stop in the Name of Love and Love Child with Diana Ross on lead vocals. Unfortunately, their songs after Diana left in 1970 are not as well known but are equally as good. I first came across them when listening to Bananarama in the 1980s when they pointed out that Nathan Jones was a cover of a Supremes song from the post Diana Ross period. The Supremes’ Nathan Jones was unusual for them in that it saw all three (Mary Wilson who by then was the only original member along with Jean Terrell and Cindy Birdsong sing lead in unison). Other excellent songs from this period included Stoned Love and Up The Ladder To The Roof . Unfortunately, Mary Wilson passed away early this year, leaving only Diana of the original Supremes – Florence Ballard left the group in 1967 and died in 1976.

Major global economic events and implications

US data remains very strong. March quarter GDP rose 6.4% annualised, but with trade and inventories detracting -2.5 percentage points from growth gross national spending rose 9.9%. US GDP is now just 0.9% below its pre coronavirus high and growth is likely to remain strong this quarter as stimulus checks are partly spent and vaccine rollout facilitates further reopening. Consistent with this consumer confidence rose strongly in April, home prices are rising strongly, pending home sales rose in April and core capital goods orders are at historically high levels.

Meanwhile, the US March quarter earnings reporting season remains very strong. Roughly 60% of the S&P 500 has now reported with 87% beating earnings expectations by an average +24% and 72% beating on revenue. Consensus earnings expectations for the quarter have now risen to +42% year on year, from +21% two weeks ago. That’s a 21% upgrade in less than three weeks. Tech sector EPS is up 42%yoy, but the cyclicals (like consumer discretionary, financials and materials) are outperforming.

Eurozone economic confidence rose sharply in April to an historically very strong reading with gains in both business and consumer confidence suggesting optimism regarding vaccines and reopening and a strong recovery ahead.

The Bank of Japan left monetary policy on hold as expected, but it lowered its near-term inflation outlook slightly and only sees core inflation reaching 1% in fiscal 2023…still well below the 2% target. Monetary tightening remains years away. Meanwhile Japanese data was stronger than expected with unemployment falling to 2.6%, the ratio of job vacancies to applicants rising slightly and industrial production up more than expected but Tokyo inflation data for April was weaker than expected with core inflation falling back to zero.

Chinese official business conditions PMIs were weaker than expected in April, but the composite remains solid at 53.8 and up from its February low. By contrast the Caixin manufacturing PMI rose more than expected. It all suggests overall conditions remain strong in China.

Australian economic events and implications

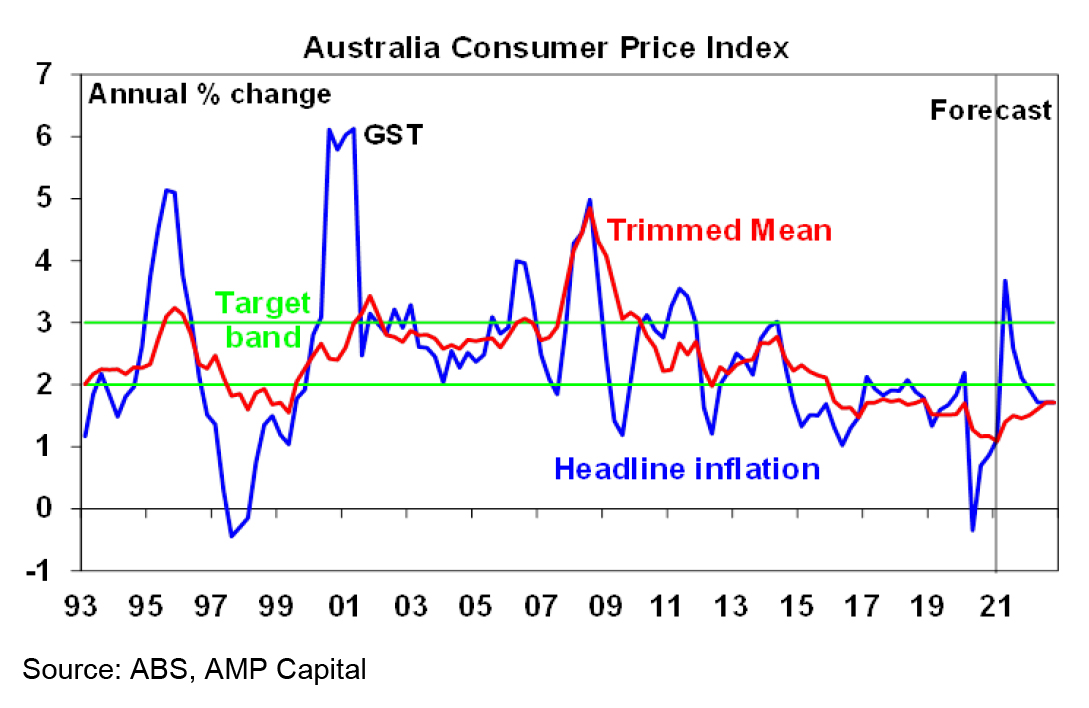

Low inflation to help keep RBA dovish. While there is much concern about rising inflation, Australian March quarter CPI data surprised on the downside coming in 0.3% below market expectations at 0.6% quarter on quarter or 1.1% year on year. At a headline level the downside surprise reflected the impact of housing subsidies offsetting higher dwelling building costs, the Government’s Job-ready subsidy and lower than expected food prices that will likely not be sustained. However, the underlying measures of inflation screen out extreme moves and they were also weaker than expected telling us that despite a few pockets of strength underlying price pressures remain very weak. Producer price inflation was also on the soft side in the March quarter despite big rises in commodity prices. Headline inflation will spike to around 3.7%yoy this quarter as the 1.9% fall in the June quarter last year drops out. However, with general pricing power remaining soft, consumer spending likely to rotate back towards services taking pressure off good prices and wages growth likely to remain weak, underlying inflation is expected to edge up only gradually resulting in both headline and underlying inflation being below target at the end of next year.

In other data payroll jobs fell into mid April but this appears to reflect seasonal weakness associated with Easter and school holidays rather than anything to do with the ending of the JobKeeper. The goods trade surplus surged again in March helped by another strong rise in exports with March quarter data showing a 9% lift in export prices (mainly iron ore) and flat import prices indicating another strong rise in the terms of trade and boost to national income.

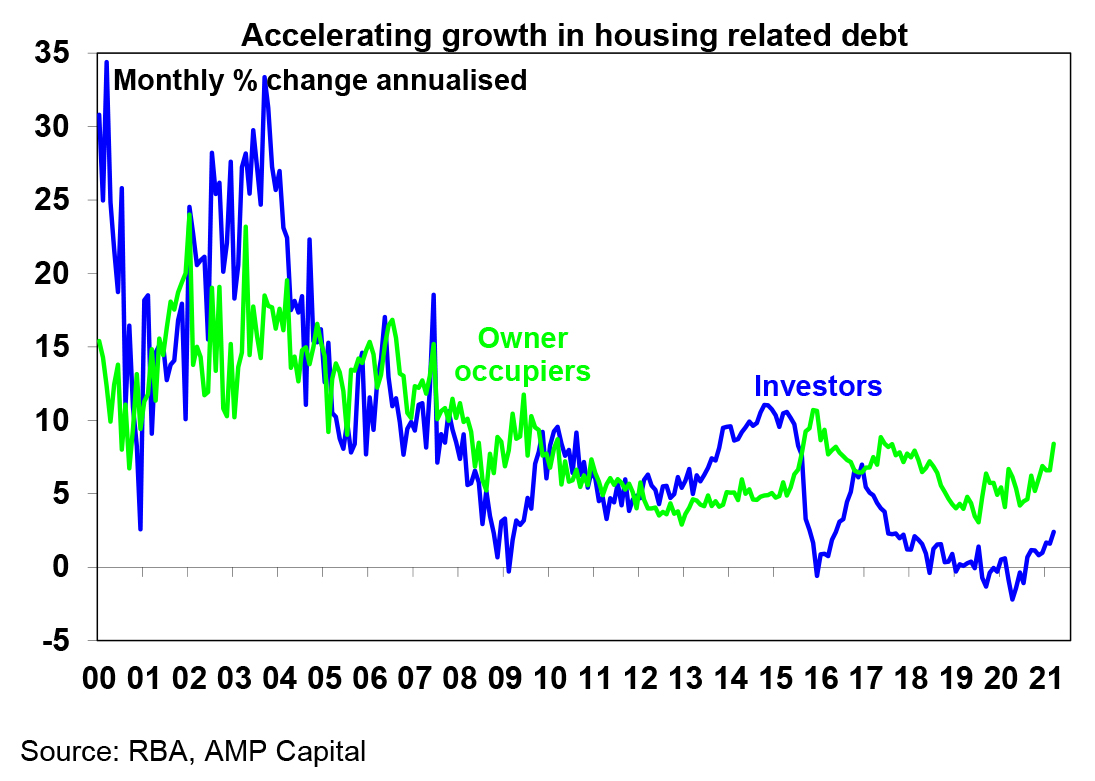

Credit data picked up in March across all categories but particularly for housing which is now accelerating as record housing finance approvals flows through to actual lending. While total housing credit growth of 4.1% over the year to March is modest, the annualised pace has picked sharply to 8.4% for owner occupiers which is at its fastest since 2017. Investor lending is also accelerating. A further rise in credit growth is likely as the housing boom continues and this will likely put further pressure on the RBA and APRA to cool things down.

What to watch over the next week?

In the US, expect the manufacturing and services conditions ISMs for April (to be released on Monday and Thursday) to remain very strong at around 65 and 64 respectively and jobs data (Friday) to show a 950,000 gain in payrolls with unemployment falling to 5.8%. The US March quarter earnings reporting season will also continue.

Chinese Caixin PMIs (Friday) are likely to see the composite PMI remain solid. Trade data will also be released Friday and is likely to show faster imports and slower exports.

In Australia, the RBA (Tuesday) is expected to leave monetary policy on hold following its meeting on Tuesday and reiterate that while the recovery is stronger than expected it still sees wages and inflation remaining subdued for many years with the weaker than expected March quarter inflation data being consistent with this. As such its likely to repeat that it does not expect to raise interest rates until 2024 at the earliest. The focus is likely to be on what it says about its bond buying programs, where we expect a tapering later this year. Its Statement on Monetary Policy (Friday) is likely to see a slight upwards revision to near term growth and headline inflation forecasts and a downwards revision to its unemployment forecasts.

On the data front in Australia, expect CoreLogic data for April (Monday) to show a slowing in monthly home price growth from March’s breakneck pace of 2.8% to a still very strong 1.8%, the March trade surplus to increase to $8.5bn helped by surging iron ore exports, housing finance to rise further (both Tuesday) and building approvals to show a further 5% rise.

Outlook for investment markets

Shares remain at risk of further volatility with possible triggers being a resumption of rising bond yields, coronavirus related setbacks, US tax hikes and geopolitical risks. But looking through the inevitable short-term noise, the combination of improving global growth helped by more stimulus, vaccines and still low interest rates augurs well for growth shares over the next 12 months.

Australian shares are likely to be relative outperformers helped by: better virus control enabling a stronger recovery in the near term; stronger stimulus; sectors like resources, industrials and financials benefitting from the rebound in growth; and as investors continue to drive a search for yield benefitting the share market as dividends are increased resulting in a 5% grossed up dividend yield. Expect the ASX 200 to end 2021 at a record high of around 7200 although the risk may be on the upside.

Still ultra-low yields and a capital loss from rising bond yields are likely to result in negative returns from bonds over the next 12 months.

Unlisted commercial property and infrastructure are ultimately likely to benefit from a resumption of the search for yield but the hit to space demand and hence rents from the virus will continue to weigh on near term returns.

Australian home prices are likely to rise another 15% or so over the next 18 months being boosted by record low mortgage rates, economic recovery and FOMO, but expect a slowing in the pace of gains as government home buyer incentives are cut back, fixed mortgage rates rise, macro prudential tightening kicks in and immigration remains down relative to normal.

Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%.

Although the $A is vulnerable to bouts of uncertainty and RBA bond buying will keep it lower than otherwise, a rising trend is likely to remain over the next 12 months helped by rising commodity prices and a cyclical decline in the US dollar, probably taking the $A up to around $US0.85 by year end.

By Shane Oliver