Advice practice sustainability – a risk management perspective

To survive and thrive in a disrupted marketplace, smaller advice practices need to embed a sustainability focus into their planning and ongoing operations.

Financial advice in Australia is facing a sustainability challenge.

Caught between the pincers of rising costs – including a 160% increase in the ASIC levy over 3 years[1] – and falling revenues (Adviser Ratings estimates a 58% decrease in average adviser income after the removal of grandfathered commissions[2]), the financial viability of advice is being challenged like never before. Indeed, the CEO of one publicly listed advice group has claimed most licensees are either losing money or are marginally profitable at best[3].

Many advisers are voting with their feet, seeing the number of active advisers in decline, and on track to be 50% lower than pre-Hayne levels[4].

Against this backdrop, however, are fundamental indicators which should be cause for optimism for those who can weather the storm and adapt. The most important of these is the continued growth in the demand for advice.

According to Investment Trends, the number of consumers expecting to see a financial adviser in the next 2 years is over 2.5 million – more than double[5] the number seen in 2015.

Meeting this demand will be the challenge for a reshaped advice profession. The shift away from larger, institutional licensees to smaller boutique firms sees 55% more AFSLs now than in 2015[6]. Many of these smaller firms will lack the resources of larger businesses including access to capital, and experience, knowledge and infrastructure around operational fundamentals such as financial reporting, planning, HR, marketing and risk management.

To survive and thrive in a disrupted marketplace, smaller advice practices need to embed a sustainability focus into their planning and ongoing operations. Viewing sustainability through a risk management lens is one way to do this, and for the benefit of practice principals we have produced a practical checklist of important business risks to be measured, monitored and mitigated.

At a high level, the key strategic and operational areas for practices to assess through a risk management lens include:

- design and documenting of key processes (including compliance)

- financial management

- reputation/brand

- insurance

- succession planning

- target markets

- client retention

- staff retention.

We will explore some of these points in more detail below.

Design and documentation of key processes

Regardless of whether you’re just launching your firm, or you’ve been in business for a while, your processes are at the heart of your business. They underpin your efficiency, determine the client experience and help ensure you remain compliant and protected.

Whilst not seen as particularly exciting, understanding and documenting your processes in detail could literally be one of the most important tasks you can undertake in terms of making your practice more sustainable.

The time you invest in documenting your processes will pay dividends in many ways, including:

- helping you understand the true cost to serve

- identifying any duplicated effort or process gaps

- ensuring a higher quality client experience is delivered more consistently

- quicker upskilling of new staff and cross skilling of existing staff minimises any productivity drop offs due to staff turnover or absences

- being able to outsource processes with more confidence

- processes that are documented – and adhered to – are ‘compliance gold’ (the majority of AFCA advice complaints involve incomplete record keeping)[7].

What processes to document

To help ensure you capture all your repeatable business processes, it can be useful to think in terms of process categories. These may include (but not be limited to):

- Financial planning/advice process

- Discovery and data gathering

- Analysis

- Plan preparation and presentation

- Plan implementation

- Ongoing monitoring and reporting

- Compliance processes, tasks, and procedures

- Documents (SOAs, FDS, FSGs)

- Fee agreements/client engagements

- Record keeping

- Complaint resolution

- Risk assessment

- Compliance training for employees

- Practice management tasks

- Hiring process

- File structure and storage

- Cyber security

- Client onboarding

- Ongoing client engagement

- Business KPI tracking and reporting

- Client billing

- Staff performance reviews

- Marketing processes

- Content creation and promotion

- Social media marketing

- Data analysis

- Website optimisation process

- Sales processes

- Lead management

- Prospect screening

- Follow up/nurturing processes.

How to do it

If the thought of documenting all your processes seems a little daunting, it may be useful to remember the adage about how to eat an elephant (‘one bite at a time’).

Tackling one task at a time can make the project much more manageable, as can starting with a general outline which you then flesh out over time. This is something you can often do while you are actually completing the steps within a process.

For example, while onboarding a new client, try documenting the steps you are taking while thinking about the timing of each step, the content you’re communicating, whether you’re missing anything, and/or any hurdles in the process.

Writing down all these details may bring to light process improvements you had not previously considered.

If you have multiple team members performing the same tasks, it is important to have them analyse their own version of those same processes. This allows you to compare notes across team members and identify any inconsistencies, as well as any opportunities for efficiencies and improvements. Allowing everyone in your team to design processes also improves staff engagement by giving them more collective ownership of the client experience.

Another handy tip is to use some sort of template for capturing and analysing your processes. There are many freely available examples online[8]. Using standardised templates will ensure consistency in the way you document different processes and can also be helpful when you have different staff analysing the same processes.

Financial management – understand your numbers

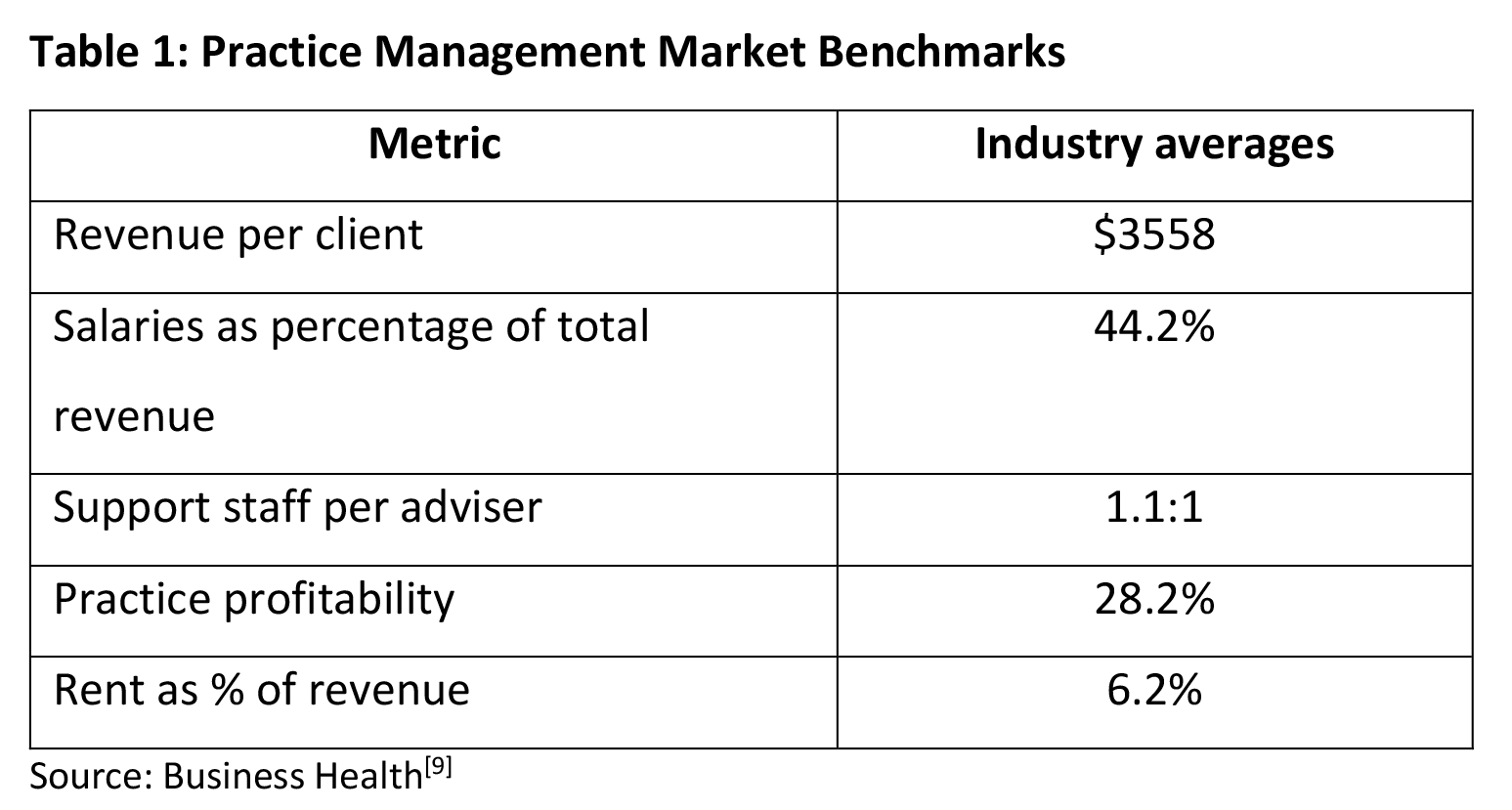

Looking at advice practice finances through a risk management lens necessitates a forensic understanding of the drivers of costs and revenues within the business. Such an analysis incorporates everything from remuneration models to staffing levels, from technology costs to rent. In many cases, truly understanding your numbers can be easier said than done. Not fully understanding processes, for example, can make it hard to calculate the real cost to serve. Lack of detailed data on key financial metrics can also be problematic, as can a lack of relevant benchmarking.

The Business Health series ‘Practice Management by the numbers’ is a useful starting point to understand how your peers/competitors may be doing things:

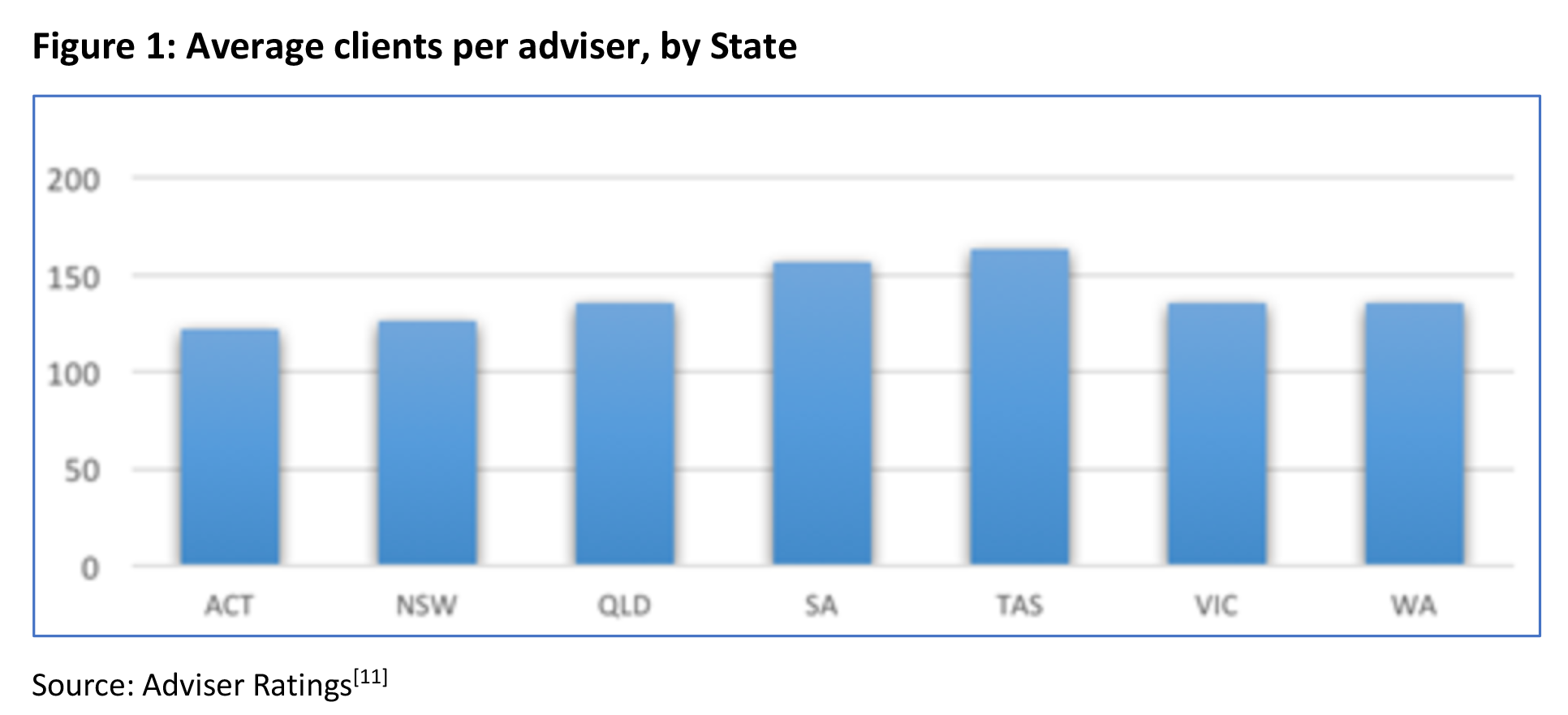

Another important metric is the number of clients per adviser.

Whilst an average of 100 clients per adviser was, for many years, seen as typical, Adviser Ratings found that this has trended up to well over 100. Their 2018 research[10] showed ACT advisers tended to average 122 clients each, whilst Tasmanian advisers serviced 164 clients each on average. The recent exodus of advisers from the market is likely to have driven these averages up further, putting service quality at risk.

Of course, these averages are just that – averages across the industry. They are not necessarily targets for individual practices to aspire to, as every business is different. What practice owners should aspire to, however, is actually knowing what these metrics are for their business, why they may be higher or lower than industry averages, and whether these differences support or undermine the sustainability of their practice. Only then can they take the appropriate steps.

Other financial management issues for practices to consider in the short to medium term include how they may be impacted by any potential changes to life insurance commissions that may result from the LIF review (now combined with the 2022 Quality of Advice Review), and whether there are any efficiency savings to be made through outsourcing, automation, or process changes.

Reputation/brand

Often regarded as the domain of only large businesses, your personal brand – and that of your practice – is vitally important when it comes to consumers choosing an adviser. This is because the crucial ingredient of trust is either reinforced, or undermined, by your reputation.

There are a number of ways to consider brand through a risk management lens. The first is to consider whether your brand (and branding) is appealing to your target customer. Does it stand out from the competition, does it convey the right signals about your services, your expertise, and your ideal clients?

Whether your target clients be high net worth professionals or blue-collar workers, retirees or millennials, your brand experience (including your processes, your website, your office location and your attire) needs to be consistent with their expectations.

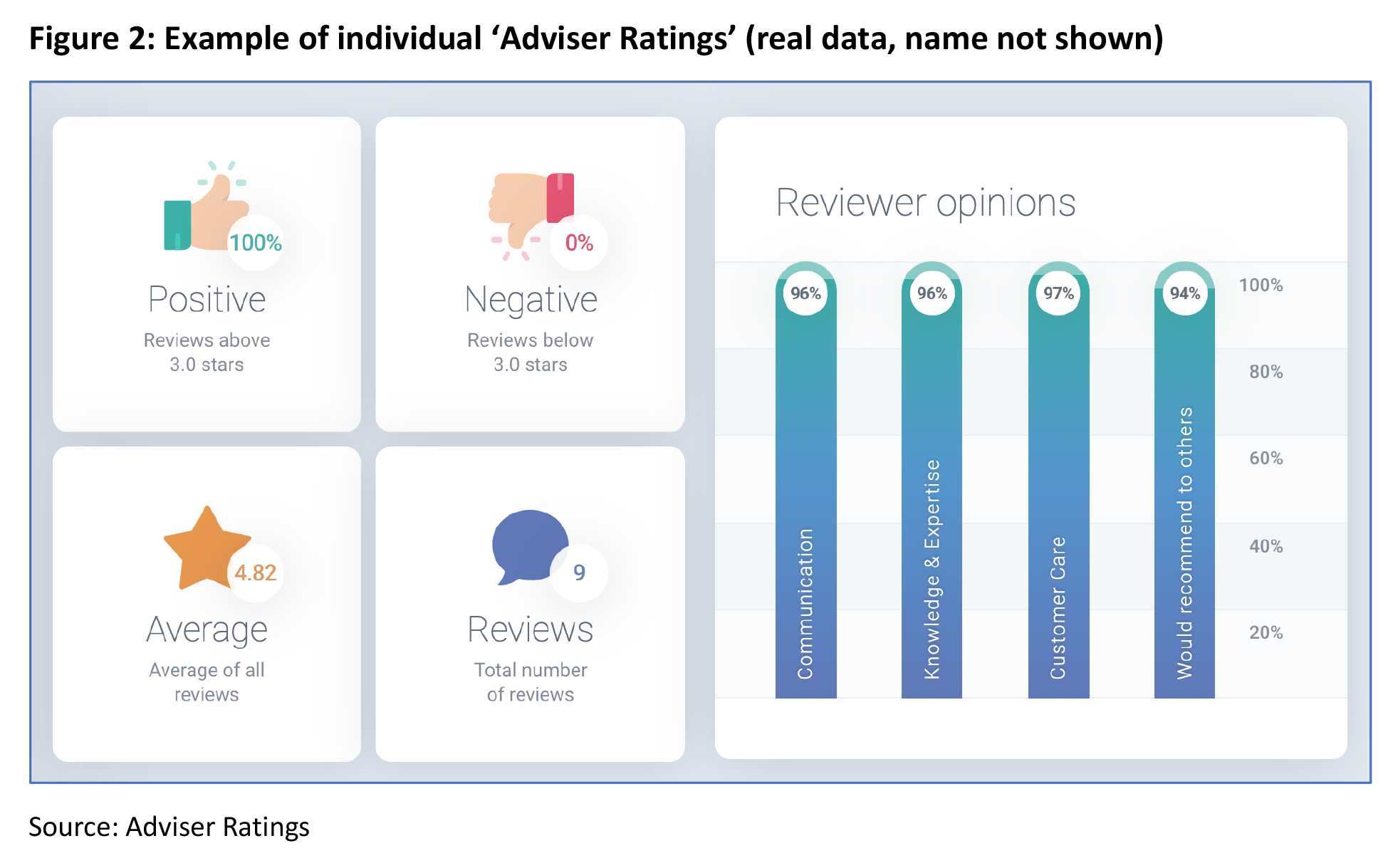

The second way to view brand through a risk management perspective lens is to consider the health of your reputation, and how to protect it. This is particularly important in a world where social media and online reviews increasingly form part of a consumer’s pre-purchase research.

In addition to social media comments and Google Reviews, the Adviser Ratings platform[12] will increase in importance as more customer ratings are uploaded. Advisers should not only take the time to monitor such reviews, they should also look to address any specific concerns contained within, and ensure that any negative reviews are not driven by systemic issues.

And of course, they should encourage satisfied customers to upload their own positive reviews!

Insurance

Advice practices will generally have a number of insurances in place, including the mandatory Professional Indemnity (PI) cover, commercial covers on premises and other business assets, and individual level personal life coverages such as income protection and trauma.

PI and cyber-risk coverage are both highly topical at the moment, for very different reasons.

Professional Indemnity cover is legally required at the AFSL level, as a means of ensuring clients can be compensated in the event of breaches of the Corporations Act.

The Hayne Royal Commission gave rise to a dramatic increase in the number of claims against such policies, which in turn saw a dramatic reduction in capacity as several insurers left the market. The small number of remaining insurers (4 at last count) have implemented significant price increases (15- 20% or more) and have also become more selective in the risks they take on[10]. According to insurance brokers PNO[13], the typical rate for PI cover ranges from 1.8 – 2.3% of practice fee income (with the nature of investments, limit size and excesses directly impacting these rates).

Factors that influence the attractiveness of AFSLs to PI insurers include:

- split of business

- compliance processes

- complaints and claims history

- quality of staff

- products and services offered.

To the extent that practices can seek to reduce PI premiums by reducing their risk profile, a review of products and services offered may identify opportunities to lower premiums by being more restrictive in your offering. However, the implications of this to the business strategy can be significant. Is ceasing to offer MDAs worth the insurance saving? (Some PI policies have a blanket exclusion on MDA related claims, making the point moot anyway.)

The hardening up in the PI market post Royal Commission has been reflected in the availability of ‘run off cover’, which provides indemnity for a number of years after a practice has been sold (recognising the long tail nature of PI claims). Previously available for 6 years, it is now difficult to get run off cover for greater than 3 years[14].

What has also catapulted PI back into the news recently has been the increased ‘chatter’ around cryptocurrencies, and their legitimacy as an investment vehicle.

Regardless of what side of the fence an adviser sits on in this debate, at this stage it seems a bridge too far for PI insurers, severely limiting the number of advisers who would be prepared and able to advise clients in this area.

Cyber-risk coverage has become more topical as the incidence of cyber-attacks against AFSLs – and awareness of them – increases dramatically.

The annual cost of cybercrime in Australia has been estimated at $29 billion[15]. And – as demonstrated in the case study below – the advice sector is particularly vulnerable by virtue of the sensitive financial and personal data held by clients.

It is no exaggeration to say that data loss can ruin lives. Consumers understand this and hold companies responsible for data security. And they are likely to abandon a business entirely, and take legal action, if they suffer a data breach – regardless of whether it leads to any personal loss – according to a study by Global cybersecurity firm Gemalto[16].

Case study: ASIC takes AFSL holder to court over poor cyber security

In August 2020, ASIC took a well-known financial advice group to court, for their alleged failure to have adequate cybersecurity systems in place for its almost 300 financial planners, thereby breaching provisions of the Corporations Act. The Australian Financial Review[17] reported ASIC as seeking a court-imposed penalty against the group and compliance orders that it implement better systems.

The incidents prompting the ASIC action – and a potential penalty of up to $12 million – included a ransomware attack in late December 2016 against one of the group’s member practices, which hacked an office computer, encrypting files and making them inaccessible. A number of other practices within the group also suffered cyber-attacks between 2016 and 2018.

As well as being offered on a standalone basis, some insurers offer cyber-risk protection as an extension cover through Professional Indemnity insurance policies.

Succession planning

Succession planning – designed to ensure a business outlives the working lives of its original founders – is perhaps the ultimate sustainability strategy. Yet whilst many advisers who work with SME clients routinely advise on business succession strategies, far fewer ‘practice what they preach’, according to recent research.

The ‘Future Ready VIII – HealthCheck Analysis’ released by Business Health[18] in January 2020, reported that only 10% of advice businesses have a proper succession agreement in place (where ‘proper’ means an agreement with an identified successor, supported by a regularly reviewed and documented plan, and covering all major trigger events).

Furthermore, the remaining 90%:

“Have inadequate arrangements in place to address the untimely death or serious illness of an equity partner. And, if it is not a forced exit and the current owner is able to retire on their own terms and timeframes, for most it remains unclear who will buy the business and why they would or should pay a premium for it.” (Rod Bertino, Business Health[18])

Regardless of whether the succession scenario involves internal succession, a merger with another practice or the outright sale of the business, one of the most common mistakes made by practice owners is leaving the process too late. This is partly because they tend to underestimate the time it takes for prospective buyers to perform due diligence on the business. (In this regard, the risk management strategies discussed above, including having highly detailed data on every aspect of the business, and having comprehensively documented processes, can actually help by making such due diligence easier and quicker.)

Another important aspect to be considered in business succession is client retention, and in this regard, a more orderly, smoother and more gradual (i.e. longer) succession process is more effective in minimising disruption and client exits.

Target client segments

In an earlier article we examined the importance of choosing the client segments the advice practice would serve. To the extent that sustainability of a practice will be maximised if there is alignment between the capabilities of the practice and the client segments it serves, then choosing these segments becomes a key strategic decision.

Such a decision is a complex one, involving the analysis of many factors including:

- the skill sets and interests of advisers in the practice

- geography

- size, growth and profitability of different segments

- competition for those segments.

Regular reviews of practice KPIs should always be done in the context of target market suitability.

Client retention

Client retention is regarded by many as the cornerstone of a successful, sustainable advice practice. And with good reason(s). The Harvard Business Review[19] tells us the cost of acquiring new customers is at least 5 times more expensive than keeping existing ones.

In the context of Australian financial advice businesses, research[20] suggests client retention rates for average to well-performing practices tend to sit in the range of 94 – 98 per cent, meaning the average client lifecycle is anything from 16 to 50 years.

Applying a 20-year lifecycle to the industry average revenue per client of $3558 (as per Table 1) we arrive at a Lifetime Customer Value of $71,160. A practice with 150 clients would theoretically therefore have a total lifetime customer value in the vicinity of $10 million.

Improving the retention rate by just 1% – to 96% – means the average client is staying on the books for 5 more years, seeing $10 million in customer lifetime value rise to over $13 million.

Client retention and client engagement activities should therefore be seen as an investment in the sustainability of a practice, and client attrition a risk to be managed.

Staff retention

In our earlier article on staff engagement, we examined the link between staff engagement and retention, and explored the financial, productivity and customer experience impacts of staff attrition.

According to the employer body Australian Industry Group[21], the cost of replacing an individual employee can be up to 150% of their annual salary. The direct and indirect costs can include:

- recruitment and advertising costs

- lost productivity of business covering for that vacancy

- lost productivity of managers involved in recruiting process

- impact to morale of remaining staff if they have to pick up extra workload

- potential loss of clients served by that employee

- poor client experience due to incomplete ‘handover’ of files

- lost productivity of personnel required to training new team member

- lower productivity amongst new starters while they ‘come up to speed’.

Your people truly are your biggest asset, and as such are critical to the sustainability of your business.

———