Andrew Zbik

When most people think about personal insurance, they think it is important to insure the main income earner of the household.

Just because a spouse may not be earning an income does not mean that they don’t need to be insured.

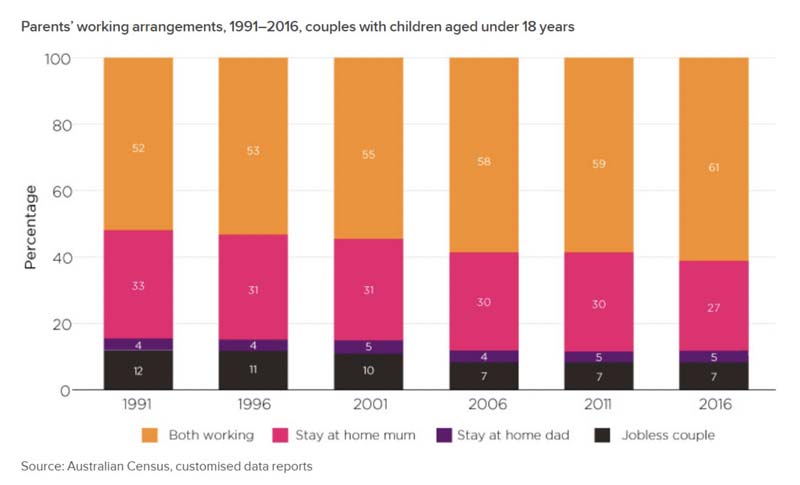

Based on research by the Australian Institute of Family Studies (AIFS), 39% of families have at least one parent ‘stay-at-home’ to look after children under the age of 18.

The AIFS found that fathers work, on average, 75 hours a week. Of that, 46 hours is on paid work, 16 hours is on housework and 13 hours is on childcare.

Mothers work an average of 77 hours a week: 20 hours is paid work, 30 hours is household work and 27 hours is childcare.

As more mothers stay at home, let’s look at the cost of replacing the ‘in-kind’ (i.e. ‘free’ or ‘unpaid’) hours contributed to running a family home if Mum is injured or ill and cannot perform their contribution.

Cost of childcare

If we assume $150 a day for childcare, 5 days of care a week amounts to $750. Over 50 weeks a year this bill is approximately $37,500 per child before any childcare subsidies which are means tested on household income.

Cost of household tasks

Hiring a cleaner once a week for 2-3 hours for some basic cleaning can cost in the vicinity of $150. Over 52 weeks that is approximately $7,800.

However, there are a many other tasks around the home that need to be completed. Airtasker is a good guide as to what hourly rate Australian households are paying for housekeeping services. The median price per house across all the various services is $100. Putting a price on the 30 hours of unpaid housework you can see would cost more than simply hiring a cleaner for 2-3 hours per week.

Cost of medical care

If a spouse cannot contribute to home care for the family, they will likely be incurring medical bills for their own care.

The nature of any condition if it is short-term or long-term will impact what costs are incurred.

The Zurich ‘Cost of Care’ health research whitepaper highlighted what costs may be incurred when an individual needs medical care. Some of the standout items are:

Patients using drugs not supported by the PBS can face bills of up to $5,000 per month or more

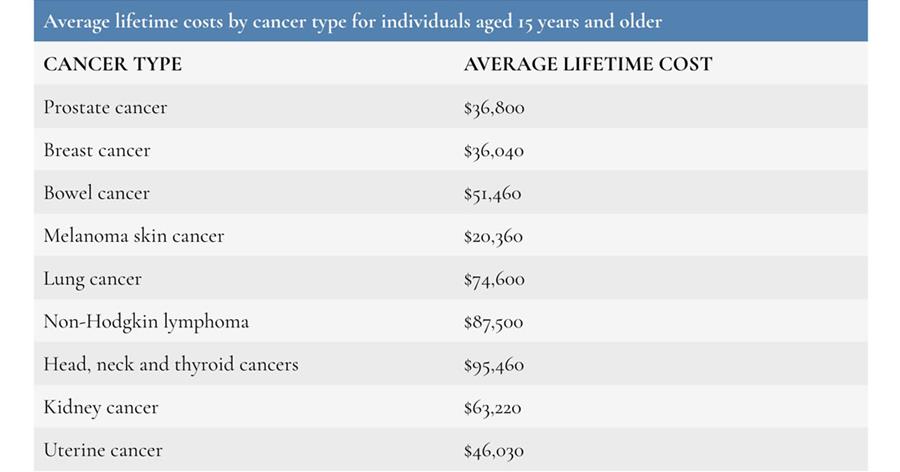

Although healthcare in Australia is largely publicly funded, out-of-pocket (OOP) costs associated with cancer diagnosis, treatment and survival can place a huge burden on sufferers and their families. For example,

* The cost of depression averages $17,190 per individual

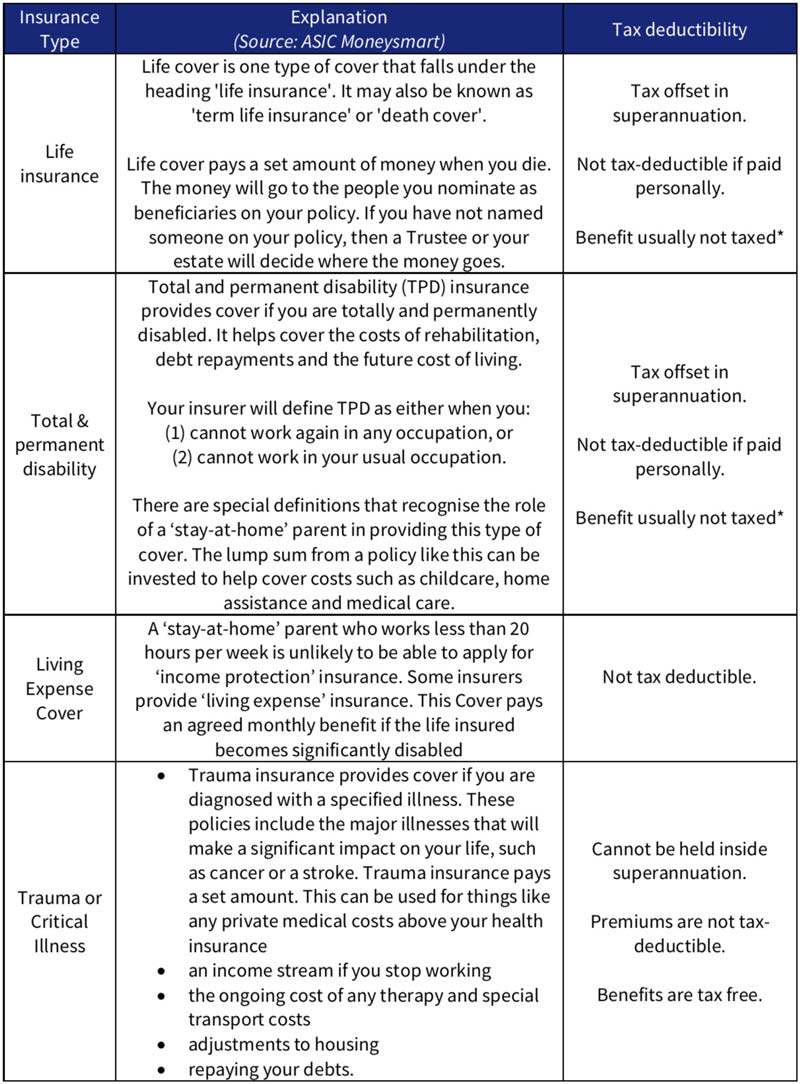

Protection for a ‘stay-at-home spouse’

Personal insurance policies are a strategy that can be used to help cover the financial burden if a ‘stay-at-home’ parent is injured or ill and can no longer make a contribution to the household.

Below is a summary of how these policies operate:

* Depending on superannuation beneficiary, some tax may be payable. You will need to seek advice from a Financial Adviser for individual circumstances.

Get the right advice

Each family’s household needs will vary. Therefore, the amount of cover a ‘stay-at-home’ parent may need will also vary. It is important to understand what are your household expenses and the time contributed by a ‘stay-at-home’ parent to calculate what is the appropriate amount of insurance protection required. A fee-for-service financial adviser can assist with providing advice that suits your needs and objectives.

By Andrew Zbik, Senior Financial Planner

———