Behaving badly – could our decision-making flaws undermine the consumer protection intent of recent superannuation changes?

The effectiveness of regulatory intervention intended to protect consumers can often be undermined by their vulnerability to irrational decision making and reliance on mental short cuts.

It is widely accepted that consumer financial protection is important not only to protect consumers but also for the stability of the financial system.

Whilst the major knowledge asymmetry that exists between consumers and financial services providers is, in itself, justification for robust protections, there is also a widely held view that consumers need protection from themselves, due to their inability to make rational decisions.

Could our flawed decision-making processes, and resulting behaviours, undermine even the most expertly designed consumer protection interventions, leading to unintended consequences, and negating some, or even all, of their protective powers?

In this article we will examine this hypothesis through the lens of the recent Protecting Your Super (PYS), Putting Members Interests First (PMIF) and Your Super Your Future (YSYF) changes, as well as the history of superannuation changes more broadly.

Poor decisions are now even easier to make

The increasing complexity of financial products and markets, combined with the growth of digital technologies and social media, has made the need for protection even more critical, with it becoming even easier for consumers to buy the wrong products and be influenced by the wrong voices (think unlicensed and untrained ‘finfluencers’!).

As discussed in an earlier article in this series, the 4 main pillars of financial consumer protection are financial literacy, disclosure, advice, and product regulation. Historically, Australian regulators have intervened regularly in the areas of disclosure and advice, to a point which has unquestionably added to the complexity and cost of financial advice and has – counterproductively – increased the knowledge asymmetry between consumer and provider.

In more recent times, regulators have looked ‘upstream’ and have started to introduce measures which influence the design and construction of products. Australia’s Design and Distribution Obligations (DDO) regime – based on similar interventions in overseas markets – and the PYS/PMIF/YSYF changes to superannuation are two recent and significant examples.

Putting aside any ideological drivers behind these changes, they are undoubtedly predicated on sound intent (protecting consumers’ interests), expert input and extensive stakeholder consultation.

Despite this, there are fears that this intent could founder on the rocks of behavioural economics, dashed by our vulnerability to psychological mirages and flawed decision making. Overlaid on structural aspects of our workforce and financial markets, some experts predict the outcomes of some of these changes could actually be the opposite of those intended.

To understand such a perspective, it is first important to refresh our understanding of the principles of behavioural economics, and how they influence the way we process information and make decisions in all aspects of our lives.

Behavioural economics and financial decision making

In contrast to classical models of economics which assume consumers to be rational financial decision makers (and why increased disclosure was incorrectly assumed to improve decision making), behavioural economics (BE) uses insights from the more empirical psychology and sociology to create a much more realistic picture of myriad of factors that also affect our behaviour in economic matters.

Behavioural economists draw on the long list of “heuristics” – mental shortcuts or biases in the way we think – developed by cognitive psychologists. The interaction between many of these has been shown to undermine our financial decision making, especially in relation to events which are intangible and in the future. Hence decisions around insurance and retirement savings can be particularly fraught.

As humans we tend to be myopic – short sighted. In BE terms, this is known as ‘present-bias’ – our tendency to overvalue the present relative to the future.

One of the most significant pieces of public policy since Federation – the introduction of compulsory superannuation 1992 – can be seen as an intervention designed to correct present bias. In other words, if we left it to individuals to save for their retirement, most wouldn’t until it was too late, with dramatic economic consequences.

Then there’s “confirmation bias” – our tendency to remember events that confirm our existing views but forget developments that cast doubt on our beliefs. In other words, we tend to ‘cherry pick’ information.

Confirmation bias explains why two people with opposing views on a topic can see the same evidence and come away feeling validated by it. Whilst this cognitive bias is most pronounced in the case of ingrained, ideological, or emotionally charged views, it can also affect our decisions (or non-decisions) around topics with which we are less engaged, such as our superannuation.

Another bias driving sub-optimal decisions is ‘cognitive overload’. This occurs when people find it too hard to process large volumes of complex information that accompany financial decisions. In the context of planning for retirement, cognitive overload can lead many of us to stick with choices we have arrived at by default. Or, perhaps more accurately, stick with the place we arrive after making no choices at all.

As Australian economist Dr David Gruen[1] noted:

“Cognitive biases create a big gap between our intentions and our actions: although people intend to save for their retirement, they often don’t translate that into action. For most people, how much to save, and in what form, are difficult cognitive problems – because of both our limited calculation powers and the apparent enormity of the task. When complicated decisions are required, people often stick with the status quo and take no decision at all.”

Behavioural economics and superannuation disengagement

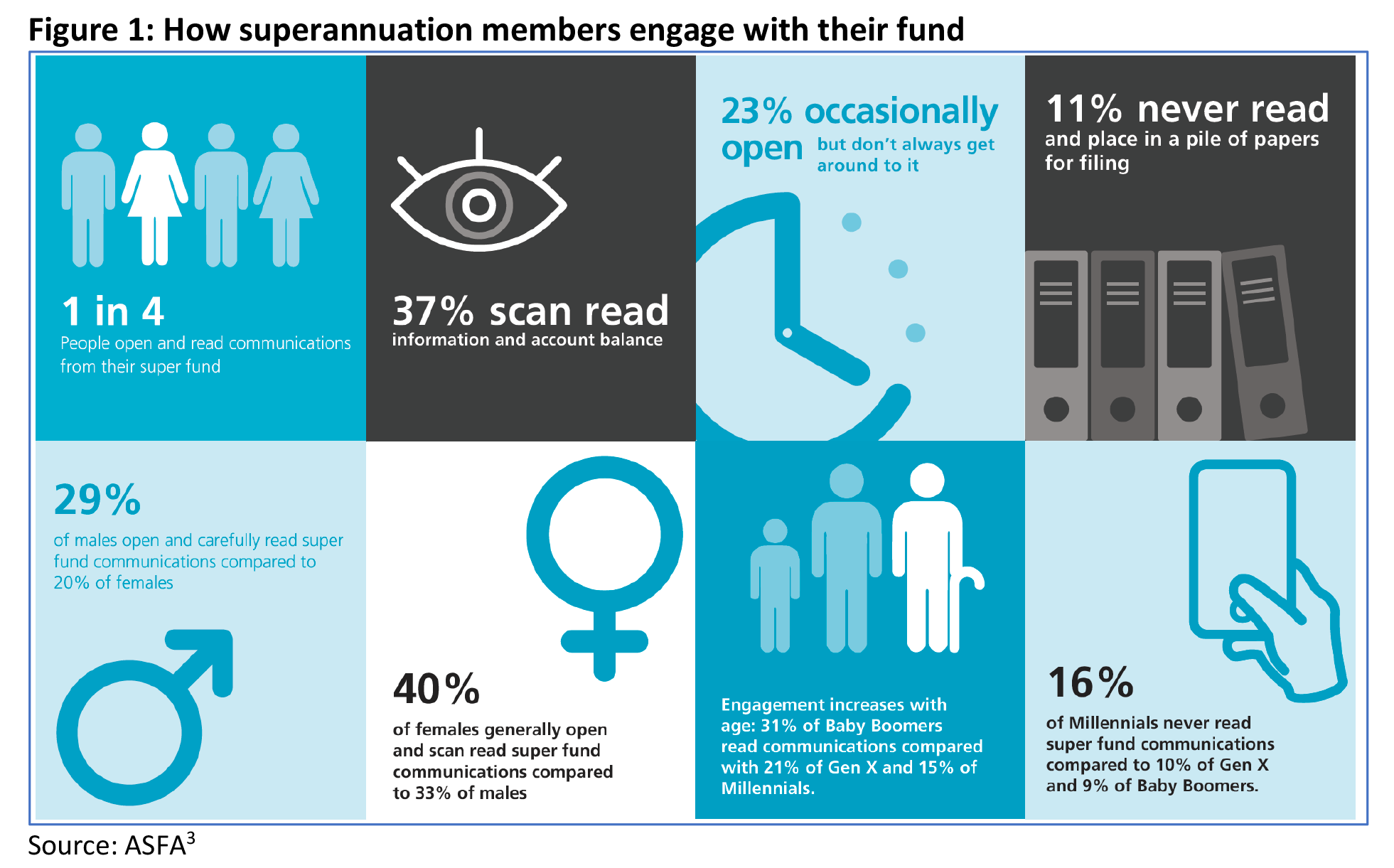

Cognitive overload, and decision inertia, is more likely where we are forced to make decisions about things we aren’t interested in or engaged with, and, as various studies have identified, Australians’ disengagement with superannuation is alarmingly high.

Member Engagement Research conducted by Coredata[2] in 2016 found around three in five (59.6%) Australians aged 29 and under are disengaged with superannuation – with almost a third of them (31.9%) ‘highly disengaged’. Disengagement levels amongst older groups were lower but still concerning, with almost a quarter of those aged 50-59 and 1 in 6 of those aged 60 and over falling into the highly disengaged categories.

(A commonly held view on why engagement with superannuation is so low relates to its ‘hidden’ nature; contributions are taken out pre-tax and thus never seen, funds are locked away for decades, and fund communication is typically infrequent and complex, making it easy to forget and/or ignore).

The importance of the ‘non-decision’

The concept of default choices is a very powerful one, with elevated relevance in the context of superannuation. Several superannuation policy interventions have been predicated on the lack of active decision making that takes place in relation to our superannuation investments, particularly amongst younger Australians.

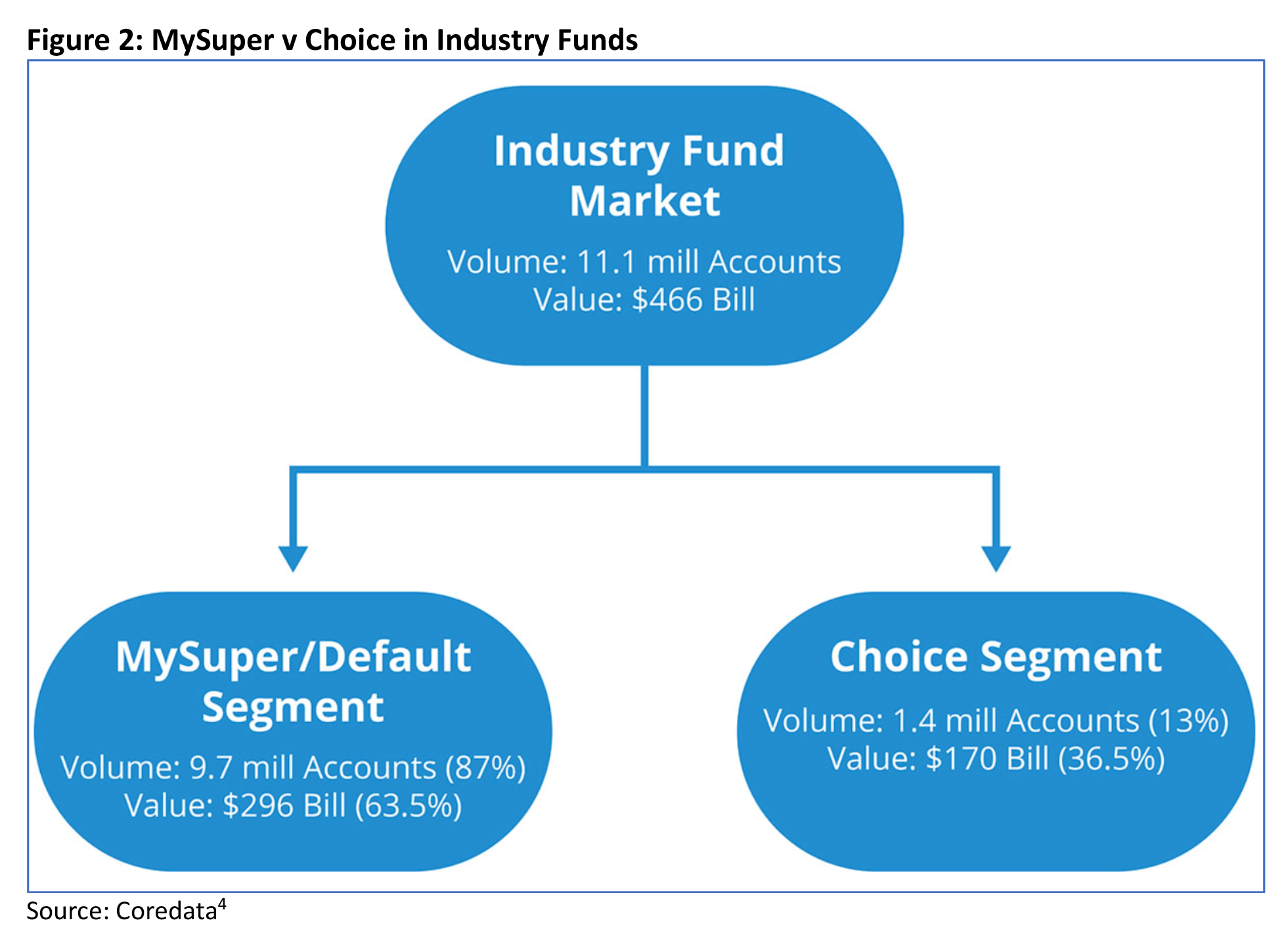

This phenomenon is perhaps best illustrated by data showing the popularity of ‘default’ options in our choices of superannuation funds and the investment options within those funds.

As shown in Figure 2, almost 9 in 10 of industry super member accounts are invested in MySuper (default) products.

And when it comes to choosing an investment option, research[5] by the Association of

Superannuation Funds in Australia, (ASFA), has found that only around 10% of members exercise investment choice within funds offering it. This is quite often a ‘balanced’ option which, in the case of younger members, could see them forfeit growth potential worth tens of thousands of dollars.

PYS, PMIF, and YSYF

It was this powerful decision inertia about superannuation that directly influenced the most recent, substantial, superannuation changes.

More specifically, our lack of active decision making around the number of funds, investment performance, and the life insurance offered through funds, was seen to be costing Australian’s billions of dollars of year in suboptimal performance and duplicated, uncompetitive, and unnecessary fees and charges.

But whilst theoretically sound and noble in objective (reducing the unnecessary erosion of superannuation balances and lowering the future pension burden borne by taxpayers), some experts believe the effectiveness of these changes could be undermined by our imperfect decision making, and the structures within those decisions are made.

Put another way, they fear mechanisms intended to protect consumers could actually end up causing them detriment.

Let’s now look at specific areas of the legislation.

Intended v unintended consequences

The passage of these reforms proved challenging for the Government, with many elements hotly debated and the subject of intense lobbying by a variety of stakeholders. Nevertheless, the government remains resolute in its belief that the changes will save superannuation members more than $17 billion over the next 10 years[6] alone, a worthy outcome should it prove correct. But what other outcomes could we see?

(Allowing for the many vested interests flavouring debate around these changes, we will now extrapolate out the potential consequences based on the behavioural economic principles discussed above. This article does so only to illustrate how such principles can influence the efficacy of consumer protection policies, and does not offer any opinion on the merits of the changes per se.)

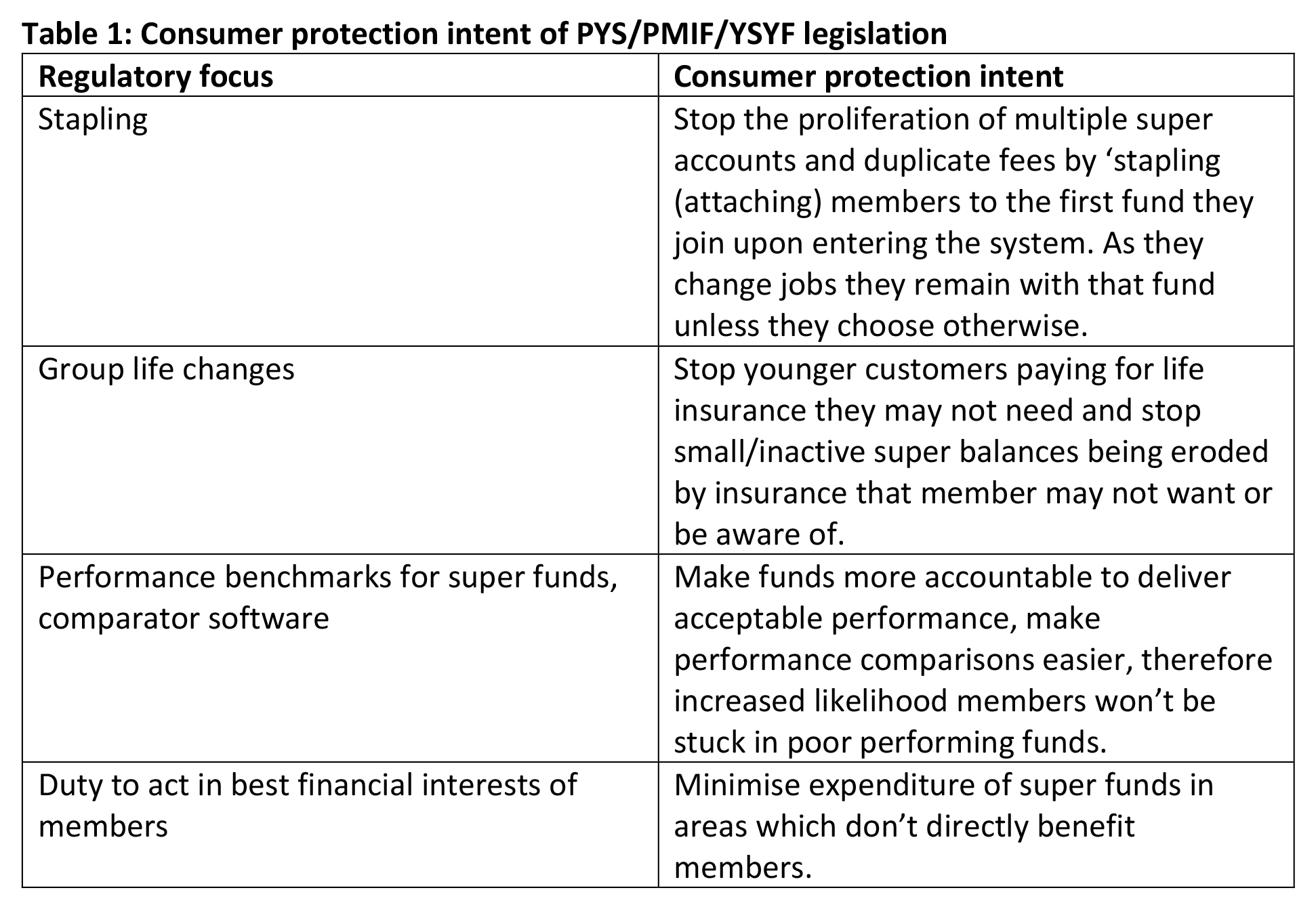

Stapling

The policy of attaching members to the fund they first join when entering the superannuation system is designed to tackle the problem of account proliferation and associated fee duplication. This problem occurred because decision inertia saw many workers defaulted into a new superannuation fund each time they changed jobs (rather than exercising their right to nominate an existing fund).

The Productivity Commission estimates a third of all super accounts are unintended multiple accounts, which are unwanted and unneeded, and that’s costing us $2.6 billion annually in fees[7]. Furthermore, many people lose track of their superannuation, explaining the more than $20 billion in lost super held by the ATO[8].

On the face of it, then, this policy seems a winner.

Not so fast say experts.

AFR analysis of APRA data suggests it is actually a handful of big industry funds like Rest, AustralianSuper and Hostplus which may benefit most from stapling. This is because many Australians’ first jobs, and first contact with the superannuation system, are in the retail and hospitality sector.

Once a member is stapled to a fund, the very inertia and lack of engagement that the reforms are intended to address will likely to see the member remain with that fund for years, regardless of whether it meets their needs once they settle in their longer-term career.

Hence while the funds serving hospitality and retail get the first grab at members, funds serving industries like construction and health may struggle to attract new members at the same rate. Over time this could see such funds facing a scale and cost base challenge which threatens their sustainability. If funds are forced to exit the market, competition will decrease, an outcome generally seen as detrimental to, rather than protective of, consumer interests.

Furthermore, members could inadvertently become stapled to poorly performed funds, and remain there for years, unaware that their retirement savings are suffering as a result. An overlooked upside of multiple accounts is that the risk of poor performance is diversified. With 14% of funds underperforming, according to the Productivity Commission[9], a person who has created three accounts has a less than 0.5% chance that all their money is invested in a poor performer.

Performance benchmarking – the road to mediocrity?

Another example of a policy which seems self-evidently good for consumers is the intent to create performance benchmarks for funds to meet. Funds falling outside the permitted variance from these benchmarks will be forced to advise their members. If they fail this test twice, they may be barred from taking on new members altogether.

What could go wrong, you ask?

Well, according to some observers, quite a lot.

In fact, one high profile Asset Consultant[10], says the new benchmark “will have potentially significant and negative impacts on investment outcomes for members”.

Some of the concern revolves around the likelihood that over time, and out of fear of being ‘named and shamed’, fund trustees will demand index investing rather than more adventurous and more expensive investment choices in private markets, or unlisted investments.

As well as removing the incentive for fund managers to achieve absolute outperformance for members who are happy to take additional risks – and thus ‘dumbing down’ performance across the board – experts believe this could create sequencing risk for members in funds whose investment mandates don’t permit them to diversify away from extreme market corrections, as we saw in the early days in Covid.

Group life changes

The PMIF and PYS legislation, which took effect in 2019, took aim at the practice of defaulting fund members into life insurance whenever they joined a fund.

Policy makers had two main areas of concern with this practice, firstly, the sense that younger members were less likely to need life insurance because of their circumstances, and secondly, millions of inactive and small balance accounts were having their balances eaten away by premiums for insurance people either didn’t want or didn’t realise they had.

PMIF had three main elements – members under 25 would now need to opt-in to insurance cover, rather than being granted in automatically. Similarly, active accounts with low balances (under $6,000) would also need to opt in. And inactive accounts (no activity for 16 months) would have life insurance cancelled (regardless of whether it had been actively selected).

To the extent that these changes came into effect 12 months earlier than the stapling and performance benchmarking changes, we have had longer to see how they played out in the market, and the outcomes haven’t been universally positive.

Whilst the majority of under 25s may not need death cover, they almost universally are highly dependent on their income to support their lifestyle (car loans, mobile phones, travel, and entertainment). As the most accident prone of all age groups, the under 25s CAN therefore benefit from the income protection cover offered through most funds. But despite this, their cognitive overload, combined with a sense of bulletproof invulnerability, sees the incidence of younger members opting in extremely low (ASFA estimated under 10%)[11].

Our inertia also was evident in the generally low response to industry efforts to have members with inactive accounts confirm their insurance preferences. ASFA research found just 16% of holders of such accounts opted to keep their life insurance[12].

As well as creating a large new block of uninsured workers, these changes will also impact age and risk profile of group life pools and perhaps force the introduction of underwriting for those opting in for cover, to avoid the problem of anti-selection. Group life premiums have already been impacted by these changed dynamics, with some funds increasing premiums by more than 30% shortly after the legislation took effect[13], thereby placing pressure on members more likely to need/want cover.

Furthermore, the creation of a large cohort of younger Australians without cover also creates a cohort who don’t understand or appreciate the value of life insurance – lower life insurance literacy – which may well impact their desire to seek out life insurance advice as they become older.

Marketing expenditure

Under their new duty to act in members’ best financial interests, fund Trustees will be required to identify a “quantifiable financial benefit to members” and provide “robust quantitative and qualitative evidence” in justifying any type of expenditure.

According to the AFR[14], Treasury experts expect the law to thwart the ability of funds to advertise their products and pay dues to lobby groups.

Whilst a thinly veiled effort to unplug the millions spent on advertising by industry funds, the legislation applies to all funds, and to the extent that smaller and newer funds may be dissuaded from investing in marketing, the law could inadvertently benefit those large, existing funds who have already invested heavily in establishing strong brand awareness.

Competition could once again be quelled.

Conclusion

The effectiveness of regulatory intervention intended to protect consumers can often be undermined by their vulnerability to irrational decision making and reliance on mental short cuts. Viewed through this lens, the latest round of superannuation changes, despite their sound theoretical basis, and independent of any ideological/political considerations, can actually be seen to have the potential to lead to consequences which are detrimental to, rather than protective of, consumers interests.

———-