Weekly economic and market update – week ending 16 July, 2021

Investment markets and key developments over the past week

Share markets were buffeted again by higher inflation and mixed messages from various central banks over the last week. While US and European shares fell slightly, Japanese, Chinese and Australian shares rose benefitting from the rally in US shares at the end of the previous week. The gain in Australian shares came despite bad news on lockdowns and was led by utility, material, retail and industrial shares. Bond yields continued to fall and commodities were mixed with metals and iron ore up but oil down as OPEC and the UAE closed in on a deal to boost production and US oil inventories rose. The $A fell as the $US rose.

Being stuck in a lockdown it’s nice to find upbeat songs. Being a big fan of Jeff Lynne and ELO after he worked with George Harrison on Cloud Nine I love Mr Blue Sky. Maybe being a relative optimist, I am naturally attracted to it. Recently I discovered One Summer Dream which is a classic very thoughtful summer song from ELO. In fact it was the B-side of Mr Blue Sky. The original of One Summer Dream had backing vocals by Ellie Greenwich a Brill Building songwriter who with partner Jeff Barry and Phil Spector wrote Da Doo Ron Ron, Then He Kissed Me, Be My Baby and a whole bunch of other classics.

Anyway, on to markets and ground hog day with coronavirus…we continue to see the fall back in bond yields as part of a correction against a rising trend in yields that will resume as global recovery continues. Shares could see more weakness in the short term as coronavirus cases rise, the inflation scare continues and central banks become less dovish and as we come into the seasonally weaker months for shares around August/September, but the rising trend in shares led by cyclical trades is likely to resume into year-end and continue through next year as rising vaccination allows the economic recovery to continue at the same time that interest rates and bond yields remain low.

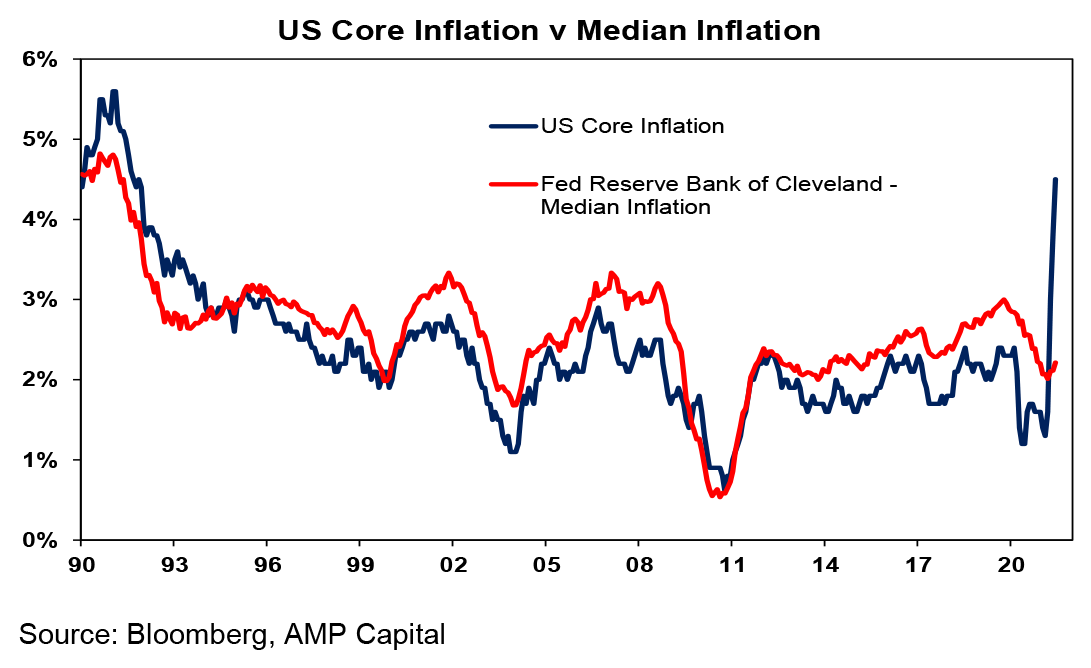

The inflation scare continued over the last week with blow out CPI reports in the US, UK and NZ and similar for producer price inflation in the US and Japan, but it still looks mostly transitory. Just 5 pandemic/reopening distorted items (covering vehicles, vehicle rental, airfares and hotels) covering just 12% of the core CPI drove 75% of its increase. The 45% increase in used car prices over the last year alone accounts for one third of the rise in core inflation. The other items rose just 2%yoy and median CPI inflation is just 2.2%yoy suggesting that it’s still not very broad based. And outside the US there is not a lot of evidence of pass through of high producer price inflation to consumers.

The news out of central banks was a bit confusing over the last week, but the big ones remain dovish. On the one hand the RBNZ surprised by abruptly ending its bond buying program one year ahead of schedule and sounding a lot more hawkish causing many to now expect the start of rate hikes by August. And this has been reinforced by higher than expected inflation which was driven by similar things to what we are seeing globally (ie, building costs, fuel, vehicles). The thing though is that underlying inflation measures were already in the RBNZ’s target range, the RBNZ is very erratic and its likely being influenced by the addition of house prices to its mandate so its not a good guide to other central banks, particularly the RBA. Meanwhile the Bank of Canada continued to taper its weekly bond buying and the Bank of Korea was hawkish and appears to be on track for a rate hike soon. Against this though comments by the ECB’s Lagarde point to a dovish adjustment to its forward guidance on monetary policy. Fed Chair Powell remained relatively dovish seeing the inflation spike as likely temporary and the economy still a “ways off” achieving further substantial progress to the Fed’s goals suggesting he is not rushing into a taper (we expect it from year-end). And the BoJ remained dovish following its latest meeting.

Will another debt ceiling battle hit US shares? It could cause some nervousness and contribute to a correction but it’s unlikely to derail shares for long. The US debt ceiling expires on August 1, Treasury can use various reserves to keep going into mid-September after which it will default on payments unless the ceiling is raised. As we saw in 2011 and 2013 there could be brinkmanship, but such disruptions are unpopular with voters and the Republicans are not as anti-debt as they used to be so 10 Republican senators can probably be found to get the 60 votes needed to raise the ceiling. If not, the Democrats can include it in their upcoming budget reconciliation bill (which will seek to pass President Biden’s American Jobs and Families Plans into law) and hence pass it with a simple majority. So I wouldn’t worry about it too much.

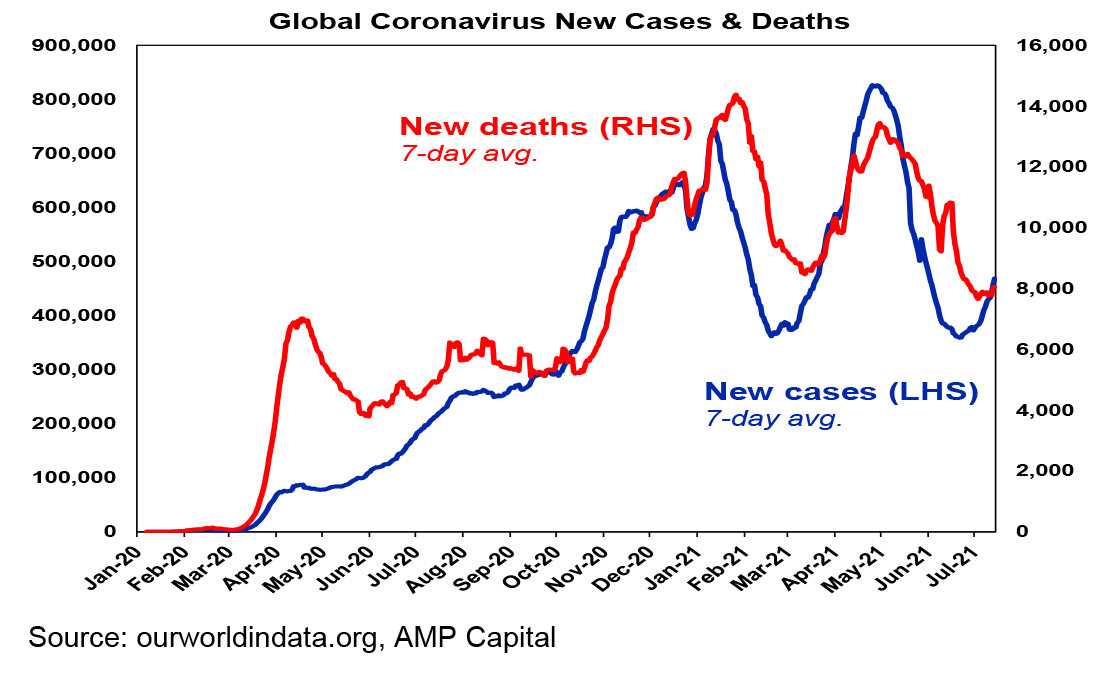

The latest wave of new coronavirus cases globally is continuing to build, with the more contagious Delta variant adding to the risk. This has the potential to further unnerve investors – but the key is what happens to hospitalisations & deaths in countries that are well down the vaccination path.

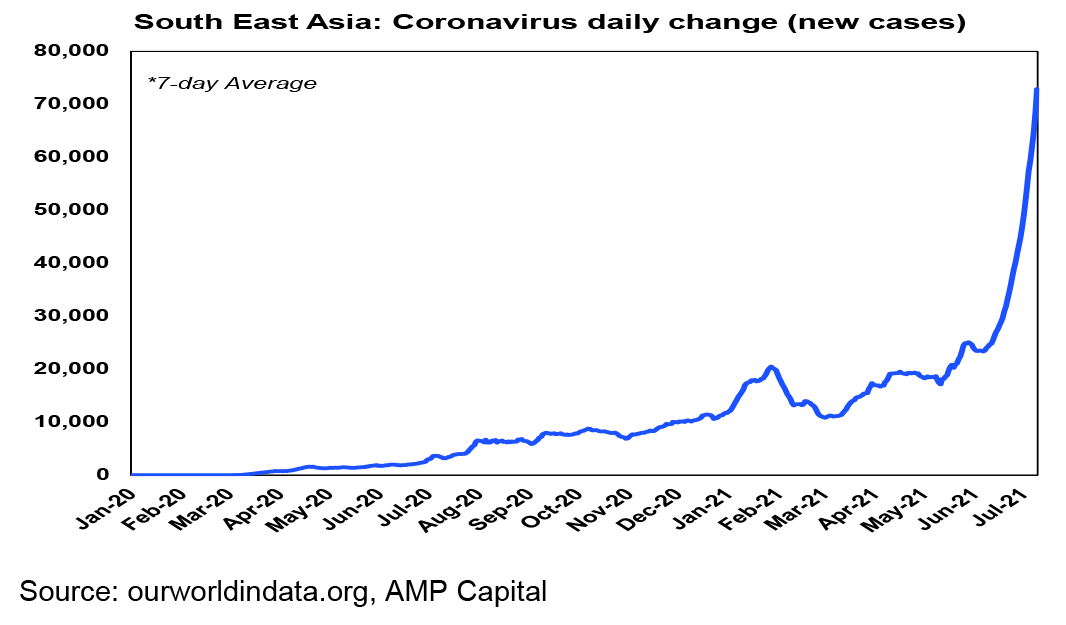

Lowly vaccinated countries have little choice but to tighten restrictions and lockdowns in order to keep pressure off hospital systems and minimise deaths and this is what we have been seeing throughout Asia, South Africa and elsewhere. Of course, Australia is in the same boat.

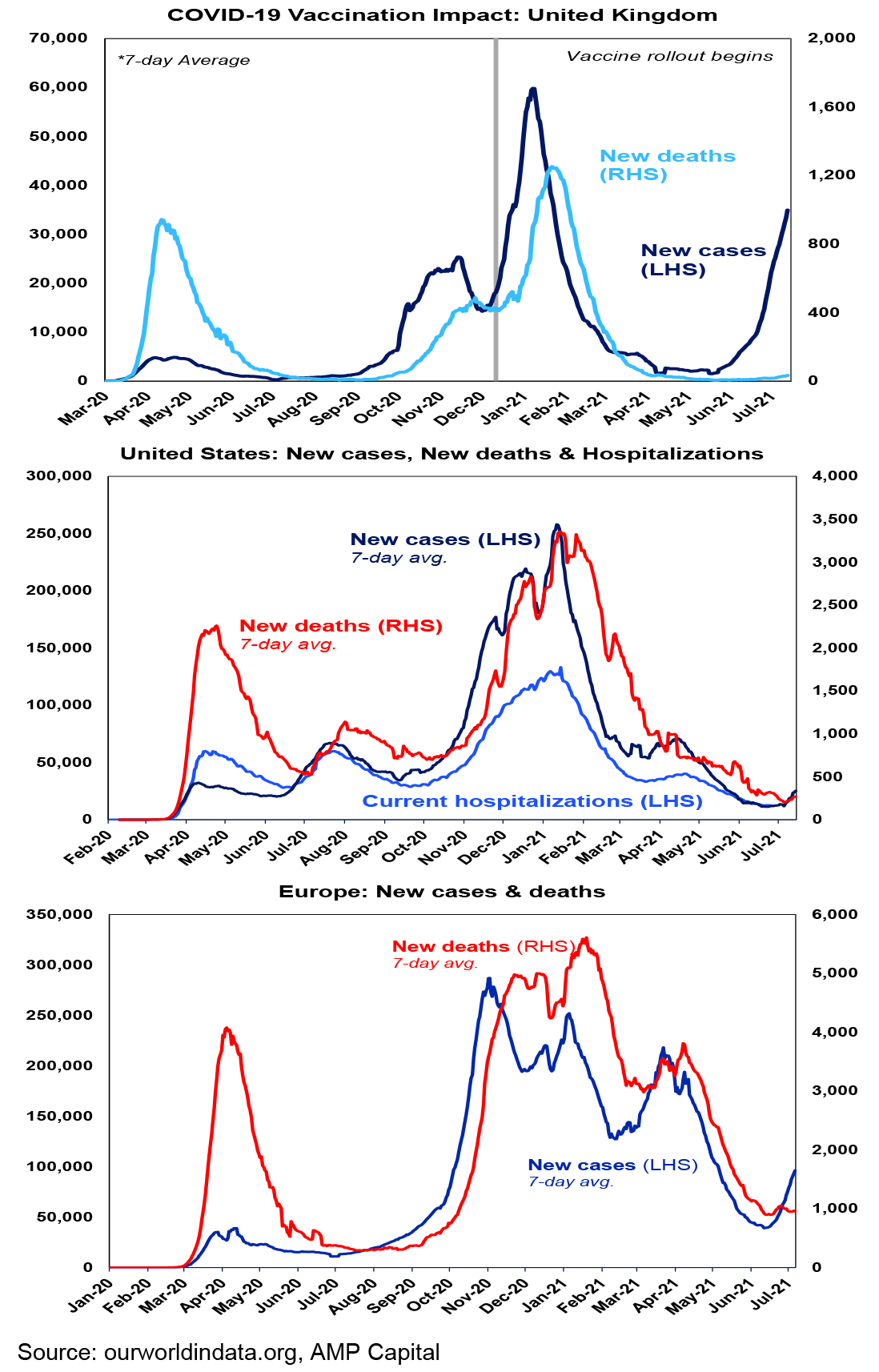

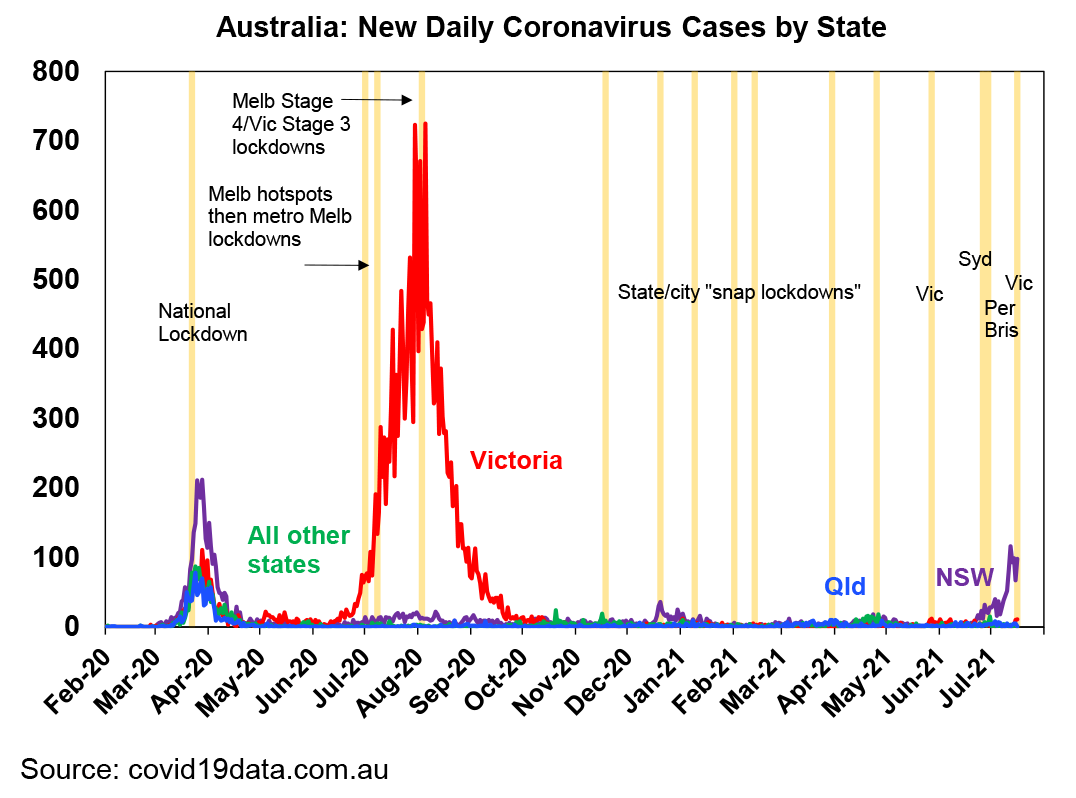

But it’s a different situation in the more vaccinated UK, US and Europe. The UK is now seeing new daily cases over 30,000 (up from a recent low of 1600 a day), the US is over 25,000 (up from 12,000) and Europe nearly 100,000 (up from 40,000) – all of which make Australia look like a non-event population adjusted or not! Of course, this poses a significant risk in that these countries are still below herd immunity and the vaccines are known to be less effective in preventing Delta infection. So, it risks causing concern particularly amongst the young and in low vaccinated (mostly Red) US states.

However, while it would be desirable to have waited for 70-80% vaccination before fully reopening, the risk of a return to severe lockdowns and a derailing of the recovery in more vaccinated countries is low compared to previous waves. First, various studies show that the vaccines are highly effective (ie 90% plus) against serious illness necessitating hospitalisation even with the new variants. Second, most older more at risk people have been vaccinated. So far hospitalisations and deaths have been edging up but remain low in the UK, US and Europe and this remains the key to watch going forward. While deaths lag new cases, note that deaths don’t seem to be following their past relationship to new cases in the chart below for the UK which is a good sign.

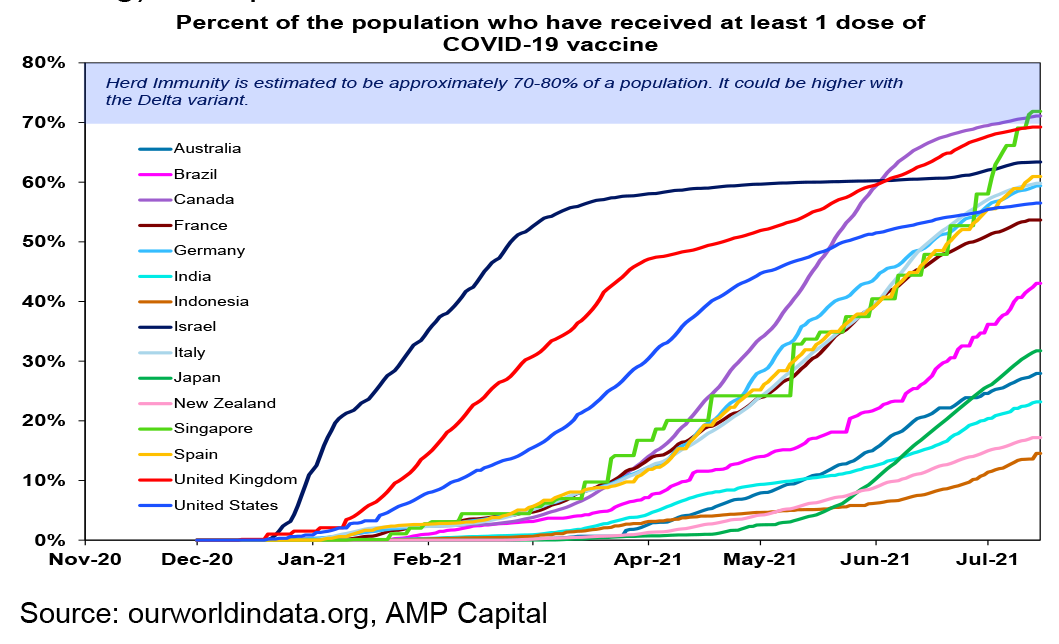

On the latest count 27% of people globally and 54% in developed countries have had at least one dose of vaccine. Canada is now at 71%, the UK at 69%, the US at 57% (and stalling), Europe at 55% and Australia is at 28%.

Being relatively lowly vaccinated, means that Australia has little option but to implement distancing and lockdowns to control the spread of coronavirus to limit pressure on the hospital system and prevent deaths following the latest outbreaks. “Learning to live with coronavirus” in the absence of high levels of vaccination will just mean “learning to die with it” and the consequences of long covid. The experience since November tells us that lockdowns that are hard and start early when new cases are running around 1 to 10 a day are successful and can end within two weeks with minimal economic impact. Whereas lockdowns that start later take longer to work with higher economic and health costs. And there is now academic support for this. This is particularly likely to be the case with the Delta variant,

Consistent with this the Sydney lockdown started relatively late in terms of new daily cases (averaging around 20 a day over the 3 days up to the start of the lockdown) and has been relatively light as far as lockdowns go. It has already been extended for five weeks and while there are some positive signs (with new local cases, the positive testing rate and new cases not isolating while contagious down from their peak a bit and not exploding higher) it’s way too early to say the worst is over and there is a high risk that it will have to be extended again and/or tightened further. Victoria has also gone back into isolation after having seen a rise in cases spread from NSW – but having started when new daily cases were running at 10 and being harder (with non-essential retail closed) it should hopefully be shorter than that in NSW and so impose a smaller economic cost. Our rough estimate is that it will cost about $700mn if it runs for five days as planned.

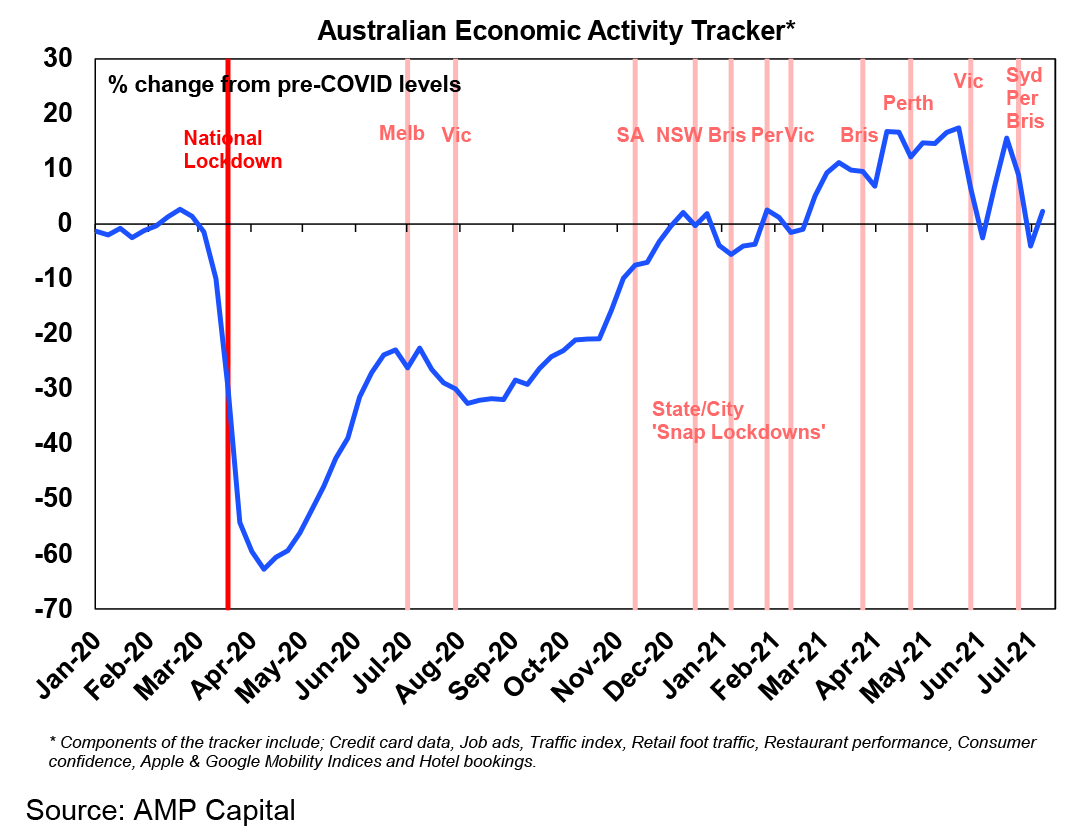

The economic impact of the lockdowns is evident in our Australian Economic Activity Tracker remaining down from recent highs but it’s not seeing the precipitous collapse seen going into April last year and in fact rose slightly in the last week because other states are providing an offset to NSW and businesses and households have found more ways to work through lockdowns. That said with NSW’s lockdown being extended and Victoria going back into lockdown we may see further softness in the week ahead.

We are now assuming that the Greater Sydney lockdown will last seven weeks. So at a cost of around $1bn a week it will cost the NSW and hence Australian economies around $7bn. To this must now be added the 5-day Victorian lockdown with a cost of around $700mn. Adding in all the lockdowns since late May it means a cost the economy spread across the June and mainly September quarters of nearly $10bn. Government income support costing more than $0.5bn a week – basically JobKeeper lite entailing payments to businesses contingent on them maintaining their workforce and payments to workers similar to what they would have received from JobKeeper late last year – will help soften the blow but will mainly serve to help keep the economy resilient so it can bounce back quickly once the lockdown ends.

Assuming other states keep growing (including Victoria beyond its current lockdown) and NSW rebounds through September helped by pent up demand and the lagged impact of support payments, the extended lockdown will likely flatten GDP growth this quarter (we were assuming growth of 1%qoq) and risks sending it slightly negative. Allowing for a solid rebound in the December quarter this will likely push GDP growth in Australia through the year to the December quarter down to around 4%yoy from our previous forecast of 4.75%. The hit to the NSW economy could push unemployment up temporarily from 4.9% currently, but it would likely quickly resume its downtrend later in the year and through next year, albeit it may not be below 5% at year-end as we were expecting. A further extension of the Sydney lockdown and further Delta outbreaks across Australia are a key risk. Although having seen the impact on Sydney, other states are likely to be extra cautious in making sure they don’t see the same (witness Victoria’s rapid response in the last week) – which means the risk of early snap and short lockdowns but averting longer economically debilitating lockdowns like that seen in Sydney. Beyond the next few months there remains reason for optimism as vaccination picks up ultimately enabling a more sustained and confident reopening through next year. This combined with significant pent-up demand and an even higher level of savings after the Sydney lockdown along with ongoing fiscal stimulus and ultra-easy monetary policy will likely result in compensating stronger growth in 2022.

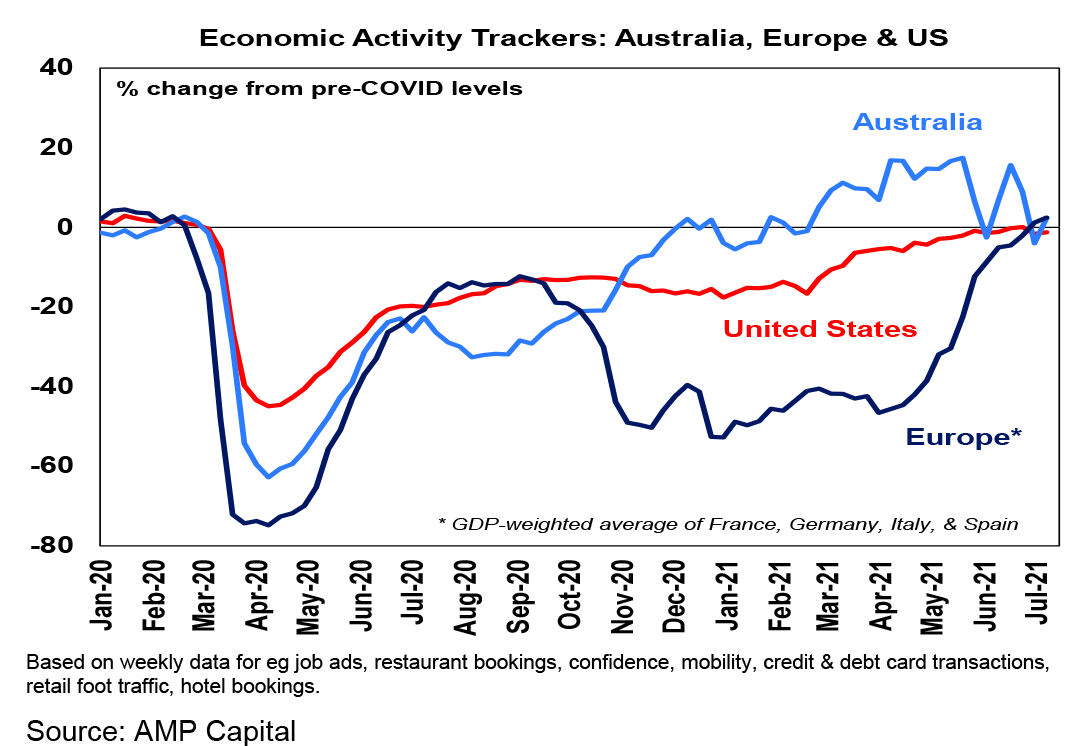

Our US Economic Activity Tracker ticked up in the past week but has been little changed since May. Our European Tracker recovered further and is above pre coronavirus levels.

Major global economic events and implications

US data releases remained solid with a rise in small business confidence, strong business conditions in the Philadelphia and New York regions and a fall in jobless claims. Industrial production rose less than expected partly due to ongoing supply chain disruptions holding auto production back. Along with stronger than expected consumer and producer price inflation, price pressures remained strong in various business surveys, albeit prices paid fell a bit in the Philadelphia and NY surveys.

The BoJ made no major changes to monetary policy but will offer banks interest free funds for climate linked lending and will exempt more reserves from negative interest rates.

Chinese GDP growth accelerated in the June quarter to 1.3%qoq from 0.4% in the March quarter. Similarly, for June activity data which showed some slowing in year on year growth but an acceleration in monthly retail sales and industrial production growth and a pickup in year ended investment growth. Export and import growth were also stronger than expected. Overall, Chinese growth remains solid.

Australian economic events and implications

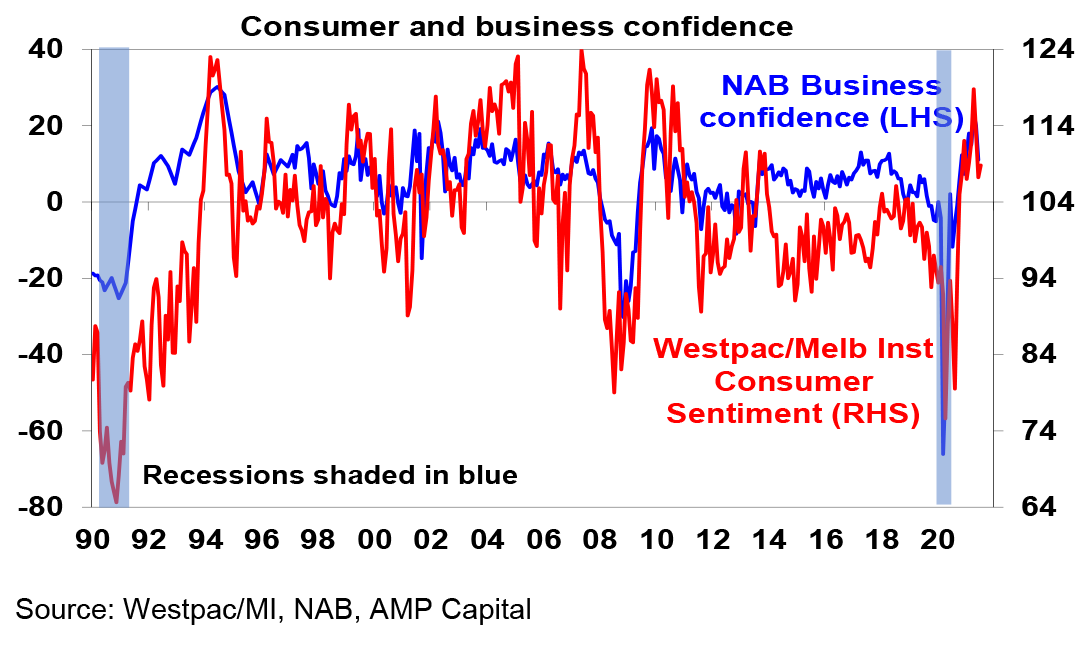

Australian economic data was mixed. Jobs data was strong in June with unemployment falling to a 10 year low of 4.9%. Normally this would have boosted talk of earlier RBA rate hikes but dated now with the NSW lockdown likely to depress this month’s jobs report. Meanwhile business conditions and confidence fell in June in response to the Victorian lockdown, but consumer confidence surprisingly rose in July as depressed confidence in NSW was offset by strength in other states.

Ongoing lockdowns are likely to depress confidence in the near term, but providing they are relatively short and given government income assistance and greater familiarity with lockdowns its likely to hold up reasonably well. Both business and consumer confidence remain reasonably strong. Finally, new home sales rose in June and remain strong.

What to watch over the next week?

In the US, expect continuing strength in the home building conditions index (Monday), a rise in housing starts (Tuesday) and existing home sales (Thursday). Business condition PMIs for July (Friday) will likely soften a touch but remain strong with the focus likely to be on price readings.

June quarter company profit results will start to ramp up with the consensus now looking for a 65% year on year rise boosted by base effects but the rebound in various macro variables suggesting this could end up being +90% or so.

The ECB (Thursday) is expected to leave monetary unchanged but is expected to adopt more dovish forward guidance consistent with its more dovish inflation target. European business conditions PMIs for July (Friday) will likely show a further rise.

Japanese CPI inflation data for June (Tuesday) is expected to remain weak with core inflation staying weak at -0.2%yoy.

The minutes from the last RBA meeting at which it announced a slowing in bond buying from September will be released Tuesday but it’s hard to see they will add much given Governor Lowe’s various addresses after the meeting and the increased risk to the outlook from the latest coronavirus outbreak. Meanwhile, expect June retail sales (Wednesday) to fall -1% thanks to various lockdowns and the Sydney lockdown to weigh on July business conditions PMIs (Friday).

Outlook for investment markets

Shares are vulnerable to a short-term correction with possible triggers being the latest upswing in global coronavirus cases, the inflation scare and US taper talk and geopolitical risks. But looking through the inevitable short-term noise, the combination of improving global growth and earnings helped by more fiscal stimulus, vaccines allowing reopening once herd immunity is reached and still low interest rates augurs well for shares over the next 12 months.

Still ultra-low bond yields and a capital loss from rising yields are likely to result in negative returns from bonds over the next 12 months.

Unlisted commercial property may still see some weakness in retail and office returns but industrial is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home prices now look likely to rise 20% this year before slowing to around 5% next year, being boosted by ultra-low mortgage rates, economic recovery and FOMO, but expect a progressive slowing in the pace of gains as poor affordability impacts, government home buyer incentives are cut back, fixed mortgage rates rise, macro prudential tightening kicks in and immigration remains down relative to normal.

Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%. We remain of the view that the RBA won’t start raising rates until 2023.

Although the $A could pull back further in response to the latest coronavirus scare and the threat it poses to global and Australian growth, a rising trend is likely to remain over the next 12 months helped by strong commodity prices and a cyclical decline in the US dollar, probably taking the $A up to around $US0.85 over the next 12 months.

By Shane Oliver