The year behind, the year ahead.

The past year: 2020/21

- In 2019/20 Australia experienced its first recession in 28 years – impacted by the COVID-19 coronavirus as well as drought, bushfires and storms. But over 2020/21 the Australian economy has experienced the sharpest recovery since the 1970s due to the relative success in suppressing the COVID-19 virus as well as the speed and size of economic stimulus and support supplied by all levels of government and the Reserve Bank.

- The cash rate ended 2020/21 at a record low 0.1 per cent; the Aussie dollar stands near US75 cents; unemployment stands at 5.1 per cent; annual inflation is 1.1 per cent; the S&P/All Ordinaries lifted 26.4 per cent over the year – the biggest gain in 34 years; and the S&P/ASX 200 index lifted by 24 per cent for the year. Total returns on shares (includes dividends) grew by 30.2 per cent in 2020/21.

The year ahead: 2021/22

- As we enter 2021/22, it is clear that COVID-19 still dominates the landscape. The bad news is that countries are still experiencing virus break-outs. The good news is that effective vaccines are being distributed across the globe.

- The economic outlook will clearly be dictated by the virus and its variants, and how quickly the vaccines can stem case numbers and allow economies to start repairing.

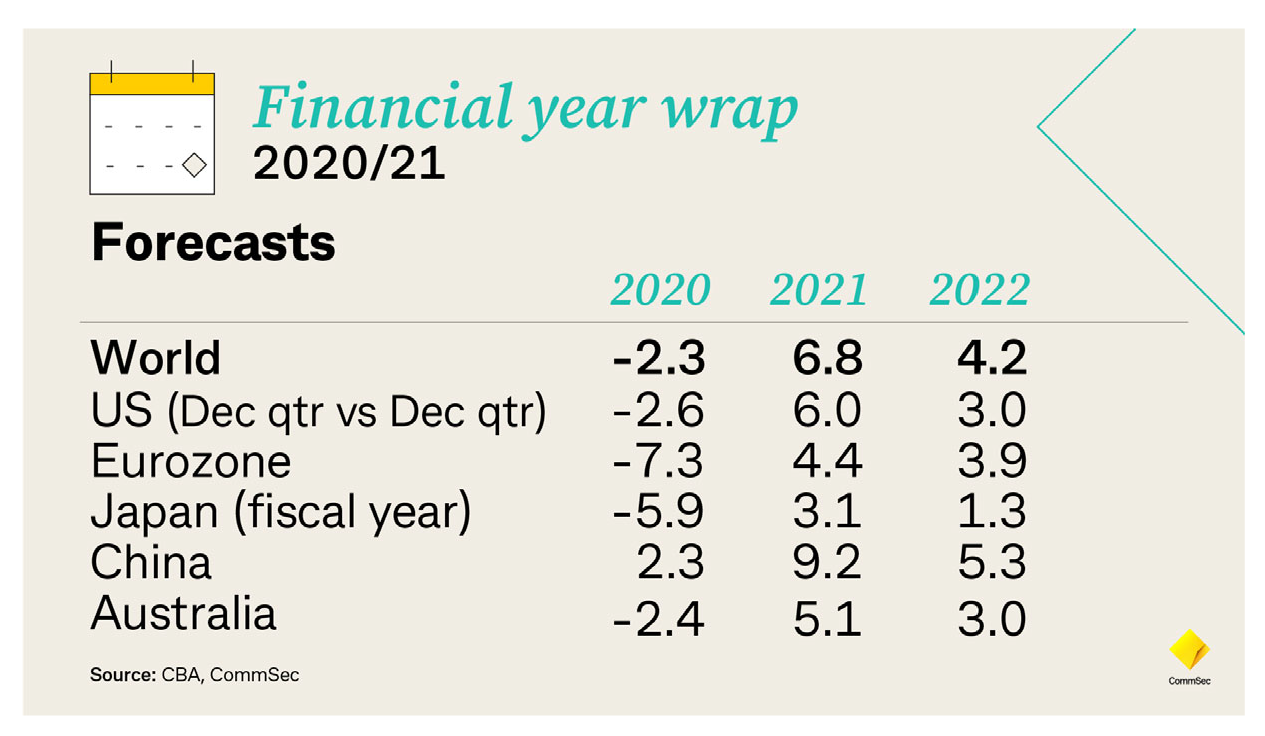

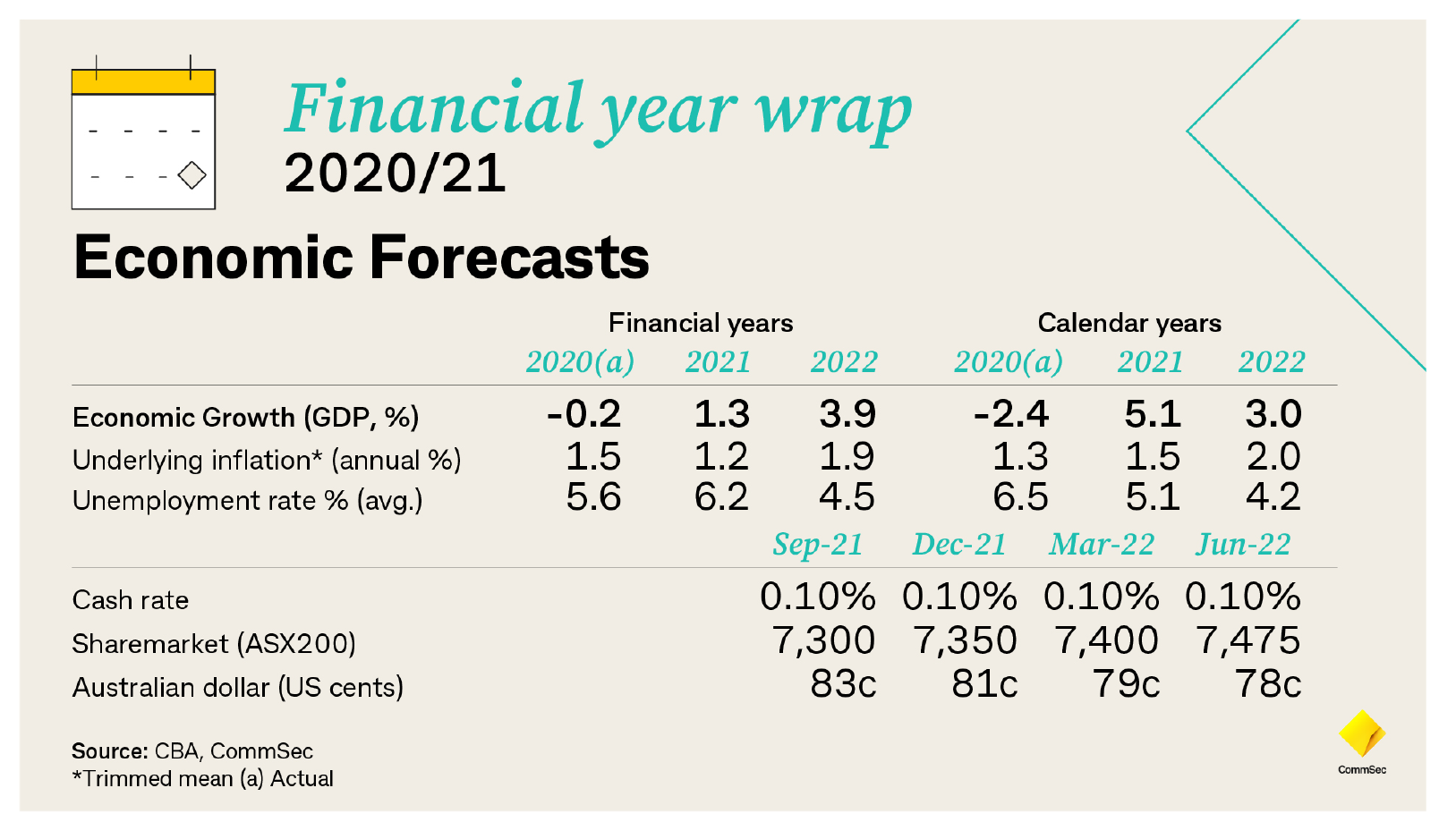

- After contracting an estimated 2.3 per cent in 2020, the global economy is tipped to rebound by 6.8 per cent in 2021. On the same basis, the Australian economy is tipped by Commonwealth Bank (CBA) Group economists to grow by 5.1 per cent in 2021 after contracting 2.4 per cent in calendar 2020.

- The Reserve Bank (RBA) doesn’t expect to start lifting the cash rate until 2024 at the earliest. However CBA Group economists now tip the first rate hike in November 2022. But there are basically three pre-conditions for rates to rise. The Reserve Bank wants to see annual inflation sustainably between 2-3 per cent; it wants to see growth in annual wages lifting to 3 per cent; and the RBA is aiming for full employment – targeting a jobless rate near 4 per cent.

- Unemployment is the focal point of all monetary and fiscal policy actions. CBA Group economists expect the jobless rate to ease to 4.5 per cent by the end of 2021 and ease further to the ‘full employment’ level of 4.0 per cent by the end of 2022. Underlying inflation is expected to gradually lift to 1.8 per cent by end-2021 and 2.2 per cent by end-2022.

Interest rates

- The cash rate has remained at a record low of 0.10 per cent since the RBA last cut the rate by 15 basis points on November 3, 2020.

- On November 3 the RBA announced:

- a reduction in the interest rate on new drawings under the Term Funding Facility to 0.1 per cent.

- a reduction in the interest rate on Exchange Settlement balances to zero.

- and the purchase of $100 billion of government bonds of maturities (also known as Quantitative Easing) of around 5 to 10 years over the next six months.

- On February 2, 2021 the RBA “decided to purchase an additional $100 billion of bonds issued by the Australian Government and states and territories when the current bond purchase program is completed in mid-April. These additional purchases will be at the current rate of $5 billion a week.”

- The market-determined 90-day bank bill rate fell from highs near 0.1056 per cent in July 2020 to record lows of 0.0097 per cent in February and yields ended 2020/21 at 0.0303 per cent.

- Yields on the long bond – 10-year government bond – held in a range of 0.75 per cent to 1.85 per cent and yields ended the year at 1.48 per cent. The low yield of 0.75 per cent was set on November 5, 2020.

Exchange rates

- The Aussie dollar lifted by 10 per cent against the greenback over 2020/21. The Aussie started the year around US69 cents and ended the year near US75 cents. The Aussie hit a 3-year high of US79.70 cents on February 25, 2021, while the year’s low of US68.95 cents was set a year ago on July 1, 2020.

- The Aussie has been supported by solid economic data, rising commodity prices (especially iron ore) and improved risk sentiment on the global economy.

- Over 2020/21 the Aussie eased against the pound sterling (-3 per cent); and the Canadian dollar (-1 per cent). The Aussie lifted against the Japanese yen (+12 per cent); NZ dollar and Chinese yuan (both less than 1 per cent); the Swiss Franc (+6 per cent) and the Euro (+3 per cent). On a trade weighted basis the Aussie strengthened by 5 per cent.

Sharemarkets

- At the end of June 2020, the Australian All Ordinaries index stood at 6,001.3 with the ASX 200 at 5,897.9. The All Ordinaries ended the 2020/21 year at 7,585, up 26 per cent – the biggest rise for a financial year in 34 years. The ASX 200 ended the year at 7,313, up 24 per cent – a record financial year gain. The All Ordinaries first regained record highs on April 14, 2021 while the ASX 200 lifted to fresh record highs on May 10.

- Movements of other key markets over the financial year were: US Dow Jones (+34 per cent); US S&P500 (+39 per cent); US Nasdaq (+44 per cent); Japan Nikkei (+29 per cent); UK FTSE (+14 per cent); German Dax (+26 per cent).

- The world index (MSCI) excluding Australia in US dollar terms rose by 37 per cent over 2020/21. The MSCI Australia index in US dollar terms lifted by 34 per cent.

Australian sharemarket sectors and asset returns

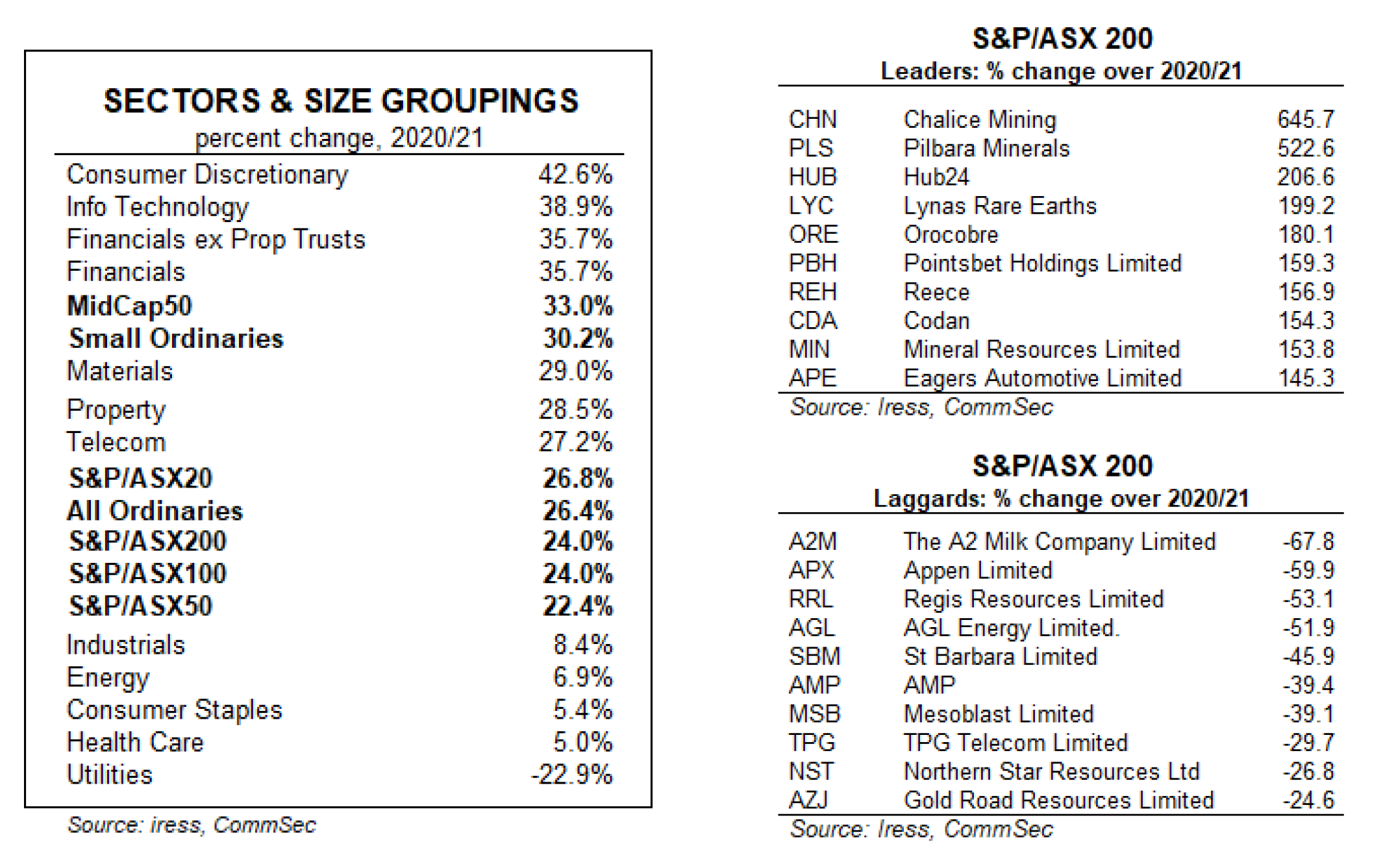

- Australia’s Consumer Discretionary sector out-performed over 2020/21. Consumer Discretionary shares rose by 42.6 per cent over the year, ahead of Information Technology (+38.9 per cent) and the Financials sector (+35.7 per cent).

· At the other end of the scale, the Utilities sector fell by 22.9 per cent while Health Care lifted by just 5.0 percent and Consumer Staples gained 5.4 per cent.

· Of the size groupings, the MidCap50 out-performed (+33.0 per cent) from the Small Ordinaries (+30.2 per cent). The S&P/ASX20 lifted by 26.8 per cent while the S&P/ASX50 recorded the smallest gain – up 22.4 per cent.

· Total returns on Australian shares (All Ordinaries Accumulation index) lifted by 30 per cent over 2020/21. The cash rate stands at 0.1 per cent while bond returns (Bloomberg AusBond Govt 0+ Yr index) fell by 1.4 per cent. And residential property (CoreLogic Home Value index) returned 14.3 per cent in the year to May.

Commodity prices

- The CommSec daily commodity index lifted by 92 per cent in 2020/21 in US dollar terms. Over the same period the Aussie dollar rose by around 10 per cent.

- The Reserve Bank commodity index in US dollar terms (using spot prices for bulk commodities) was up by 60 per cent in the year to May. Bulk commodity spot prices were up 98 per cent over the period while rural commodity prices (us dollar terms) were up by 24 per cent.

- In contrast, the CRB futures commodity index rose by 55 per cent over 2020/21.

- Some of the stand-out gains from an Australian perspective have been natural gas (up 468 per cent), thermal coal (up 158 per cent), iron ore (up 116 per cent), crude oil (up 87 per cent) and coking coal (up 79 per cent).

- At the other end of the scale, the rice price fell by 14 per cent, followed by gold (down 2 per cent).

Outlook 2021/22

- The Australian economy continues to surprise and much has to do with the strength of the job market. The latest data shows that a stunning 115,200 jobs were created in just the month of May. Employment is back at record highs – recovering all pandemic losses – in fact it is one of only a few economies to have achieved that feat.

- The jobless rate now stands at 5.1 per cent, a 17-month low. In fact the reduction in the jobless rate over the past six months has been a record for any similar period. And monthly data extends back to 1978. The underutilisation rate stands at an 8-year low of 12.5 per cent (lowest since February 2013). The underemployment rate stands at 7.4 per cent – a 7-year low.

- Reduction of the jobless rate is regarded a “national priority”. And there is good scope for unemployment to fall further given that job vacancies stand at 12½-year highs. This is just not important in terms of the spending power of the newly employed, but also the boost to confidence of those people in jobs.

- CBA Group economists now expect the jobless rate to end 2021 at 4.5 per cent and fall further to 4.0 per cent by end 2022. As a result, annual wage growth is expected to lift from 1.5 per cent currently to 2.4 per cent by the end of 2021 and to lift to 2.9 per cent by the end of 2022.

- Across a raft of sectors, businesses are finding it harder to find suitable workers. There are likely to more examples of visas being granted to migrants to fill skill shortages.

- Overall we expect the Australian economy to grow by 3.9 per cent in 2021/22 after rising by an estimated 1.3 per cent in 2020/21. Risks to the forecasts include virus outbreaks; slow vaccine take up or vaccine shortages; policy mistakes on the removal of support measures; Chinese political tensions and extended delays in the re-opening of foreign borders.

- While the annual rate of headline inflation is expected to spike to 3.0-3.5 per cent in the June quarter, underlying inflation is expected to remain below the Reserve Bank’s (RBA) 2-3 per cent target band. After averaging 1.2 per cent in 2020/21, trimmed mean inflation is expected to average 1.9 per cent in 2021/22. Still, underlying inflation is expected to gradually lift to 1.8 per cent by end-2021 and 2.2 per cent by end-2022.

- The RBA currently expect the cash rate to stay at 0.10 per cent through to 2024. However we believe that the risks are tilted to unemployment surprising on the downside and wage and price inflation surprising on the upside.

- The RBA wants to see the jobless rate fall to the “full employment” level near 4 per cent. Only when it is near these levels does the RBA believe that the hoped-for wage growth of around 3 per cent will materialise.

- And when these conditions hold, the RBA expects inflation to sustainably hold between 2-3 per cent. The RBA doesn’t expect all this to occur until 2024 at the earliest. But as noted, CBA Group economists expect these conditions to be met earlier – with the RBA starting the process of normalising the cash rate in November 2022.

- Turning to the housing market, a record number of homes will be built in 2021. And this increased supply, together with the restraint on demand through the closure of the foreign borders will serve to slow the pace of home prices. That said, CBA Group economists expect national home prices to lift at double-digit annual rates over most of the 2021/22 financial year.

- The Australian sharemarket has performed strongly over the past few months. Clearly this is explained by the success that fiscal and monetary stimulus has achieved in driving growth and securing improvement in the job market. Stronger global growth has also boosted commodity demand and prices, supporting the mining sector.

- While we expect further gains for the S&P/ASX 200 over the coming year, there will almost certainly be periods of correction and consolidation reflecting inflation and interest rate jitters and any local or global setbacks in reducing Covid-19 base numbers.

- We conservatively forecast the ASX 200 index to be in a range of 7,400-7,700 points by mid-2022.

- Turning to the Australian dollar, the currency is expected to remain supported by strength of the global economy. The global economy is expected to lift 6.8 per cent in 2021, and 4.2 per cent in 2022.

- More economies are expected to join China in lifting spending on infrastructure, further underpinning demand for metals and ores.

- In June 2022 CBA currency strategists expect the Aussie dollar to be near US78 cents. Upside risks include faster-than-expected re-opening of foreign borders reflecting virus control and vaccine take-up.

- However should the US Federal Reserve reduce stimulus earlier than the Reserve Bank, that could serve to boost the greenback and put downward pressure on the A$/US$ exchange rate.

- Clearly this is an evolving situation – and like most forecasts – reflects the uncertainties related to the once-in-a-century pandemic.