Happy 40th! Why Millennials are no longer the future of financial advice – they are the present

Millennials are the largest cohort of consumers and workers in Australia, who stand to benefit from the largest intergenerational wealth transfer ever seen.

Introduction

In an earlier article in this series, we discussed client segmentation, examining the many different ways segmenting clients and target markets can improve client engagement, efficiency, and practice profitability.

In this article, we commence a deeper exploration of specific client segments, shining a spotlight on Millennials (also known as Gen Y). Still considered by many advisers a fringe market for advice, due to their age and lack of assets, the Millennial generation has grown up fast, and is actively seeking expert financial help with their financial affairs. Beneficiaries of the $3 trillion intergenerational wealth transfer[1] that will take place in Australia over the next two decades, Millennials are not just the advice clients of the future, they hold the keys to building sustainable, fee-based financial advice businesses right now.

Meet the Millennials

So just who are the Millennials?

Whilst a brief online search reveals many different definitions, most are similar to that used by McCrindle Research[2], which sees the oldest Millennials having just turned 40:

According to McCrindle[3], there are over 5 million Millennials (or Gen Y) in Australia, meaning they outnumber both Gen X and Gen Z. By 2025 they are expected to represent a third of the workforce, which would again see them outnumbering Gen X (28% of the workforce), and Gen Z (31%).

Rather than being the focus of the future, Millennials already make up around a third of all consumer spending[4], making them a segment that companies across all sectors need to take notice of, immediately.

Most of us have seen/heard the Millennial stereotypes: they are lazy, expect to be promoted quickly, need constant praise (too many ‘achievement’ awards in school), spend all their time on social media, and still live at home.

Some financial advisers, too, have been guilty of pigeonholing them, deciding they don’t fit the traditional orthodoxy of needing or wanting advice because they are too young, and don’t yet have the assets or complexity of situation to warrant expert help.

But is any of this actually true?

Meaningful stereotypes

Focussing on insights of more practical value, it is possible to identify several characteristics shared by Millennials which reflect the world into which they were born.

- Tech savvy: the first generation to be digital natives, shaped by the internet and mobile technology.

- Social media smarts: Smartphones and social media feeds have become the chief information source for Millennials, and the way they consume products and services.

- Cause motivated: At work and in their personal lives, Millennials are heavily driven by the causes they support, and they are at the forefront of issues including climate change, sweatshop labour, and diversity & inclusion.

- Value experiences: Forgoing the suburban dream of their parents, many are living in the city, choosing travel and other experiences over mortgages and car loans. They are the first generation to embrace the concept of work/life balance.

Millennial money behaviours

Their money behaviours also differentiate them from older generations.

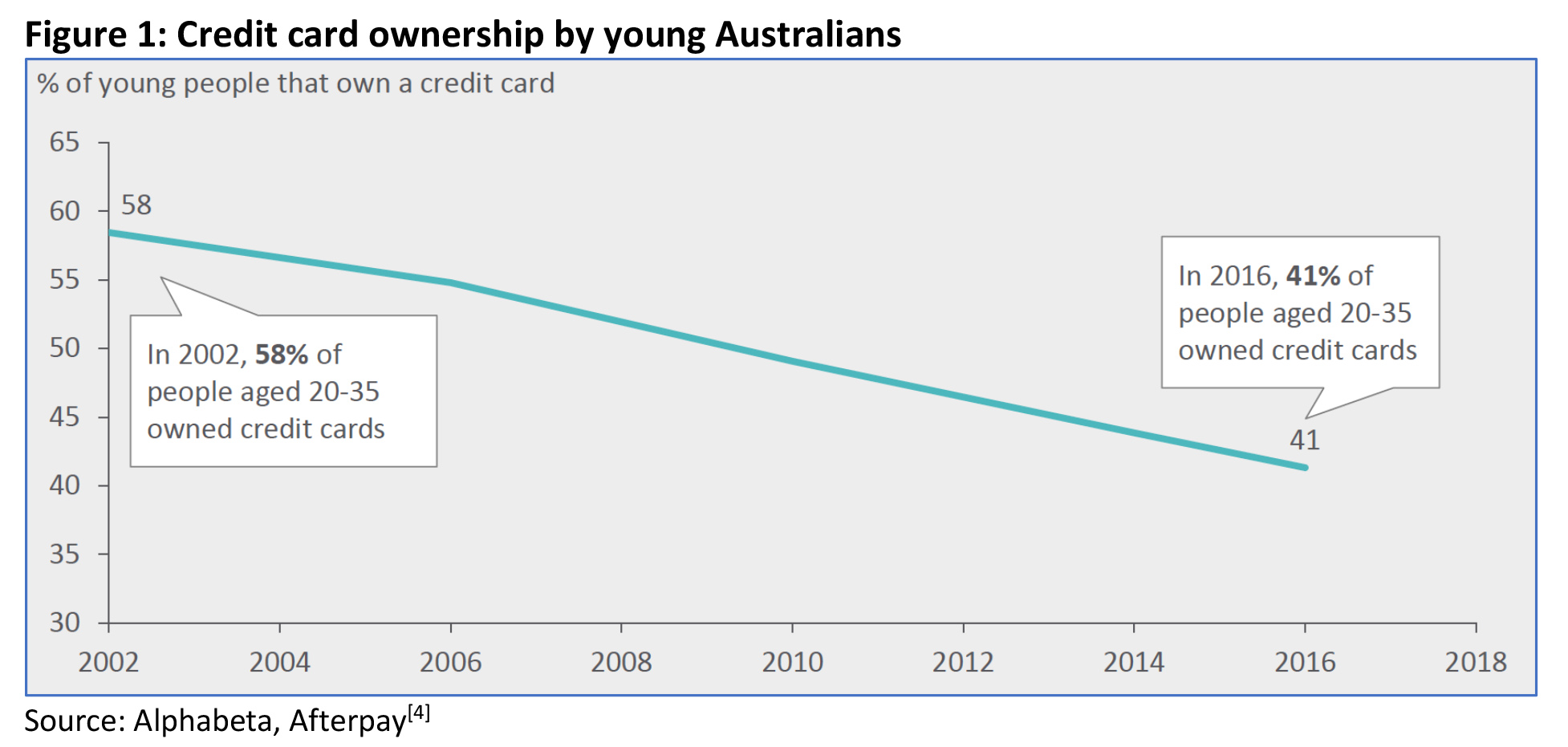

Credit

Millennials have a different attitude to credit than their parents, being 37% less likely to own a credit card (by choice) and holding lower debt levels as a proportion of income (10% of income vs 19% for older Australians).

Property

Probably the most significant financial challenge facing Millennials is that of home ownership. Driven by runaway demand for real estate, which not even a pandemic could dampen, rising property prices are making it harder for younger people to get a foothold on the property ladder.

Despite nearly 1 in 3 Millennials being university educated[5] (compared to 1 in 4 Gen X), and starting to enter their earnings prime, only 30% of Millennials own their own property, compared to 54% of Gen Xers and 68% of Baby Boomers[6].

Far from giving up on home ownership, one survey[7] found close to 80% of Millennials still aspire to ‘the Great Aussie Dream’ and are prepared to make major sacrifices to achieve this goal. More than half those polled said they would sacrifice little luxuries, experiences, and big-ticket items to make it happen and more than one quarter said they would even put off having children to afford their own home.

There are several implications of this reality.

Firstly, if you are a parent of Millennial children, the bad news is around a third expect to be living at home until they are 30[8].

Secondly, it means we have a whole generation desperately trying to amass the funds required for their first deposit. And with continuing low interest rates conspiring against the traditional savings path, more and more Millennials are turning to the stock market to accelerate their wealth.

Shares

Of the 46 per cent of Australians who now hold investments other than their primary residence or superannuation, the fastest growing demographic is Millennials[9], with the average age of new investors over the last 2 years being 34.

According to Canstar[10], around 40% of young Australians invested in the sharemarket in 2020, with 44% of Millennials participating for the very first time.

And the way they participated was noteworthy too.

The majority (58 per cent) directly invested in shares, 30 per cent invested via a managed fund, 20 per cent via a fractional investing app (e.g., Sharesies, Spaceship, CommSec Pocket) and 17 per cent via an exchange-traded fund[11].

Not all these investors are self-directed, either. Analysis of trading data by the Australian Investment Exchange (AUSIEX) found Millennial investors accounted for 8.4 per cent of trading accounts opened by financial advisers on the platform as of March, up from 3.8 per cent before November 2019 and the onset of the coronavirus pandemic12[12].

Other investment behaviour

Away from the sharemarket, Millennials are changing the face of other investment categories too, with research suggesting:

- They account for more than half of all new SMSFs[13]; and

- Are the most avid buyers of crypto currencies, with around 20% owning a digital currency[14].

But they need – and want – expert help

Despite being regularly lauded for their savings habits (36% say they save regularly, compared to 28% of older Australians[15]), research has found a majority of Millennials (61%) still don’t have a formal savings plan[16]. And they have still have ground to make up to in terms of the amount of savings, holding roughly two thirds[17] the amount held by their parents.

This can be problematic given their top financial priorities (home deposit, travel, financial independence) are largely enabled by savings.

Encouragingly, Millennials are self-aware enough to know that they need expert help, and savvy enough to realise that the best qualified experts to provide relevant help are financial advisers.

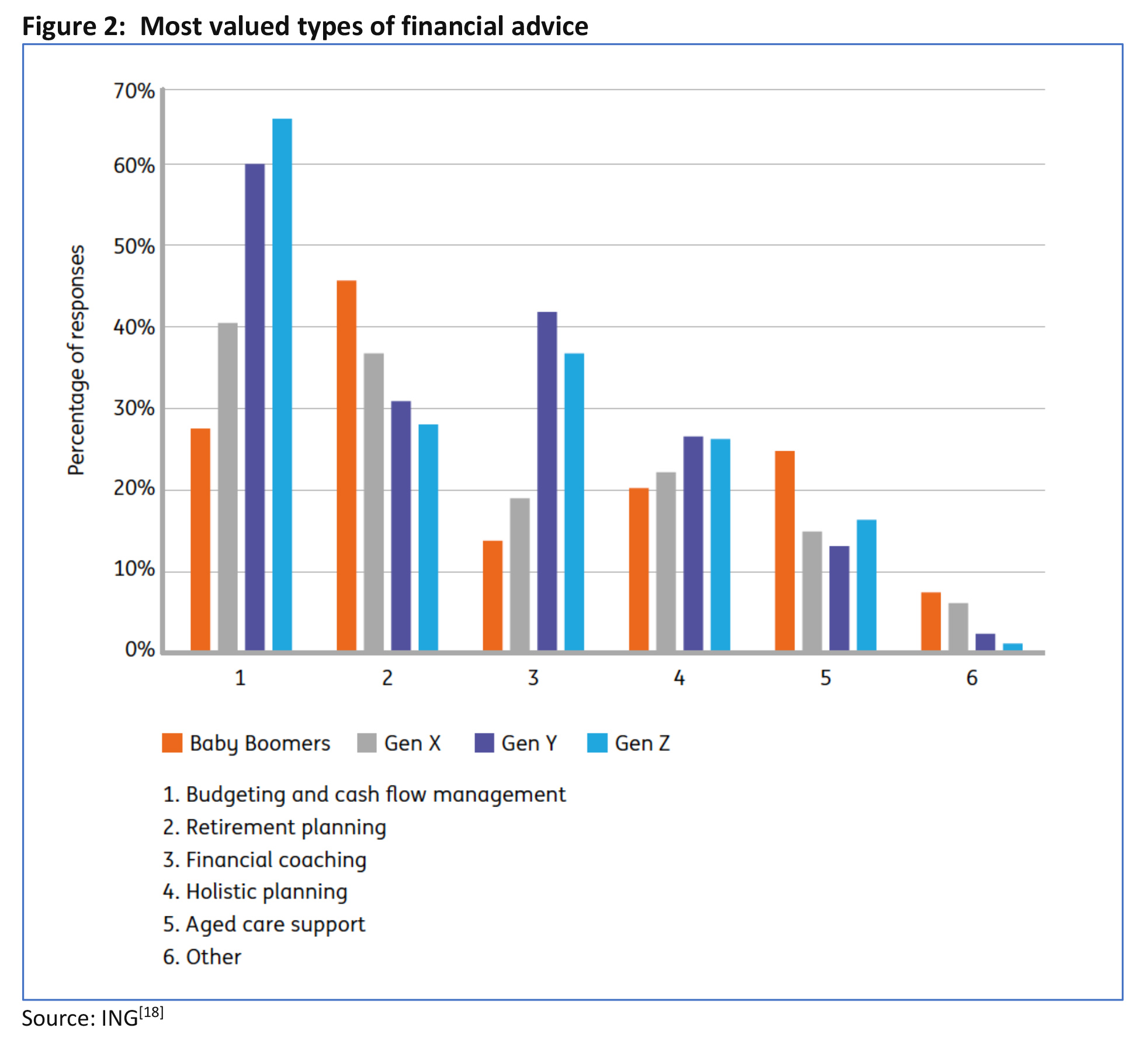

As seen in the chart below, the top financial advice needs for Millennials, according to ING research[18], are around:

- budgeting and cash flow management

- financial coaching and,

- retirement planning.

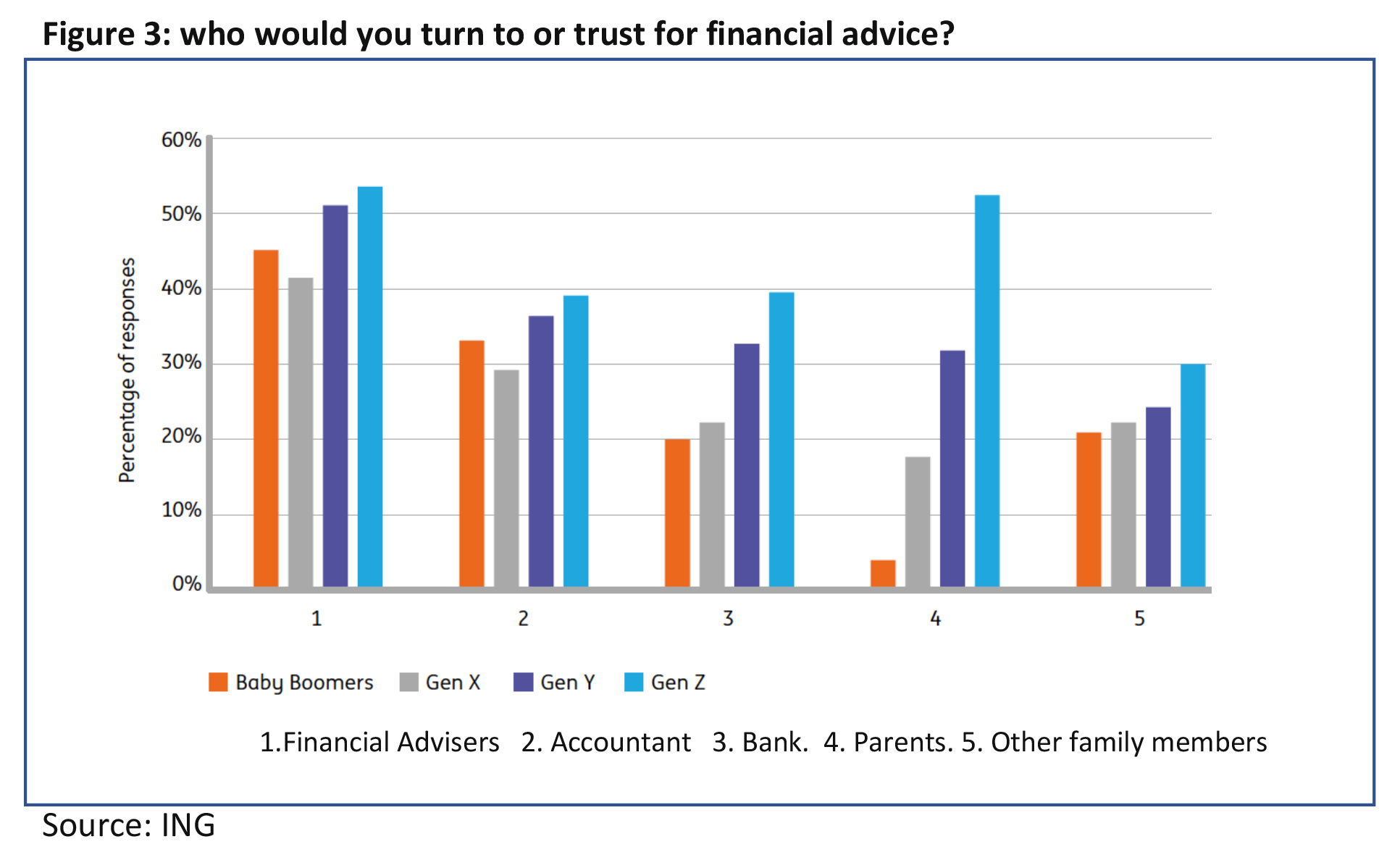

And the preferred source of that financial advice?

Results from the same survey were consistent with earlier ASIC findings[19] that the preferred source of financial advice for Australians of all generations is a qualified financial adviser, with accountants being the next preferred source.

Implications for advisers

Having introduced ourselves to the Millennials, and gained an understanding of their lives, their money behaviours, and their attitude to financial advice, we now turn our attention to the practical implications for financial advisers seeking to engage this increasingly important segment. In particular, advisers must tailor their approach to the unique needs and preferences of Millennials across key parts of their value chain, including areas such as:

- types of advice needed, and fees charged

- communication preferences and marketing approach

- ESG investing.

The types of advice to offer and how to charge

Two key observations stood out from the ING research referred to earlier in this article:

- the demand for help with budgeting and cash flow management advice was strong across all generations

- the demand for financial coaching was particularly strong for younger generations.

Whilst research[20] suggests around half of Australian advisers are offering some sort of cash flow and budgeting assistance to their clients via software, the proportion of advisers who are actively ‘coaching’ their clients around money behaviours is likely to be much lower.

And yet this is not only something clients want, and advisers are qualified to deliver, it is a service for which clients will happily pay. And in the context of Millennials, this means an opportunity to generate fee-based revenue from clients who may not yet have the assets or complex situation to be viable under a traditional advice approach.

If coaching takes the form of specific assistance around budgeting and cash flow, there are a number of options open to advisers. Firms already in this space are experimenting with different pricing models, designed to balance affordability and value with sustainability.

Models being explored across the market include:

- offering short, digital courses on the fundamentals of cash flow and budgeting for a small fee (e.g., the ‘She’s on the Money’ Budgeting and Cash Flow Masterclass)

- tiered models with differentiated fees and services

- month to month subscription services with flexible packages

- upfront set-up fee plus small monthly or annual fee alongside existing advice fees.

And in terms of more general financial coaching, there are a variety of approaches advisers could take to setting fees here, too.

One approach is based on a fixed period of engagement—e.g., $2,500 for a six-month program. Another is a monthly retainer option, or per hour/single session options. Charging on the basis of savings achieved is another option, the value of which is clear to the client.

Group coaching can also be a very effective and efficient way to deliver coaching to fee paying clients.

Importantly, if it is to be offered as a standalone service, it needs to be priced accordingly (not as a loss leader or bundled in with product or asset-based remuneration).

Communication and marketing

Whilst Millennials are tech savvy, and happy to research, shop, and conduct their banking on their mobile device, they still seek human connection when it comes to financial advice. So, whilst AFA research[21] did find that they preferred to receive ‘one to many’ updates from their financial adviser via social media (as opposed to printed or emailed newsletters), they still preferred meeting their adviser in person for one-on-one communication, rather than relying on email (albeit they favoured informal coffee meetings or meetings at their own premises to formal meetings at their advisers’ offices).

Social media preferences are changing

Whilst there is no disputing the importance and effectiveness of social media in reaching advice audiences, advisers need to be aware of the changing social media landscape. As well as the stratospheric rise of Tik Tok (which has unfortunately also helped the stratospheric rise of the ‘finfluencers’), the last couple of years in particular we have also seen Instagram become a more popular channel for serious financial content, with pictures of shoes, cars and holidays now vying with slideshows on topics ranging from household budgeting, to diversifying your income, to ESG investment. According to Netwealth[22], the proportion of advisers using Instagram for their practice more than doubled between 2018 and 2020).

These channels seem to have resonated particularly with a younger, more tech savvy audience and with females, many of whom feel disconnected to a financial advice sector perceived as male dominated.

In Australia, one of the most successful ‘financial influencers’ is the She’s on the Money podcast, produced by financial adviser Victoria Devine of Zella Wealth. Central to the podcast’s success is the engagement Devine drives through the @shesonthemoneyaus Instagram group. The group is private, so followers must request to join, and interactivity is encouraged, both with the host and between other group members, who share their experiences and post questions.

Equally as important in successfully connecting with younger audiences is the language used. With financial services communications once likened to ‘speaking martian[23]’, advisers should remember that younger clients are actually interested in becoming more educated about their finances (more so than older generations, in fact[24]), but they struggle to absorb traditional, jargon filled financial services messages.

Increasingly, financial services providers are turning to gamification, the use of apps, cartoons, and interactive graphics, to improve the effectiveness of their communication (BankWest’s cartoon T’s and C’s is one recent, high-profile example[25]).

A word about ESG

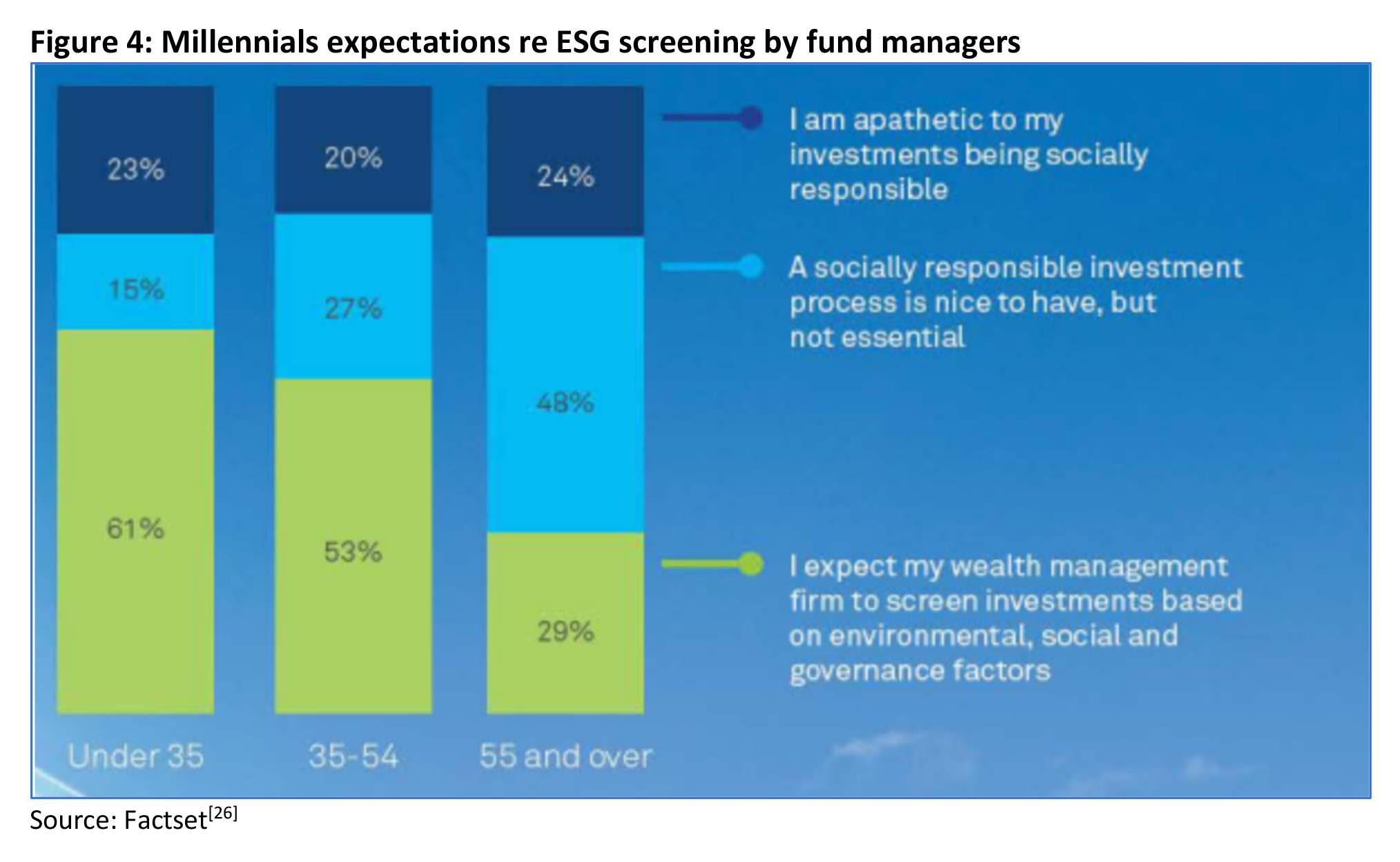

Millennials are the most likely to consider sustainability factors when selecting an investment, with investors under 35 more than twice as likely as those over 55 to expect fund managers to screen investments based on ESG factors (Figure 4).

As advisers engage with more and more millennial clients, they will encounter more interest in sustainable investment philosophies and demand for sustainable investment products.

Advisers should identify whether there are any gaps between increasing demand for sustainable offerings on the part of their clients, and the extent to which these offerings are understood and available for client consideration.

Conclusion

Millennials are the largest cohort of consumers and workers in Australia, who stand to benefit from the largest intergenerational wealth transfer ever seen.

Whilst the financial advice market for Millennials was previously considered unviable – due to their perceived current lack of assets and appetite for advice – many Millennials are recognising their need for expert help in improving their money behaviours and financial knowledge and are preferring to seek that help from financial advisers.

Their demand for financial coaching and help with budgeting and cash flow management in particular, opens up an exciting opportunity for advisers to engage clients much earlier in their financial journey, and allows firms to charge stand-alone advice fees more confidently, to clients who are more willing to pay them.

Advisers seeking to engage this segment need to be aware of the many characteristics that differentiate Millennials from older consumers, and tailor their approach accordingly.

———-

References: