Weekly economic and market update – week ending 30 July, 2021

Investment markets and key developments over the past week

Despite some concerns about Chinese regulatory tightening early in the week and ongoing worries about coronavirus US and European shares rose over the last week helped by strong earnings results in the US and strong data in Europe. Japanese and Chinese shares fell though with regulatory issues weighing on the latter. The positive US lead helped push the Australian share market up to a new high despite an extension to the NSW lockdown. Bond yields mostly fell, helped by benign June quarter inflation in Australia. Oil and metal prices rose but the iron ore price fell. The $A rose as the $US fell.

Shares remain at risk of a short-term correction or volatility as coronavirus cases rise globally, the inflation scare continues and as we come into seasonally weaker months, but surging company profits in the US and lower bond yields are providing support and in any case the rising trend in shares is likely to remain in place into next year as rising vaccination rates allow economic recovery to continue as interest rates & bond yields remain low.

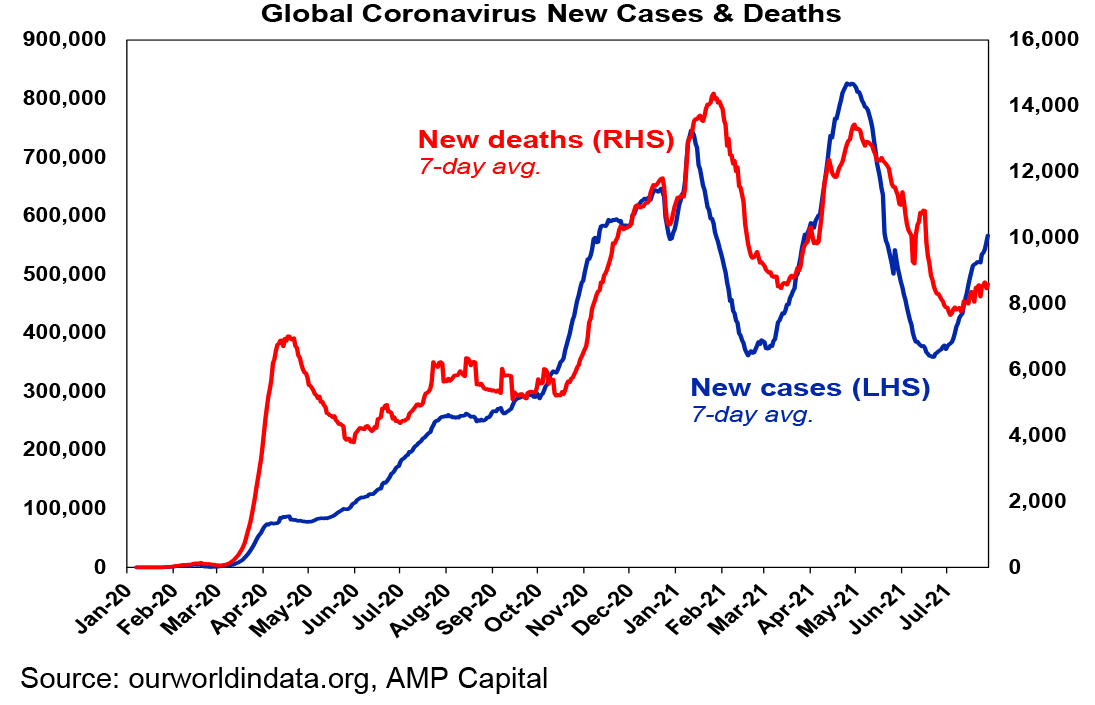

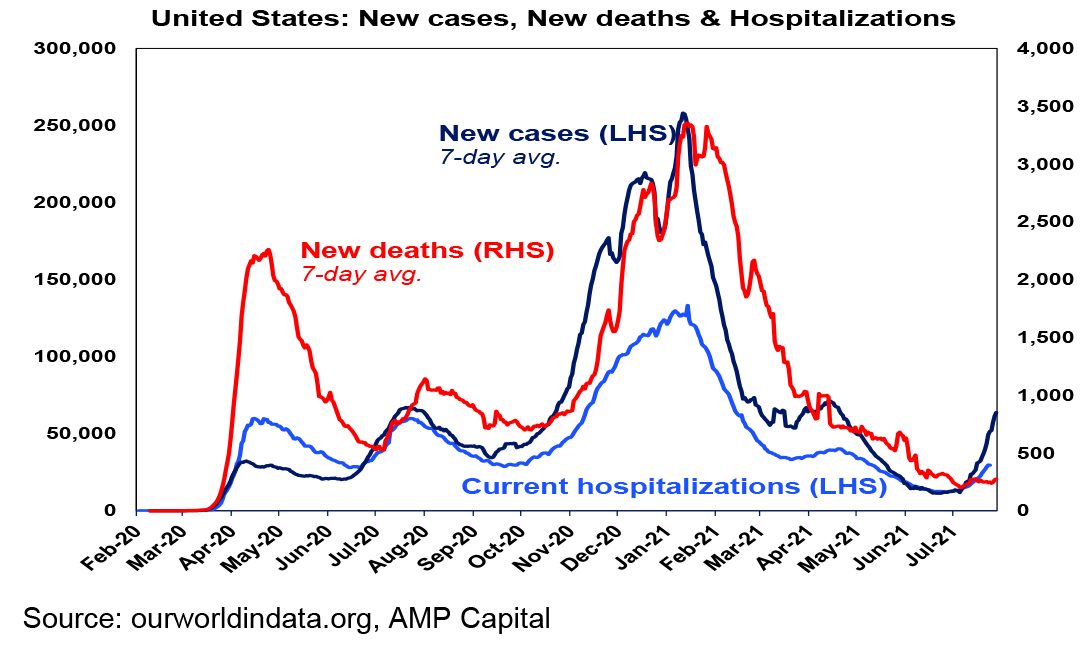

The resurgence of coronavirus in the US is now becoming more of an issue with new cases and hospitalisations surging in many lowly vaccinated states, eg hospital admissions in Florida are now surpassing the peak in January, Arkansas has declared a public health emergency with its hospitals overwhelmed and Texas is running low on ICU beds. This is starting to see a return of restrictions mainly in terms of mask mandates along with delayed returns to the office along with increasing vaccination mandates for workers. The Delta variant is now accounting for more than 80% of new US cases. Even China is having problems with the Delta variant.

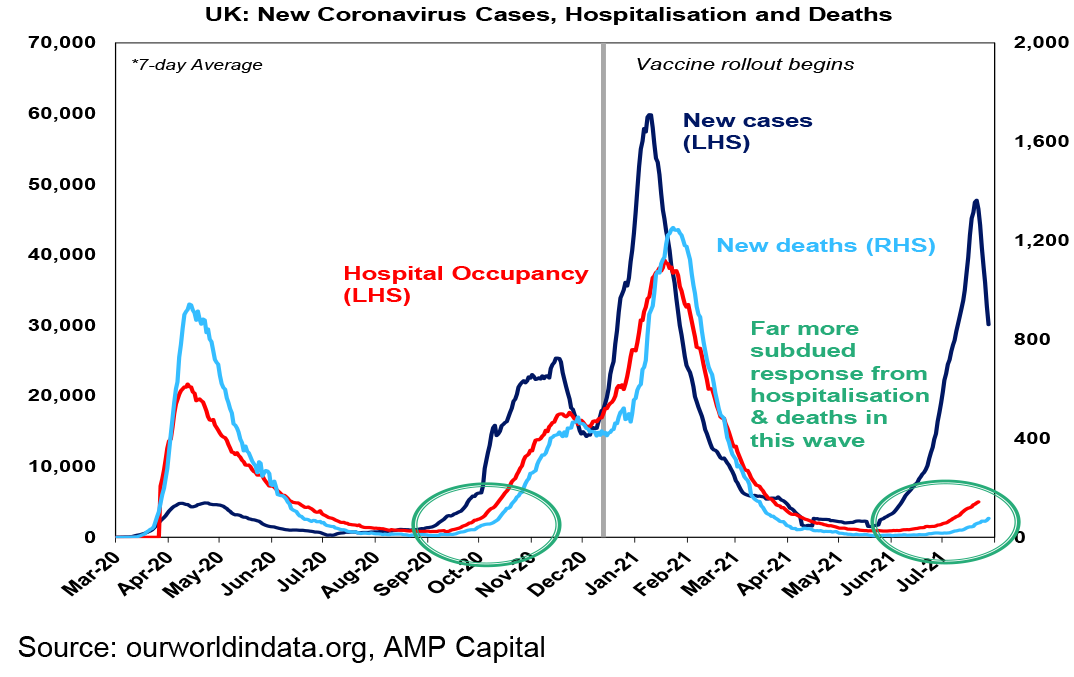

However, the UK which remains an important test case given its relatively high level of vaccination has continued to see hospitalisations and deaths remain far more subdued in the latest wave of new cases providing confirmation the vaccines are highly (90% plus) effective in preventing the need for hospitalisation and death. It’s the same story in Israel and Europe. And deaths remain subdued in the US. The UK has also seen a surprising fall in new cases. A decline in testing may explain some but not all of this. Maybe vaccines are more effective than expected in preventing spread? Or maybe it’s just noise? Time will tell.

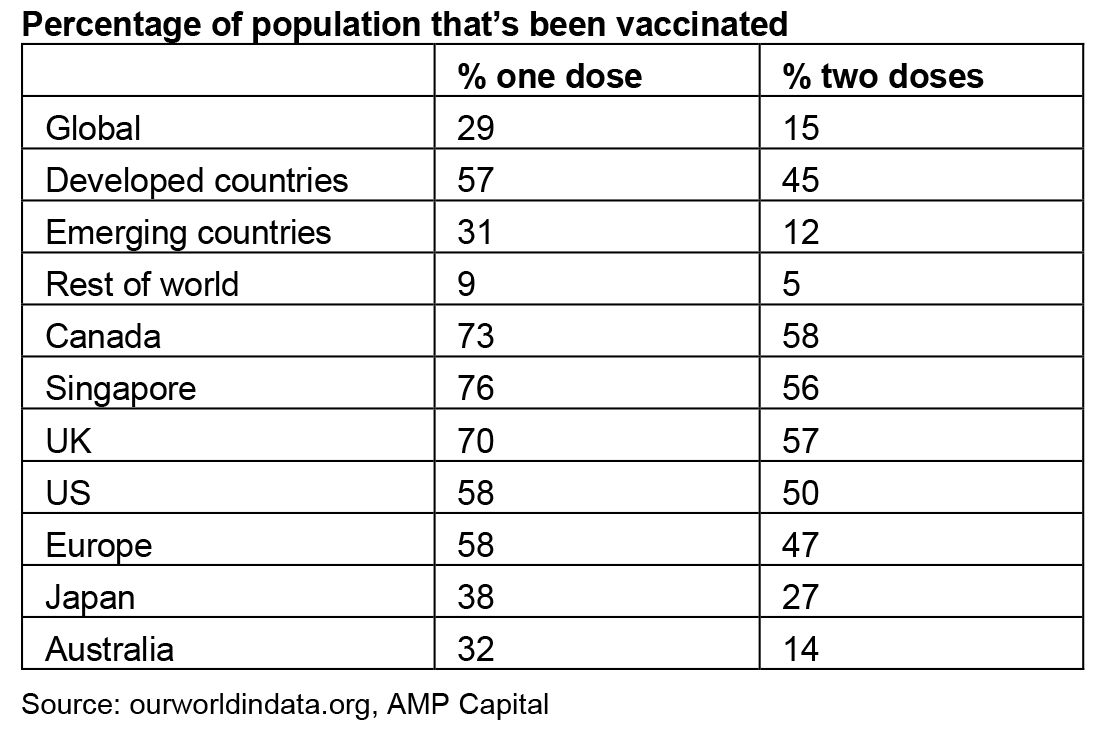

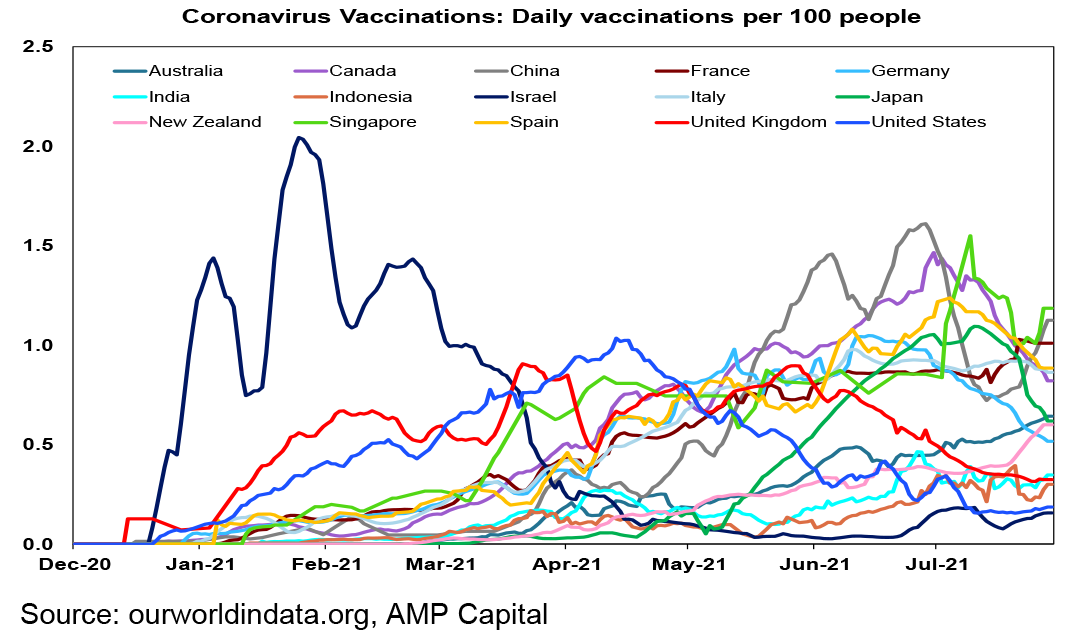

On the latest count 29% of people globally and 57% in developed countries have had at least one dose of vaccine.

Australia’s vaccination rate – see the thick line in the next chart – is continuing to accelerate reaching 1.14 million doses over the last week reflecting increased vaccine availability and a sharp fall in vaccine hesitancy in the face of the latest outbreaks and lockdowns. According to a Melbourne Institute Survey the proportion of the adult population that is unwilling to get vaccinated has fallen to 11.8% (just 7.6% in NSW) from 18% at the end of May. The pace of vaccination is also now reportedly rising again in previously vaccine resistant US states in the face of rising cases.

Herd immunity with the Delta variant is likely to require 80% or so of the population fully vaccinated. If this is achieved with 95% or so of at risk older people being fully vaccinated offsetting lower vaccination rates for children then Australia should be able to avoid the need for snap lockdowns and tolerate the circulation of coronavirus in the community without undue pressure on the health care system with deaths being kept to a minimum. At the rate 1.14 million doses a week Australia should be able to reach 60% vaccinated in December and 80% in March. If it rises to 1.5 million doses a week consistent with rising supply, we should be able to reach 60% in November and 80% by around year end. In the meantime, we have little choice but to continue with restrictions and snap lockdowns to limit pressure on the hospital system and prevent deaths following outbreaks. But the key is that the lockdowns be implemented hard and early to ensure that they are short with minimal economic impact.

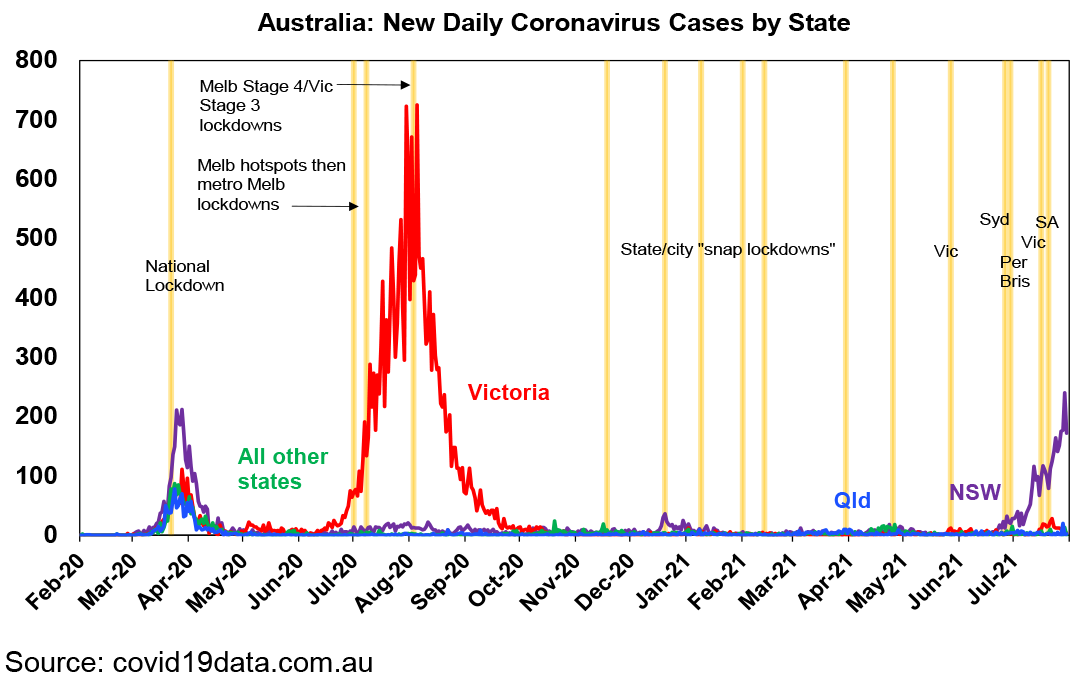

On the lockdown front in Australia there has been good news and bad over the last week. The good news is that the lockdowns in Victoria and South Australia have worked in controlling new cases and have now ended demonstrating yet again that lockdowns that start hard and early (when new cases are running at around 1 to 10 a day) still work quickly against the Delta variant even in the absence of high levels of vaccination and so can be short with minimal damage to the economy. This has been and rightly remains the strategy in most states.

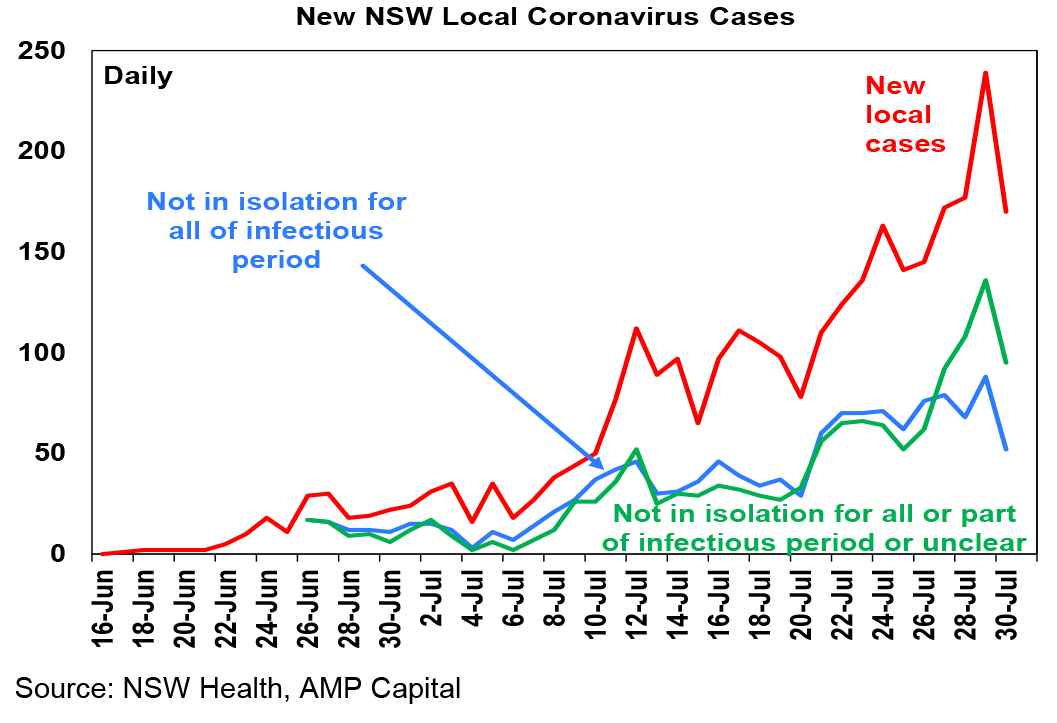

The bad news is that new daily local cases and new local cases that are infectious in the community (however defined) rose to a new high in NSW in the past week and its lockdown has been extended for another four weeks and tightened in some hotspot areas. Reported cases fell on Friday but they are known to be volatile and there are too many cases infectious in the community to read much into that. Unfortunately, NSW is continuing to pay the price for not going hard and early enough when it started its lockdown (although I admit its easy to say that in hindsight – but it’s worth remembering next time when a state announces a snap lockdown with just a few cases).

Putting that aside the message from Victoria and SA for NSW is that lockdowns still work against Delta – it’s just that having started later in terms of the flow of new cases and easier it’s now going to take longer in NSW to reach the objective of new cases that are infectious in the community being close to zero. Some modelling is pointing to September and of course the faster we can move on vaccines the more that will help too.

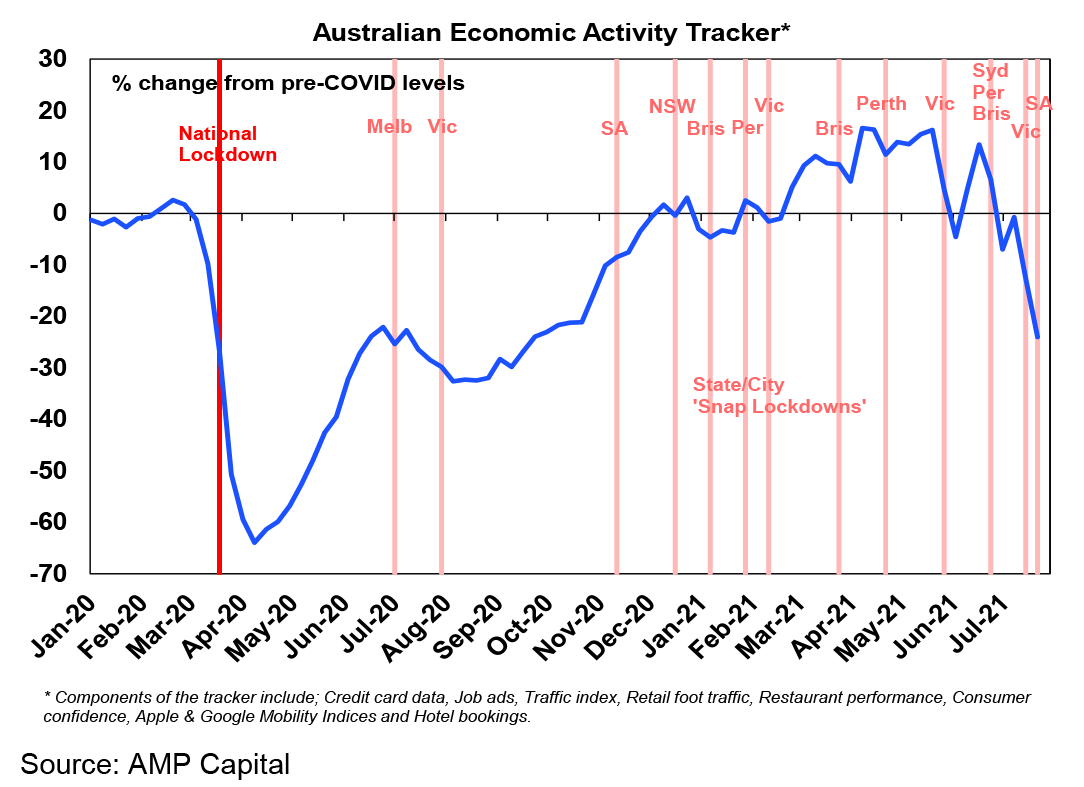

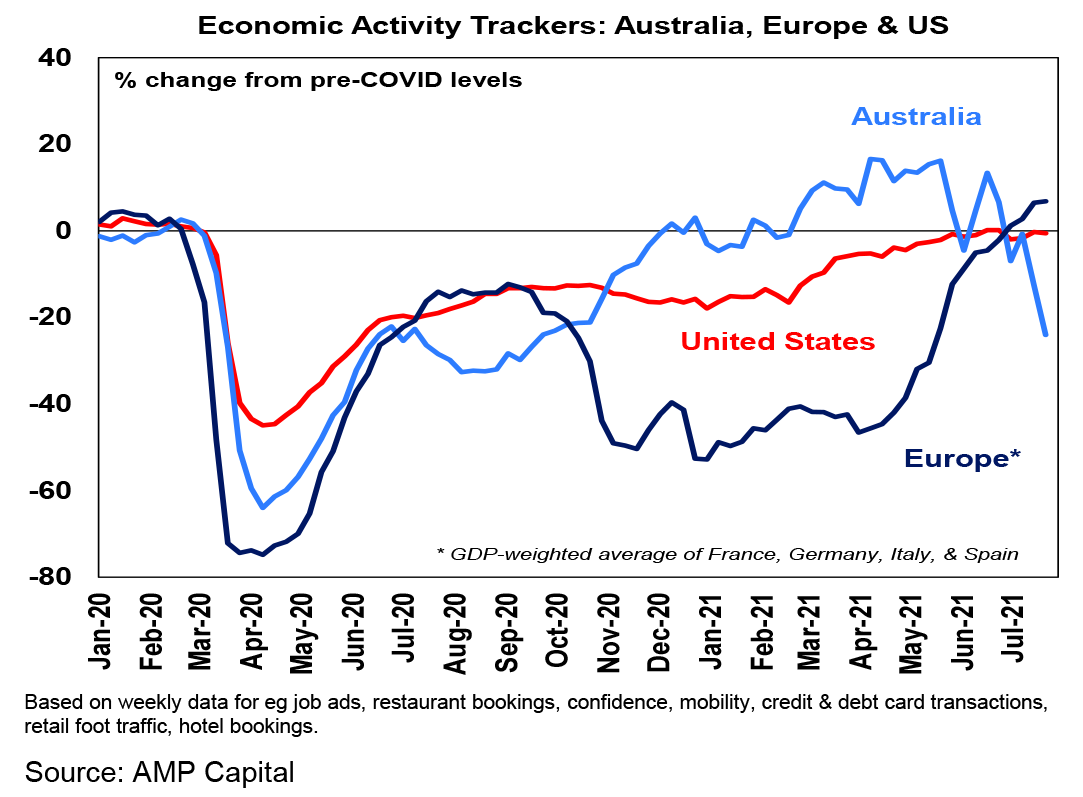

The economic impact of the lockdowns continues to be evident in another fall in our Australian Economic Activity Tracker over the last week reflecting falls in all of its components. With NSW likely having fallen about as far as it’s going to go and Victoria and South Australia reopening it may soon bottom out assuming no further problems in other states.

With the NSW lockdown now extended to the end of August, the total direct cost of the lockdowns since end May has now been pushed to around $14bn and with less time to now rebound at the end of the current quarter. The further boost to government support costing about $1bn a week – with bigger payments to NSW businesses contingent on them maintaining their workforces and payments to workers who have seen their hours of work reduced by at 20 hours a week equivalent to what they would have received from JobKeeper in the middle of last year – will help but will mainly serve to enable the economy bounce back quickly. Even though other states are likely to keep growing (helped by the ending of the Victorian and South Australian lockdowns) GDP is now expected to contract by around -2% or so this quarter. That said providing the lockdown ends this quarter (and the Victorian and SA experience highlight that lockdowns do still work against the Delta variant) we should see a strong rebound in the economy in the December quarter aided by pent up demand from another round of government support payments. This will leave growth through the course of 2021 at around 3% year on year, albeit down from our forecast prior to all the latest outbreaks of 4.8%yoy. Assuming only short snap lockdowns from next quarter and then the attainment of herd immunity through increased vaccination early next year allowing an end to lockdowns through 2022, then 2022 growth is likely to be about 1% stronger than previously expected at around 4% compensating for weaker growth this year. But that’s a long way off!

In the meantime, the set back to growth this quarter is likely to push unemployment back up to around 5.25-5.5% in August and September which will keep the RBA cautious and likely to delay the tapering of its bond buying program. Of course, the longer the lockdown drags on the great the risk of the December quarter GDP contracting too. But at this stage we continue to put the risk of a fall back into recession at just 25%. Fortunately, enhanced government support has helped offset the increased risk posed by the extension of the lockdown.

Our US Economic Activity Tracker remains little changed since May. Our European Tracker is pushing further above pre coronavirus levels. Its Europe’s turn to shine!

How big a threat is China’s regulatory crackdown? For some time, China has been cracking down hard on its tech stocks. This then moved on to private education (or tutoring) and property companies with talk it may also move on to medical services. Global investors became concerned on the grounds that it will depress the earnings of Chinese companies in which they are invested, and it also fed long held concerns that western countries might start ramping up the regulation of their own technology companies. China’s moves are consistent with a desire to ease the financial burden on lower and middle income households and to support the three child policy. They tap into an element of resentment towards mega rich moguls. They are also consistent with greater Government involvement and control in the Chinese economy which has been evident under the current leadership. But they don’t look designed to threaten long term growth and industrialisation in China. The long term nature of China’s social welfare goals indicate that the regulatory crackdown could continue for a while yet, but Chinese authorities have indicated they are aware of investors’ concerns and have moved to calm market fears, so it may take a short term pause.

More US infrastructure stimulus on the way but should we worry about the debt ceiling which expires on 1 August? Our assessment remains that argy bargy over the debt ceiling could cause investor nervousness and contribute to a correction but it’s unlikely to derail shares for long. Treasury can use various reserves to keep going into mid-September after which it will default on payments unless the ceiling is raised. As we saw in 2011 and 2013 there could be brinkmanship, but such disruptions are unpopular with voters and the Republicans are not as anti-debt as they used to be so 10 Republican senators can probably be found to get the 60 votes needed to raise the ceiling. If not, the Democrats can include it in their upcoming budget reconciliation bill and pass it with a simple majority. This will be necessary to implement the remaining $US3.5 trillion in President Biden’s American Jobs and Families Plans into law, assuming the $US550bn bipartisan deal covering traditional infrastructure is passed into law, which looks likely.

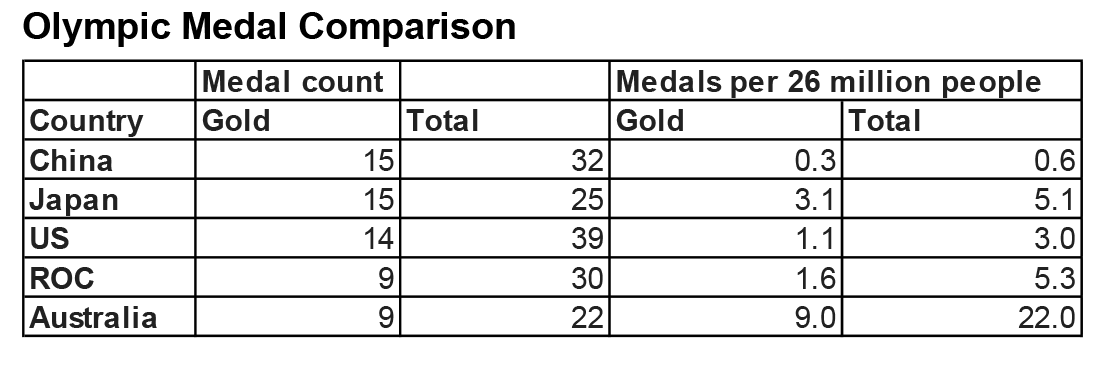

Australia is off to a good start at the Olympics – population adjusted it looks even better compared to the top 4!

Major global economic events and implications

US June quarter GDP rose by a strong but less than expected 1.6%qoq, which took it above its pre coronavirus high. Consumption and investment were strong but detractions from housing and inventory will likely reverse going forward. While new and pending home sales fell home prices continue to surge, durable goods orders remain in a strong rising trend and consumer confidence remained strong.

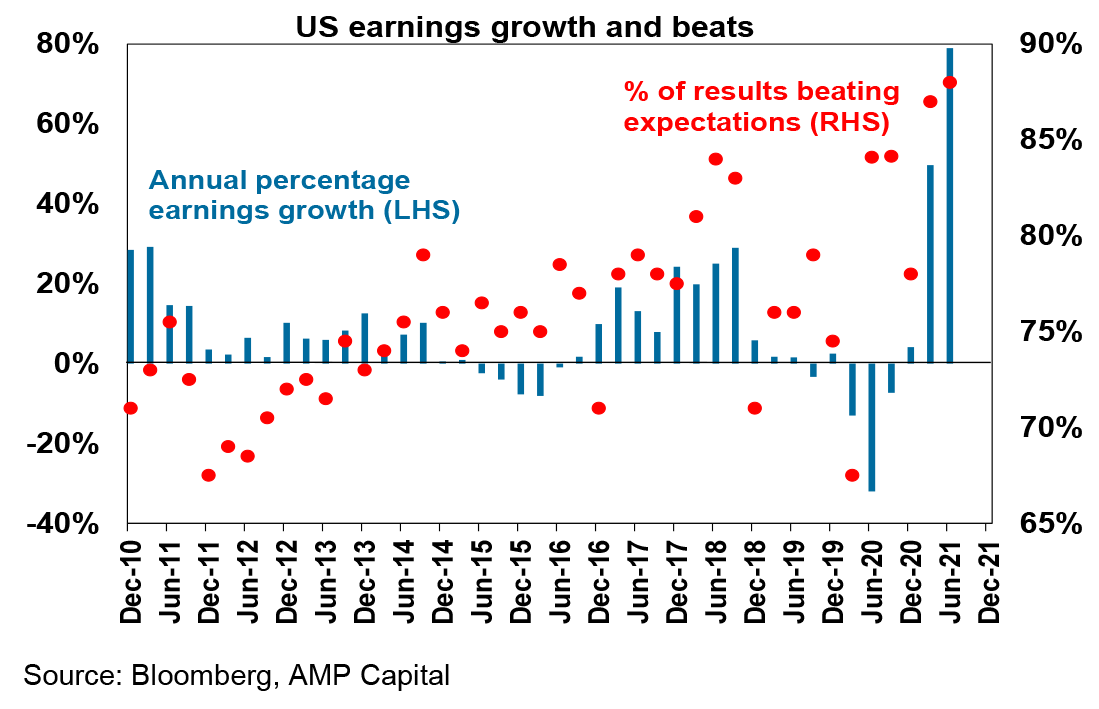

So far, the US June quarter earnings reporting season is now 55% done with a huge 88% of results so far beating expectations (compared to a norm of 76%), 84% beating on revenue and consensus earnings expectations for the quarter have been revised up from 62%yoy at the start of July to now 79% with upside surprise concentrated in cyclical sectors. Given the rebound in various macro variables we remain of the view that this could end up near +90%. The strength in earnings partly explains the ongoing resilience of US shares lately.

Meanwhile the Fed is still only gradually moving towards tapering. The Fed and Fed Chair Powell are more bullish on growth and see the economy as having made progress towards the Fed’s goals but it’s still seen as “some way away” from the “substantial progress” needed to taper. Our assessment remains that a taper will be announced later this year to start early next year.

Eurozone economic confidence rose to a record high in July propelled by reopening.

Japans business conditions PMIs fell further in July reflecting the latest coronavirus state of emergency. However, June jobs and industrial production data was stronger than expected.

Australian economic events and implications

Australian CPI inflation spiked in the June quarter pretty much as expected to 3.8%yoy largely reflecting the unwinding of free childcare and last year’s collapse in petrol prices. Abstracting from pandemic driven distortions underlying inflation remained subdued at 0.5%qoq or 1.6%yoy. As some of the various distortions drop out, we expect headline inflation to fall back to around underlying inflation which in turn will likely gradually rise towards 2% by the end of next year. Meanwhile producer price inflation rose but only to 2.2%yoy, which is well below that seen in other countries. There is nothing here to justify the RBA bringing forward rate hikes and if anything, the risk is that the Sydney lockdown delays progress towards full employment and hence the 3% wages growth necessary for inflation to be sustained in the 2 to 3% target range.

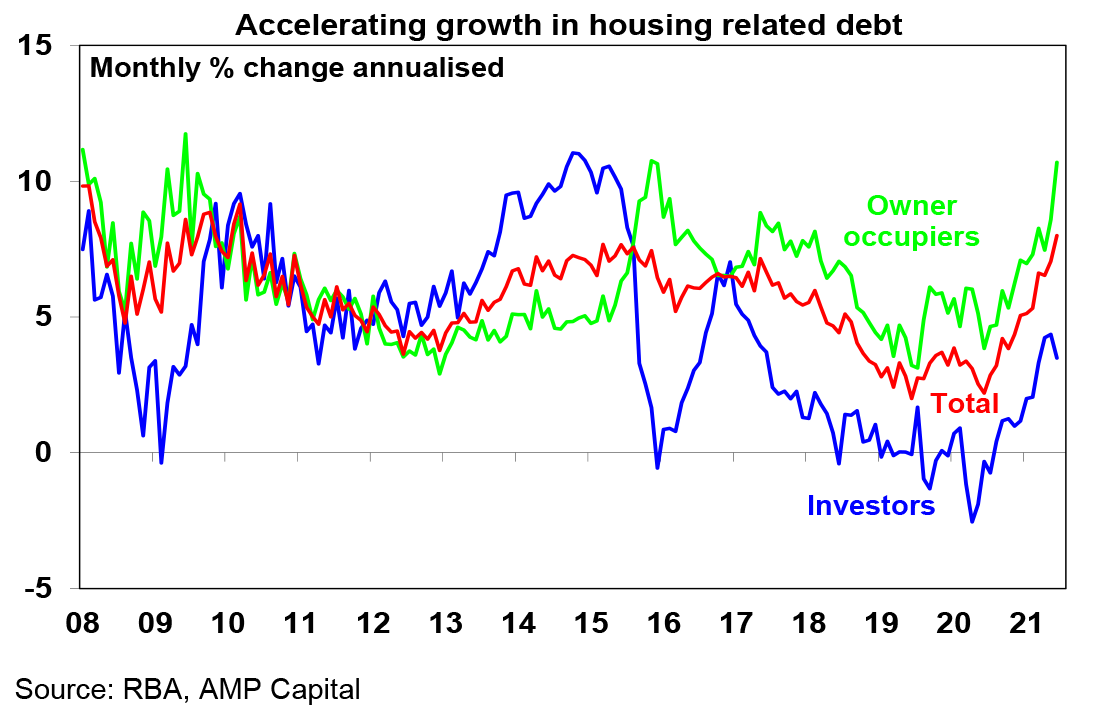

Credit data showed a further acceleration in housing credit reflecting record levels of housing finance. While investor credit growth slowed a bit in June, owner occupier credit growth is booming and total housing credit growth is now running above the levels when APRA started to tighten lending standards in late 2014 and we expect the same to occur this time around, although APRA may wait for the dust to settle from the Sydney lockdown.

Meanwhile a surge in export prices means another surge in the terms of trade in the June quarter & a boost to national income.

What to watch over the next week?

In the US expect the ISM manufacturing and services conditions indexes (due Monday and Wednesday) to remain strong although they may fall back a bit from around the 60 level and July jobs data (Friday) to show payrolls up by around 900,000 and unemployment down to 5.7% from 5.9%. And US June quarter company profit results will continue to flow.

Japanese data for household spending will be released Friday.

China’s Caixin business conditions PMIs for July will be released on Monday and Tuesday.

In Australia, the main focus is likely to be on the RBA (Tuesday) which is expected to be very dovish. With the ongoing NSW lockdown now set to send the economy backwards in the September quarter and heightened uncertainty around when it will end the RBA is expected to revise down its growth forecasts for this year and revise up its unemployment forecasts. In fact, the RBA’s forecasts to be published in its SOMP on Friday may end up looking nearer its “Downside” scenario for this year but if there is a good rebound it could end up with the “Upside” scenario for next year. But of course, it’s the near term that the RBA will focus on and the dramatic change in the outlook for the economy for the current half since the last meeting is likely to see the RBA delay the step down in its bond buying from September until early next year when the outlook improves again. It’s also likely to state that it stands ready to do whatever it can to help the economy. The RBA may also consider shifting the target bond for the 0.1% bond yield target out to the November 2024 bond. And its likely to reiterate that under its central scenario the conditions for a rate hike will not be met until 2024.

On the data front in Australia, CoreLogic data (Monday) is expected to show another strong 1.6% gain in home prices for July led by Sydney despite its lockdown and Brisbane. In other data, expect a 2% bounce in June building approvals after a sharp fall in May and flat housing finance at record levels (both Tuesday), June retail sales data (Wednesday) to confirm a -1.8% decline but show a 0.7% rise in real terms for the June quarter and trade data for July to show a near record surplus of $9.5bn.

The Australian June half profit reporting season will start to get under way. Consensus earnings per share growth expectations are for a 49% rise in earnings for 2020-21 and a 56% rise in dividends. The resources sector is expected to see a near doubling in profits (as evident in Rio’s already released result) followed by 58% growth in bank earnings and a 47% gain in media sector profits. Telcos, general industrials and utilities are likely to see a decline in earnings. Outlook statements are likely to be cautious though given the uncertainty posed by recent coronavirus outbreaks and lockdowns, particularly that in NSW. Only 5 major companies will release results in the next week though including GUD and Resmed.

Outlook for investment markets

Shares remain vulnerable to a short-term correction with possible triggers being the upswing in global coronavirus cases, the inflation scare and US taper talk and geopolitical risks. But looking through the inevitable short-term noise, the combination of improving global growth and earnings helped by more fiscal stimulus, vaccines allowing reopening once herd immunity is reached and still low interest rates augurs well for shares over the next 12 months.

Expect the rising trend in bond yields to resume as it becomes clear the global recovery is continuing resulting in capital losses and poor returns from bonds over the next 12 months.

Unlisted commercial property may still see some weakness in retail and office returns but industrial is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home prices look likely to rise 15 to 20% this year before slowing to around 5% next year, being boosted by ultra-low mortgage rates, economic recovery and FOMO, but expect a progressive slowing in the pace of gains as poor affordability impacts, government home buyer incentives are cut back, fixed mortgage rates rise, macro prudential tightening kicks in and immigration remains down relative to normal. The lockdowns have increased short term uncertainty though.

Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%. We remain of the view that the RBA won’t start raising rates until 2023.

Although the $A could pull back further in response to the latest coronavirus scare and the threat it poses to global and Australian growth, a rising trend is likely to remain over the next 12 months helped by strong commodity prices and a cyclical decline in the US dollar, probably taking the $A up to around $US0.85 over the next 12 months.

By Shane Oliver