Weekly economic and market update – week ending 10 September, 2021

Investment markets and key developments over the past week

Global shares were mixed over the last week. US and European shares fell on concerns about the growth outlook and central banks reducing stimulus, but Japanese shares continued to rise on hopes for more fiscal stimulus after PM Suga announced he would step down and Chinese shares rose. Australian shares fell on the back of the weak global lead, lower iron ore prices and concerns about the lockdowns led by falls in resources, property and consumer staple shares. Bond yields rose slightly in Australia but fell elsewhere. Oil and iron ore prices fell but metals rose. The $A fell as the $US rose.

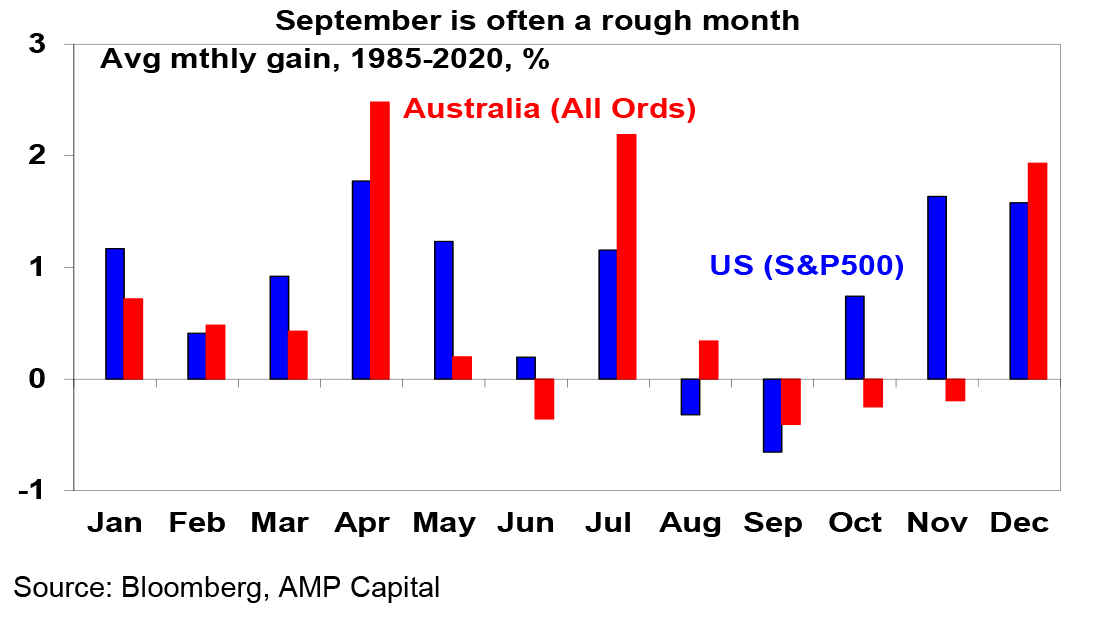

The curse of September? While shares have been remarkably strong since their March 2020 lows, its interesting to note that US and Australian shares both had falls last September. Over the last 35 years September has averaged the weakest month of the year for both share markets. There are a bunch of risks for the next month or so with: threats from coronavirus – notably around the reopening in Australia; central banks slowing stimulus; the US debt ceiling; the passage of Biden’s remaining stimulus and tax hikes; and global supply constraints and inflation. These could all add to current fears that growth has peaked resulting in a correction. Key to watch technically will be whether the US share market continues to find support around its 50-day moving average. However, the likely continuation of the economic recovery beyond near term interruptions, vaccines ultimately allowing a more sustained reopening and tight monetary policy being a long way off augurs well for shares over the next 12 months.

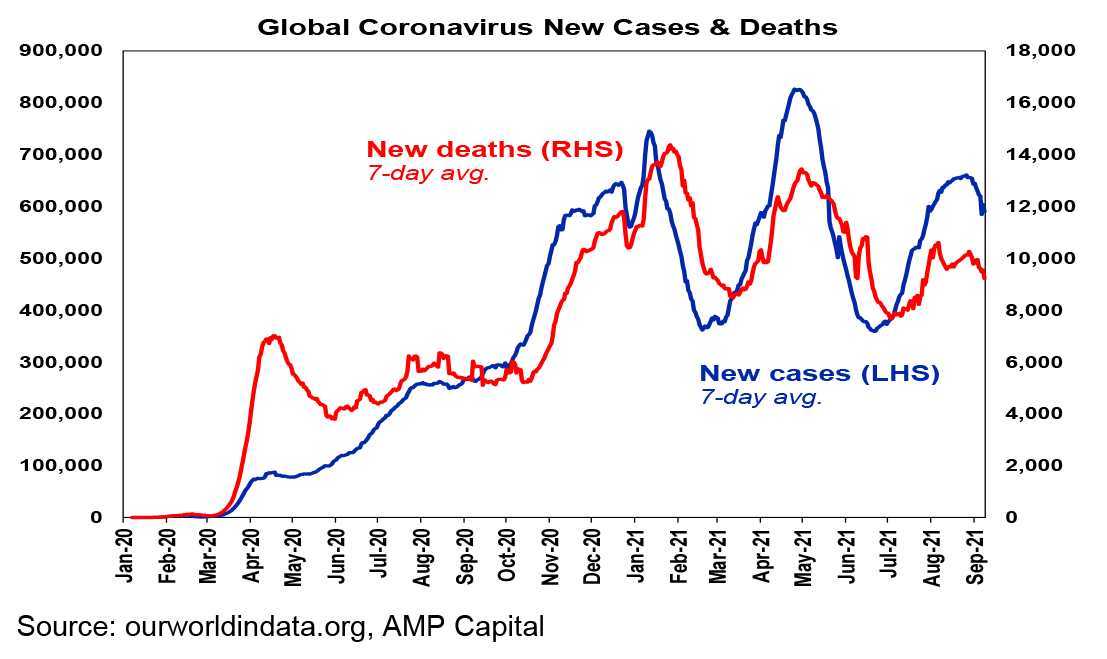

New global coronavirus cases have now clearly rolled over again, with Asia continuing to decline, South America remaining in a downtrend and Europe and the US stabilising. New Zealand with a sharp decline in new cases also appears to be showing, along with China, that its possible to bring Delta outbreaks under control with lockdowns (albeit its lockdown has been much tighter than that in NSW).

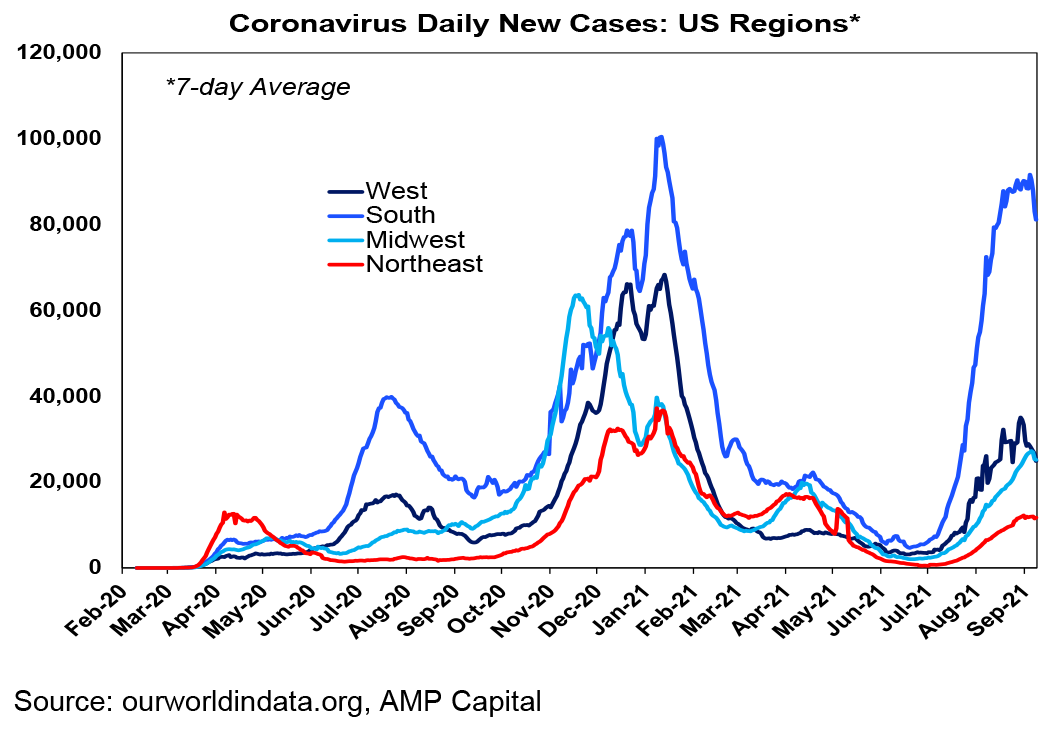

The US “pandemic of the unvaccinated” appears to be stabilising with new cases in the lowly vaccinated South starting to roll over. Helped by higher vaccination rates, hospitalisations remain well below previous waves in the Northeast, West and Midwest regions.

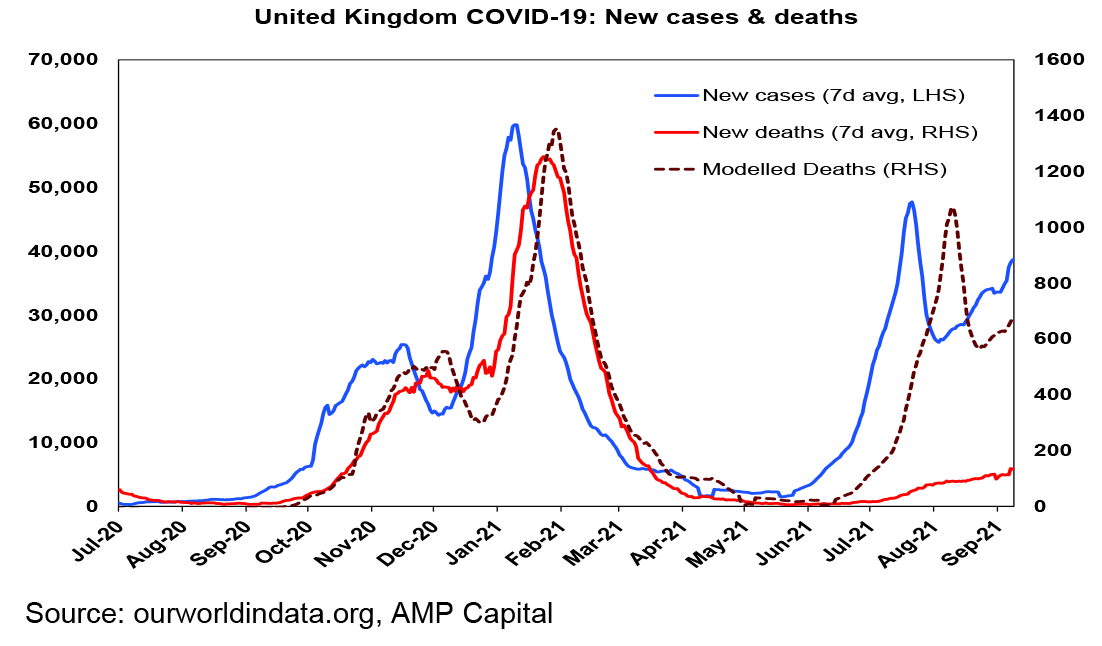

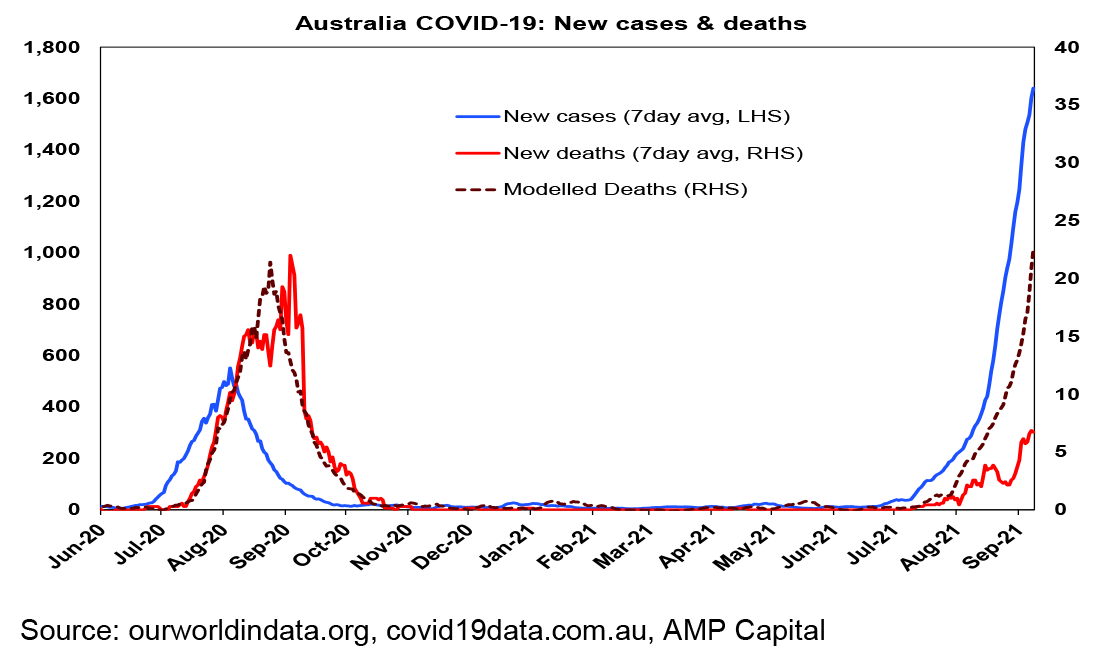

New cases have increased in the UK and Canada but are stable in Europe (after rising since July). However, hospitalisations and deaths remain relatively low compared to previous waves in the UK, Europe and Canada – consistent with vaccines being only 60-80% effective in preventing infection but highly effective at around 90% in preventing serious illness. For example, deaths in the UK (the red line in the next chart) are running well below the level predicted on the basis of the previous wave (dashed line). Given the experience with Israel that saw declining vaccine efficacy after about six months, combined with 30% to 45% still being unvaccinated, the main risk in Europe, the UK and North America may come in winter unless booster shots are sped up for those who were vaccinated earlier this year.

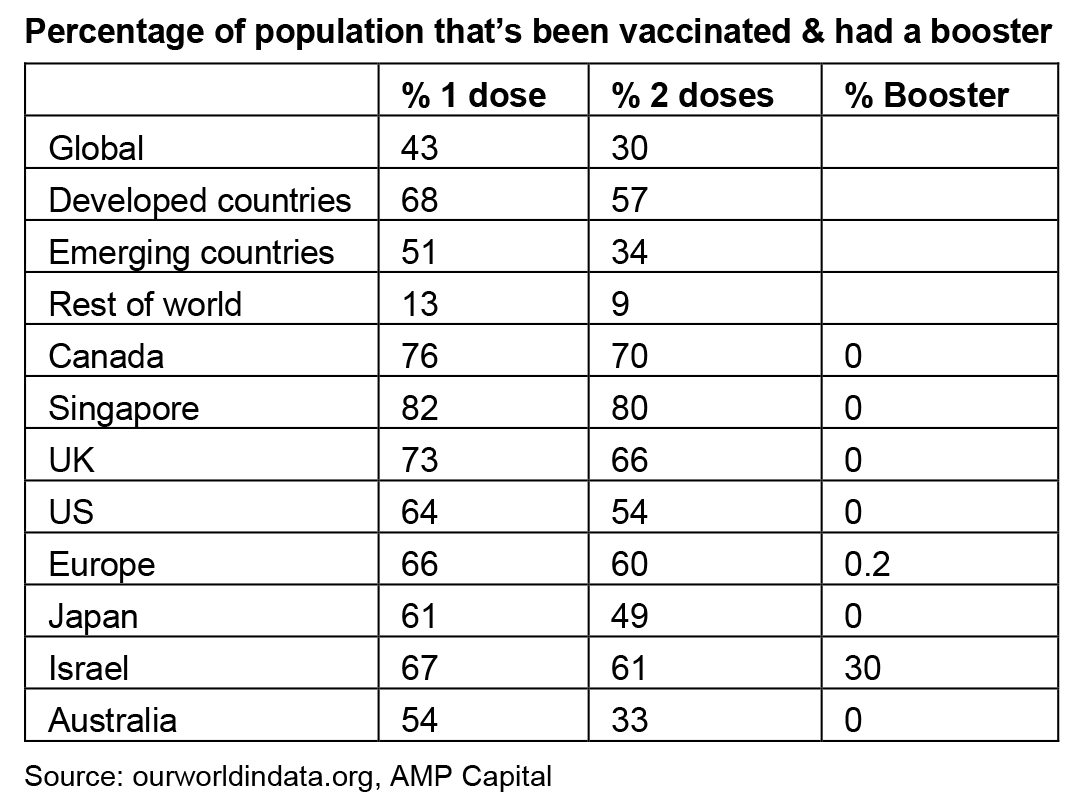

Vaccinations are continuing to ramp up globally – but the low level of vaccinations in less developed countries is a concern. 43% of people globally and 68% in developed countries have now had at least one dose of vaccine. But its only 13% in less developed countries.

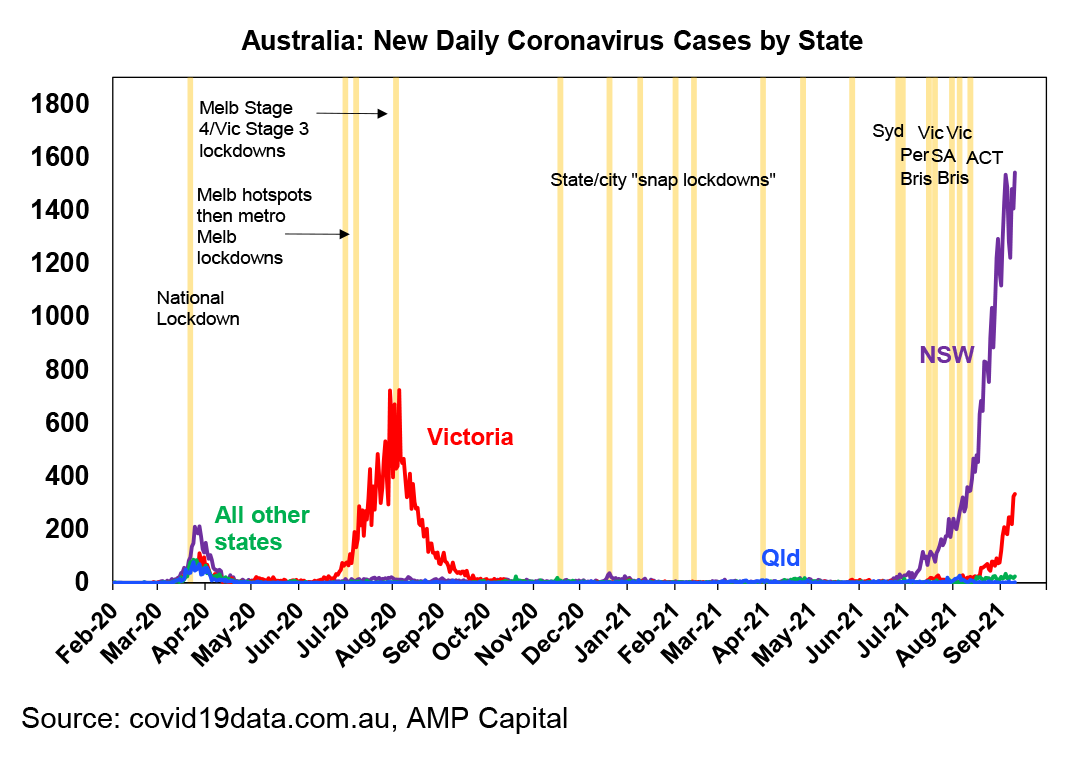

The flow of new cases has been mixed over the last week in Australia. While Victoria has seen a continuing spike in new cases, NSW saw a marginal new high but it may be starting to stabilise with its effective reproduction rate estimated to have fallen to 1.

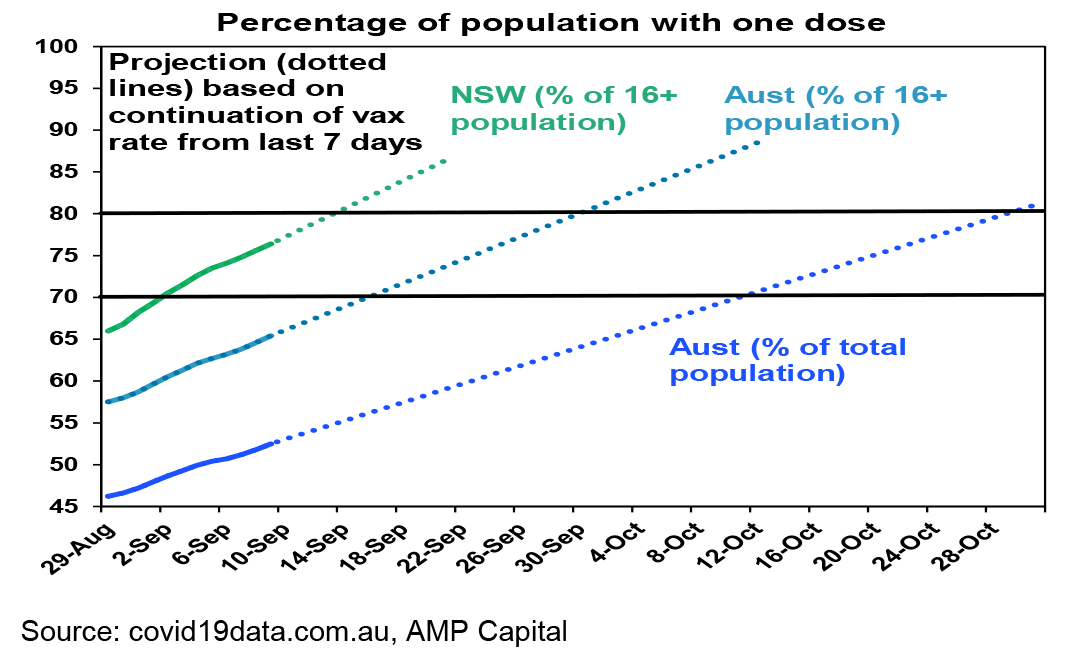

Australia now has around 54% of its whole population with one dose. The past week has seen the pace of vaccination slow slightly to 1.82 million people a week from 1.95 million just over a week ago. This may reflect Australia reaching vaccination levels that saw the pace slow in the UK and US. But it’s more likely reflective of supply which is expected to pick up again into month end, which combined with confirmation that only the fully vaccinated will participate in NSW’s reopening next month will likely see the pace of vaccination pick up again. The next chart shows a projection of when NSW and Australia will meet vaccination targets for one dose based on an extrapolation of the average daily vaccination rates seen in the last 7 days. To this can be added the average lag between 1st and 2nd doses to get a rough idea when the double vaccination targets will be met. This is now running at around 45 days or 6.5 weeks.

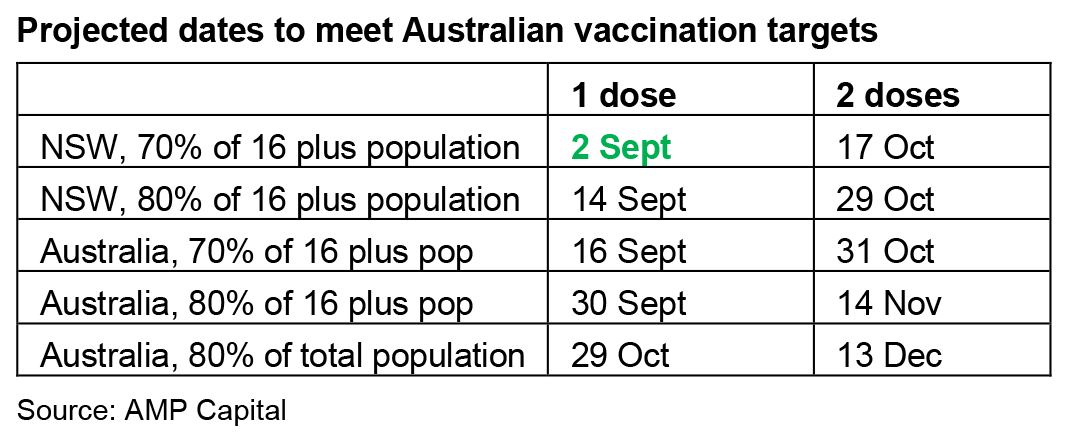

On the basis of this projection the following table shows roughly when key double dose vaccination target dates will be met. Victoria is running around 15 days behind NSW in terms of when it will meet its vaccination targets.

So on this basis NSW is on track to start reopening in the second half of October and Australia is on track to follow in the first half of November. Consistent with this NSW has announced a reopening roadmap that allows the fully vaccinated to enjoy greater freedoms in terms of gathering, restaurants, shops, hairdressing, gyms, theatres, trips in NSW etc, providing distancing requirements are met from the first Monday after the 70% fully vaccinated target is met.

As we have noted in previous Weekly Market Updates, because of the greater transmissibility of the Delta variant, indications that the vaccines only provide 60 to 80% protection against infection and the reality that the national objective of 80% of adults will still leave 36% of the population unvaccinated and at risk there is a strong argument to aim for a higher vaccination rate of 80% or more of the whole population which Singapore has reached. Vaccine hesitancy amongst 10% or so of adults may make this difficult to achieve but the combination of vaccinating 12 to 15 year olds and the requirement that only the vaccinated will participate in the initial reopening (as already declared by NSW) may make this achievable.

Meanwhile, the vaccination of older people appears to be continuing to help keep the level of hospitalisations and deaths more subdued in this wave than was the case in the Victorian wave last year. Deaths (the red line in the next chart) are running around one third below the level predicted on the basis of the previous wave (dashed line).

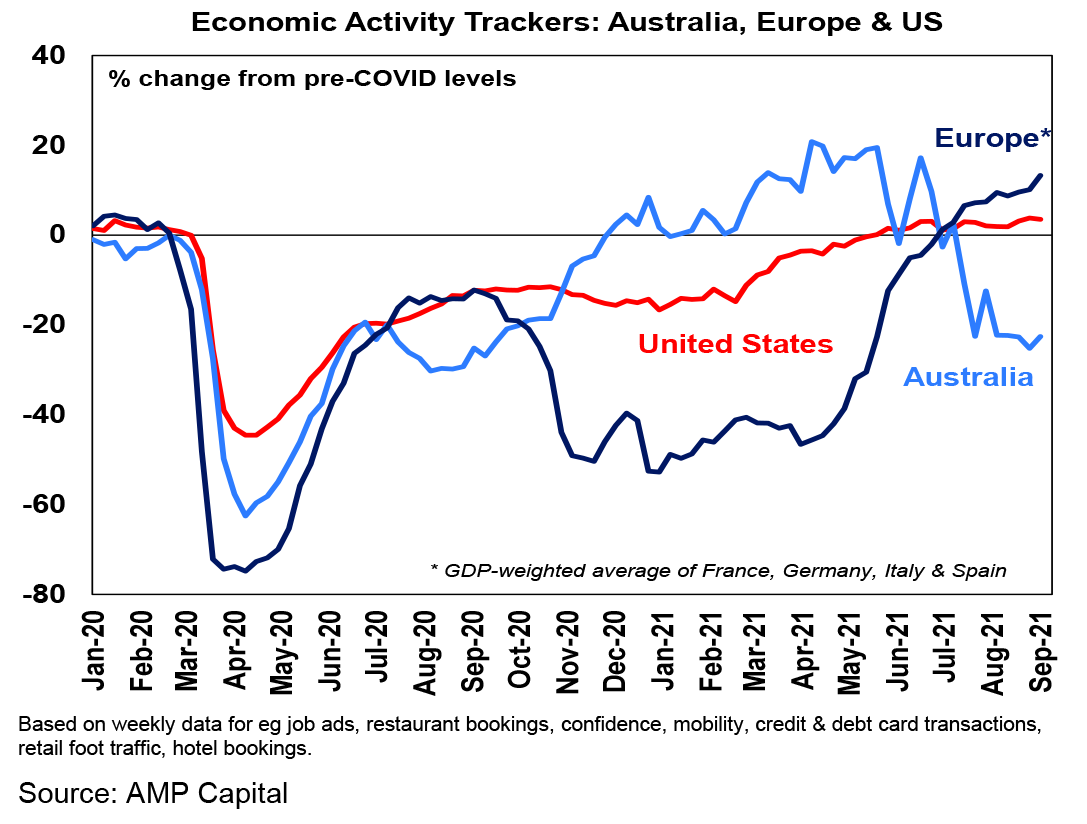

Our US and European Economic Activity Trackers have held up despite recent Delta outbreaks reflecting the absence of lockdowns as vaccines have helped keep hospitalisations and deaths down. In fact our European Tracker moved higher again over the last week.

While our Australian Economic Activity Tracker is well down from its June high, it saw a small rise in the past week. After its plunge it’s probably hit bottom as NSW and Victoria are about as low as they are going to go – providing other states manage to avoid long hard lockdowns.

NSW is showing the path to recovery – but it’s likely to initially be more constrained and riskier than the recovery after last year’s national lockdown, which occurred against a backdrop of very low covid cases. Our rough estimate of the cost in terms of lost economic activity from the lockdowns since May is now at $29bn assuming they continue to the end of September and around $35bn if Greater Sydney continues to around 17th October and Melbourne to the end of October. However, when comparing to last year’s national lockdown there are some favourable factors: the lockdowns have only covered around half of the national population; Australian households and businesses seem to have found more ways to better handle lockdowns compared to 18 months ago; consumer confidence and job ads are holding up far better than seen last year; this may suggest that the more targeted government assistance may be working better this time around and that the hope offered by the vaccines is helping support confidence in contrast to last year; and this is likely to be reinforced by NSW’s reopening roadmap which suggests it will at least start to see some recovery in the December quarter.

But there are also some negatives: the NSW and now Victorian lockdowns look like extending into next quarter; JobKeeper is not protecting jobs like it did a year ago risking sharper headline job losses in impacted states; reopening may be more gradual than seen after the national lockdown, being limited to the fully vaccinated, subject to change if covid cases are too high risking the hospital system and with some states potentially lagging and holding out for higher vaccination rates; and reopening with high case numbers may constrain confidence and hence the pace of recovery compared to last year. Pulling it all together we are sticking with our expectation for September quarter GDP to be down by around 4%, expect a bounce in the December quarter but only of around 1.5% or so which will leave GDP through this year at around flat, but then see a far stronger rebound of 6.5% or more through next year as confidence builds.

RBA retains the taper – but hedges its upbeat outlook by extending bond buying to February. Contrary to our expectations the RBA proceeded with its July decision to slow its bond buying from $5bn a week to $4bn on the grounds the lockdowns will delay but not derail the recovery and that it will be back to around its pre-Delta path in the second half of next year. We are optimistic on a growth rebound next year but not quite that optimistic. But to cover the risk that it may be too optimistic and provide a bit more monetary policy certainty the RBA has extended its bond purchases at the $4bn a week rate out to mid-February whereas prior to the Delta lockdowns some form of further slowing was likely beyond November. The RBA clearly has a high hurdle to reversing its taper with the focus now more firmly on fiscal policy. Short of a major further change in the economic outlook we are unlikely to see any significant policy changes from the RBA out to February with the focus now more firmly on fiscal policy to help with the recovery.

Back when I was trying to get my PhD going my neighbours’ daughter got into a habit of playing Belinda Carlisle’s Mad About You over and over. Its great head candy for times like these. After it initially sent me bonkers, I became a fan. Belinda was formally of the GoGos and when she appeared with The Beach Boys in Hawaii with Wouldn’t It Be Nice and Band of Gold and George Harrison provided a slide guitar solo in Leave A Light On I was really impressed.

Major global economic events and implications

US data showed continuing labour market strength with record job openings in July and a further fall in unemployment claims, but the Fed’s Beige Book noted a downshift in growth to “moderate” with escalating input costs and supply constraints.

As widely expected, the ECB dialled back its pandemic emergency bond buying to a “moderately lower pace” after the “significantly higher pace” through the June and September quarters that was put in place to deal with the bond sell off earlier this year. While President Lagarde said this is not tapering and it still leaves bond buying higher than it was at the start of the year, we have now likely seen the peak in ECB bond buying. A decision on tapering may come in December.

Japanese household spending in July was weaker than expected and the Eco Watchers sentiment index saw a sharp fall in August as the coronavirus state of emergency widened.

Chinese exports and imports surprisingly accelerated in August with the former possibly boosted by higher prices and a front loading of orders. Price pressures were mixed with producer price inflation accelerating to 9.5%yoy, but headline CPI inflation slowing to 0.8%yoy with core at 1.2%. The relationship between producer and consumer price inflation has been weak over the last decade.

Australian economic events and implications

It was a relatively quiet week for Australian economic data releases but what there was provided a mixed picture in terms of the size of the hit from the lockdowns. ABS payroll data showed payroll jobs down 3.5% since mid-June and those in NSW down nearly 9% which is worse than seen in last year’s lockdown. Victorian payrolls jobs are down but are yet to fully reflect its lockdown. Against this the payroll report tends to exaggerate actual job losses and they may look bigger in NSW because last year JobKeeper kept workers on payrolls and consumer confidence as measured by the weekly ANZ/Roy Morgan survey and job ads as measured by the ANZ, Seek and other surveys are holding up far better this time around. Meanwhile the MI Inflation Gauge fell 0.1% in August with more items up in price than down, although its up 2.3% year on year.

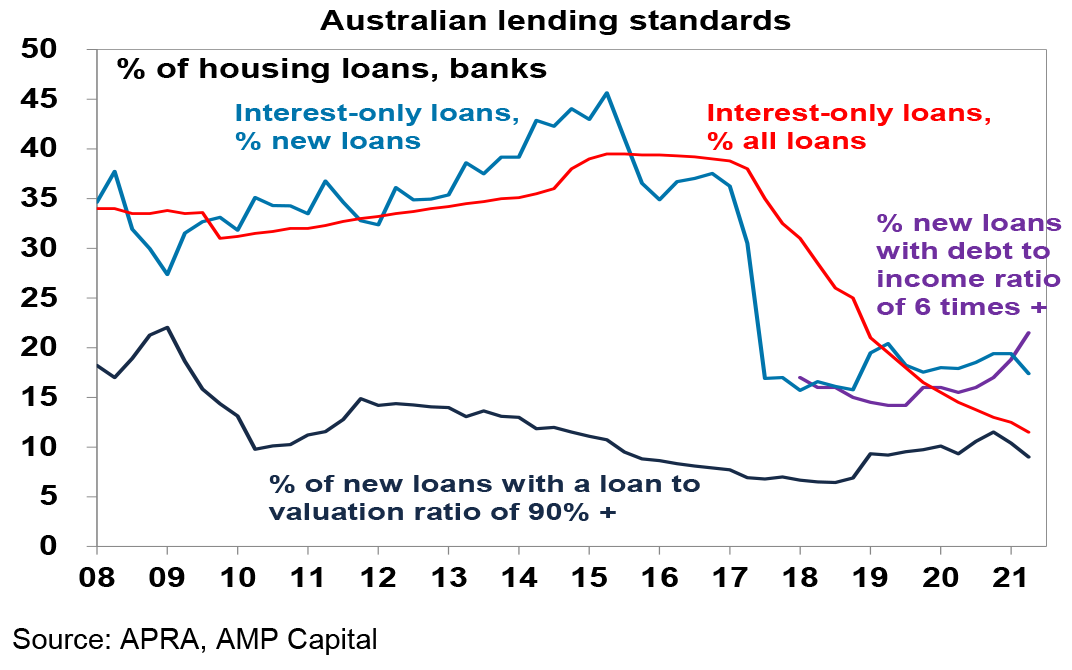

Mixed readings on lending standards. Key APRA metrics relating to housing lending standards were mixed in June. The share of interest only loans and high loan to valuation ratio loans declined in the June quarter, but the share of high debt to income ratio loans rose to a record. The contrast is hard to reconcile but the latter is more consistent with the continuing acceleration in house prices, debt, investor lending and average loan sizes. We continue to expect APRA action to tighten lending standards but given the mixed metrics and lockdown uncertainty it may not come until sometime next year.

What to watch over the next week?

In the US, the focus is likely to be back on inflation with the August CPI (Tuesday) expected to show monthly inflation off its highs but still elevated as supply constraints impact and annual core inflation remaining at 3.3% year on year. In other data, expect a fall in August small business optimism (Tuesday) and retail sales (Thursday) reflecting the Delta outbreak, but a modest gain in industrial production (Wednesday) and stronger September readings for the regional manufacturing surveys (Wednesday and Thursday) and consumer sentiment (Friday).

Chinese August data for industrial production, retail sales and investment (Tuesday) are likely to slow further due to covid restrictions (but should improve this month as restrictions have since been relaxed). Credit data will also be released.

In Australia, August jobs data due for release on Thursday is expected to show a big hit from the lockdowns. While hours worked will bear the brunt of the impact, we expect a 250,000 decline in employment due mostly to NSW and unemployment to spike to 5.5%, with a decline in participation to 65.4% (from 66%) partly muting the rise in unemployment. Both business confidence as measured by the NAB survey (Tuesday) and consumer confidence in the Westpac/MI survey (Wednesday) and expected to be subdued relative to recent highs but to remain well above last year’s lockdown lows. ABS home price data for the June quarter (Tuesday) is expected to show a 6% gain based on private sector dwelling price data already released. A speech by RBA Governor Lowe (Tuesday) will no doubt reiterate the RBA’s “glass half full” optimism but also indicate that it remains dovish on rates and prepared to extend bond buying if needed.

Outlook for investment markets

Shares remain vulnerable to a short-term correction with possible triggers being coronavirus, the inflation scare and US taper talk, likely US tax hikes and a debt ceiling standoff and geopolitical risks. But looking through the short-term noise, the combination of improving global growth and earnings helped by more fiscal stimulus, vaccines ultimately allowing a more sustained reopening and still low interest rates augurs well for shares over the next 12 months.

Expect the rising trend in bond yields to resume as it becomes clear the global recovery is continuing resulting in capital losses and poor returns from bonds over the next 12 months.

Unlisted commercial property may still see some weakness in retail and office returns but industrial is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home prices look likely to rise by around 20% this year before slowing to around 7% next year, being boosted by ultra-low mortgage rates, economic recovery and FOMO, but expect a progressive slowing in the pace of gains as poor affordability impacts, government home buyer incentives are cut back, fixed mortgage rates rise, macro prudential tightening kicks in and immigration remains down relative to normal. The lockdowns have also increased short term uncertainty.

Cash and bank deposits are likely to provide poor returns, given the ultra-low cash rate of 0.1%. The setback from coronavirus lockdowns could push the first rate hike back into 2024.

Although the $A could pull back further in response to the latest coronavirus outbreaks, the threats posed to global and Australian growth and falling iron ore prices, a rising trend is likely over the next 12 months helped by strong commodity prices and a cyclical decline in the US dollar, probably taking the $A up to around $US0.80.

By Shane Oliver