Cracking the HNW Code – The changing face of High-Net-Worth Clients and why they are reshaping financial advice

The High Net Worth segment offers enticing professional and financial possibilities, but one which is also misunderstood.

As we continue our deeper dive into customer and market segmentation strategies for financial advisers, this article examines the High Net Worth (HNW) segment, a segment which many advisers aspire to serve, and yet which remains deeply misunderstood.

While clients within the HNW segment may share some common characteristics – including their service expectations, and their capacity to pay for expert advice – they are far from a homogeneous group, varying greatly in their behaviours, motivations, and sophistication. In fact, the only universal truth for this segment may be that a ‘one size fits all’ approach is doomed to fail.

In this article we aim to explore the themes that unite and differentiate members of this segment, across dimensions such as:

- demographic characteristics

- money motivations and behaviours

- perceptions of advice and advisers

- expectations around fees and services, and

- engagement preferences.

An awareness of relevant considerations across each of these dimensions will be valuable to advisers preparing to enter this segment for the first time, and to those already active in the HNW space who are looking to fine tune their offering to this most demanding of all client segments.

Who are the HNW?

The label ‘high net worth’ conjures up many different images and meanings for people, and certainly there are several definitions that can legitimately be used, including:

- the Investopedia definition[1] – $1 million in liquid assets (family home excluded)

- the Coredata definition[2] – $1m in the share market, or earning an annual income of $450k and over (family home excluded), and even

- the ASIC sophisticated investor definition[3] (annual income over $250k or net assets of $2.5m).

To be consistent with the Australian-focused research we will refer to throughout this article – and because rocketing real estate prices are rendering the ASIC definition less meaningful all the time – this article will use the $1m in net investable assets criterion common to both Coredata and Investopedia.

Across the globe, according to Capgemini[4], there are around 21 million HNW investors. Of these, around 200k are classified as ultra-high net worth individuals, with net investable assets in excess of $30m USD.

In Australia, the HNW segment is also sizeable, and in 2021 was estimated by Investment Trends[5] to comprise around 485,000 individuals, investing more than $2 trillion AUD.

The changing face of HNW clients

Any notion of a stereotypical HNW client (male, middle aged, professional) should be abandoned. Nowadays new entrants to the HNW segment are just as likely to be female, young, and an entrepreneur or IT whiz.

The rising economic power of female investors is indeed a standout trend around the world and is redefining the way firms are approaching this segment.

Global analysis reveals that the gender wealth gap is closing fast, and females are growing their wealth at a much faster rate than males. In the US, females own around 40% of all businesses[6], and hold 37% of all wealth[7]. In Australia females hold around 32% of wealth. This same analysis predicts female wealth globally to grow almost 40% faster than male wealth between 2019 and 2023[8].

From a financial advice perspective, this is noteworthy for a number of reasons. Research[9] has shown female investors often have different motivations around investing, are generally more risk averse than their male counterparts, and are more likely to be concerned about ESG and social justice issues when investing (Figure 1, below).

When viewed in tandem with finding from the same study that younger females are also taking the lead more in household financial decisions (Figure 2, below), a picture emerges of female HNW clients who are looking to be more active and hands on in financial decisions than previously seen.

HNW investors are getting younger too, with recent research suggesting that around a quarter are millennials[10], and almost three quarters are aged 50 and under[11]. (This age profile will skew younger still as Australia’s 3.5 trillion intergenerational wealth transfer gets into full swing.)

What are they like as investors?

Australian HNW investors, it seems, are a cautious bunch.

Research by CoreData[12] characterises Australian HNW/UHNW investors as conservative and unsophisticated in their approach to investing, traditionally concentrating their wealth in just three asset classes – cash, Australian shares and residential property – representing roughly 75% of portfolios.

Their portfolios also show a strong home bias, with around half owning Australian shares only, less than one in four (23.1 per cent) owning international shares, and less than one in 10 (9.8 per cent) having international bonds. Only one in seven (14.6 per cent) have alternative investments such as emerging markets shares, private equity and hedge funds.

Paradoxically, this conservative outlook, coupled with a lack of knowledge – including the availability, characteristics, and costs – of alternative investment types, could actually be increasing their portfolio risk by limiting asset diversification.

Attitudes may slowly be shifting though – perhaps driven by continuing low interest rates – with various studies[13] suggesting a growing appetite amongst this segment for alternative investments, including private equity and hedge funds, crypto, commercial property, ESG and impact investments, and more bespoke (wholesale) opportunities tailored to individuals.

What are their money motivations?

To some extent, the money motivations of HNW and UNHW clients mirror those of many other investors – saving for retirement, the desire to make a social impact, preserving wealth and passing it on to family members, and leaving a legacy. However, the quantum of the amounts involved increases the number – and complexity – of solutions available.

Older HNW clients, boomers and beyond, have ridden a wave of enormous asset growth over their lives, in both equity and housing markets. It is these clients who are at the very centre of the enormous intergenerational wealth transfer we will see over the next two decades.

They will be more focused on preserving wealth as opposed to chasing it, with key considerations being:

- an orderly transfer of wealth to younger family members (44% of HNW clients are worried about this)[14]

- asset protection, and

- optimising tax treatment.

Increasingly, due to improving life expectancies, the challenge of the ‘early inheritance’ must also be faced.

HNW investors of all ages are also taking more notice of environmental, social and governance (ESG) considerations as part of their investment decisions.

Almost half the investors in one survey[15] said they now choose funds or companies to invest in according to ESG considerations. More than half (54%) said they avoided investing in companies with controversial track records, while a massive 89% said that fund managers should ‘police’ companies to ensure they act responsibly.

Interestingly, the specific focus area within the ESG universe tends to differ across generations, with younger investors placing more emphasis on environmental factors, middle-age investors looking more at social factors and investors over 50 years considering governance to be the priority[16].

This increasing desire to make a difference has also translated into support for philanthropic causes, and the growth in scale and visibility of HNWI’s philanthropy has been dramatic in the last decade.

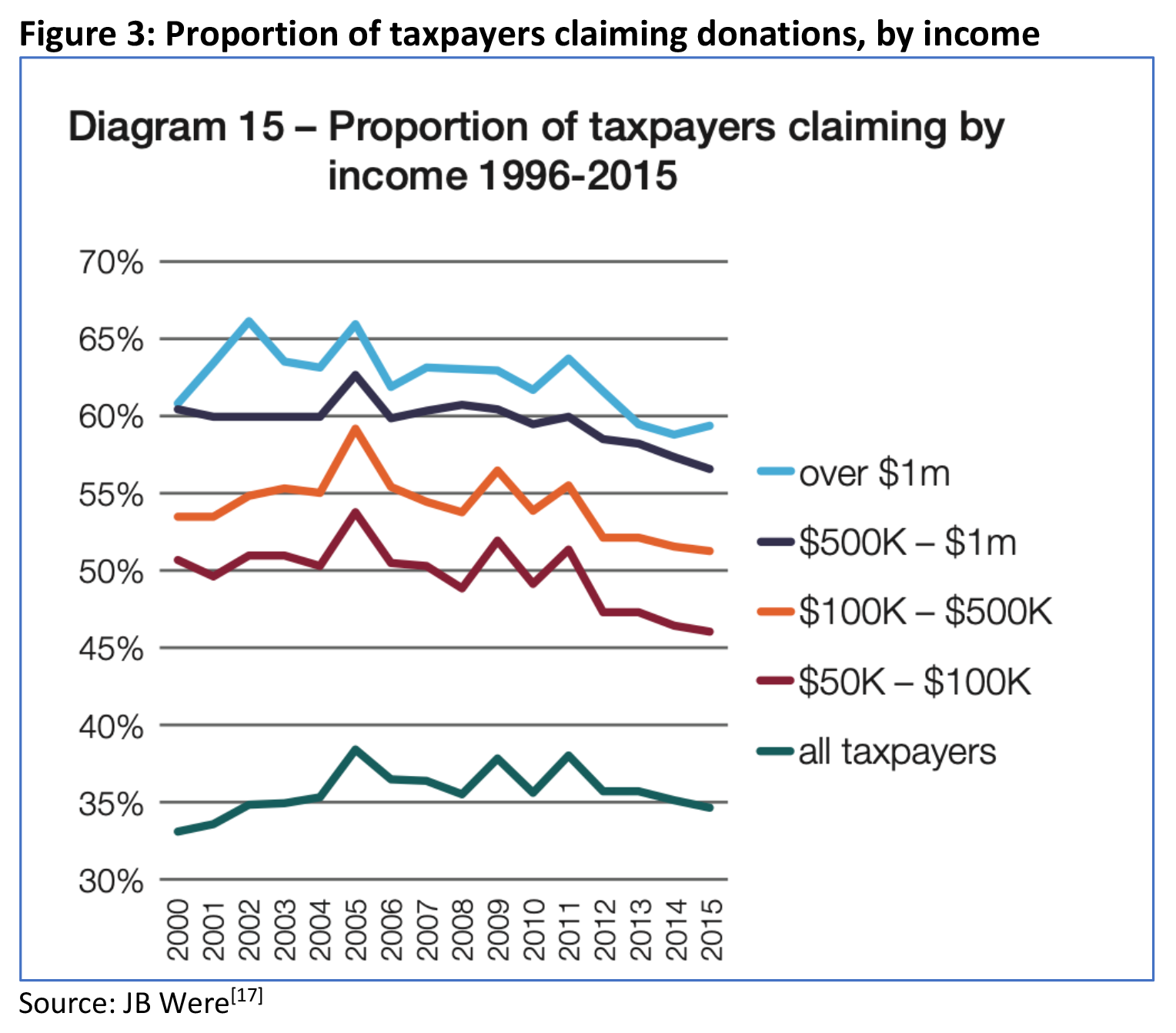

In 2017-18, almost 4.5 million individual taxpayers claimed a total of $3.75 billion as tax-deductible donations[17]. This represented a 7% growth in donations compared to the prior year, although the number of donors actually shrank by 2%. This is consistent with trends over the last decade that show a smaller proportion of Australians are giving, but they are giving larger amounts.

A major factor in the growth of the HNW contribution to overall philanthropic giving was the introduction of Private Ancillary Funds (PAFs) in the early 2000s. These funds enabled donors to be more structured, and tax effective, in their giving, with contributions to PAFs immediately tax deductible, whilst the funds can be disbursed to chosen causes over time (subject to minimum annual disbursement limits).

The causes that HNW donors support are markedly different from those supported by mass market donors, with HNW donors being financially more supportive of universities, arts and culture, health and medical research, and the environment. (Mass market donors are more supportive of religious and overseas aid charities.)[18]

HNW appetite for advice

As tempting as it might be to characterise all HNW clients as financially literate and self-directed, the truth is somewhat different.

Certainly, the majority of HNW investors do not use a financial adviser, but that is also true of the broader population. The good news is that the recognised need and appetite for advice amongst this segment is definitely increasing.

More than half[19] have recognised they have advice needs, and recent research[20] has found particularly strong growth in the segment referred to as HNW ‘validators’ – those who would consider using an adviser to get a second opinion or for their technical skills and access to a wider array of investments.

Between late 2019 and late 2020, the percentage of HNW validators open to financial advice rose from 40% to 56%. Over the same period, there was a corresponding fall in self-directed HNWs, from 49% to 34%.

Another way of looking at the validators is as ‘coach seekers’. In other words, they like to feel in control and to be reasonably involved in managing their wealth, but they also like to seek some form of advice for information and higher-level ideas.

According to King Loong Choi, Investment Trends associate research director, this group represents a unique opportunity for advisers:

“The uncertainties caused by the pandemic has prompted many HNWs to reconsider how they view professional financial advice, which presents a unique opportunity for advice providers to demonstrate their value-add – through their technical expertise, guidance and proactive communications”.[21]

However, notwithstanding the value HNW investors place on the ‘second opinion’ of a financial adviser, intention still hasn’t translated into action, and usage of financial planners (19%), full-service stockbrokers (15%), wealth managers (7%) and private banks (5%) has largely remained static over the last 12 months[22].

Does this disconnect suggest advice providers need to rethink their value proposition and delivery model to HNW clients?

How to attract and retain HNW clients

For financial advisers looking to tap into the HNW segment, there are a number of propositional elements that deserve particular focus.

Hyper-personalised service

As you would expect, HNW clients are extremely demanding. An overwhelming majority (86%) want personalised offerings, and for 91% of them, service quality is the most important criteria in choosing an adviser[23].

What does this mean in practical terms?

Whether it’s leaving a legacy for their children or philanthropic giving, understanding what motivates your clients, their goals and challenges, is critical to delivering a personalised service.

Once you’ve spent time understanding their needs, don’t squander that goodwill by sending HNW clients mass email campaigns or generic updates with little relevance to their personal situations. Instead, take them off your primary mailing list and send them fewer but more personalised updates, such as custom monthly reports.

Of course, providing a truly tailored offering and regular personalised communication – including 24-hour access to you if they need it – isn’t economically viable for most standardised advice fee models. But that’s exactly the point. Serving HNW clients will, for many advisers, necessitate a rethink of their fee and service approach, perhaps even their entire business model.

The advice firms who get this personal connection right will reap the rewards: ‘Personal Connection Leaders’ are 26% more likely to get recommended, generate significantly more fees, and are almost twice as likely to generate new inflows[24].

A more flexible menu of modular services

A traditional approach to financial advice has been to deliver an entire financial plan. The offering of modular, or limited, advice has not proved especially popular within the advice community, partly because some advisers perceive it as carrying higher compliance risks, while many don’t see it as economically viable.

Here, again, a mindshift is necessary. HNW clients are more able, and more willing, to pay fees for service. The appetite amongst the ‘validators’ is almost certainly growing, for ‘a la carte’ advice rather than the entire buffet, and advisers looking to enter this segment must be prepared to provide advice in a more modular fashion.

Fee expectations

As with all advice clients, the topic of fees is an important one. For HNW clients though, the issue is not around affordability, but around value and transparency.

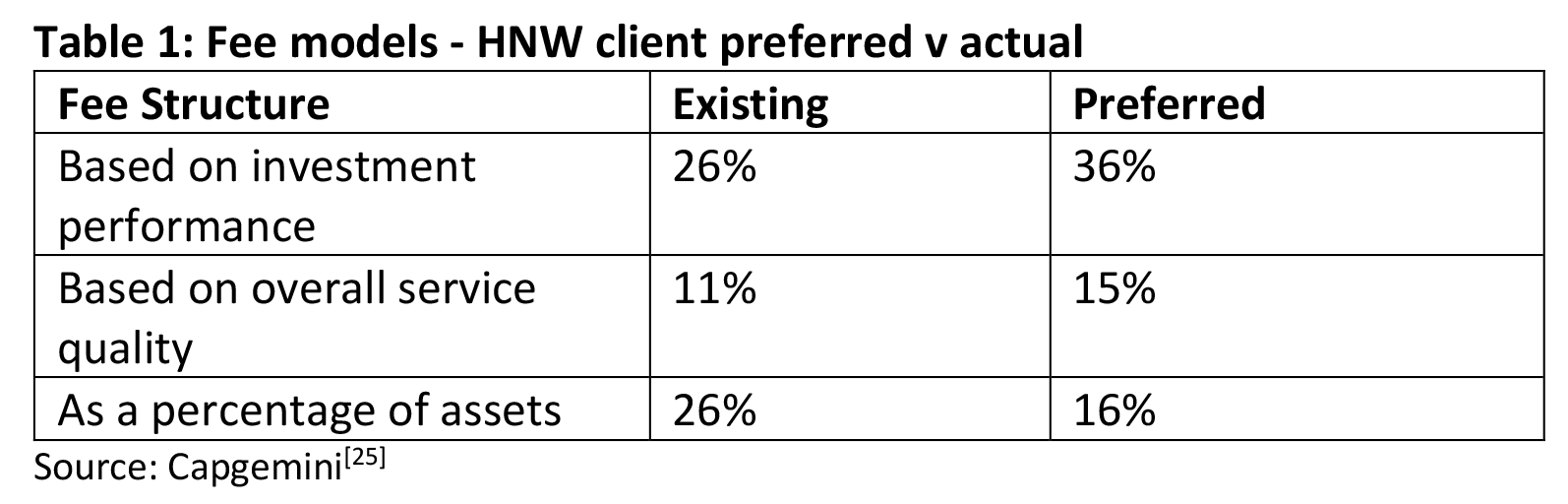

Research[25] suggests a growing preference for fees which reflect the value added and the time spent by the adviser.

Consistent with the above, Australia has seen a pronounced trend in recent years towards charging HNW clients a flat fee, rather than a percentage of assets. In 2016, according to a Netwealth analysis[26] of advice firms on its platform, almost 30% of clients with an account balance of more than $3 million were charged either a flat fee or a combination of flat and percentage-based fees. Three years later, in 2019, the total number of HNW clients who were charged a flat fee had increased significantly. By then, a majority of clients with a $3 million+ account balance (51.7%) were charged in the same way, as were clients in the $1-3 million band.

You have to get the technology right

HNW clients are extremely demanding and mostly tech savvy, and they expect the quality of their digital engagement with their wealth to offer the same personalisation and seamlessness as their interactions with other brands and categories.

Globally, over half of HNW individuals believe it is important for their financial adviser or wealth manager to have a strong digital offering – and across the Asia Pacific region that rises to almost two-thirds (even higher for those under 45)[27]. This expectation is not currently being universally met, especially among younger HNW clients, of whom almost half are dissatisfied with their adviser’s digital maturity[28].

Increasingly then, a strong digital game is just a hygiene factor for this segment. This is not just about relying on the superb functionality offered by the market’s leading platforms; this means advice firms investing in their own technology – including Artificial Intelligence – which allows a new hybrid, omnichannel approach, combining hyper-personalised self-service with modular, human delivered, on-demand advice. This is an approach which allows HNW clients to ‘stay in the driving seat’, with a guiding hand, and meets their needs for transparency, visibility, and responsiveness.

From the supply side, advisers serious about improving their efficiency, and their ability to offer a broader array of educational resources and improved engagement in a more economically viable way, should already be exploring a more technology enabled ‘hybrid’ advice model.

A flexible service offering tailored to HNW needs

A standard APL and model portfolio approach won’t cut the mustard with HNW clients, with a great many HNW clients expressing dissatisfaction with their wealth managers, personalised offerings, or digital interfaces. More than a third say a lack of value-add beyond investment expertise is likely to drive them elsewhere.

Advisers serving HNW clients need to ensure their product and service offering reflects the segment’s needs for modular advice, personalisation, and specialised expertise. Examples include (but are not limited to):

- tailored portfolio construction and management services

- financial coaching

- limited scope advice

- ESG investments

- access to bespoke, alternative, and non-retail investment opportunities including private equity, infrastructure, private credit and hedge funds

- structured giving expertise

- estate planning, insurance, and asset protection advice

- ax planning, and

- cash flow planning.

Importantly, HNW clients aren’t looking for an adviser who needs to ‘hand them off’ to other experts. That undermines their needs for efficiency and deeply personalised service. In this space you need an all-encompassing offering. As Netwealth put it:

To succeed in this segment, the firm should be seen (in the eyes of the high-net-worth client) almost as an all-purpose financial hub that offers personalised solutions to specific challenges”[29]

As we start to see the age and gender mix of HNW clients transform, advice firms should also consider better demographic alignment between the adviser and client, which in many cases will improve the extent to which the adviser – and their advice – is relatable.

Conclusion

The HNW segment is an attractive one for many advisers, due to its strong growth and its increasingly attractive financial viability at a time when advice is becoming more expensive to deliver.

It is, however, an extremely challenging segment to serve well, demanding high touch, hyper-personalised service, and specialised and flexible expertise beyond the realm of many ‘cookie cutter’ advice business models.

As the face of the segment continues to transform, the importance of an advice firm’s digital offering is also growing in importance.

The advisers who will succeed in this space are those who best meet the segment’s needs for a true hybrid (human and digital) model, and who can act as the all-purpose financial hub through which clients can access a wide range of bespoke services from an a la carte menu of solutions.

———-