What are the key requirements of the DDO regime and the practical implications for advisers and practices?

Introduction

On October 5th, 2021, the new Design and Distribution Obligations (DDO) regime – and associated Product Intervention Powers – came into effect.

One of the most significant regulatory reforms of the last decade, the essence of the DDO regime is to ensure financial products are designed for, and distributed to, the right people.

Such a regime has been on the cards since the Financial Systems Inquiry (FSI) of 2014, which laid bare the notion that suitable disclosure always leads to informed consumer decision-making. Recommendation 21 of the final FSI report was:

“Government should amend the law to introduce a principles-based product design and distribution obligation. The obligation would require product issuers and distributors to consider a range of factors when designing products and distribution strategies.”[1]

Some of the more memorable stories from the Hayne Royal Commission, such as those relating to ‘junk insurance’ or mass sales of funeral insurance to indigenous communities, only sought to reinforce the resolve of regulators to introduce such a regime (which is conceptually similar to those in existence in other parts of the world, including MiFID 2 in Europe.)

In simple terms, DDO is intended to act as constant, organic feedback loop, where:

- a product issuer articulates the target market the product is suitable for (via a Target Market Distribution, or TMD)

- distributors provide data to issuers that helps them assess whether the product design – or the definition of the target market – needs to change, and

- issuers provide data to ASIC, for them to assess appropriateness of products and product categories.

Of course, describing DDO in such simple terms belies the significance of this new regime on advisers, who must come to grips with a range of practical challenges, including:

- obtaining and understanding current TMDs for every product they recommend

- deciding how to incorporate TMDs into the advice process, and

- implementing data capture and reporting processes to meet ASIC and issuer requirements.

These challenges bring a range of considerations into play, including the role of technology, staff training, advice costing, and APL construction.

DDO at a glance

Products captured by DDO

DDO applies to products, and platforms, as defined below, that are distributed after 5th October 2021.

- products that need a PDS (e.g., interests in a managed investment scheme, insurance, and superannuation products)

- certain securities that need a disclosure document under Part 6D.2 of the Corporations Act, but not ordinary shares (e.g., securities with an investment purpose, such as listed investment companies, listed investment trusts, hybrid securities and real estate investment trusts)

- credit contracts (e.g., credit cards, home loans, funeral expense policies), and

- other products prescribed by the Corporation Regulations (including but not limited to investor directed portfolio services and exchange traded products).

Issuer obligations

The design obligations applicable to product issuers include requirements to make a target market determination (TMD) and make it publicly available.

Distributor obligations

The distribution obligations applicable to distributors (AFSLs and their representatives) include requirements[2] to:

- not engage in retail product distribution without a TMD

- not engage in retail product distribution where a TMD may no longer be appropriate

- take reasonable steps so that distribution is in accordance with the TMD

- collect, keep, and provide distribution information as required by the distributor

- notify the issuer of any significant dealings inconsistent with the TMD.

What are reasonable steps?

Where a product is sold via a personal advice process, the tailored nature of that process, and the pursuant Best Interests Duty, are taken as a proxy for ‘reasonable steps’, and RG 274 specifically notes that financial advisers providing personal advice are not required to meet the reasonable steps obligation under DDO:

“When a distributor provides personal advice, it will not be required to take reasonable steps that will, or are reasonably likely to, result in distribution of a financial product being consistent with the TMD: see s994E (3) and the definition of excluded conduct in s994A (1).” ASIC RG274.200

However, in the case of general advice or execution only sales, distributors must take ‘reasonable steps’ to ensure distribution is in accordance with the TMD. Just what constitutes ‘reasonable steps’ for distributors depends on the likelihood of distribution being inconsistent with the TMD, the potential harm that might arise from inconsistent distribution, and the steps that can be taken to mitigate these harms.

Factors ASIC may consider when administering the ‘reasonable steps’ requirement include:

- distribution method

- does the distribution method/sales process direct or limit distribution to the target market?

- marketing and promotional materials

- are materials informed by, and consistent with, the TMD?

- inappropriate incentives

- are there incentives for products to be sold to customers outside the target market?

- staff training

- are staff sufficiently trained and possessed of sufficient skill to take ensure customers fall within the target market?

- steps taken to assess whether customer is in the target market

- what steps are taken? What information must customers provide about themselves to determine whether they fall in the target market?

- customers must not be asked to ‘self-certify’ that they are in the target market

- product governance

- what is the overall framework the distributor has for oversight and control over its distribution processes?

NOTE: For the purposes of DDO, the law provides that the act of asking for personal information solely to determine whether a person is in the target market for a financial product, and of informing the person of the result of that determination, do not, of themselves, constitute personal advice [Corporations Act s766B(3A)].

The TMD

One of the central pillars of DDO is the Target Market Determination (TMD).

Under DDO, product issuers will be required to make publicly available a TMD for each product (although it is not mandatory to give the TMD to clients).

The TMD will describe the typical objectives, financial situation and needs of consumers in the target market, describe the product features, and explain why those features are likely to meet consumers’ needs. The TMD will generally also articulate time horizon, risk level, and other relevant suitability criteria. In many cases a ‘traffic light’ system for assessing suitability will be used.

Importantly, the TMD will also describe the data that distributors are required to provide back to the issuer, including:

• ASIC mandated data

- significant dealings outside the TMD

- if complaints were received, and is so, the volume, and

- issuer mandated data

- examples can include more detail on complaints, and/or any dealings outside the TMD (regardless of whether they are significant or not).

To the extent that each product issuer will differ in their requirements, it is vital that advisers take the time to examine all TMDs and be alert to variations.

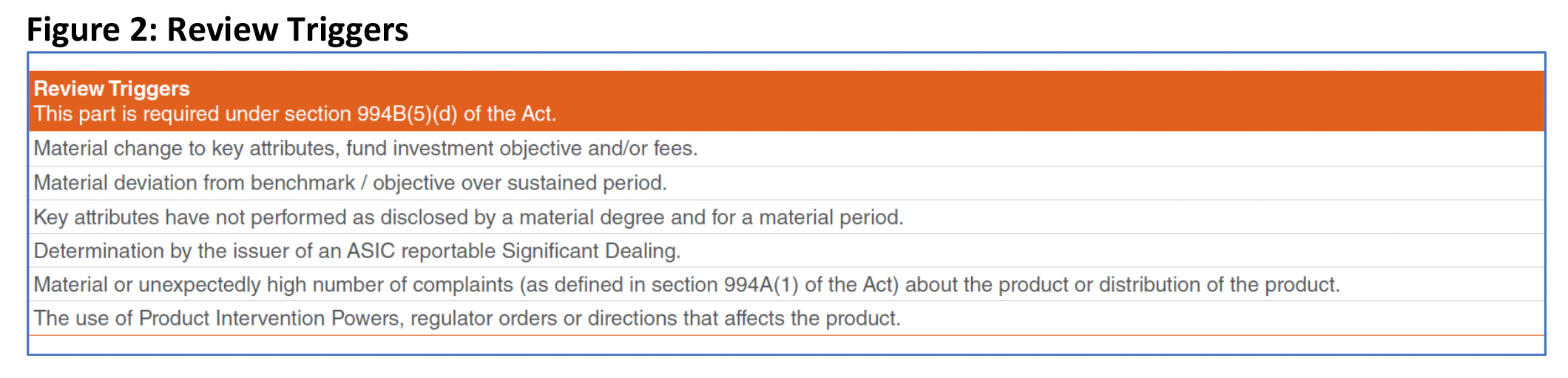

The TMD will also specify any events that suggest the TMD is no longer appropriate – known as ‘review triggers’ – along with the normal schedule of TMD reviews.

TMD Format

Whilst ASIC does not specify the exact format of a TMD, many fund managers and life insurers have supported the Financial Services Council (FSC) in their call for a degree of consistency, to help streamline the product comparison process. They have made more than a dozen templates3 – across many product categories – available to their members free of charge (and available to be licensed by non-members).

Using examples below, we will briefly illustrate how TMDs tackle each of the areas mentioned above:

Significant dealings

A critical DDO concept is that of ‘significant dealings’.

Distributors are obliged to report any ‘significant dealings’ in the product to consumers falling outside the defined Target Market. Whilst a TMD must reference the reporting requirements around significant dealings, many are vague around the definition of ‘significant’.

RG 274 does not define ‘significant’ (nor does the Corporations Act) and recognises that its meaning is likely to vary between product types and issuers, depending on:

- the actual or potential risk of harm to a consumer including any financial loss

- the nature and extent of inconsistency (for example, two ambers and one green assessment versus three red)

- with insurance products, some consideration of premiums or gross income, and

- the time period during which these dealings took place.

Dealings may be significant if they represent a material proportion of the overall distribution conduct carried out by the distributor in relation to the product, or they constitute an individual transaction which has resulted in, or will or is likely to result in, significant detriment to the consumer (or class of consumer).

Definitions are likely to vary by product issuer, and by product category, and advisers must be diligent to understand the different reporting requirements between issuers.

As an example, one fund manager regards significant dealings as including circumstances where:

- 10% of consumers who have acquired the product who are outside the target market over a quarterly period

- 10% of consumers who have acquired the product have characteristics that are specifically excluded from the target market, and/or

- distribution conditions have regularly not been met in that the product has been sold to consumers who have not received personal advice.

It is worth noting that as per Figure 3, some providers require reporting on all dealings – not just significant ones – outside the TMD.

The data challenge

All distributors must collect and maintain complete and accurate records of ‘distribution information’: see section Corporations Act 994F(2)–(6). This information must be kept for up to seven years.

One of the biggest challenges relating to this distribution information is data format. This has important implications for the systems and processes advisers use to capture that data, and how they then pass that data on.

To aid consistency, and drive efficiency, the FSC developed, in conjunction with its members, a comprehensive set of templates and data definitions, and advisers will find that these are the standards referenced in many TMDs.

Whilst AFSLs will set standards around data capture and reporting for their authorised representatives, self-licensed advisers will need to take on responsibility for this themselves, and adopting the standards required the FSC is likely to be an efficient and effective way of ensuring processes are robust enough to suit the majority of issuers.

Table 1, below, shows the FSC’s recommended data format for complaints data capture and reporting.

Another of the standards developed by the FSC relates to information on dealings outside the TMD[5] It suggests 5 ways of categorising and recording reasons for dealing outside the TMD:

- investment product in a diversified portfolio

- product assessed as suitable for customer’s objectives, financial situation and needs, despite TMD

- customer assessed as outside TM after dealing occurred

- distributor considers risk of customer harm to be low, and

- other.

Technology and DDO

Technology has an important role to play in supporting compliance with DDO.

From an adviser’s perspective, technology can help with:

- obtaining the most current TMD for a product

- being aware of when a TMD has been withdrawn/changes

- attesting receipt of a TMD

- recording client assessments against a TMD (including cases where the client fell outside the defined target)

- recording complaints data

- recording other distribution information required by issuers.

To the extent that many advice practices already collect much of this data to support their existing advice processes and compliance obligations, the additional data collection burden imposed by DDO may be incremental. The reporting obligation on the other hand, in terms of both the frequency, and the number of places that reporting needs to be sent, does represent a step change, and is a scenario where automation can provide a significant benefit of more ‘manual solutions’, in terms of both efficiency, and compliance.

A number of advice technology providers have launched DDO solutions, including IRESS and Morningstar[6]. These solutions address issues such as real time publishing of, access to, current TMDs, and TMD data collection and dissemination, including data for distributor analysis, monitoring and reporting.

Dealings outside the TMD are not outlawed

Whilst the DDO places much emphasis on the reporting of dealings outside the defined target market, this is not to say advisers cannot recommend products to clients falling outside the TMD. On the contrary, there are many circumstances where advice truly tailored to the unique circumstances of the client may well involve such products.

RG 274 notes:

“It may be appropriate for a financial adviser to advise a consumer outside of the target market to acquire a financial product, when acquisition would be in the best interests of the consumer. For example, it may be appropriate in the broader context of a particular consumer’s portfolio, taking into account their relevant circumstances, for an adviser to recommend a product that would ordinarily be too high-risk for the consumer if it were a concentrated holding.” RG274: 203

A summary of practical considerations for advisers

The DDO regime undoubtedly presents challenges for advisers, initially – as the TMD concept beds in and data capture processes are tweaked – and the ongoing challenge of extra reporting requirements. Practices offering general advice or execution only services will also need to ensure they have a robust governance process in place to support their ‘reasonable steps’ obligation. A summary of the key practical considerations is below.

———–