Impact alpha – emerging trends in SDG aligned impact investing

How to identify investable opportunities arising from SDGs, especially in the retail investor space.

Introduction

The Sustainable Development Goals are 17 objectives for improving human society and ecological sustainability adopted by the United Nations in 2015. They cover a broad spectrum of sustainability topics, ranging from eliminating hunger and combating climate change to promoting responsible consumption and making cities more sustainable.

Critically, these weren’t goals left in the hands of governments alone to initiate, and the UN has called on business, corporates, and individuals to also play their part. Despite this call, there has been a persistent SDG financing gap estimated at around $2.5 trillion per annum[1].

Fortunately, SDG aligned investing is growing rapidly, in line with growing investor appetite for impact investments more broadly.

Whilst early innovations in impact investing have mainly catered to institutional investors, the next frontier for impact investing – including SDG aligned investing – lies with retail investors, who globally command around $100 trillion in investing power[2].

In order to understand what the future of SDG aligned investing looks like, it is necessary to understand both the challenges in creating investable opportunities from the SDGs, as well as the motivations of investors seeking to make an impact with their investments. Within this context, we can then explore product innovation trends in this space, the opportunities for investors, and the implications for financial advisers.

The SDG investing challenge

There are a number of major challenges into creating investment opportunities that progress the SDGs. Firstly, it is not always straightforward to be able to measure the link between economic activity and SDGs. Secondly, and related to the first point, the individual companies behind this economic activity can both positively and negatively impact any one of the 17 SDGs and their 169 underlying targets, making it difficult to assess their ‘net impact’. Thirdly, many of the high-level goals themselves don’t automatically present as investable.

Economic activity and SDGs

In societies, companies undertake numerous types of economic activities, which sustain livelihoods and produce goods and services that help people attain a better life, but which can also have negative consequences.

Different types of economic activities can impact different SDGs, however, there has been a general shortage of evidence on how individual economic activities interact with the SDGs. This lack of evidence adds a layer of complexity for companies, governments, and investors trying to create smart SDG strategies that steer towards net positive impact.

A recent study[3], by academic Rob Van Tulder and Robeco SDG strategist Jan Anton van Zanten, shed new light on this problem.

At an overarching level, their study found that economic activities bring ample opportunities for advancing the SDGs, as most are sources of economic productivity, which directly benefit SDG 8 (decent work and economic growth) and/or SDG 9 (industry, innovation, and infrastructure).

However, widespread negative impacts were identified, especially afflicting ecosystems reflected by SDG 14 (life below water) and SDG 15 (life on land). Others were found to be bad for global warming, adversely impacting SDG 13 (climate action), or they harm human health SDG 3 (good health and well-being).

Agricultural activities, for instance, feed the world, thereby having clear potential to help achieve SDG 2 (zero hunger), however, they also account for 70% of water withdrawals globally which raises concerns for SDG 6 (water and sanitation), and the use of fertilizers and pesticides threatens SDGs 14 and 15 (life on land and below water).

Electricity generation promotes SDG 9 (industry, innovation, and infrastructure), but when it is generated through non-renewable sources, SDG 13 (climate action) is at risk, while SDG 3 (health and well-being) may be harmed due to air pollution. Estimates suggest that in China, for example, 15 million years of life that is lost through pollution from power generation could be avoided.

The Van Tulder and van Zanten study observed an increasing recognition amongst scientists and policymakers that SDG progress could be accelerated through a ‘nexus approach[4]’. This nexus approach aims to identify and manage interactions between SDGs such that multiple SDGs can be advanced simultaneously, whilst mitigating the risk that progressing one will undermine another.

For example, eradicating hunger (SDG 2) improves health and well-being (SDG 3) and can help people escape poverty (SDG 1). Targeting these SDGs together, instead of treating them as isolated silos, brings opportunities for bigger impacts.

Making SDGs investable

At a high level, the investment opportunities underlying many of the SDGs are not that obvious. Where, for example, do the opportunities lie with SDG 14 (Life below water), or SDG 16 (peace, justice, and strong institutions)?

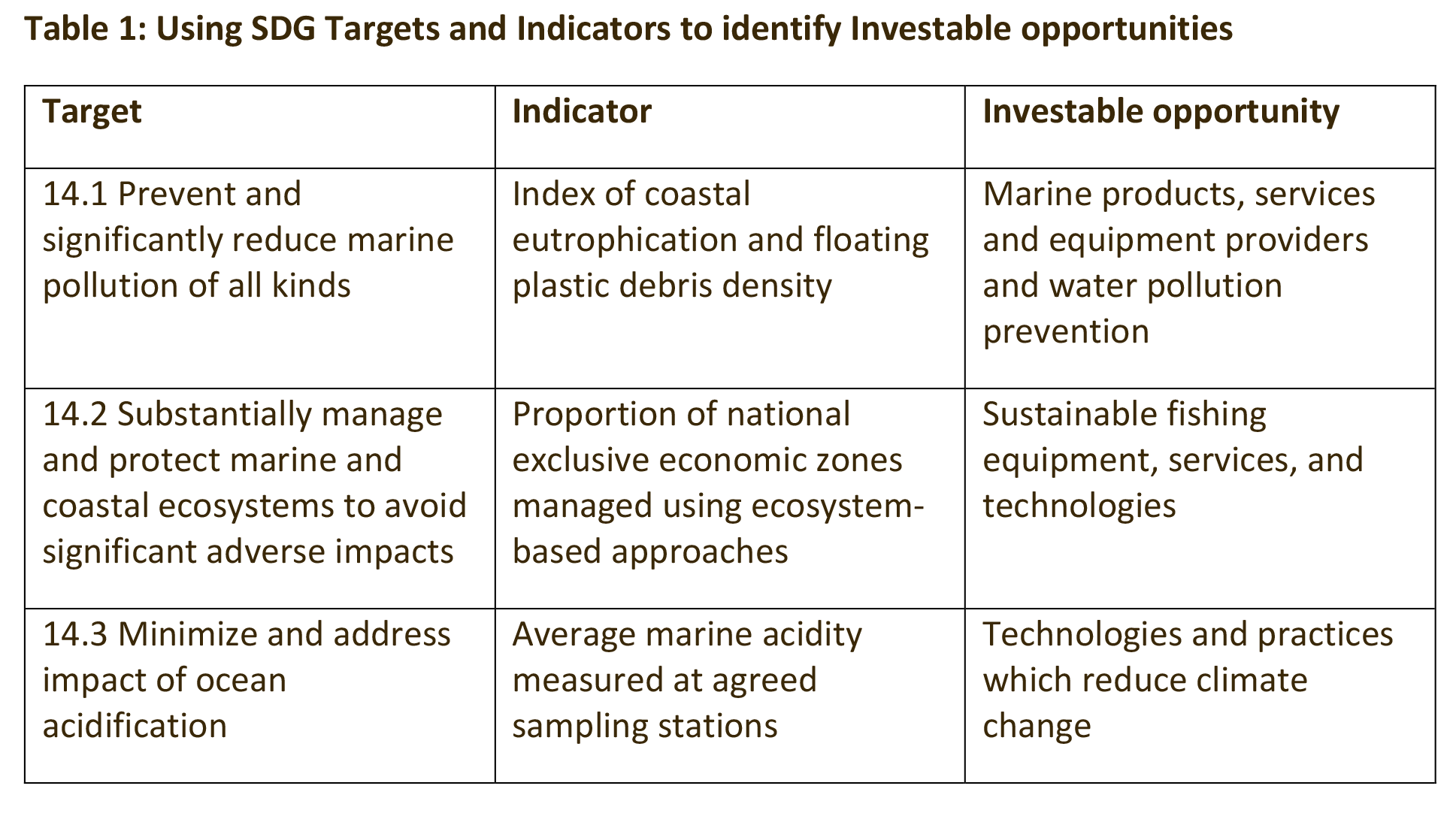

To answer this question, we must look to the targets underlying each goal, along with the UN defined progress indicators for each goal. Across the 17 SDGs there are 169 targets and 232 unique progress indicators[5], and it is the granularity of these goals and measures which helps illuminate the potential investment opportunities.

Using SDG 14 as an example, there are 7 underlying targets, each with its own corresponding indicators[6]. Focusing on a subset of these targets, Table 1 below shows how these can manifest as investment opportunities.

Frameworks to bring it all together

Creating a universe of appropriate investment opportunities from SDGs requires us to connect the investment potential of SDGs with the activities of individual companies, and as discussed in our first article in this series, there are a number of frameworks that have been developed for this purpose.

Robeco’s proprietary framework[7] is one such example.

The first step in their framework is to link companies’ products and services to the SDGs. To what extent do they contribute? Companies are assessed on an extensive set of rules and Key Performance Indicators (KPIs). These are summarized in a guidebook. The guidebook states whether – as a starting point – the contribution of these products and services is positive, neutral, or negative.

For the telecom sector, for example, the starting point is positive. Telecommunications are an essential part of the infrastructure in a safe and connected society. Farmers can use mobile phones to check market prices before selling to middlemen, and market traders can accept payments in mobile money. This way, the telecom sector can contribute to a proper infrastructure (SDG 9), economic growth (SDG 8) and ultimately to the reduction of poverty (SDG 1).

Next, the degree of that contribution has to be determined.

Whilst under the Robeco framework this defaults low in the case of Telcos, closer examination of individual companies within the sector, and assessment against a set of proprietary KPIs may reveal outliers. If, for example, more than 25% of the Telco’s sales take place in emerging markets (which have most to gain from a good telecom network) they will upgrade the impact from positive-low to positive-medium.

The second step is to assess how the companies operate themselves. Are they polluting, do they respect labour rights, do they refrain from corruption? Ratings are then adjusted accordingly.

Robeco’s final step is to check whether the company concerned has been involved in any controversies, such as oil spills, fraud, or bribery. This step can lead to adjustments in the rating. If firms commit serious and structural breaches of the UN Global Compact, for example, they are excluded.

When this framework was applied to a sample[8] of 450 companies, 62% of the companies have been assessed as making a positive SDG contribution. These included grid operators, healthcare companies, banks (by providing finance, especially in emerging markets, banks play an important role in fostering innovation and stimulating economic growth) and utilities with a relatively small share of coal, nuclear energy, and oil in the energy generation mix.

26% of the companies assessed were found to make a negative contribution, including energy producers with a relatively large share of fracking, companies that produce unhealthy food, or car manufacturers with a low share of EV/hybrid models.

How does this translate into investment opportunities?

The SDGs have broadened the scope of impact investments from traditional and mostly private impact investing vehicles, such as microfinance funds or renewable energy projects, to listed equities and credits, as well as thematic strategies.

Thematic or issue investing

Three examples of investment strategies that target an issue rather than a specific SDG, can be seen in themes that are gaining traction in environmental protection: renewable energy, the circular economy, and green bonds:

Renewable energy

Renewable energy is a genre of investing in its own right that now straddles impact investing and mainstream sustainable investing. Once considered niche, the solar, wind and hydroelectric power industries have become an important part of the international energy mix, accounting for 28% of global energy production in 2020[9]. Investing in renewables, however, is often done indirectly through more mainstream investing.

Circular economy

2020 saw the launch of several funds targeting the circular economy. These aim to replace the current ‘take-make-dispose’ model of production and consumption, which relies on the continual use of resources. To this end, such funds invest in companies engaged in activities starting with ‘re’: recycle, reuse, refurbish, repair, redesign, recover. There is no specific SDG for the circular economy – although it ties in with SDG 12 (responsible consumption and production).

Green bonds

Green bonds are debt securities that are exclusively used to promote environmental projects. They are issued mainly by governments, municipalities, and NGOs. For a bond to qualify as ‘green’, its proceeds should be used for projects with clear environmental benefits, such as renewable energy or waste management. The first green bond was a Climate Awareness Bond issued by the European Investment Bank in 2007, and it is becoming increasingly mainstream, with an estimated EUR 700 billion in green bonds now in circulation[10].

Listed equity and credit strategies

Investors wanting an approach more directly linked to SDGs may seek out equities or bonds of companies that are demonstrably making a positive contribution to achieving one or more of the 17 goals.

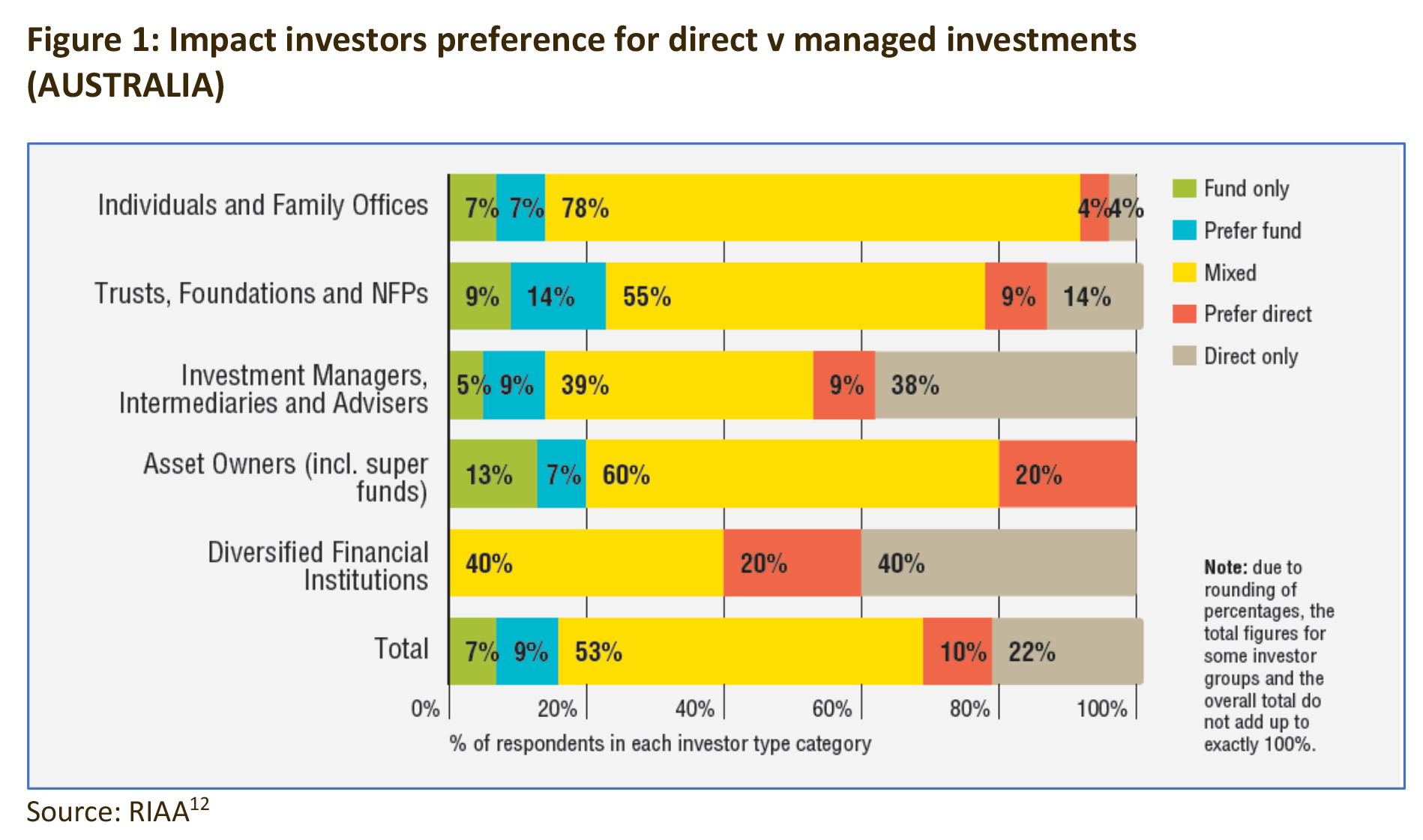

Australian research[11] suggests most investors are equally happy to access such strategies either directly through the underlying instruments, or via managed funds based on these strategies, and to the extent this view is mirrored by investors around the world, it has driven a great deal of product innovation, especially at the retail investor level.

In the direct investment space, some of the innovation has occurred through the development of platforms that make such investments more accessible.

US based CNote[13], for example, allows retail investors to crowdfund impact investments in increments as small as $1.50, whilst in the UK, several asset managers have partnered with the Big Issue to create the Big Exchange platform[14], which offers a choice of around 30 environmental impact funds.

In terms of the managed fund approach, global asset manager Robeco is one of the pioneers in this space and has been offering SDG linked credit strategy products for several years. These strategies, one of which is now accessible to Australian investors, are based exclusively on bonds that, using Robeco’s own framework (described above), have been assessed as having an SDG score of 0 (neutral) or higher. The strategies do not invest in companies that detract from the SDGs. As such, the strategies are designed to make a clear contribution to the SDGs while also aiming to outperform a mainstream corporate bond index or optimize yield and income.

Impact alpha

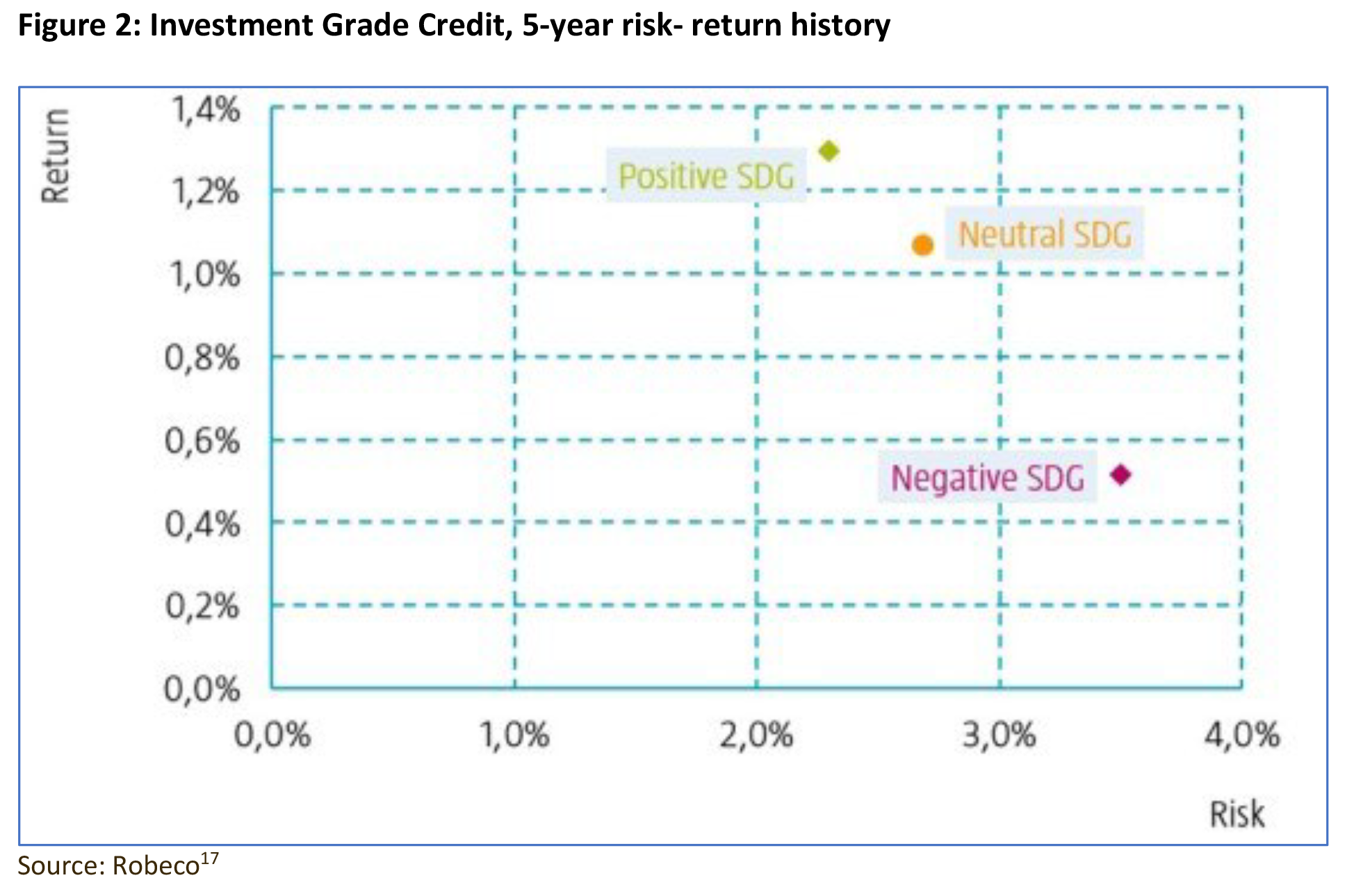

As discussed extensively in the first article in this series, despite perceptions to the contrary, impact investing does not come at the cost of investment performance.

In fact, some experts[15] make an argument that, by considering impact in the investment process, you can actually do better financially; what’s termed ‘impact alpha’.

Portfolio level data from Robeco[16], which includes Covid market corrections, showed credit investments rated as SDG positive delivered higher performance and lower risk than those with neutral or negative ratings over the 5 years to August 2019 (see Figure 2 below).

The role of governments in growing the impact investing sector

Many governments have recognised the role they can play in fostering a vibrant, effective, and accessible market for impact investing.

The UK government for example, has been clear that the supply of retail impact investment products is failing to meet demand, and has pledged to work with leaders in the investment and savings industry to make social investment more accessible to the everyday investor.

In Australia, the Commonwealth Government has several measures in place to support the development of the domestic social impact investment market, although to date their focus hasn’t been at the retail investor level.

2017 saw the launch of the Australian Government Principles for Social Impact Investing, and since the 2017-18 Budget[18], the Commonwealth has announced $57 million in initiatives, including:

- partnering with state and territory governments on social impact investing projects

- developing a Sector Readiness Fund to grow the social impact investing market by providing capability-building grants to impact businesses looking to become investment ready

- building the capacity of the Australian social impact investing sector to measure its outcomes and impacts

- co-designing, implementing, and evaluating payment-by-outcome funding trials in the social services sector, and

- overseeing a number of social impact investing programs that advance the interests of Aboriginal and Torres Strait Islander people, in particular through Indigenous Business Australia (IBA).

The future

Whilst impact investment products (of which SDG aligned investing is a subset) currently account for around $20 billion in FUM (across around 110 products), the potential demand from investors over the next 5 years has been estimated at $100 billion[19].

Innovations in technology and products, coupled with an evolving level of sophistication in measuring and reporting the environmental and social impact of investments will help make SDG aligned investing far more accessible to retail investors.

As the sector grows, Advisers must ensure they develop and maintain a contemporary understanding of its high-level dynamics, the range of solutions available within it, and the evolving motivations of individual investors driving this growth.

———