SDG investing deep dive – understanding consumer motivations and the evolving societal and policy context

Advisers need to meet the growing expectations of their clients to discuss and provide responsible investment solutions.

The Responsible Investing context

On a global level, the increasing focus of individuals, governments, and businesses, on acting ethically and sustainably has been well documented. This focus has manifested itself across many aspects of society, including government policy, business operations, and institutional and individual investment behaviours, fuelling growth in the responsible investment sector that has outpaced other areas of the market[1].

This trend has been mirrored in Australia, with recent research[2] by the Responsible Investment Association of Australasia (RIAA) finding that, during 2020, Responsibly Invested (RI) Assets Under Management (AUM) increased by $298 billion to $1,281 billion, while the AUM in the remainder of the managed fund market decreased by $234 billion to $1,918 billion over the same period.

Underneath the overall RI umbrella fall several investment sub-categories, including ESG-integrated investing, various types of screened investing, and ‘impact investing’ – defined by global asset manager Robeco as “the process of intentionally making investments with the aim of creating a measurable beneficial impact on the environment or society, as well as earning a positive financial return[3].”

Over the 2020 period, impact investing – a popular form of which is targeting companies that can contribute to the UN’s Sustainable Development Goals (SDGs) – also grew strongly, surging 46% over the year to $29 billion AUM, while the number of impact investing products grew[4] over this period from 111 to 145.

Drivers of growth

This fundamental reshaping of the investment landscape is no ‘flash in the pan’, with powerful social, economic, and political forces ensuring it will eventually become the prevailing investment orthodoxy around the world.

Government policy

The extent to which political forces are driving this reshaping of investment markets is certainly more pronounced overseas than in Australia, where government policy is relatively less interventionalist.

By way of comparison, whilst Australia has recently committed to net zero carbon emissions by 2050, this is not legislated. In Europe, on the other hand, member states are legally bound to achieve net-zero emissions by 2050, creating a roadmap for investments in technology and infrastructure that has already driven seismic shifts across many industries.

In the car industry for example, the pressure to bring down vehicle emissions has been given extra impetus by the City of London – one of Europe’s biggest car markets – banning the sale of petrol and diesel cars by 2030. On the expectation that other cities will follow suit, many major car manufacturers have stated their intention to transition to Electric Vehicle (EV) only production in the future. The world’s largest car manufacturer – Volkswagen[5] – have indicated they will go EV only from 2035, whilst Volvo aim to get there 5 years earlier[6].

The implications, and opportunities, for investors are enormous.

In Australia, the EV tide is slowly starting to turn, with a number of new EV policies coming into effect recently to encourage the uptake across government and non-government fleets. For example, NSW and the ACT waives stamp duty on new zero-emission cars, and South Australia has announced a $13.4 million spend on charging infrastructure. NSW is also currently offering a $3,000 rebate to purchases of new EVs (subject to a cap of 25,000 vehicles).

Of course, with more than half of Australians now considering the purchase of an EV as their next vehicle[7], the future growth in sales of electric vehicles in Australia will be driven by bottom-up demand as well as top-down policy, reflecting a growing realisation that a more sustainable approach can often benefit the hip pocket as well as the planet. The opportunity to save on power bills, for example, has seen one in four Australian homes instal solar energy sources, the highest uptake in the world, and the main reason that one quarter of all electricity in Australia is now generated from renewable sources[8].

Consumer expectations

Consumers are also increasingly expecting that their financial services providers will act sustainably and ethically.

RIAA research[9] from 2019 found that 86% of Australians expect their super or other investments (excluding banking) to be invested responsibly and ethically, and 87% expect the money in their bank accounts to be invested responsibly and ethically.

The same study found that:

- three quarters of Australians would consider moving their banking, super or other investments to another provider if they found out their current provider was investing in companies engaged in activities not consistent with their values

- two thirds (67%) of Australians who don’t currently invest in ethical companies, funds or superannuation funds would be most likely to consider doing so in the next 5 years

- recent weather conditions in Australia have prompted 2 in 5 Australians to think about switching financial institutions (banks, super funds etc.) to one which invests ethically or responsibly

- half of Australians say they would be motivated to invest and save more money if they knew their savings or investments made a positive difference in the world

- 54% of Australians believe their own investment decisions can influence the amount of climate change caused by humans.

Consumers have similarly high expectations of their financial advisers, with 90% expecting their adviser to offer them responsible or ethical investment options, and 86% believing that it is important for their adviser to ask them about their interests and values in relation to their investments.

Demographic differences

Notwithstanding the clear growth in demand for sustainable investing at an aggregate consumer level, several demographic groups exhibit especially strong interest:

- female investors

- younger Investors

- High Net Wealth/Worth (HNW) investors.

Female investors

Various studies have shown female investors – from affluent to HNW – are more interested in social and environmental impact investing than their male counterparts. Morgan Stanley1[10] found 84% of females to have an overall interest in social impact investing, compared to 67% of males, whilst BCG[11] found female investors were more likely to rank social responsibility amongst their top 3 investment objectives (Figure 1 below).

Interestingly, female investors are significantly more likely to believe there is a positive association between ESG factors and corporate financial performance[12], putting them ‘ahead of the curve’ in embracing RI.

Younger investors

As has been witnessed throughout history, the behaviours and attitudes of younger generations towards concepts such as career, relationships, and public institutions, are usually markedly different from their forebears. This is also true in investing, where their heightened concerns around the environment, equality, and social justice translate into significantly higher interest in RI.

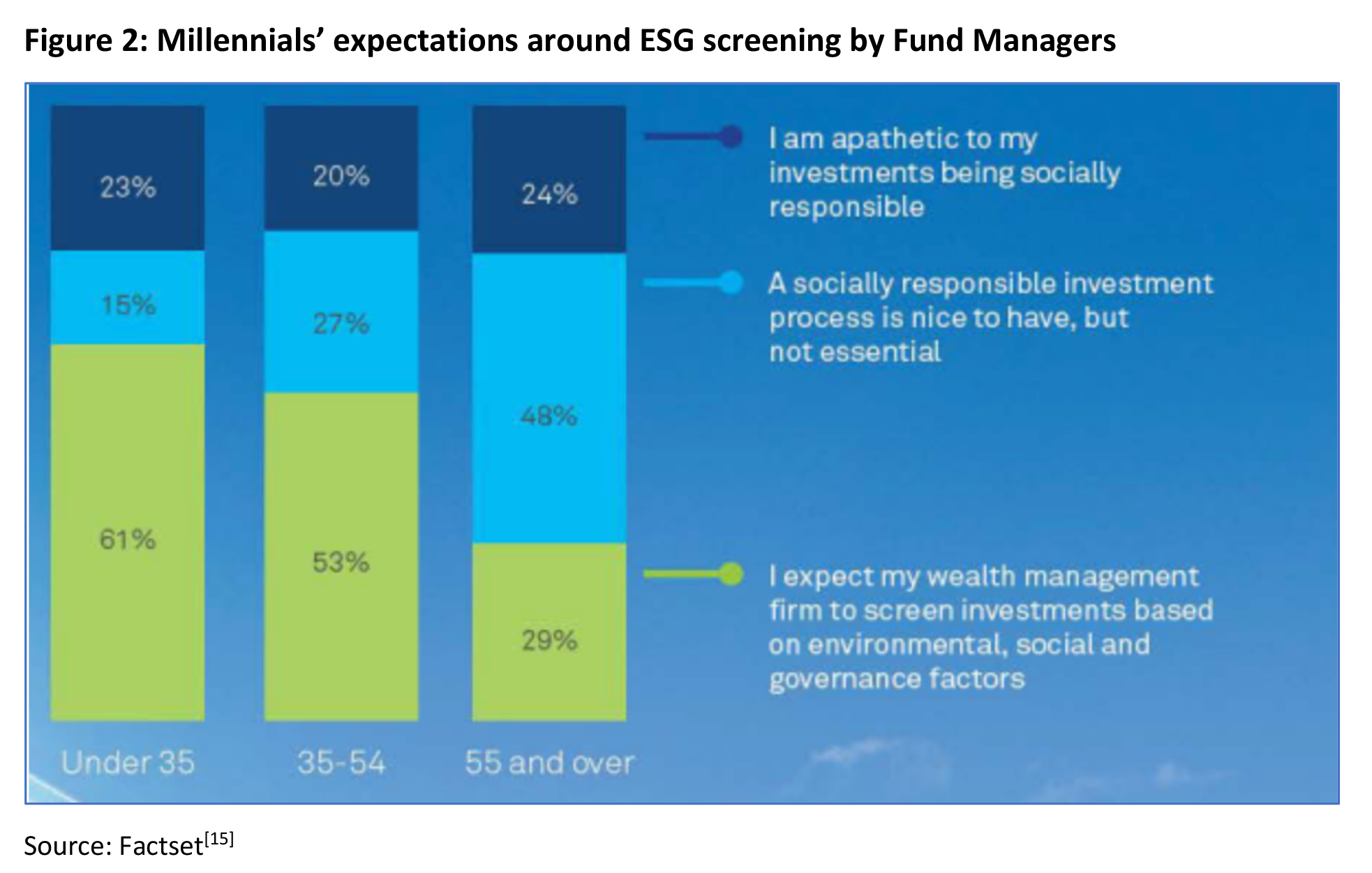

For example, Bloomberg[13] measured millennials’ interest in social impact investing at 77%, compared to just 35% for Baby Boomers. In Australia, investors under 25 were found to be twice as likely as retirees to name ESG/ethical considerations a top three investment consideration[14]. Figure 2, based on US research, shows a similar generational difference in expectations around ESG screening of investments.

HNW investors

HNW investors

According to Capgemini, the world’s wealthy are increasingly putting their money towards socially, ethically, and environmentally conscious businesses, which could spur the growth of sustainable investments.

In their 2020 World Wealth Report[16] more than a quarter (27%) of high-net-worth individuals (those with investible assets of $1 million or more) said they were interested in sustainable products. That figure rose to 40% among ultra-high net worth individuals (UHNWIs), those with $30 million or more to invest.

The same report found that their interest is translating into action, with wealthy investors planning to allocate 41% of their portfolio to businesses actively pursuing environmental, social, and corporate governance (ESG) policies by the end of 2020, rising to 46% by the end of 2021.

Almost half the respondents to an Australian survey[17] of HNW investors said they now choose funds or companies to invest in according to environmental, social and governance (ESG) considerations. More than half (54%) said they avoided investing in companies with controversial track records, while a massive 89% said that fund managers should ‘police’ companies to ensure they act responsibly.

Investor motivations

Investor motivations

Whilst a desire to invest in line with personal values, ‘give back’, and ‘make a difference’ to society, are common motivators for individuals to invest in RI products, they are not the only ones. And there are also significant differences in the specific issues targeted by investors for impact.

At an overall level, environmental issues are closest to the hearts of Australian investors, as shown in Figure 5. Renewable energy, sustainable water management and healthy river and ocean ecosystems are the top three priority environmental issues, and healthcare and education the key social issues.

In terms of preferred ways to impact the environment, differences are apparent across generations. Millennials (25-39 y.o), for example, feel clean and renewable energy sources have the most impact, whilst those aged under 25 feel energy consumption reduction should be the key priority. All other age groups prioritised recycling of non-biodegradable waste as the most important[19].

‘Traditional’ investor objectives – performance and risk management

Perhaps ironically – and contrary to the perception (now lessening) that sustainable investing comes at the cost of lower returns – the biggest catalyst to propel the growth of sustainable investing in Australia may well lie in traditional investment metrics – performance and risk management. Indeed, smart investors have already figured out that sustainable companies are generally better managed and less susceptible to governance failures, and as a result tend to perform better. Similarly, ‘sustainable’ industries are less likely to be negatively impacted by regulatory intervention or falling consumer demand, and also therefore represent better long-term investments.

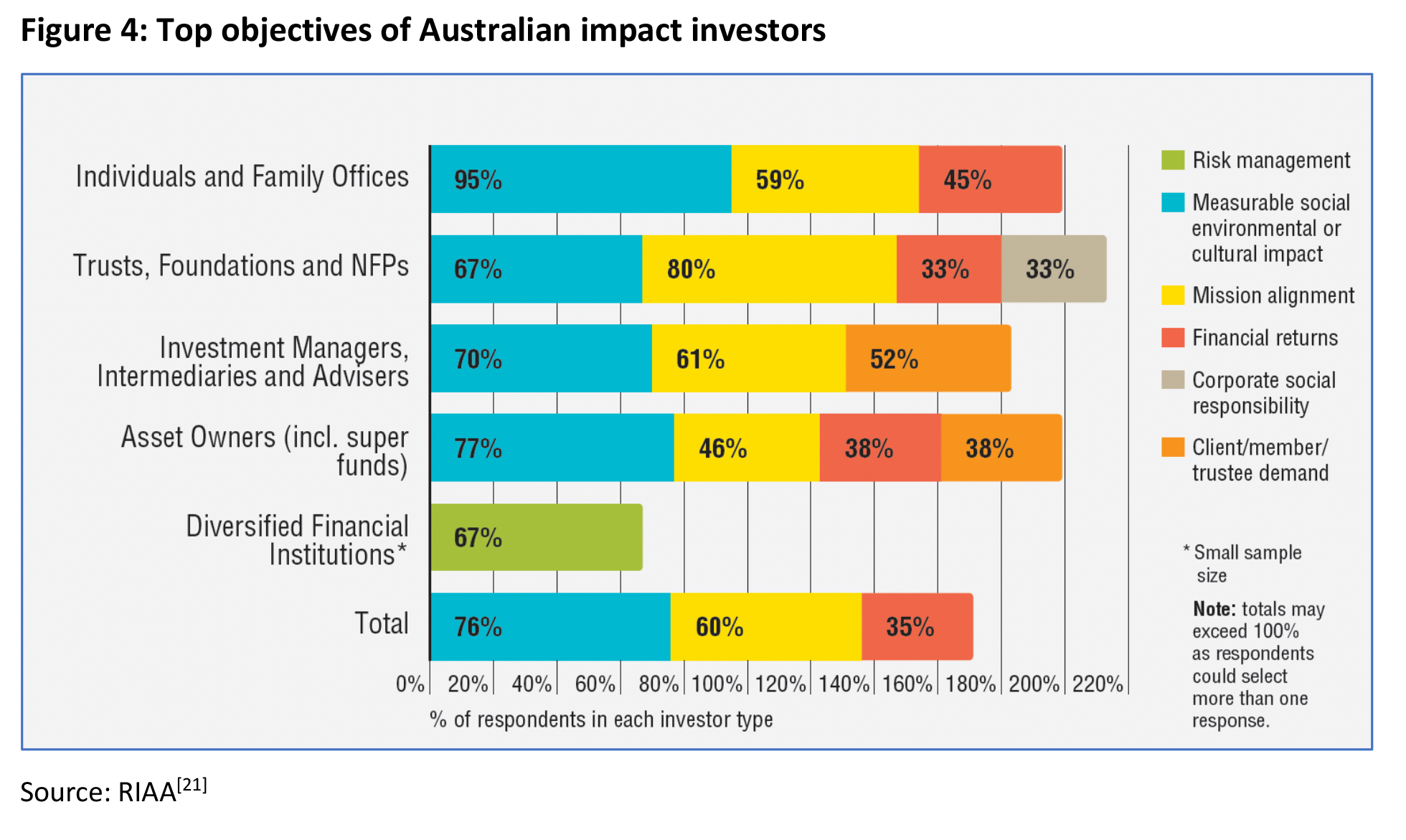

Consistent with this, research by Capgemini[20] found expectations around superior performance to be the number one driver of increased demand by HNW investors in ESG investments, cited by 39% of respondents. Financial returns are also a top 3 motivator for impact investing across various categories of individual, corporate and institutional investor, according to the RIAA (Figure 4).

And their confidence is warranted.

Overseas, Morgan Stanley[22] notes that sustainable funds outperformed traditional peers and reduced investment risk during 2020. Locally, tracking by the RIAA has confirmed the extent to which responsible investment options have outperformed mainstream offerings, over both the short and long term[23].

Against the economic setback of Covid-19, responsible investment funds outperformed both international share and multi-sector growth funds in 2020 and performed on par with the Australia Fund Equity Large Blend category, as shown in Figure 5, below.

Drilling down further into specific RI categories, portfolio level data from Robeco[24], which includes Covid market corrections, showed credit investments rated as SDG positive delivered higher performance and lower risk than those with neutral or negative ratings over the 5 years to August 2019 (see Figure 6 below).

BFID, Fiduciary duty and sustainable investing

Recognition that socially responsible investment is consistent with delivering sound financial outcomes is seen in the embedding of ESG considerations in fiduciary obligations for pension fund managers in Canada, the UK and Europe.

Recognition that socially responsible investment is consistent with delivering sound financial outcomes is seen in the embedding of ESG considerations in fiduciary obligations for pension fund managers in Canada, the UK and Europe.

In Europe, for example, the Swedish parliament introduced reforms in 2018 requiring the four main national pension funds to become “exemplary” in the field of sustainable investment[25]. Mercer[26] estimates suggest 54 per cent of all European Pension Funds are taking climate change into consideration.

In Australia there is no such policy mandate, although many larger superannuation funds are building more sustainable investment frameworks. Whilst this is generally proactive, in some cases strengthening these frameworks are a reaction to member agitation, as was the case with Rest Super, recently sued by a member over its lax approach to climate risk[27].

Some funds have specifically sought to align their investment approach with the SDGs, although all have approached the task differently. Australian Super, for example, has participated in the development of a platform for assessing the SDG impact of individual companies[28]. HESTA[29] has chosen seven SDGs to align its portfolio with: good health and wellbeing, gender equality, clean water and sanitation, affordable and clean energy, climate action, sustainable cities and communities, and decent work and economic growth. NGS Super lists all 17 SDGs on its website and details the contribution it is making towards each through its investing practices and staff action.

Australia’s recent superannuation reforms included the introduction of a Best Financial Interests Duty for superannuation trustees. Given the body of evidence around financial performance, such a duty should strengthen, rather than undermine, the ability of trustees to allocate more funds to sustainable investments.

ASIC ‘greenwashing’ review

The growing consumer interest in sustainable investing makes the spruiking of green credentials a very powerful marketing tool. Unfortunately, there is often a lack of transparency in the link between investments made and outcomes achieved, which companies can exploit by falsely claiming ‘green’ credentials.

The potential for funds to overrepresent the extent to which their practices are environmentally friendly, sustainable, or ethical is referred to in the market as ‘greenwashing’.

Greenwashing is very much an issue in Australia, with the RIAA estimating only about one quarter of the investment managers who say they invest responsibly can actually prove their credentials[30].

There is growing global unease about the risks of greenwashing of financial products, and international regulators have established a Sustainable Finance Task Force that covers greenwashing and other investor protection concerns. ASIC is participating in this task force, and in July 2021 they announced their intentions to conduct a review of environmentally focused investment funds in Australia[31].

Best practice transparency

Advisers seeking to offer responsible investment solutions to their clients should prioritise those investments and fund managers who are able to comprehensively demonstrate their social and/or environmental impact.

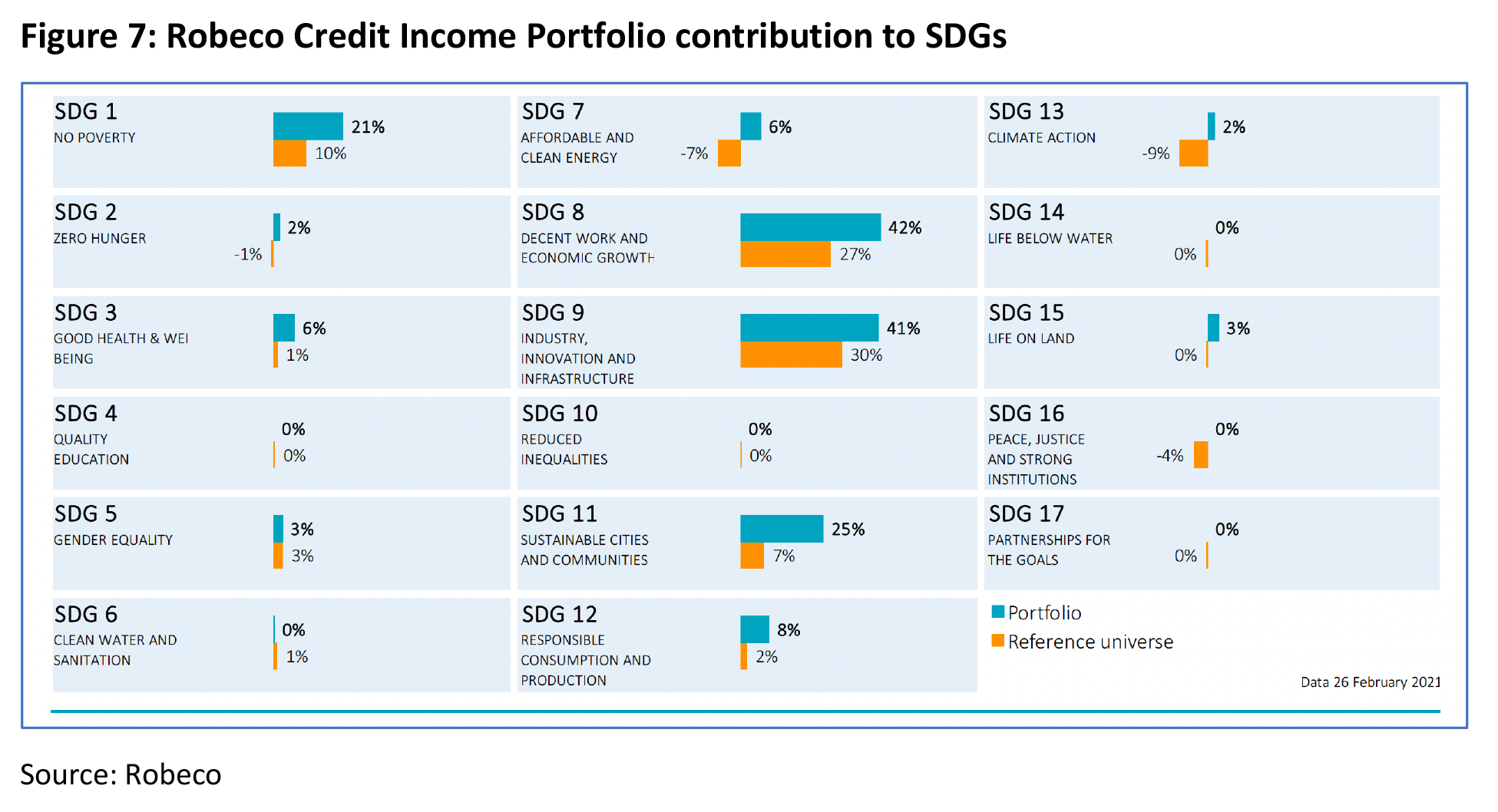

One example of best practice in this area is global asset manager Robeco, who in Australia offer an SDG-aligned credit income strategy.

For the SDG Credit Income strategy, Robeco publishes monthly reports on how the portfolio contributes to the SDGs. As can be seen from Figure 7, an extract from the February 2021 report32, the portfolio contributes the most to SDG 1 (no poverty), SDG 7 (affordable and clean energy), SDG 8 (decent work and economic growth), SDG 9 (industry, innovation & infrastructure), SDG 11 (sustainable cities and communities) and SDG 12 (responsible production and consumption).

Conclusion

In the long run, the desire of future generations to make an impact, the evolution of government policy, and improvements in our ability to map the impact of investments against sustainable indicators will ensure that responsible investing becomes the norm, and terms like ‘responsible’, ‘ethical’ and ‘ESG’ will become redundant.

As we have demonstrated across the three articles in this series, SDG-aligned impact investing is a rapidly growing area, largely driven by consumer demand, and reflecting societal trends and evolving policy frameworks. Consumers increasingly expect their financial adviser to discuss their personal values with them and be able to discuss and offer investment solutions aligned to these values. Advisers should equip themselves to have such discussions now – not to get ahead of the game, but simply to keep up with the way the world is changing.

———