Financial Advice tech – a practical checklist for driving increased efficiency and better client engagement

Advisers will benefit from more actively focusing on their use of technology in their practice.

As the financial advice landscape devolves away from large institutions to smaller, self-licensed entities, advisers and practice principals are increasingly being faced with the need to be far more active in choosing technology solutions for their business. Far from being a burden, this should be viewed as an exciting opportunity, as a growing array of advice software solutions make possible substantial improvements in compliance, efficiency, and customer experience.

In this article we will take a snapshot of adviser technology solutions currently available and examine how they can be incorporated across the advice value chain. We will take an especially close look at developments in regulatory technology (Regtech), collaboration tools, and basic advice process software. And, at a time when more and more client interaction is done away from an office environment, we will also explore best practice in virtual meetings.

Technology as an enabler of better advice

Advisers are increasingly recognising the crucial role of technology in improving business efficiencies and improving the client experience. To the extent that both of these outcomes help make advice more accessible and sustainable, it’s no exaggeration to say technology will shape the entire future of advice.

Across the financial advice landscape, we are seeing a proliferation of technology solutions (many of them advice specific) that are cloud based, easily tailored, and easily integrated, giving the modern advice business far more flexibility to build a ‘tech stack’ to support its own unique business model and client needs.

Technology is being applied to most aspects of the advice value chain, including:

- document production and storage

- workflow management

- compliance and risk management

- onboarding and ongoing client management

- financial and investment reporting

- marketing

- client engagement and communication

- customer satisfaction tracking

- cybersecurity; and

- HR.

Solutions that are becoming increasingly popular with more innovative advice businesses include:

Information gathering and scoping tools

Providers like Astute Wheel, My Prosperity and Finametrica are revolutionising the initial client engagement process, making steps like fact finding and risk profiling quicker, more accurate, and more convenient for clients. By cutting out the reliance on hardcopy forms, and instead allowing clients to self-complete a variety of documents in real-time, meaningful time savings are possible, and a digital audit trail allows more robust and consistent compliance.

Workflow

A growing number of platforms are being built specifically for Australian financial planners, helping them to drive efficiencies in record keeping and client communication. Such platforms can be particularly valuable in automating processes such as document management, Fee Disclosure Statements (FDS) and opt-in. One platform growing in popularity is Worksorted, which recently announced an integration with digital fact-finding software Advice Revolution.

Worksorted also acts as a revenue management solution, and as a CRM, competing with established providers in this space such as AdviserLogic, Midwinter and Xplan.

Cash flow modelling

According to research, almost a third[1] of advice practices use cashflow, budgeting and account aggregation tools for client advice. Cash flow modelling software has multiple applications and is used by advisers offering cash flow and budget management as part of their advice offering, as well as by those offering life insurance advice who need to do long term budget projections to verify the future affordability of cover. Popular options here include MyProsperity (which offers free and paid options), MoneySoft, Xero, and MoneyBrilliant.

E-learning and education platforms

Advisers seeking to digitise their approach to financial literacy – either one on one or one to many – are turning to a number of market solutions. Options such as Thinkific and Kajabi provide users with customisable templates to create engaging content in the form of online courses or coaching programs. Advisers can choose to make these available only to their clients, or to a much broader audience. Some solutions also offer the opportunity to commercialise this content, allowing advisers to maximise the value of their intellectual property by opening up new, non-traditional revenue streams (e.g., selling online courses).

Survey and client feedback tools

Monitoring customer satisfaction by gauging feedback is critical to driving a loyal, engaged, customer base. A variety of tools automate the process of designing and sending surveys, and summarising responses to create meaningful, actionable insights. Survey Monkey is one of the most popular tools here, along with the increasingly important client rating systems, such as Adviser Ratings, Google Reviews and Trust Pilot. Customer reviews are a critical factor in the online search process, and advisers should see asking for a review as the modern equivalent of asking for a referral.

Digital signature tools

The COVID related shift to remote working and virtual engagement has proved a significant catalyst in the uptake of digital signature tools, with more than half[2] of advisers using tools such as DocuSign, Adobe, and MyProsperity to capture handwritten or digital signatures via computer or mobile device. The advantages in streamlining administration are obvious, as are the customer convenience benefits.

Email marketing, newsletters, and customer communication

A variety of solutions are available to automate the creation and distribution of electronic customer communication, including emails, newsletters, and SMS messages. Such tools typically also allow a degree of customisation and personalisation and offer in-depth reporting tools to help track open rate, readership, and other relevant metrics. The most widely used option by Australian advisers is currently Mailchimp[3], with Xplan and Worksorted also proving popular.

RegTech in financial advice

Whilst many of the solutions mentioned above make aspects of compliance easier for advisers, there is a growing number of platforms developed specifically to aid compliance. This Regulatory technology (RegTech) uses software and data to support compliance and is proving increasingly integral to meeting the regulatory cost burden faced by financial advice.

Technologies used across the growing RegTech ecosystem include Artificial Intelligence (AI), big data, data visualisation, machine learning, blockchain, and APIs.

RegTech can be used to streamline compliance in areas as diverse as product documentation, marketing, client communication, knowing your customers, cyber security, and anti-money laundering.

Marketing compliance software like Red Marker can identify legal and brand risks in documents and websites. PDF-to-digital technologies can help advisers capture and audit content from thousands of PDF documents, and voice data analytics providers can record conversations to pick up on the nuances of customer interactions, allowing greater transparency, in an aggregated form, on the quality of those interactions. Automating processes such as opt-in, FDS, identity verification, and the use of AI to scan SOAs, are increasingly becoming mainstream.

Whilst much RegTech has been developed for use across multiple industries, there is a growing number of solutions developed specifically to support financial advisers and licensees, such as those offered by Fourth Line, TIQK, and Advice RegTech, to name but a few.

Social media management tools

Social media management tools can boost practice efficiency by permitting individual posts to be easily posted across multiple platforms (Facebook, LinkedIn, Instagram etc). Such tools also allow posts to be scheduled, meaning they can be pre-loaded in advance and then released at a pre-determined time and frequency. The reporting from these tools also provides deep insights into the performance of your activity, allowing it to be fine-tuned. For those practices who don’t outsource their social media management, the most popular platforms are Hootsuite, Buffer, and Zoho.

Virtual client engagement

In 2015, the McKinsey whitepaper[4] – The Virtual Financial Advisor: Delivering Personalized Advice in the Digital Age – observed that “Consumers increasingly use Skype or FaceTime to discuss personal matters and connect with friends and family globally. It is only a small leap to imagine a couple using the same tools on a Saturday morning to receive personalized financial advice without leaving the comfort of their living room.”

Fast forward to 2021, and, courtesy of a pandemic-shaped catalyst, virtual client meetings are the norm, not a novelty.

For most advisers and clients, this is a highly positive development.

From the client perspective, the convenience is hard to overstate. They no longer have to factor in travel time to and from the adviser’s office, nor deal with the stress of what to wear or wear to park.

Virtual meetings – shorter, more focused, and less likely to be cancelled

From an adviser perspective there is now the flexibility to hold meetings from non-office locations, outside traditional hours, and without the normal support staff that may be needed in an offline world.

To the extent that people expect – and even prefer – virtual meetings to be shorter and more focused, advisers can engage with more clients on any given day, and increase the frequency of contact: for example, exchanging a 60-minute quarterly meeting to monthly meetings of 20 minutes each (which may be more useful at keeping the client on track).

Shorter virtual meetings will also reduce frequency of clients cancelling meetings at short notice due to sick children, inclement weather, or transport woes. If the meeting involves them staying at home, those excuses disappear!

Virtual meetings can strengthen the emotional connection between client and adviser

While some advisers assume virtual meetings create a barrier to personal connection, research suggests the opposite. A study5 for the US Journal of Planning examined the experience of ‘teletherapy’ and the implications for financial advice. The study found that the lower barriers to entry of virtual meetings (both emotional and logistical) can actually make them more effective than physical meetings in addressing the client’s emotional needs. (The ability of clients to meet from the comfort of their own home was found to be therapeutic in itself!)

Tips for better virtual meetings

While the efficiency and client engagement benefits of virtual meetings are clear, not all advisers have fully optimised their approach in this area, with many falsely assuming the same meeting structures and materials that worked offline will also work online. Similarly, many undermine the customer experience by failing to take account of issues such as lighting, sound quality, and the general aesthetics of virtual meetings.

Happily, there are some quick and easy tips you can follow to make your virtual client meetings more engaging, professional, and productive:

1. Choose your platform and understand how it works

Zoom remains the most popular online meeting platform with Australian advisers, at around 90% usage, followed by Microsoft Teams, Skype, and GoTo Meeting[6]. While all these platforms have similar functionality, there are minor differences in each. Make sure you fully understand the commonly used functions of your chosen platform, especially around screensharing and recording.

2. Make sure your client knows how to use your chosen platform

Small differences in functionality and user experience between different platforms can be stressful for some clients who aren’t familiar with your chosen platform. Make sure you write up simple instructions on how to access and use the platform and email them to your clients well before the meeting. Also show a little patience if you need to coach your client in the middle of a meeting.

3. Invest in quality hardware

Although they are convenient, built-in microphones and webcams are generally of a lower quality. A few hundred dollars invested in quality external cameras and microphones, and perhaps even some ring lighting, can elevate your visual presence and the quality of the meeting enormously. Such items are easily found online or instore at places such as Officeworks or JB Hifi.

4. Think about security

Be careful how widely you share meeting links. In the case of Zoom, avoid sharing your Personal Meeting ID via public forums, lest you attract uninvited guests. Instead use the waiting room and Personal Meeting ID random generator to have better control over who comes and goes.

5. Back up plans

Have a back-up plan in case your Wi-Fi or video quality is patchy or the platform crashes. (Audio calls might be one such contingency.)

6. Avoid distractions – you and your clients

Research[7] suggests we are easily distracted by our own face. Depending on your platform you can choose to turn off your ability to see yourself, or at the very least minimise yourself and instead make the client(s) the main focus on your screen. Help your client stay focused by encouraging frequent interaction, and by adapting any presentations to a virtual context (see below).

7. Optimise your location

If you are using Wi-Fi, ensure you are in a spot with a strong signal. Also pay attention to the sound quality – carpet makes for better acoustics, as does a quiet location. Having a window behind you is generally not recommended as it can play havoc with the lighting. Ideally your background should be plain enough that people aren’t distracted by what’s over your shoulder, but not so plain you look like you are in a prison cell.

8. Avoid virtual backgrounds

Virtual backgrounds make you look weird, and like you are hiding something. People find them very distracting.

9. Make eye contact – try to look at the camera

Even in a virtual context it can be a bit off-putting if we feel eye contact isn’t being made. As hard as it is, try to ensure you are looking at the webcam. One tip to make this easier is to position the screen view of your client right next to your camera. This way, watching them will mean you are almost looking ‘direct to camera’.

10. Have an agenda and let the client know in advance

Virtual meetings can go off track too. An agenda will help keep you focused and sending it well in advance will help your client with any preparation they may need to do.

11. Adapt materials for a virtual environment

One of the biggest traps we can fall into with virtual meetings is assuming the same documents and presentations work online as they do offline. They don’t.

Word documents and PDFs full of technical language can be very hard to navigate on a screen and can be quite distracting.

If you are screen sharing technical documents, consider shortening where possible into e-books or flipbooks to make the on-screen experience easier. Try to add some colour and graphics too.

There are a variety of software solutions – many of them free or low cost – that can help you turn PDFs into flip books. Popular choices include Canva, Designrr, Issuu, and even Google Docs.

The same applies to PowerPoint presentations. According to research[8], people have an attention span of around 10 minutes for presentations, and the optimal length is about 10 slides. In a virtual context you really need to dial up the colour and graphics, with no more than a quarter of the slide devoted to text.

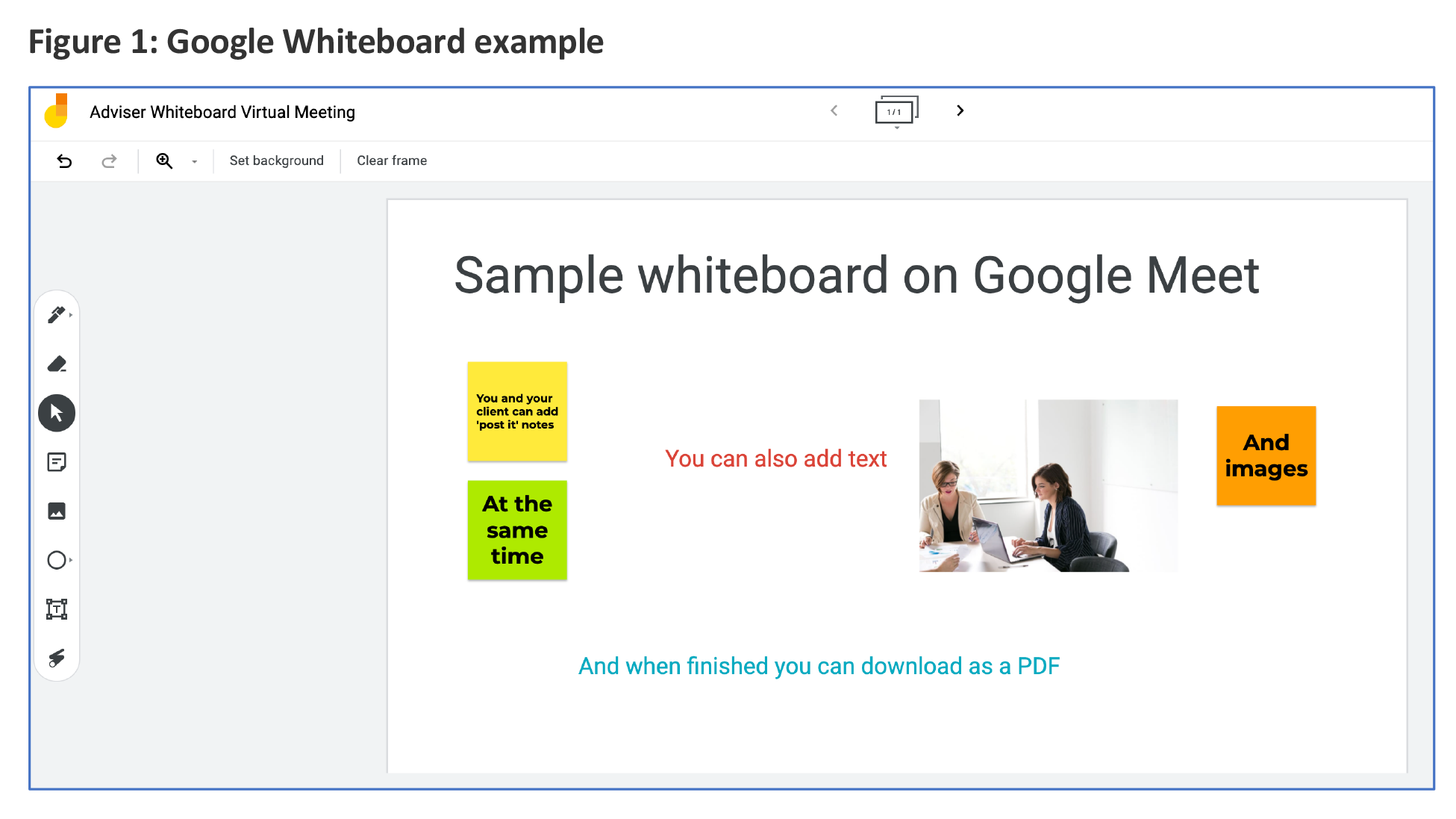

12. Use the whiteboarding functionality embedded in many virtual meeting platforms

The whiteboard is a trusted friend to many an adviser. The great news is that platforms such as Zoom and Google Meet include in-built whiteboarding and other collaborative functionality (also available through dedicated collaboration software like Miro). These tools allow you and your clients to simultaneously write on, or add notes to, the same whiteboard, and can encourage more interactivity and focus from your client.

Summary

As the advice landscape continues to evolve away from large institutional licensees to smaller and boutique self-licensed firms, advisers are finding themselves with more control over their own destiny and more license to build a business in their own way. At the same time, we are seeing the proliferation of new technological solutions that can help drive improved efficiency, compliance, and client engagement. No longer dictated to in terms of technology solutions, the new breed of entrepreneurial adviser can choose from an array of platforms across the advice value chain, and which can be tailored to the unique needs of individual practices. By providing a brief snapshot of the current advice tech landscape, this article aims to help deepen advisers’ understanding of the options available, and where and how each can add value and help create more sustainable businesses and more engaged customers.

———