Weekly economic and market update – week ending 3 December, 2021

Investment markets and key developments

Global share markets had another rough week as uncertainty around the impact of the Omicron variant on global growth and Fed Chair Powell flagging a faster taper led to a bit of a roller coaster ride. While Eurozone shares are up slightly for the week and Chinese shares are flat, US and Japanese shares are down. The week global lead and news of the arrival of Omicron in Australia pushed the Australian share market lower led by sharp falls in health, IT, consumer staple and property stocks. 10 year bond yields fell on safe haven buying and a concern the Fed may start to tighten too early. Iron ore and copper prices rose slightly but oil fell on concerns about the growth outlook with OPEC agreeing to proceed with a supply increase in January but subject to Omicron’s impact on demand. The Australian dollar fell further on global growth concerns and as the $US rose slightly due to safe haven demand and expectations for a faster Fed taper.

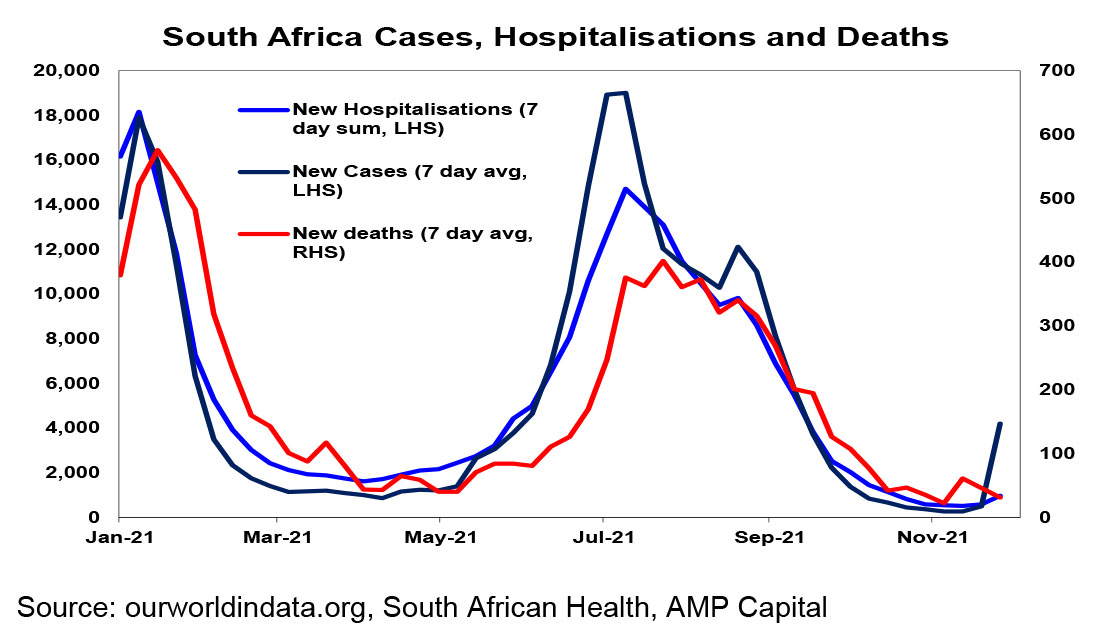

It’s still too early to know how big a problem Omicron is. While its clearly more transmissible than Delta with a higher risk of reinfection and has rapidly spread globally its still not known if it results in more or less severe infections and how significant the impact will be on vaccine effectiveness. So far it seems to have resulted in mostly mild cases in South Africa but this is just anecdotal, it may be because its mostly infected younger people and given the lags it could be too early to tell the true picture. Hospitalisations are picking up again in South Africa but its early days yet in in the Omicron wave. And while the head of Moderna said new vaccines would be needed given the number of mutations in Omicron, the makers of the two other main vaccines indicated existing Pfizer & AZ vaccines should still provide some protection against serious illness. If it turns out Omicron is more transmissible but results in milder cases, then it could come to dominate the other variants and turn out to be a good thing. So, share markets would quickly rebound as it could speed the end of the coronavirus threat (the Optimistic Case). If alternatively, it is more transmissible, results in more severe cases and new vaccines are needed which will take at least 3 or 4 months then share markets could have much more near-term downside (the Pessimistic Case). Ultimately though this downside is likely to be limited and turned around as central banks and governments would yet again provide more support (prioritising growth over inflation concerns). Of course, there could be variations in between these two scenarios. We should get a better idea in the next week or two.

Fed Chair Powell ditches “transitory” and flags a faster taper decision at its December meeting, but much will depend on Omicron. While Powell seemed to flip between leaning dovish one day in his prepared remarks to Congress to hawkish the next the shift to a faster taper had been flagged by various Fed officials over the last two weeks. As we noted last week this could clear the way for a rate hike mid next year. However, the Fed meeting is still two weeks away and much will depend on what we learn about Omicron between now and then. If it turns out to result in more severe cases against which existing vaccines are far less effective, then a decision on a faster taper will be pushed into next year. Either way we will still be a long way from tight US monetary policy and the ECB, BoJ and RBA are lagging the Fed.

In other US policy developments, Congress passed another stop gap funding bill averting a Government shutdown, but resolving the need to raise the debt ceiling is tied up with the passage of the Build Back Better bill in the Senate and so may not be resolved till later this month or early next year.

Meanwhile there are more signs that we are seeing some easing in supply bottle necks with the Baltic Dry index and commodity prices well down from their highs, the US ISM index showing some decline in order backlogs, supplier deliveries and prices paid and China’s PMIs showing reduced input prices. And while the inflation spike has gone beyond what the Fed originally meant by transitory and is likely to continue for a while yet, it should start to slow by the second half of next year.

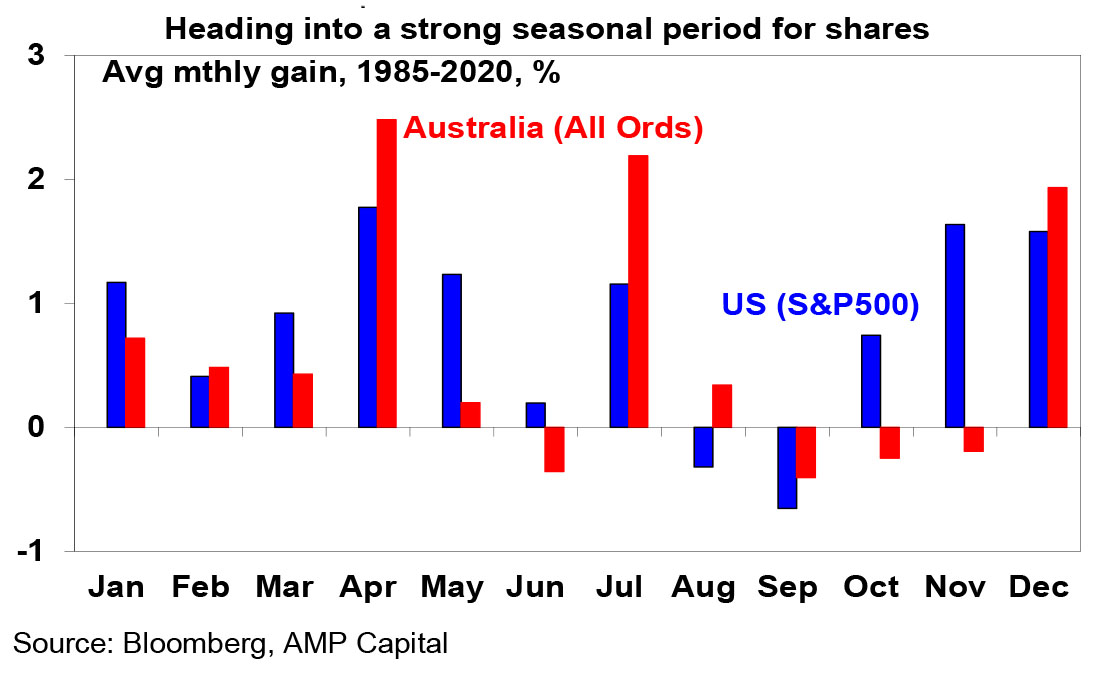

So far, the 5% or so pull back in share markets just looks like a normal correction after markets had become overbought again. Historically share market seasonality turns more decisively positive in December, particularly from mid December. Of 22 cases of negative Novembers in the US share market since 1950, 19 were followed by gains in December. Of course, much will depend on Omicron as noted above.

Elvis from Hawaii via Satellite. 1973 was a major highpoint in Elvis’ career with his Hawaiian concert beamed via Satellite around the world and watched by an estimated 1 billion people (although they may not have watched it all at once). Apparently Elvis wanted to go on a global tour but Colonel Tom Parker his manager talked him out of it because the Colonel didn’t actually have US citizenship so feared he would be not be allowed back in. Hawaii was chosen because of its suitability for beaming into the Asian time zone. Given the risks associated with the technology back then (no one had yet beamed a live full concert around the world) a “rehearsal” version was first filmed for use if a problem occurred with beaming the live version. Both are now available, and some might say it’s a bit hard to tell them apart. The highlights would have to be Something and Suspicious Minds. A few years ago, in Adelaide I met a lady who actually went to the concert as a child because her father was working on the Ala Moana shopping centre in Honolulu and the construction company gave the workers tickets to attend the concert. Now that would have been something!

Coronavirus update

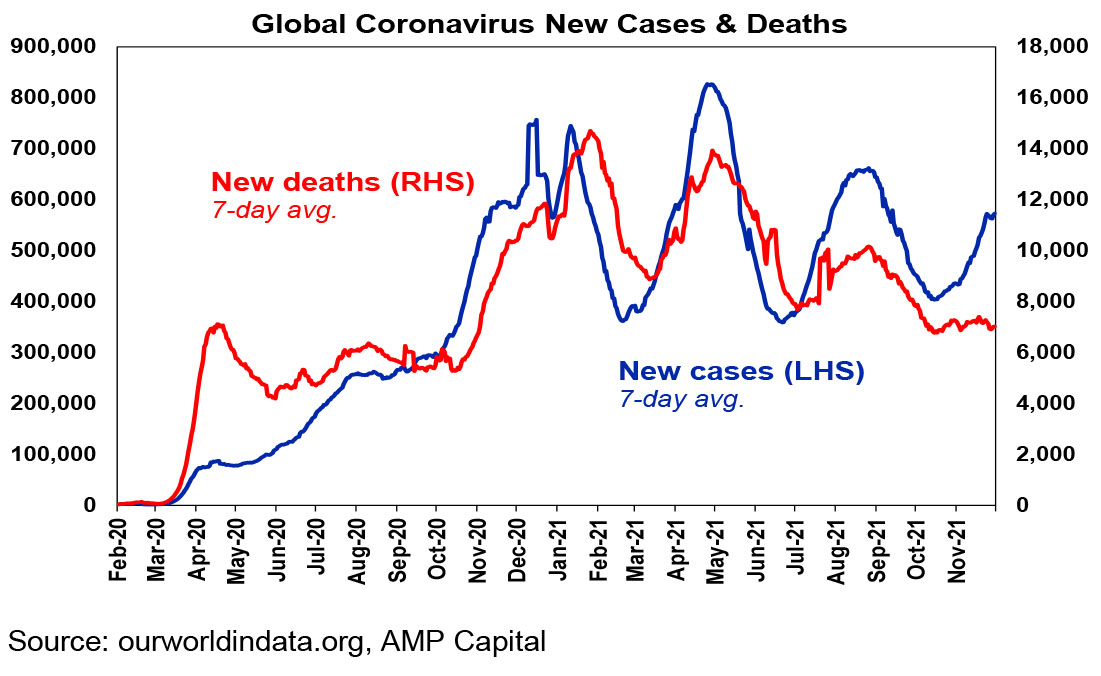

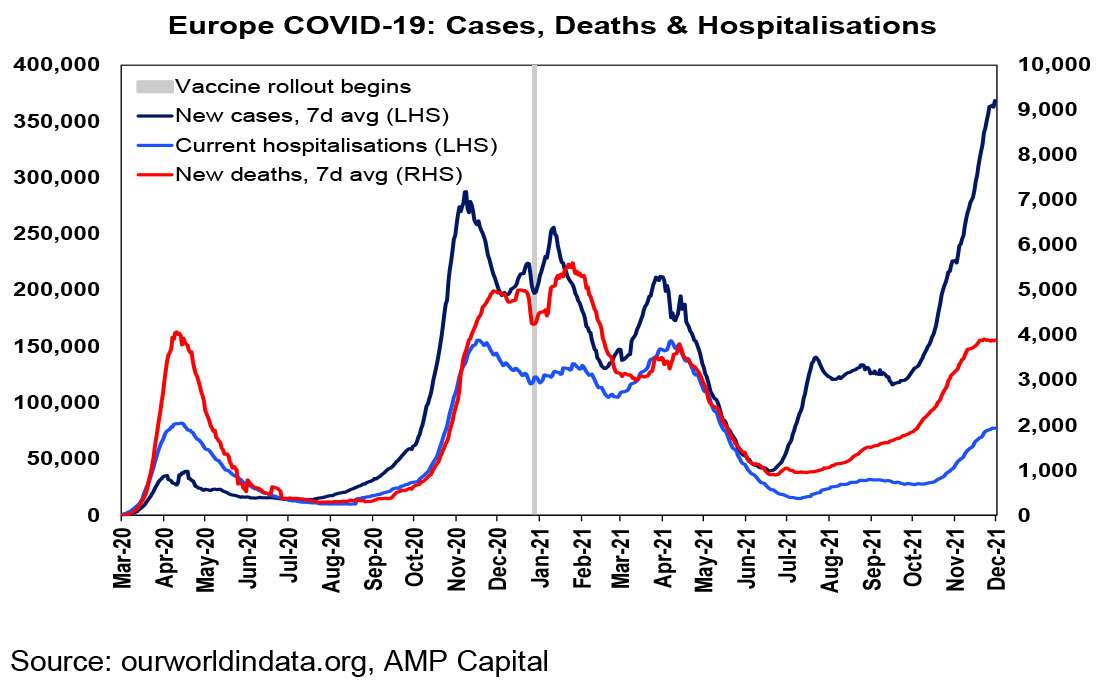

Global coronavirus cases remain in a rising trend but showed some slowing over the last week. Deaths so far remains subdued compared to previous waves. Its still very early days in the Omicron wave though.

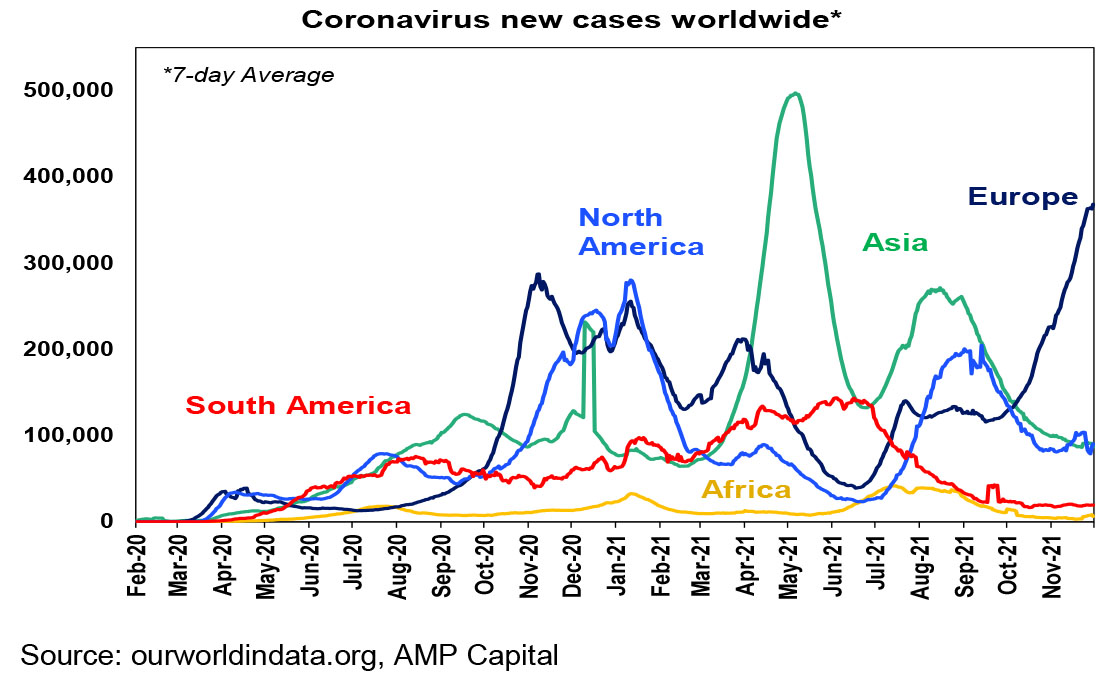

Most of the surge has been driven by Europe – although it’s slowed a bit in Germany, Austria and the Netherlands but with France, Italy and Spain picking up. US numbers have flattened out a bit but its too early to tell given the onset of winter, relatively low vaccination rates and entry of Omicron. Africa is starting to pick up with Omicron, but from a low base.

The key to the threat the latest wave poses to the economic outlook remains whether vaccinations are successful in keeping hospitalisations down such that hospital systems can cope without lockdowns. The level of hospitalisations is also the key issue in relation to the new Omicron variant. So far hospitalisation and death rates in Europe remain subdued relative to the wave a year ago. This is also the case in the UK where hospitalisations and deaths are actually trending down.

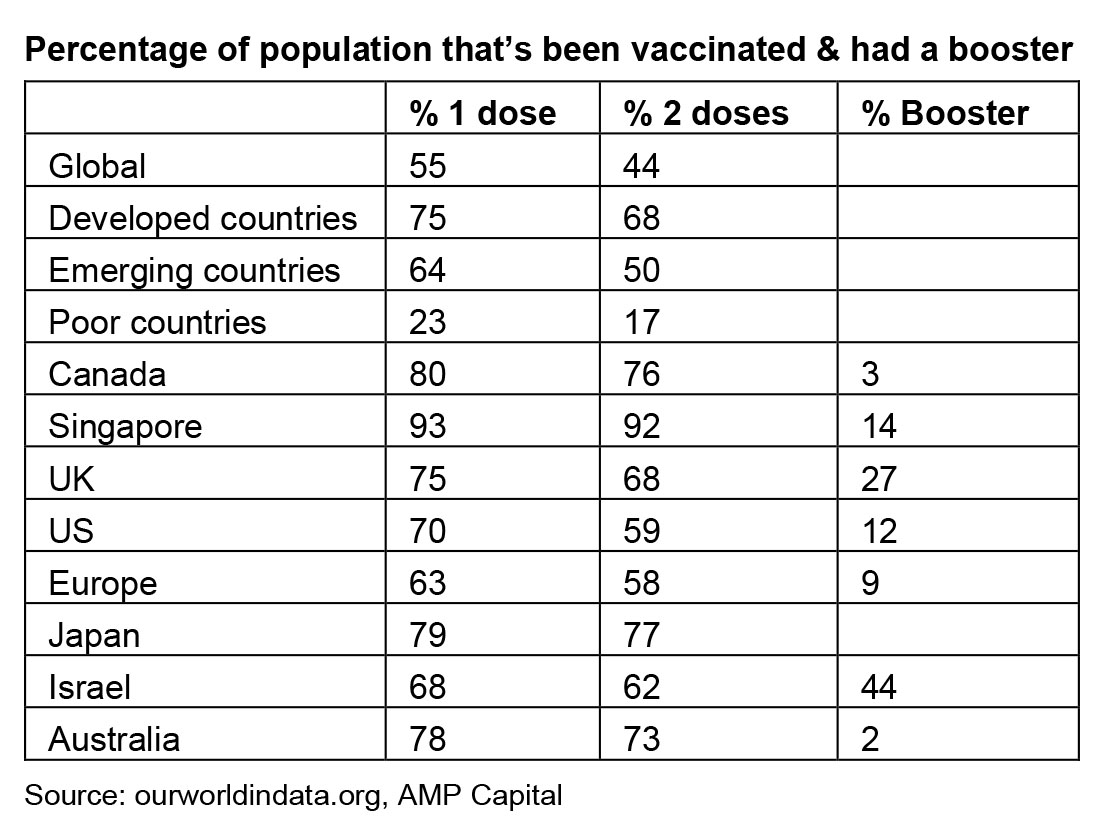

55% of people globally have had one vaccine dose, 75% in developed countries and only 23% in poor countries. While vaccine efficacy against Omicron is not yet known, a key problem beyond that is that vaccination rates in Europe and the US remain low and the very low vaccination rates in poor countries leave open a high risk of further mutations. So it remains in the interest of developed countries to help poor countries vaccinate as quickly as possible. Germany is also joining Austria in moving to make vaccines mandatory.

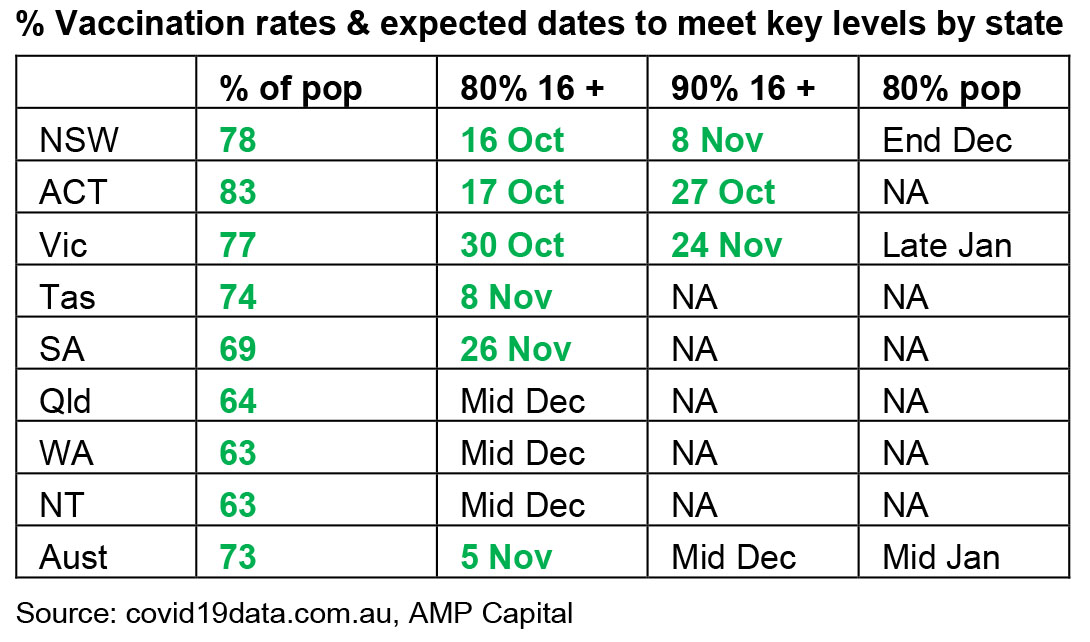

Australia at 78% of the population with first doses and 73% with second doses is at the high end of developed countries. On current trends Australia will average 80% of the whole population fully vaccinated around mid-January. New coronavirus scares and the likely approval of vaccines for 5 to 11 year olds should take the percentage of the population fully vaccinated well beyond 80%.

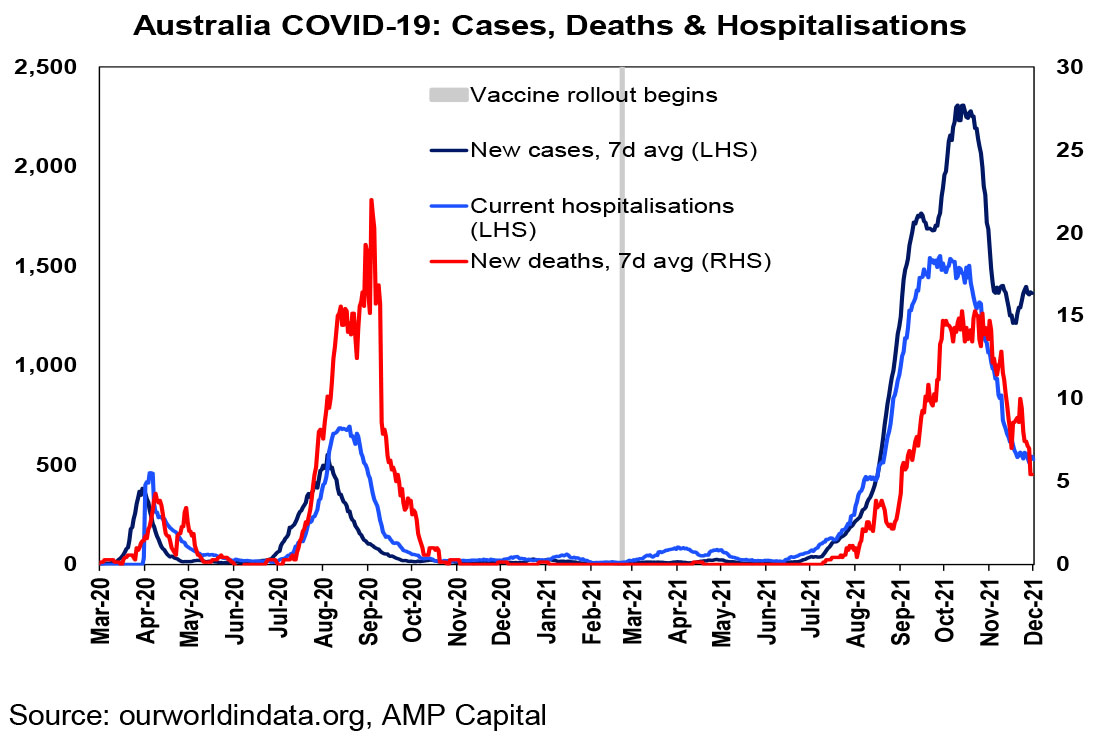

A resurgence in new cases in Australia looks almost inevitable given the experience of other countries and with the likely more transmissible Omicron variant now spreading in Australia. In fact, cases are already starting to trend up again. But the key will be if vaccines help keep hospitalisations subdued such that the hospital system is not overwhelmed. At present new cases are up from their lows but hospitalisations and deaths remain subdued.

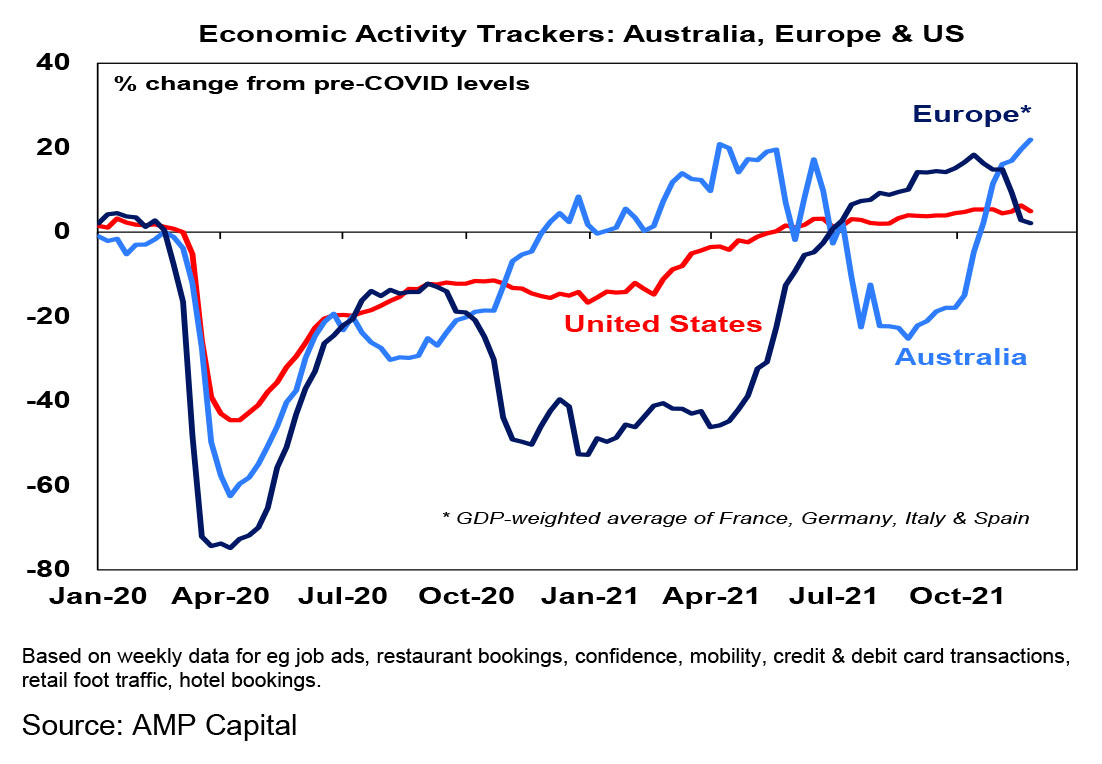

Economic activity trackers

Our Australian Economic Activity Tracker rose again over the last week with broad based gains on the back of reopening and is now just above pre-Delta levels. The rebound in our Economic Activity Tracker reflects a resurgence in mobility, credit and debit card transactions and restaurant and hotel bookings amongst other things and points to points to a very strong rebound in Australian GDP this quarter. By contrast our European Economic Activity Tracker fell again in response to rising cases and restrictions in Europe and our US Tracker also fell slightly. Lockdowns or not, fear of Omicron is the main risk going forward.

Major global economic events and implications

US data remained mostly strong over the last week. While consumer confidence fell the ISM manufacturing conditions index rose and remains very high, jobs data was strong, pending home sales rose and home prices continue to rise solidly. The Fed’s Beige Book referred to “moderate to robust” price increases which were widespread across the economy but the ISM survey also showed some easing in price pressures albeit from very high levels.

Eurozone economic sentiment remained around 21-year highs in November despite the rise in coronavirus cases and unemployment fell to 7.3% in October. CPI inflation rose further to 4.9%yoy in November with core inflation rising to 2.6%yoy but the rise is narrowly based with the trimmed mean measure of inflation remaining very low. Producer price inflation surged a whopping 21.9%yoy in October although this in large part reflects a 62.5%yoy increase in energy (mainly gas) prices

Japanese jobs data was soft and industrial production fell, but both should strengthen as covid restrictions have been relaxed.

Chinese business conditions PMIs were mixed with the official PMIs rising but the Caixin PMIs down. The overall picture suggests growth may have stabilised. There was also a sharp fall in manufacturing price components suggesting producer price inflation may have peaked.

Asian manufacturing conditions PMIs saw a broad-based improvement with their average rising to a seven month high.

Australian economic events and implications

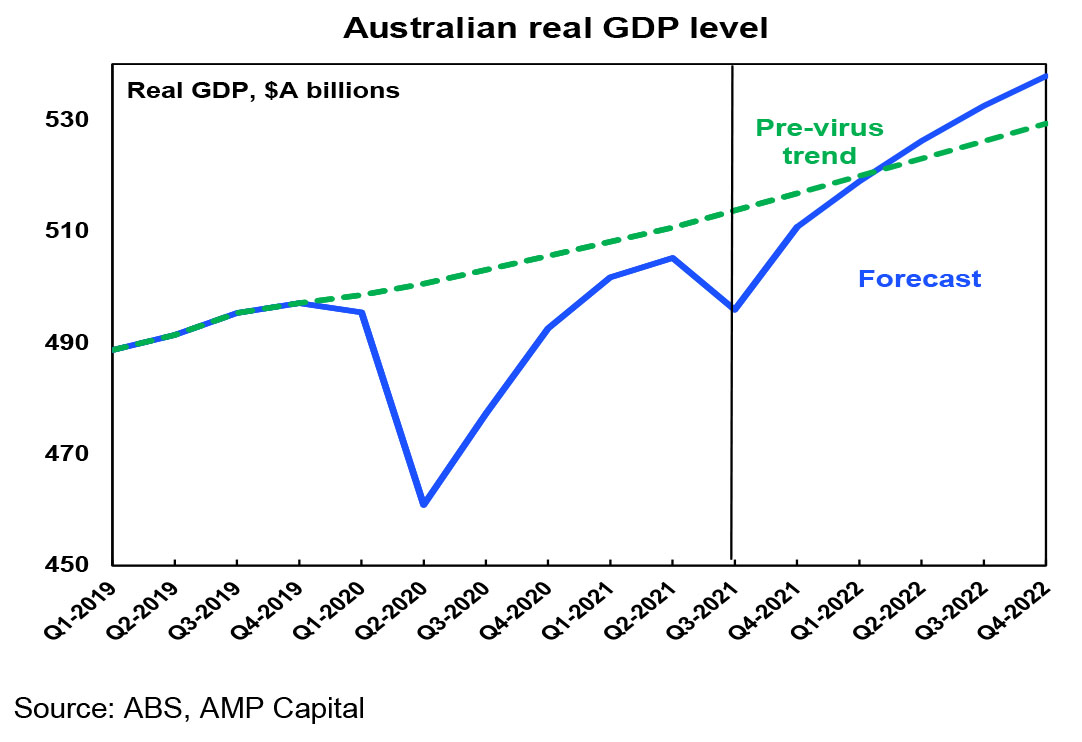

Australia GDP fell less than expected in the September quarter and looks to be recovering rapidly. While September quarter GDP data showed the third largest quarterly hit to the economy on record it wasn’t as bad as the 4% slump we expected earlier in the lockdowns. While its painful, consumers and businesses have found better ways to manage through lockdowns resulting in a smaller hit to economic activity and public spending and other states provided an offset to NSW, Victoria and the ACT. As noted earlier, our weekly Economic Activity Tracker shows that economic activity is now rebounding rapidly. And there is good reason to expect strong growth through next year of around 5.5%yoy: the savings rate has rebounded to 20% and there is now roughly $250bn (or 13% of GDP) in excess savings built up through the pandemic which will spur future consumer spending; business confidence is high and investment plans point to 15 to 20% growth in business investment; and some pre-election Government spending is likely to add to fiscal stimulus through next year. This in turn is likely to lead to a tighter jobs market and higher wages growth than the RBA is expecting through next year resulting in the start of rate hikes around November. The main threat would be if Omicron turns out to be more deadly than Delta with vaccines offering little protection resulting in a return to lengthy lockdowns, or people cutting back on their mobility anyway out of fear, until new vaccines come along and are distributed resulting in another year of disrupted growth.

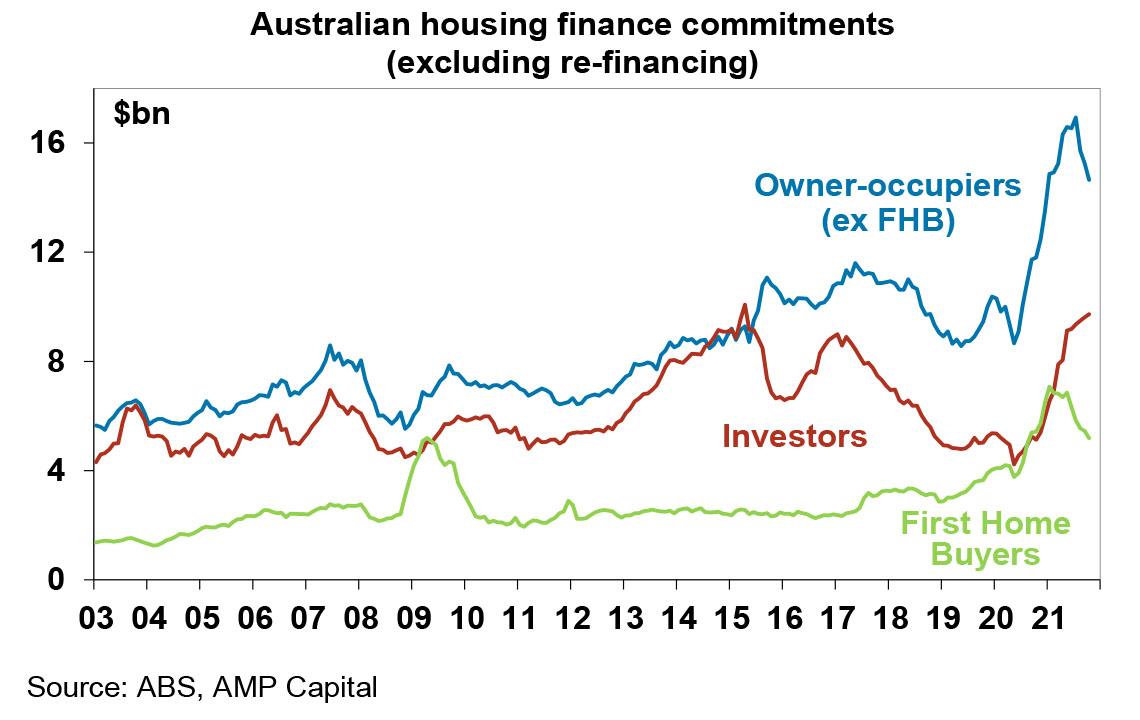

More slowing housing indicators. The housing sector led the recovery but its now clearly slowing down with building approvals, new housing finance and housing credit growth slowing in October and national home price growth slowing further in November. While CoreLogic data showed a 22% rise in prices over the last year, the monthly growth rate slowed further 1.3%mom and as a result of worsening affordability, rising fixed rates, tightening lending standards, rising listings and a rotation in spending back to services we see home price growth slowing to 5% next year ahead of a 5 to 10% decline in 2023. As can be seen in the next chart housing finance going to first home buyers and other owner occupiers is now slowing as more potential buyers are being squeezed out by worsening affordability. Investor finance has pushed up to around its 2015 high though as investors are less affected by affordability.

The trade surplus fell further in October but remains high at $11.2bn. The value of iron ore exports fell as lower prices impacted, but this was partly offset by coal and gas exports.

What to watch over the next week?

In the US, CPI inflation (Friday) is likely to show another lift for November with headline inflation rising to 6.7%yoy and core inflation rising to 4.9%yoy. Job opening and hiring data for October (Wednesday) is expected to show a continuing tight jobs market.

In China, trade data for November (Tuesday) is expected to show some slowing in export growth but strong imports and CPI inflation (Thursday) is expected to rise to 2.5%yoy due to base effects but PPI inflation is likely to drop below 12%yoy.

In Australia, the RBA is expected to leave rates on hold and reiterate its dovish guidance on rates. It only removed the 0.1% yield target at its last meeting and since then economic news has been mixed – with stronger than expected September quarter GDP and data showing a strong reopening driven rebound in growth but continuing low wages growth and a new risk to the outlook from the Omicron variant. So the RBA is likely to simply reiterate its dovish guidance that it will not raise the cash rate until inflation is sustainably within the target range and that this will require the labour market to be tighter and wages growth to be materially higher. While on its “central scenario” the RBA does not see the conditions being met for a rate hike until 2024, our view remains that they will be in place late next year. Market expectations for 3 or 4 rate hikes next year by the RBA still look too aggressive though.

On the data front in Australia, ABS house price data for the September quarter (Tuesday) is expected show a 4.5% rise consistent with private sector data already released. Payroll jobs data (Thursday) will likely show a further improvement.

Outlook for investment markets

Shares remain vulnerable to further short-term weakness given the rebound in coronavirus cases globally and the new Omicron variant, the inflation scare, less dovish central banks, the US debt ceiling and the slowing Chinese economy. But we are now coming into a stronger period seasonally for shares and the combination of solid global growth and earnings, vaccines hopefully still allowing a more sustained reopening and still low interest rates augurs well for shares over the next 12 months. However, continuing inflation and interest rate concerns will likely result in rougher and more constrained gains than what we’ve seen since March last year.

Expect the rising trend in bond yields to continue as it becomes clear the global recovery is continuing, resulting in capital losses and poor returns from bonds over the next 12 months.

Unlisted commercial property may still see some weakness in retail and office returns but industrial is likely to be strong. Unlisted infrastructure is expected to see solid returns.

After rising by around 22% this year Australian home price gains are likely to slow to around 5% next year as poor affordability, rising fixed rates, higher interest rate serviceability buffers, reduced home buyer incentives and rising listings impact. Ultimately giving way to a 5-10% price fall in 2023.

Cash and bank deposits are likely to provide poor returns, given the ultra-low cash rate of 0.1%.

Although the $A could pull back further in response to the latest coronavirus threats, tightening US monetary policy and the weak iron ore price, a rising trend is likely over the next 12 months helped by still strong commodity prices and a cyclical decline in the US dollar, probably taking the $A up to around $US0.80.

By Shane Oliver