Weekly economic and market update – week ending 21 January, 2022

Investment markets and key developments

Global share markets remained under pressure over the past week on the back of concerns about rising inflation, monetary tightening, Omicron and tensions with Russia over Ukraine. The negative global lead and talk of higher interest rates in Australia also pushed Australian shares down with falls led by health, IT, Telco and financial stocks. Long term bond yields rose initially but their increase was curtailed by safe haven demand as share markets fell. Oil, metal, gold and iron ore prices rose but the $A fell as the $US rose.

Shares are having a rough start to the year. From their highs US shares have now fallen by 6.5% which is their biggest pull back since 2020, with the tech heavy and interest rate sensitive Nasdaq is down 11.3%, and global shares are down 5.3%. Australian shares are also down by around 6%, having caught down to the fall in US shares over the past week as RBA rate hike expectations were brought forward.

While the Omicron surge globally and in Australia will weigh on March quarter economic activity, it looks to be sharp and short. With an absence of hard lockdowns, most of the disruption has come this time on the supply side as many have had to isolate and can’t make it to work. But with Omicron cases now showing signs of falling in many countries including Australia we may be seeing the worst of the economic impact now with a possible improvement from next month. China remains the biggest risk though as its vaccines are reportedly less effective and its covid zero policy risks resulting in more lockdowns adding to global supply shortages.

Inflation and rate hike concerns have continued to build. High inflation readings for December point to rate hikes in Canada and the UK in the next two weeks and the US money market is now pricing in four rate hikes this year with some talking of a rate hike in the week ahead. The latter seems unlikely, but the Fed is likely to be more hawkish at its meeting in the week ahead and ends its bond buying program.

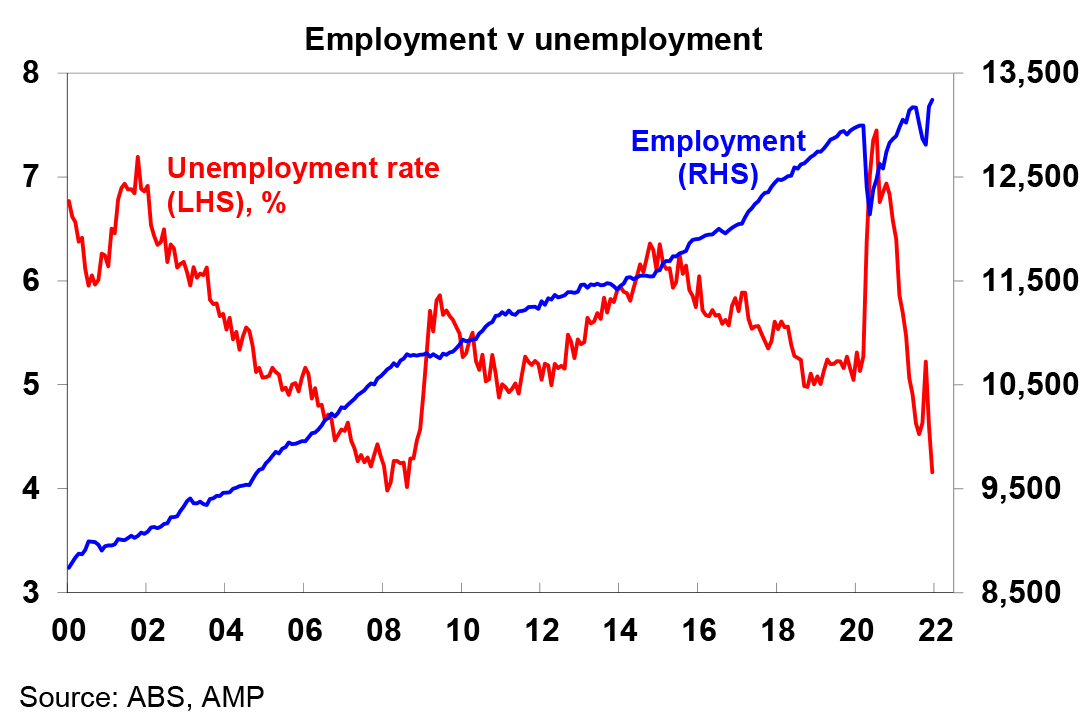

We have brought forward our forecast timing for the first RBA rate hike from November to August. Jobs data for December was far stronger than expected with unemployment at 4.2%, well below the RBA’s forecast for December of 4.75%. January and February jobs data will be disrupted by Omicron. But with new cases now trending down, strong jobs data is likely to quickly resume with unemployment falling below 4% this year and annualised wages growth rising above 3% setting up the conditions for the start of rate hikes in the second half. So, we now expect a 0.15% hike in August taking the cash rate to 0.25% followed by another hike to 0.5% in September with the RBA then pausing until early 2023. Market expectations for 4 or 5 RBA hikes this year are too hawkish though.

Monetary tightening will contribute to a more volatile and constrained ride for shares this year and could push shares lower in the short term. However, we don’t see monetary tightening this year being enough to end the economic recovery and cyclical bull market as monetary policy will still be relatively easy, some central banks including the RBA, the ECB and the BoJ will be lagging the US and China’s central bank is now through a tightening cycle and into easing.

Another potential source of volatility for investment markets is the threat of a Russian invasion of Ukraine. Its hard to see Russia invading all of Ukraine but US President Biden appears to be expecting some sort of conflict (after talks with Russia over Russia’s demands for Ukraine not to join NATO and for the west not to station strategic weapons in Ukraine failed to make much progress). But a partial invasion could lead to more sanctions on Russia worsening Europe’s gas shortage which would be bad for demand and inflation in Europe. Geopolitical tensions are normally relatively positive for US assets and the $US.

George Harrison’s My Sweet Lord has to be one of the most joyous pop songs. It has a nice little trick that got the western mainstream at the time singing along to “Hallelujah” and before they knew it moving on to “Hare Krishna” and a Vedic prayer. It along with the Hare Krishna Mantra which was produced by George and released on the Beatles’ Apple record label did much to explain the popularity of the Hare Krishna movement in the 1970s. George originally gave My Sweet Lord to Billy Preston (who can be seen in Get Back) and here’s Billy singing My Sweet Lord in Concert for George. I could never see the link to The Chiffons’ He’s So Fine, the publishers of which accused George of plagiarism.

Coronavirus update

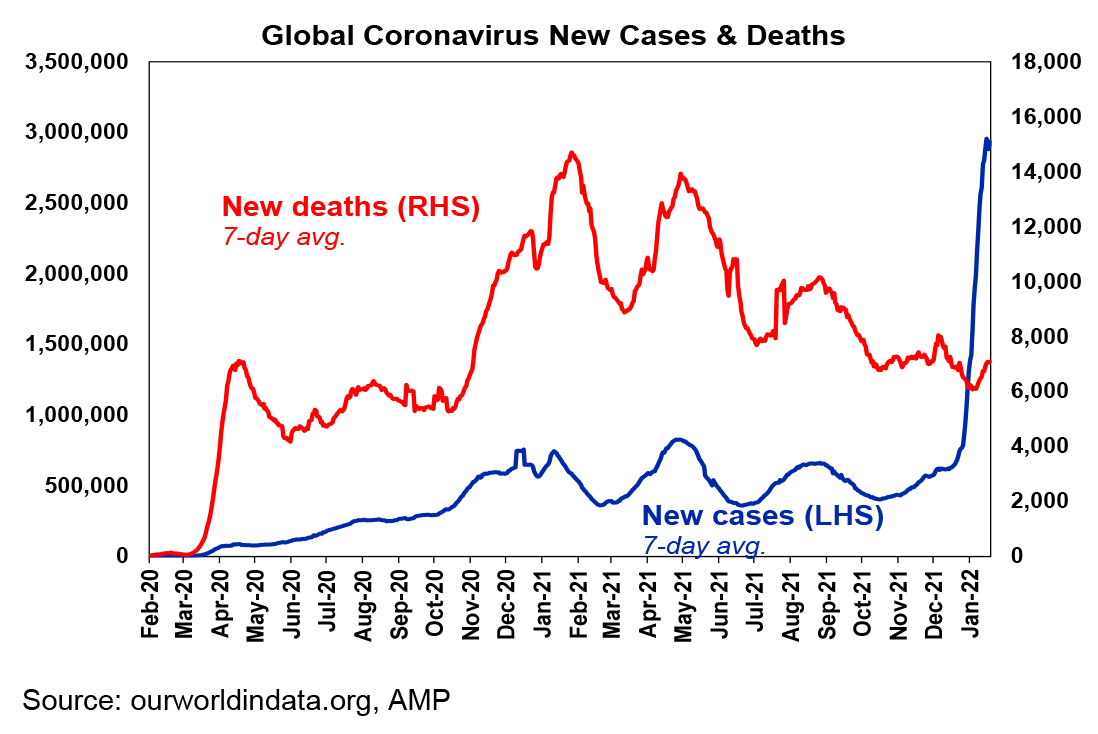

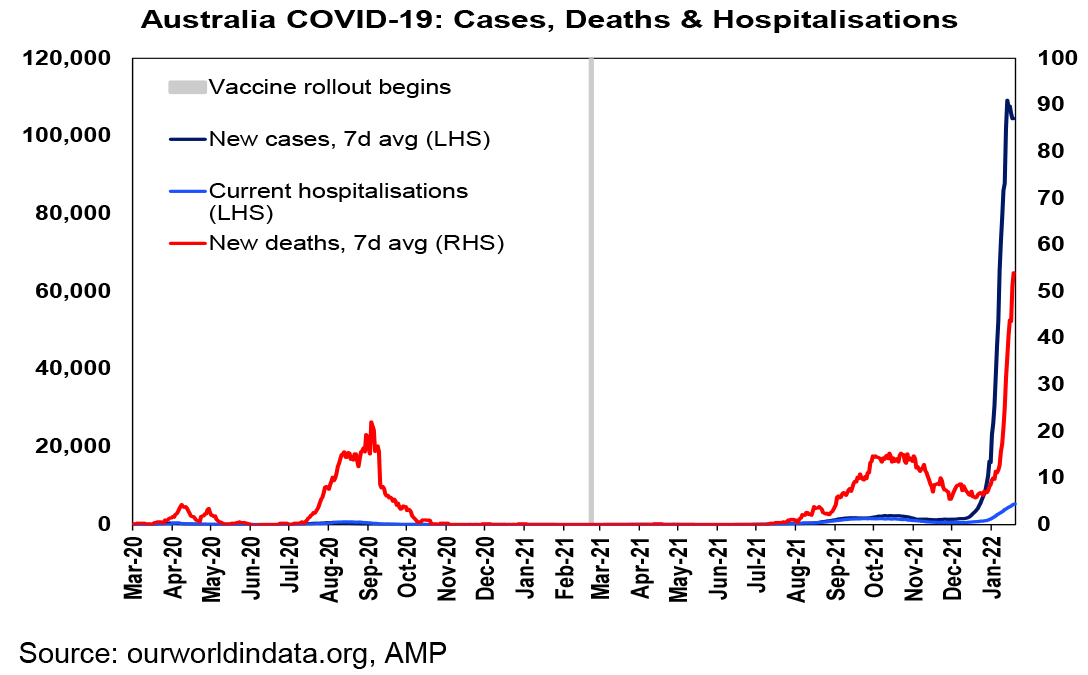

The Omicron wave, which has seen global coronavirus cases surge to record levels, is now showing signs of slowing.

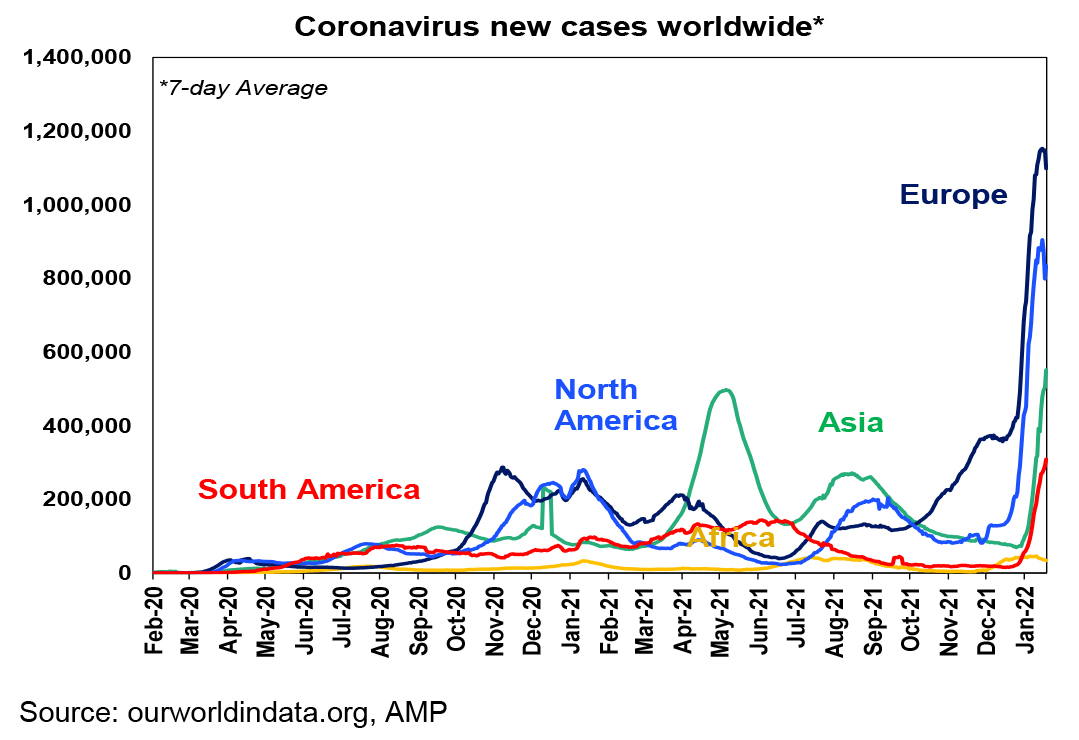

Just as South Africa saw Omicron cases peak and start to roll over a month or so after the first case, the same appears to be happening in the UK, US, Canada and Europe…and Australia. South America and Asia are lagging and still on the rise though.

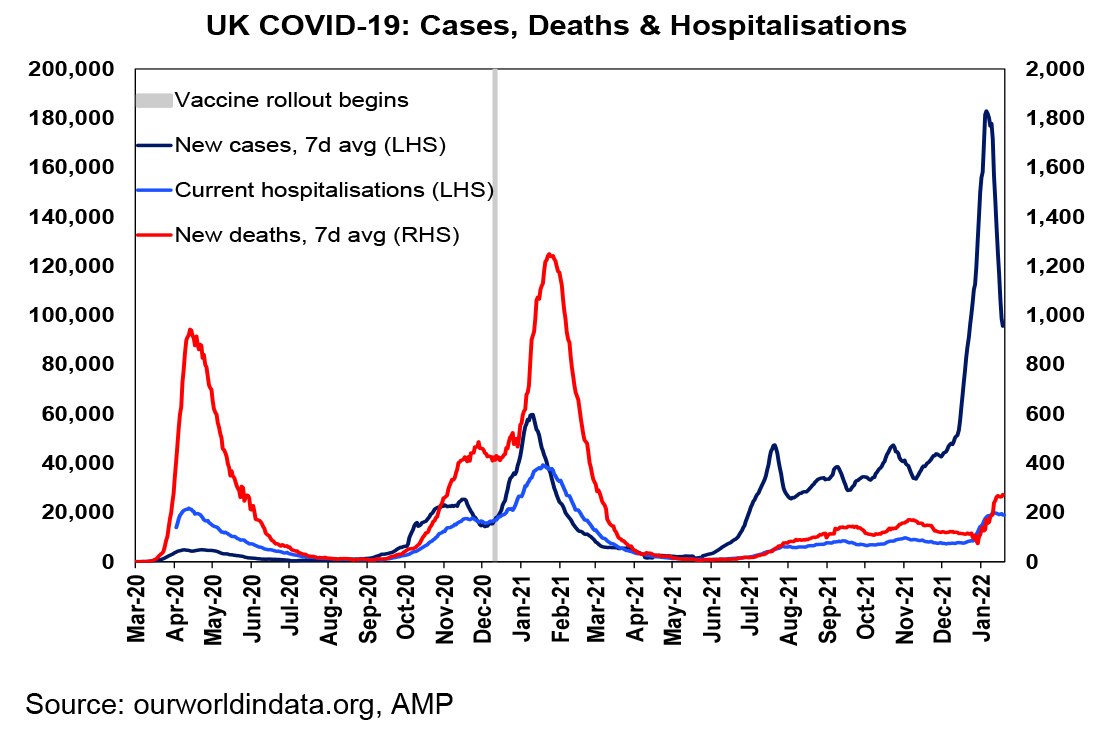

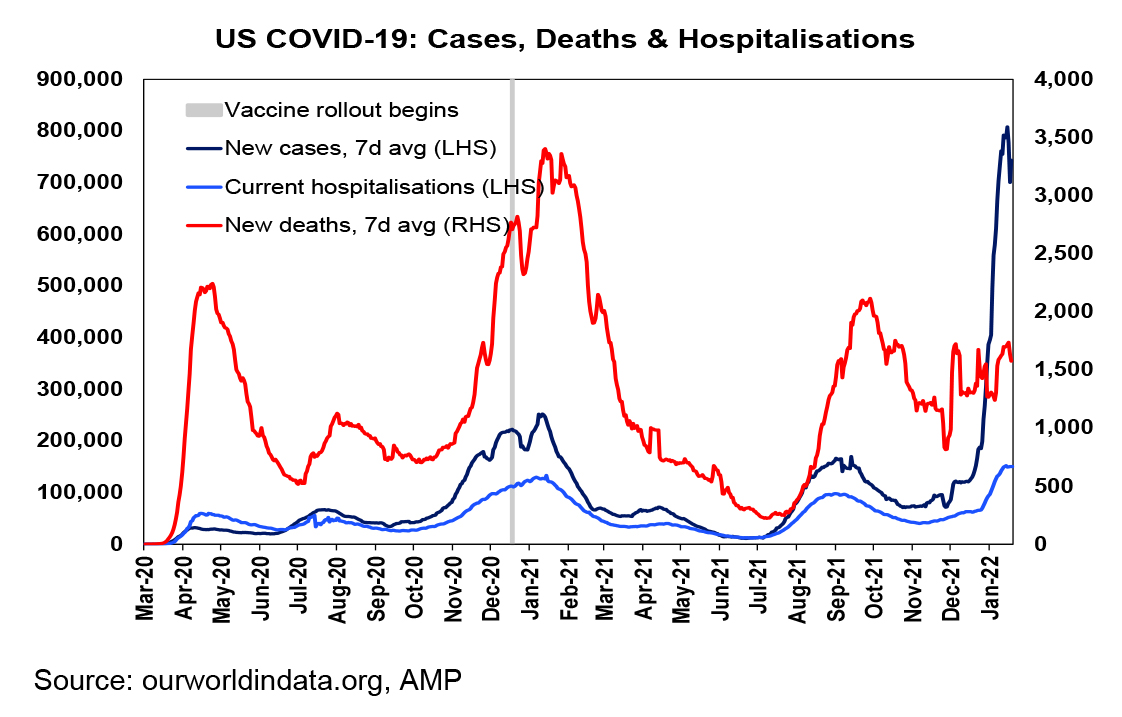

While deaths and hospitalisations have increased reflecting the lagged response to the surge in cases since mid December, they remain subdued relative to new cases compared to prior waves. This is evident in most developed countries and is consistent with the initial Omicron experience in South Africa – and can be seen in the next two charts for the UK and the US. It appears to reflect a combination of prior covid exposure and vaccines providing some protection against serious illness and the Omicron variant being less harmful. The easing in new cases and the likely flow on to reduced pressure on hospitals is seeing a move towards some easing in restrictions in some countries.

It’s a similar story in Australia – with cases showing signs of peaking and the proportion of cases suffering serious illness remaining low versus prior waves. The sheer surge in cases combined with staff absences due to isolation requirements has placed immense pressure on hospital systems. However, hospitalisations and deaths remain subdued relative to the surge in cases compared to previous waves and hospitalisations are slowing in NSW and Victoria.

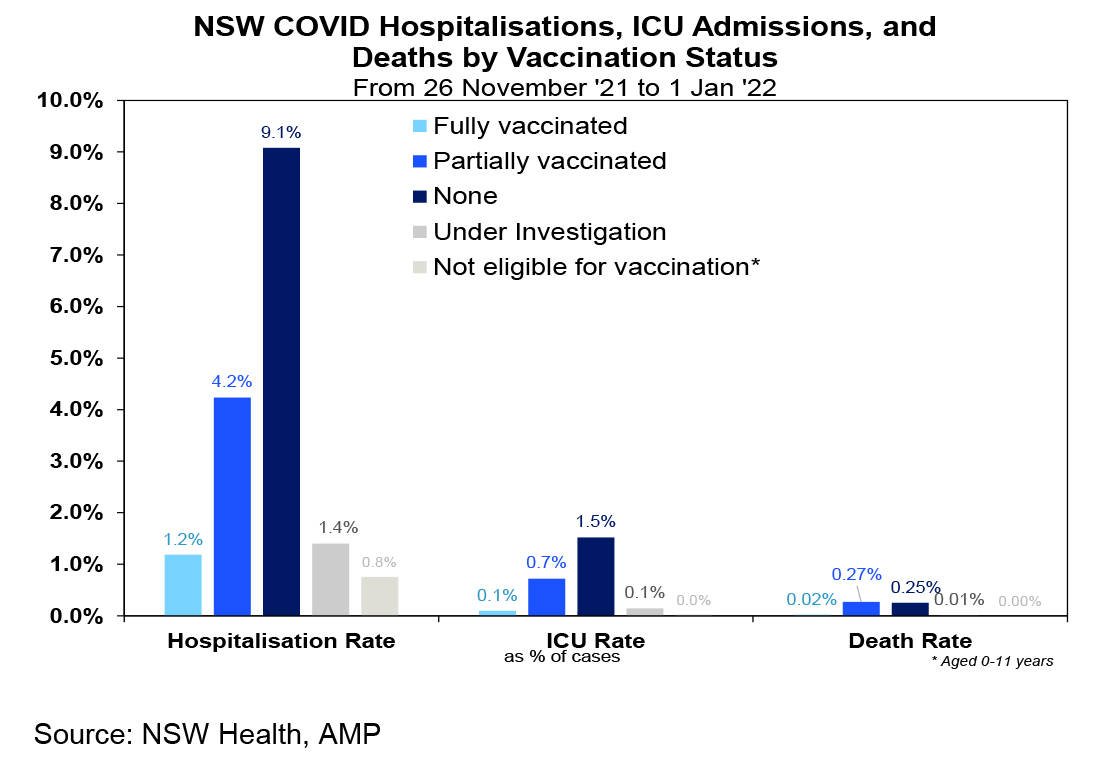

less harmful than previous variants and vaccines providing protection against serious illness. Data from NSW Health show that Omicron cases are about a third as likely to end up in hospital as Delta cases. It also shows that 1.2% of the fully vaccinated are likely to go to hospital compared to 9.1% of the unvaccinated and 0.1% of the fully vaccinated ending up in ICU compared to 1.5% of the unvaccinated. So, an unvaccinated case is 7 times more likely to end up in hospital and 15 times more likely to end up in ICU than a fully vaccinated case.

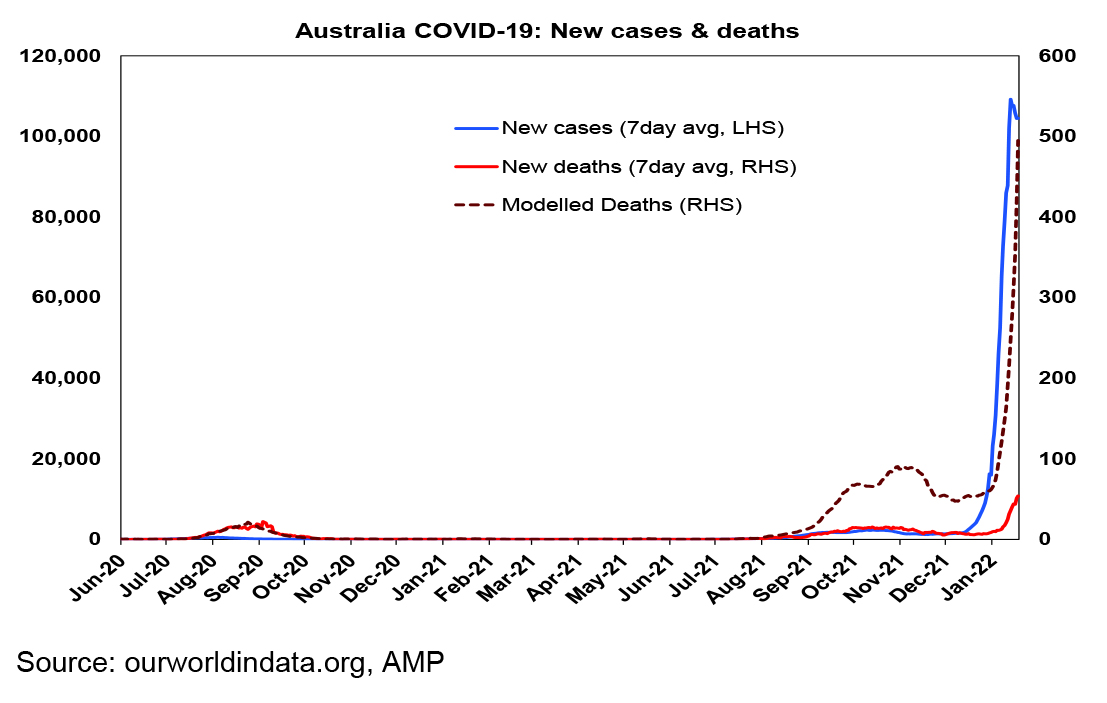

And while new deaths (red line in the next chart) are at record levels in Australia they are running around 10% of the level suggested by the 2020 wave (dashed line) reflecting protection from vaccines and Omicron being less harmful.

The combination of greater exposure to covid globally and vaccines providing increased immunity, covid morphing in a way which is more transmissible but less harmful with Omicron and better treatments all provide reason for optimism that the pandemic may be heading down a path towards being endemic and where the world can live with covid.

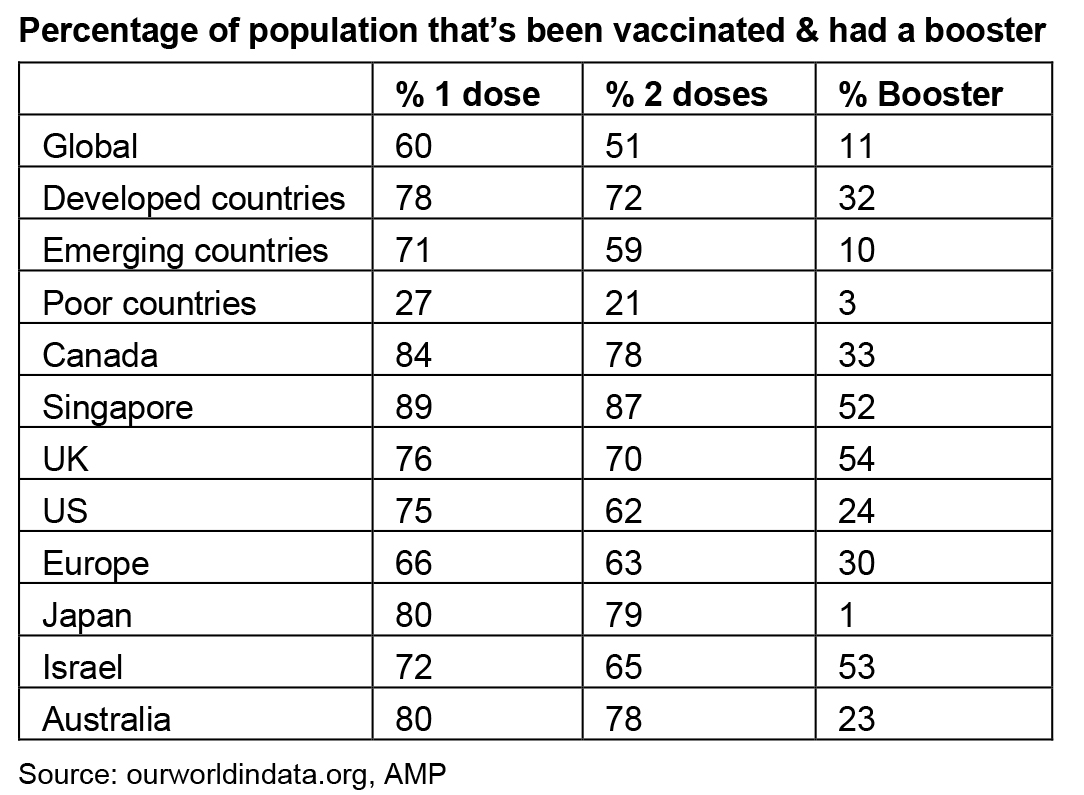

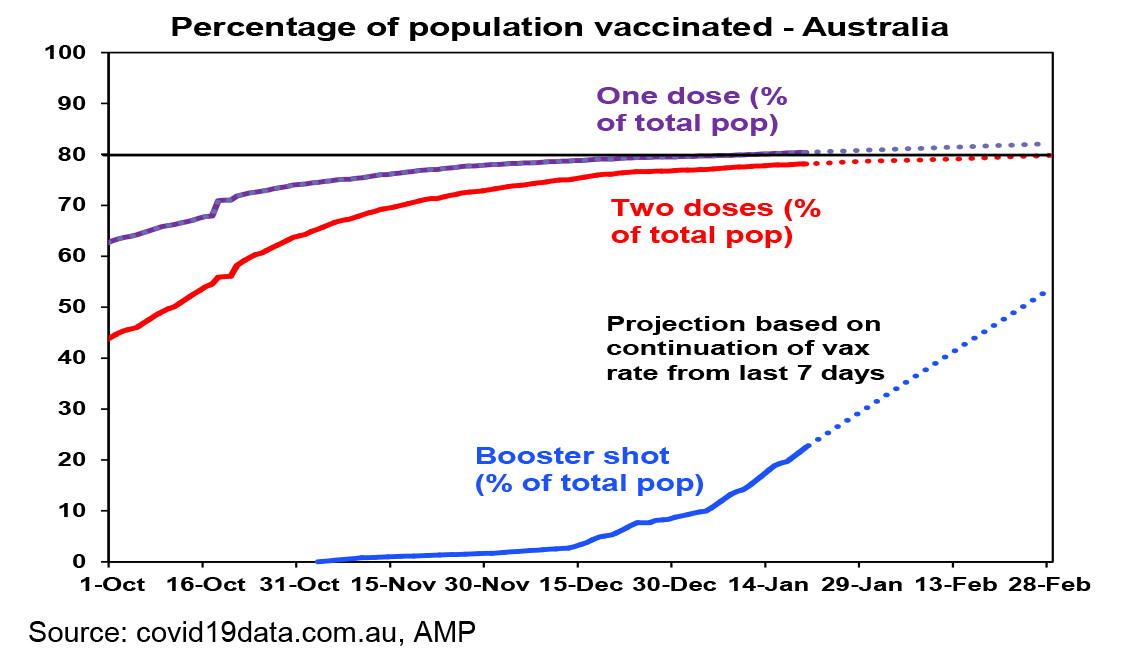

The main risk remains of more harmful variants emerging – particularly in poorer countries where only 21% of the population is fully vaccinated. It’s in the rich world’s interest to help vaccinate poor countries to reduce the risk of more mutations. Australia at 78% double vaccinated is at the high end of developed countries where the average is 72%.

While boosters started slowly in Australia 23% of the population have now had one and its rising rapidly.

Economic activity trackers

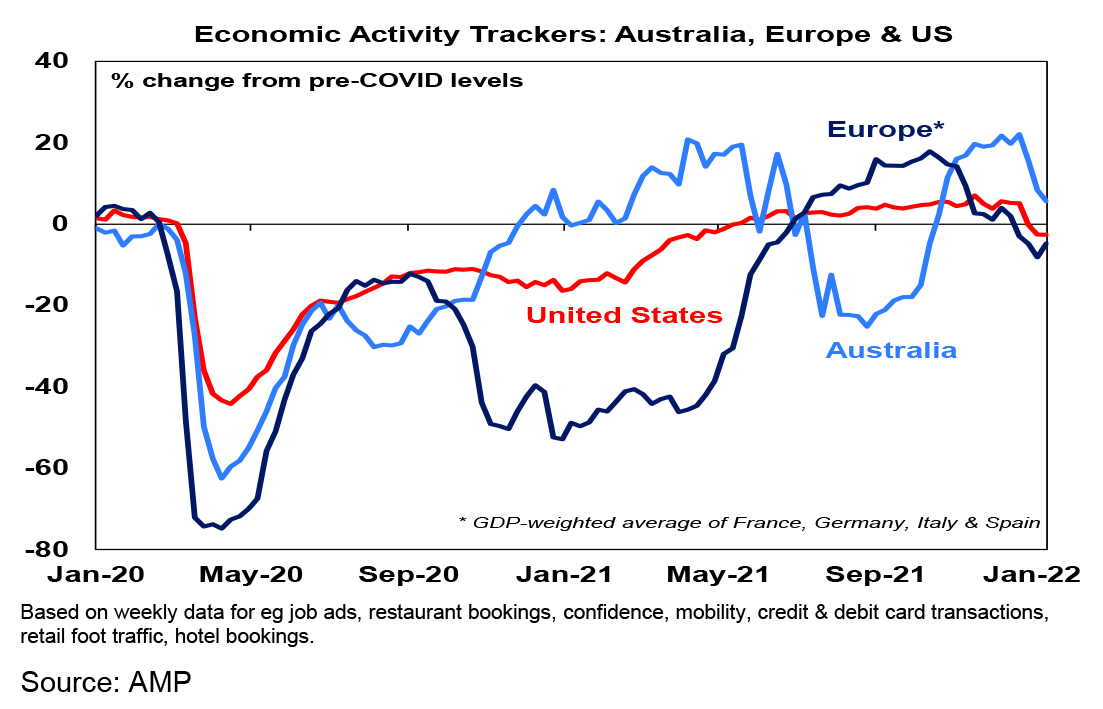

Our Australian Economic Activity Tracker fell further over the last week as the Omicron wave continued to disrupt economic activity. However, mobility has shown signs of improvement and with new cases rolling over Australian economic activity should start to improve in the weeks ahead. Our European and US activity trackers showed signs of stabilisation and improvement in the past week helped by a slowing in new coronavirus cases and are also expected to start improving.

Major global economic events and implications

Mixed US manufacturing data, housing strong. US manufacturing conditions indexes for the New York and Philadelphia regions were mixed with the former down presumably as Omicron disrupted things but the latter up. The good news though is that price components in both surveys mostly fell and expectations and capex plans in the New York survey remained strong. Jobless claims rose again but with Omicron cases falling the impact is likely to be temporary. Home builder conditions remained strong in January though and housing starts rose more than expected in December telling us the housing sector remains strong. Only 12% of US companies have reported December quarter earnings results but so far 79% of results have surprised on the upside with an average beat of 8%.

More inflation. UK and Canadian core inflation for December came in stronger than expected at 4.2% and 2.9% respectively consistent with both countries central banks raising rates in the next two weeks. Producer price inflation in Germany rose to 24%yoy in Germany, mainly due to the surge in gas prices.

The Bank of Japan left monetary policy on hold and ultra-easy as expected consistent with inflation still around zero – core inflation was actually -0.7%yoy in December. But the BoJ did revise up its growth and inflation forecasts slightly.

Softish Chinese data, PBOC eases. While Chinese December quarter GDP growth was stronger than expected it still saw annual growth slow to 4%yoy and December retail sales growth slowed sharply. As a result, the PBOC cut various interest rates slightly – but only by around 0.1% – and signalled that further easing is likely. With Chinese growth having slowed after last year’s policy tightening, coronavirus posing a risk and inflation weak in contrast to the US, the PBOC is now in very different point of the policy cycle to the Fed and other central banks. While Chinese growth will take a few months to pick up, policy easing there could be supportive for commodity prices offsetting tightening elsewhere.

Australian economic events and implications

Strong jobs, but confidence down – but only a bit. The December jobs data is now a bit dated thanks to Omicron disruptions which will show up in January and February, but it showed that the jobs market was far stronger than expected at the end of last year: employment is at a record high and unemployment at 4.2% and labour market underutilisation are the lowest since 2008 and this is despite labour force participation being around a record high and above pre-pandemic levels. While Omicron disruptions will hit employment and, much more so, hours worked in January and February, with Omicron already showing signs of peaking and employers likely keen to hang on to workers jobs market strength is likely to quickly resume pushing unemployment below 4% and annualised wages growth up to 3% in the second half of the year.

Meanwhile consumer confidence only fell 2% in January and remains just above its long-term average suggesting only a modest impact from the Omicron wave and new house sales rose 11% in December and are well above pre coronavirus levels.

What to watch over the next week?

The main focus in the week ahead is likely to be the Fed on Tuesday which is expected to confirm the pivot to a more hawkish tone flagged in recent comments from various Fed officials with the focus shifting from boosting growth to controlling inflation. Inflation has now been above the 2% target for some time and jobs data indicates that its objective of maximum employment is likely to have been reached. While it’s not expected to raise rates, there is a good chance it will announce the end of quantitative easing this month and signal that the first rate hike will come in March followed by several more and the commencement of quantitative tightening later this year. We see the Fed hiking rates four or five times this year. The Bank of Canada also meets Wednesday and is likely to raise rates.

On the data front in the US, January business conditions PMIs (Monday) are likely to show a fall on the back of Omicron disruptions, home price data for November is likely to show further solid increases but January consumer confidence is expected to have fallen (both Tuesday), December quarter GDP is expected to have increased by 6% annualised and underlying durable goods orders are likely to show a further rise (Thursday) and employment costs are expected to have risen 1% in the December quarter with December core private final consumption inflation rising to 4.8%yoy (Friday). The flow of December quarter earnings will start to speed up – consensus earnings expectations have now increased to 21%yoy but are likely to end up at around 26%.

Eurozone business conditions PMIs for January (due Monday) are likely to slow further with the Omicron wave, which is also likely to weigh on economic confidence (Friday).

Rising coronavirus cases albeit from a lower base could also weigh on Japan’s PMIs for January (Monday).

In Australia, the focus will be on December quarter inflation data (Tuesday) which is expected to show a 0.9%qoq increase pushing annual inflation up to 3.1%yoy from 3%yoy in September with the main drivers likely to be a 7% rise in petrol prices and a 3% rise in new dwelling costs. Underlying inflation is expected to rise 0.8%qoq partly reflecting bottleneck pressures in the economy which will push annual underlying inflation up to 2.4%yoy. This is consistent with the message provided by the Melbourne Institute’s Inflation Gauge. It’s above RBA expectations for a 2.25%yoy rise in underlying inflation and we expect a further rise in inflation pressures this year to be consistent with the start of RBA rate hikes in August. Meanwhile, January business conditions PMIs (Monday) and the December NAB business survey (Tuesday) are expected to show reduced confidence on the back of rising covid cases.

Outlook for investment markets

Global shares are expected to return around 8% this year but expect to see the long-awaited rotation away from growth & tech heavy US shares to more cyclical markets in Europe, Japan & emerging countries. Inflation, the start of Fed rate hikes, the US mid-term elections & China/Russia/Iran tensions are likely to result in a far more volatile ride than 2021, and we are already starting to see this. Mid-term election years normally see below average returns in US shares and since 1950, have seen an average top-to-bottom drawdown of 17%, usually followed by a stronger rebound.

Australian shares are likely to outperform (at last) helped by stronger economic growth than in other developed countries, leverage to the global cyclical recovery and as investors continue to search for yield in the face of near zero deposit rates but a grossed-up dividend yield of around 5%.

Still very low yields & a capital loss from a rise in yields are likely to again result in negative returns from bonds.

Unlisted commercial property may see some weakness in retail and office returns, but industrial property is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home price gains are likely to slow with prices falling later in the year as poor affordability, rising mortgage rates, higher interest rate serviceability buffers, reduced home buyer incentives and rising listings impact.

Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%.

Although the $A could fall further in response to coronavirus and Fed tightening, a rising trend is likely over the next 12 months helped by still strong commodity prices and a decline in the $US, probably taking it to around $US0.80.

By Shane Oliver