A market in such a state of constant flux can produce significant investment opportunities.

The Australian credit market is forever evolving. The structure and breadth of the market today doesn’t look anything like the Australian credit market from twenty years ago, and certainly bears no resemblance to the credit market twenty years prior to that time. A market in such a state of constant flux can produce significant investment opportunities, but only for sophisticated investment teams that understand the risks within newly developed areas of the market.

How is the credit market defined?

The Australian credit market currently includes a very broad universe of products that can be grouped into three broad categories: single name credit products, structured credit products and more complex credit products. The market currently is $1.56 trillion in size which represents around 70% of Australian gross domestic product (GDP).

Single name credit products

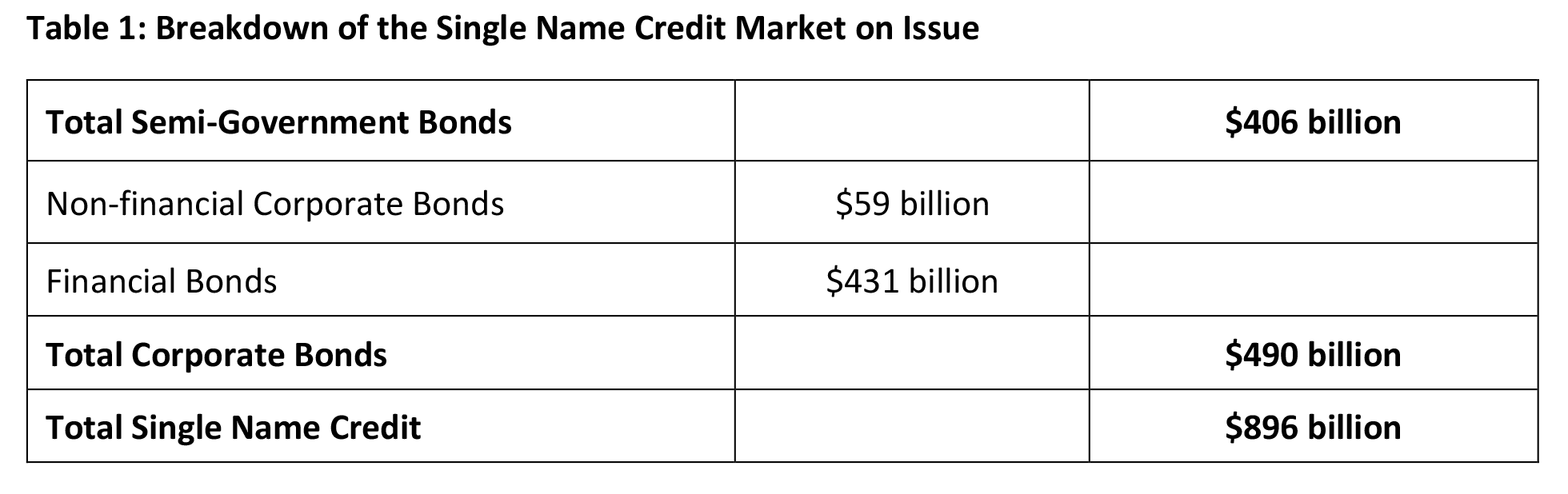

Single name credit products fall into 2 main categories, corporate bonds and semi-government bonds.

Corporate bonds include:

- non-financial corporate bonds

- bank senior debt

- subordinated bank debt

- tier 1 bank debt,

while semi-government bonds are securities such as those issued by NSW Treasury Corporation.

Single name credit is thus named because the securities are exposed to the idiosyncratic risks of a particular issuer. When BHP issues a corporate bond, investors holding that security are accepting the risk that BHP could default.

The market size of single name credit products in Australia is currently around $891bln or 57% of the total credit market. The split between corporate bonds and semi-government securities is roughly 55/45 and, within corporate bonds, bank debt dominates. Non-financial corporate bonds only comprise 6.5% of the total market for single name credit products.

Structured credit products

Unlike single name credit products, the risk in structured credit products is systemic, meaning that the security’s risk is linked to a portfolio of assets rather than a single asset.

Structured credit products include:

- Residential mortgage-backed securities (RMBS), where the underlying assets are mortgages backed by residential property; and

- Asset backed securities (ABS), which are financial securities backed by income-generating assets; these may include auto loans, personal loans or loans to small business.

An RMBS will not suffer a loss if one of its underlying mortgages defaults. In fact, it’s assumed that there will be defaults within the loan pools supporting these securities and this is considered when structuring them. Features such as the levels of subordination (the proportion of principle outstanding in the junior tranches which will absorb initial credit losses) and excess spread (the difference between interest received and paid), aim to ensure that within an expected level of defaults the structure is sound.

Similarly, ABS are comprised of multiple loans. When a consumer takes out a loan, their debt becomes an asset on the balance sheet of the lender who, in turn, can sell these assets to a trust or ‘special purpose vehicle’. They are then packaged into an ABS that can be sold in the public market.

While an investor in a BHP bond may experience a jump-to-default situation where they wake up one morning and there is headline news on BHP, structured credit assets are more susceptible to a general economic downturn that leads to higher than expected levels of defaults broadly across the mortgage, SME or consumer credit markets.

Complex credit products

Complex credit products typically have limited liquidity and have additional requirements for investors versus single name credit and structured products, including document negotiation and execution and monitoring performance. More complex credit products include:

- Leveraged loans; and

- Warehouse notes.

While each product in the complex credit space is different, there is a commonality; each provides investors in the credit markets access to an exposure they are unable to achieve through single name corporate and structured credit markets.

Historical trends within the Australian credit market

The size of the Australian credit market as a percentage of Australian GDP has shifted markedly over the past 100 years. The current credit market % of GDP is significantly higher than it was the 1980s (it was less than 10% of GDP) and more than double where it was back in the 1920s (around 30% of GDP).

Fiscal expansion following the Great Depression led to an explosion of issuance of semi-government bonds, which caused the total size of the credit markets to reach a high of close to 80% of GDP. As fiscal policy became more constrained in the 50s and 60s, the amount of semi-government bonds on issue as a percentage of GDP dropped to low single digits. The growth in the credit markets since that time has been driven by corporate bonds and structured credit products (although this didn’t start to take place until the 1980s).

Prior to the 1980s, Corporate bonds in Australia were a retail offering traded through a stock exchange. Retail investors had become accustomed to war bonds and this carried through to buying corporate bonds (mainly mining companies) in the 1950s and 1960s.

However, the market for these products was relatively limited given that the trading of corporate bonds was done by stockbrokers. Prior to the digital age, debt traded on the floor of the stock exchange through chalkies. Brokers offered the entire capital structure of a company, from equity to convertible notes to debentures, but ultimately any debt was more of a side issue and limited to the very well-known Australian names.

The real growth in corporate bonds appeared when global investment banks entered the Australian landscape. Corporate issuers could do larger deals, more quickly and at a cheaper level through the over-the-counter institutional market compared to the listed retail market (It is more expensive and time consuming for a company to issue via the ASX through a product disclosure statement than to issue through the over-the-counter market institutional market via an information memorandum).

This has meant that access to the Australian credit market has shifted over the past forty years from a place where retail investors dominated trading to one that is mainly an institutional market. The listed market comprises only around 3% of the credit market today.

At the same time that the corporate bond market moved to a more institutional product, structured credit products started to be introduced to Australian (institutional) investors. Demand for RMBS and ABS grew substantially from the mid-1980s until the Global Financial Crisis, which saw a number of defaults in RMBS product in the US (although none in the Australian market) and caused appetite to abate for a period.

However, this resulted in a supply/demand imbalance that led to significant increase in the relative value of these assets versus corporate bonds. Ultimately the outsized reward in structured credit drew investors back in and its market share of the credit market began to grow again. Structured credit on issuance is now larger than the corporate bond market and nearly as large as the single name credit market (corporate bonds and semi-government bonds).

The evolution of the Australian credit market from a retail to an institutional market has also allowed for the expansion of more complex credit products. Twenty years ago, many of these products didn’t exist, and while aspects of this market, such as leverage loans or credit indices are significantly more developed in offshore jurisdictions such as the US, the domestic market continues to expand.

Current landscape

One area of recent development within the more complex credit products has been in warehouse funding. This has been caused by significant growth in the size of non-bank financial institution (“NBFI”) market which in turn require financing to fund their loan book. One of the most efficient methods for NBFI’s to fund their lending activity, is through the use of a warehouse structure. These are similar products to RMBS and ABS transactions in that they are supported by a pool of hundreds, if not thousands, of underlying assets such as mortgages or car loans but are privately originated.

Unlike RMBS and ABS however, they are generally not rated by an external rating agency, which means that for unsophisticated investors, the risk is unknown. Such products are not actively traded in the over-the-counter market and the specific detail of each transaction is unique to each specific warehouse and negotiated between the provider of capital and the originator of the loans.

Investors wishing to participate in the warehouse market must have the required experience and knowledge with respect to how to assess risk, legal and reporting requirements, management of liquidity issues and how to negotiate on terms. There is a limited number of potential funders that have this expertise and so the supply of funds available to non-bank financial institution has been limited. This supply/demand imbalance has resulted in attractive pricing versus risk for investors who can arrange, execute and manage these products.

Retail investors’ direct access to the credit market in Australian is generally limited to listed bank tier one securities which some argue is not a true fixed income credit product, but rather quasi equity due to the standard structural elements of no fixed maturity date, coupon deferral and equity-conversion properties. In order for retail investors to get access to a diversified portfolio across the entire spectrum of credit products they need to go through a fund manager. However, it is important to ensure that the chosen fund manager has the expertise and resources on hand to successfully review, select and monitor the more complex asset types. The ever-increasing and ever changing product mix within the Australian credit landscape provides opportunities for credit fund managers who can adapt their processes to understand credit risk across a broad range of security types. Having a credit manager that is able to adjust and adapt to an ever evolving market provides investors with the best platform to profit from a market that doesn’t remain constant.