Responsible Investing – How green is your client and is it important?

How to identify the right ESG or socially responsible investments product type for each client, to ensure they meet their best interest duty obligations.

The importance of environmental, social and governance (ESG) integration has reached universal recognition. In Australia, there’s been a proliferation of ESG products competing for investor dollars. How do you best guide your clients to find a socially responsible investment option that genuinely meets their requirements and ensures you meet your best interest duty? This article, proudly sponsored by Russell Investments, examines the options available to your client and how to match the right product to the right client.

The global goal of net zero 2050 has put the spotlight on ESG investing. However, it’s not straightforward. There’s the nomenclature – ethical investing versus socially responsible investing versus ESG investment. Under these umbrella terms are a number of investment approaches, each of which has different investment inputs, and delivers different investment outputs.

It is also important to note that many ESG considerations have become mainstream, and a large number of investment managers now use some form of ESG screen when scrutinising investment opportunities. It has been said that ESG is a key part of identifying quality; if a company’s management team is switched on to ESG challenges to their business model, there’s a strong chance they’ll also be switched on to other challenges.

Integration of ESG factors

For some investors, the integration of ESG factors into mainstream funds is sufficient to meet their desire for some form of ‘responsible’ investment.

Russell Investments’ annual ESG survey[1] canvassed 369 asset managers around the world, which collectively represented $79.6 trillion assets under management. It found that across the asset classes, the strategies which provide ESG integration represent the largest proportion of strategies offered to date.

The survey also asked which type of strategies asset managers saw the most interest and asset growth in over the past 12 months. The results show proportionally more demand in ESG integrated strategies. These findings suggest that investors may be looking to substitute existing core allocations for sustainable strategies with ESG outcomes.

Other findings from the Russell survey include:

- there’s a general acceptance that incorporating ESG considerations provides asset managers with a more comprehensive, forward-looking picture of their investment opportunities

- the attempt to harmonise ESG frameworks within organisations is happening across most asset classes

- an increased number of firms are adding more ESG metrics into their investment process, expanding their dedicated responsible investment resources, and providing greater transparency through reporting

- asset managers are increasing efforts to improve the overall quality of inputs when integrating ESG considerations; 55% of respondents had dedicated ESG professionals, up from 43% in the previous year.

Importantly, the results from this survey indicate an amplified focus on climate risk and a strong commitment to reaching net zero greenhouse gas emissions by 2050, something likely to resonate with Australian investors. Research[2] shows that 75 percent of Australians are concerned about climate change and 82 percent support the phase-out of coal fired power stations, arguably one of the largest contributors to emissions.

Whatever the reason investment managers use ESG screening – altruistic, financial or a mix of the two – Australian investors have plenty of investment options. How then, do you as an adviser ensure that the right ESG product is matched to the right client?

ESG or socially responsible investment options

As well as the different labels attached to the various investment options, there are also a range of investment approaches. The top three responsible investment approaches[3] (ranked by assets under management) are ESG integration, negative screening, and corporate engagement and shareholder action. Impact investing saw the largest increase since 2019, increasing by 46 percent, followed by corporate engagement and shareholder action, which increased by 15 percent.

The first step to being able to recommend the appropriate product/s to your client is to understand the investment options available.

Screening

Russell’s research found that screening is one of the most widely used tools utilised to implement a responsible investment policy. Screening uses a set of criteria to determine which sectors, companies or countries are eligible or ineligible to be included in a specific portfolio as a baseline investment decision.

The most popular screening criteria is value-based negative screening for both labelled and non-labelled sustainable strategies. Specifically, 47% of the respondents who use some form of screening criteria apply the value-based negative screening for the labelled sustainable strategies.

Negative screening with value or ethical-based criteria systematically excludes regions, sectors, companies, issuers or activities. Exclusion criteria often include product-based considerations or sectors, such as fossil fuels, weapons or tobacco. This approach may also exclude specific company practices, such as animal testing or human rights violations.

In Australia, negative screening increased its reach from $535 billion in 2019 to $557 billion assets under management in 2020 and remains the second most widely used responsible investment approach[3].

In 2020, the most frequently excluded categories were tobacco (76 percent), controversial weapons (64 percent) and gambling (58 percent). Screening of human rights abuses and controversial weapons increased in 2020[3].

Importantly, RIAA research shows that negative screening approaches and the expectations of investors do not always align. For example, after fossil fuels, consumers seek products that screen for human rights and animal cruelty. This doesn’t align with the investment managers whose focus is on excluding tobacco, weapons and firearms[3].

Positive screening focuses on business activities that may identify firms as leaders among peers. It’s the inclusion of particular sectors, companies or even projects based on positive ESG or sustainability performance criteria relative to industry peers[3].

Positive screening is mostly applied to renewable energy and energy efficiency, followed by sustainable water management and use, transition risk management and circular economy reuse and recycling. According to the RIAA, application of positive screening declined from 2019 to 2020.

Norm-based screening focuses on screening of investments on the basis of minimum standards of relevant business practice. This could include screening out violators of the United Nations Global Compact or UN Convention on Cluster Munitions or screening in based on ESG criteria developed by international bodies such as the United Nations Human Rights Council or International Labour Organisation[3].

ESG Integration

While a number of ‘mainstream’ investment managers incorporate ESG factors into their investment process, there are those whose investment process and decision making is built around the explicit inclusion of ESG risks and opportunities.

The 2021 Russell Investments ESG Manager Survey revealed a continuously high level of ESG awareness and increasing integration of ESG data and analysis into investment processes within asset management across the globe. The survey results conclude that while the starting point varies, many asset managers are evolving their ESG integration practices to capture material ESG-related information in their investment processes.

Many firms have moved their ESG integration practices from making a gesture to meaningful compliance. Others have shown greater commitment, such as identifying material ESG-related information and incorporating such inputs into key investment decisions. Ever-growing regulatory pressure and client demand are further pushing ESG integration practices.

In Australia, ESG integration remains the predominant responsible investment approach, growing from $580 billion assets under management in 2019 to $628 billion in 20203.

Corporate engagement and shareholder action

Corporate engagement and shareholder action refers to the influence and power of shareholders over corporate behaviour through engagement with company management and boards. This might include engaging and voting on ESG-related company resolutions to contribute to better performing companies and stronger sustainability outcomes, or proxy voting in alignment with ESG guidelines.

This was one of the top three responsible investment approaches (measured by assets under management) in 2021[4] and in Australia, increased as a key responsible investment approach, growing from $409 billion in 2019 to $471 billion in 20203[5].

Sustainability-themed investing

Sustainability-themed investing refers to investment in thematic products or funds that have specific objectives to improve social or environmental sustainability alongside financial returns. This might include products focused on clean energy, water management or green property. It could include broader portfolios that focus on climate and decarbonisation, or sustainable agriculture.

The RIAA report found sustainability-themed investing has decreased in Australia, falling 8.5 percent from $84 billion assets under management in 2019 to $76 billion in 2020. Measured by assets under management, the most common sustainability themes are climate-related investments (34 percent), natural capital (21 percent), and healthcare and medical (13 percent)5.

Impact investing

Impact investing refers to investments made with the explicit intention of generating positive social and/or environmental impact alongside a financial return. Among impact strategies, climate risk and the United Nations Sustainable Developments Goals (SDGs) are identified as the most popular themes4.

Social bond issuance has materially surged since the COVID-19 crisis, as the pandemic brought heightened attention to the importance of social issues. However, the overall social bond market remains very small, relative to the rest of the global bond market. In addition, social issues generally apply to companies’ operational aspects – such as employee safety, diversity and data privacy – which require more subjectivity in assessing the investment opportunity set. This is an area that is behind scientific-based themes, such as climate risk, which provides greater transparency and data availability.

The greatest ESG issues for investors

When assessing a client’s appetite for responsible investment, the second step is to consider the issues of greatest importance to your client. Is the client happy to screen out negative issues, or do they specifically want to invest in such a way that supports particular sectors, companies or issues?

In Australia, 87 percent of clients express climate and environment as the most significant issue. The recent floods and other climate-linked natural disasters are focusing attention on climate, decarbonisation and broader environmental issues.

Does your client want to invest broadly in a climate themed fund or one that has a more targeted investment approach? An example could include a product focused investing in renewable energy companies or a renewable energy project via an impact investment.

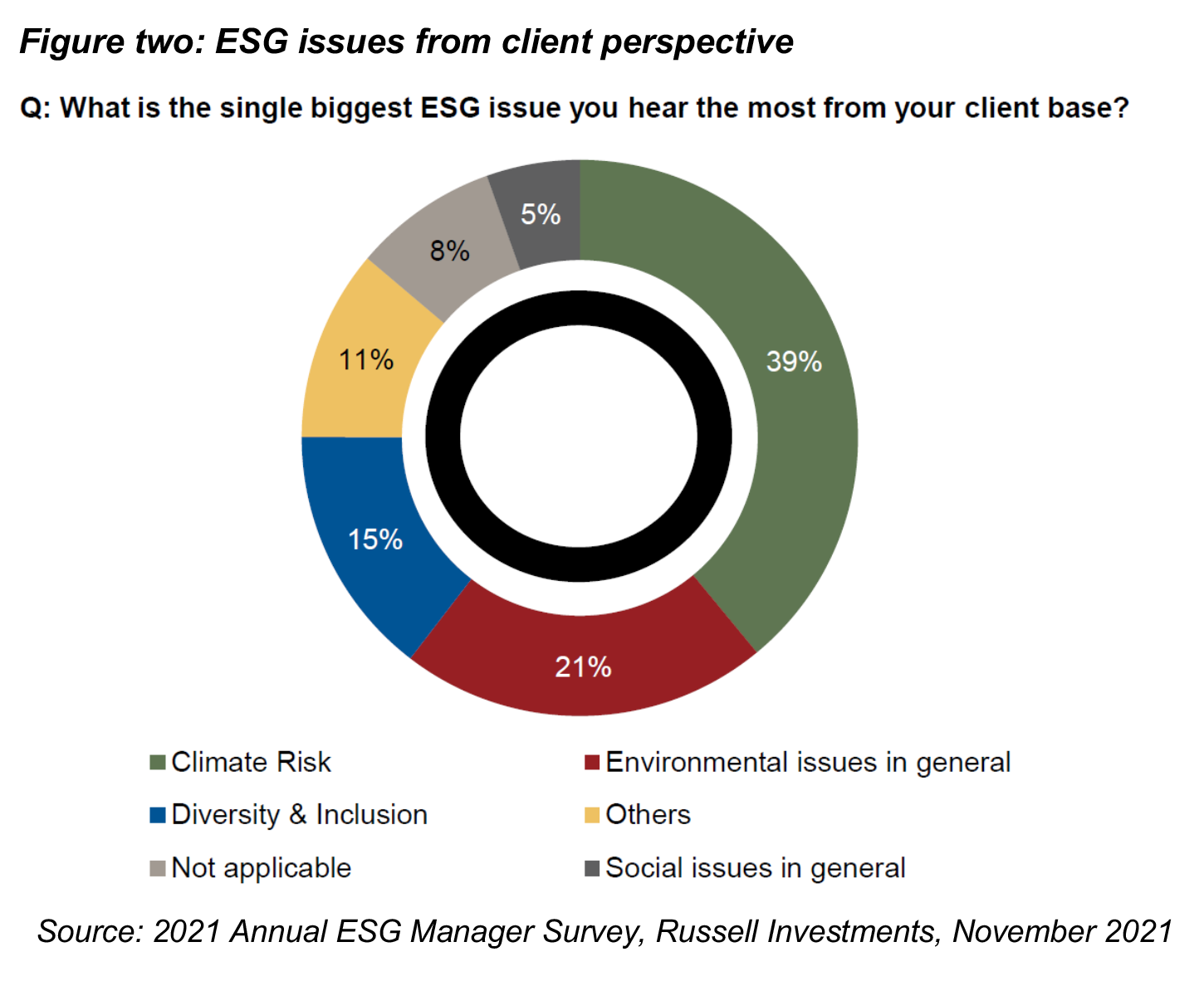

Russell’s survey asked participants to select the single largest ESG issue they tend to hear from their client base. The global results are as follows:

- 39 percent selected climate risk

- 21 percent selected general environmental issues

- 15 percent selected Diversity, Equity and Inclusion (DEI).

Among the respondents who selected “Others” in this section, many cited both climate risk and DEI issues, and believe they are equally important issues.

The research found that while DEI is considered to be an important social issue, it has a perceived reduced importance due to climate risk being a dominant factor. In other words, it’s not that DEI is less important, there is greater urgency in terms of climate risk control across the globe.

Assessing ESG products

There’s a vast range of ESG product available, a set that is growing in terms of unlisted and listed investments. How then do you select which is the right product for your client? While your approved product list and product research are key screening tools, you will need to further examine the product set available to your client.

Firstly, there are two key features that ESG style funds should have:

- Negative screens or tilts – companies/industries that are excluded or held at underweight positions relative to the market

- Positive tilts – companies/industries that investors want overweight exposure to relative to the market

Negative tilts

As outlined earlier in this article, typical negative screens include fossil fuels, alcohol, and gambling. These industries can result in some form of harm, for example the burning of fossil fuels results in environmental (E) impact that is contributing to climate change. Similarly, alcohol and gambling can have negative community and social (S) impacts due to the potential damage on the health and wellbeing of individuals. Those companies lacking transparency or involved in some type of fraudulent activity would be screened out on governance (G) measures.

Positive tilts

Positive tilts will use Environmental, Social and Governance metrics to identify stocks to include in a portfolio and take an ‘overweight’ position. Examples might include renewable energy, sustainable forestry or health care. Another approach is to score companies across a wide range of ESG metrics and then overweight stocks that have the highest aggregate ESG scores.

Understanding the approach taken by the investment manager will help you identify those products most closely aligned responsible investing objectives.

A note on greenwashing

The increased demand for responsible investment options has led, unsurprisingly, to many investment houses looking to capture some of this growth through the launch of new products. However, it has also led to the rebranding of existing products which, in turn, has led to concerns about ‘greenwashing’.

Greenwashing can be described as overstating a product’s ESG credentials or misleading investors about the degree to which the financial product is environmentally sound or focused on responsible investment.

The client conversation

When choosing the right responsible investment product for a client, you need to ascertain:

- What type of investment option will best meet my client’s needs with respect to their financial and responsible investment objectives?

- What are the specific ESG issues important to the client?

- Do any negative screens used by the investment manager match the client’s beliefs?

- Are any positive tilts used in managing the product consistent with the ESG issues important to that client?

- Is the product certified by RIAA[6]?

Once you understand your client’s ESG objectives, you can recommend a product that will best meet their needs and objectives. That way, not only will you have a satisfied client, you will also meet your best interest duty obligations.

———