Retired? Now what?

It’s vital advisers understand the importance of funding, housing and wellbeing to ensuring older clients meet their retirement objectives.

For so many, retirement seems to be an end goal. However, what should advisers do when their clients reach retirement? This article, proudly sponsored by Russell Investments, examines those early days of retirement and the importance of sound planning for funding, housing and wellbeing.

Most Australians have a positive vision of retirement, viewed through the rosy lens of retirement advertising. A golden time of precious moments with family and friends. A time of exploration, whether as a ‘grey nomad’ exploring Australia’s vast territory or heading overseas to tick off items from the bucket list.

Demographer Bernard Salt believes 2021-2027 will represent the peak years of the Australian baby boom retirement surge, a cohort of nearly five million. This will, he says, translate into an elevation of retirement issues: concerns about health care, aged care and access to various aged-based financial concessions[1].

“The driving force behind the next generation of retirees will be a desire to reset the agenda, to extract value out of every minute of every day: to live life to its fullest.” Bernard Salt, August 2021

The now retiring cohort of baby boomers have a strong memory of their parents in retirement. After all, they have been helping their parents navigate different parts of the system – Centrelink, support services, aged care services. Baby boomers are generally more tech savvy than previous generations and are arguably more educated and sophisticated; they are also the first generation to retire with some superannuation savings.

The average life expectancy of Australians has shot up by nearly a decade in the last 20 years. While on one hand, this is great news – more years to fulfil those retirement dreams. For others, the halcyon retirement vision fades as fear of outliving retirement savings becomes a reality.

How can advisers ensure their clients are well prepared for retirement? Not just financially, but more holistically? The three main drivers for wellbeing in retirement uncovered by research[2] – income, community and control – are aspirations that can underpin the transformative impact of advice for retirees.

This research found retirees are more satisfied if they feel financially secure. Secondly, retirees who remain a part of their established community and are embedded with family and friends received a better wellbeing score than those who chose to relocate. The feeling of control, inextricably linked to financial security, reinforces the value of financial advice. Finally, home ownership is important. Those retirees who own their own home have a much better retirement experience than those who don’t; in fact, owning a home was found to be the clearest driver of satisfaction and happiness in retirement.

While no two retirements are the same, there are issues that when resolved, can lead to positive outcomes. By working with clients to set goals and implement strategies to meet them, advisers are in a unique position…one that can help retired Australians improve their income, feel safe and comfortable and experience wellbeing. In other words, you’re in a strong position to ensure your clients can have the best possible retirement.

Retirement funding

Although baby boomers are the early beneficiaries of the compulsory superannuation system, for many, this enforced retirement savings was introduced too late in their working lives to fund 25 or so years of retirement. The 2020 Retirement Income Review was the first major inquiry into Australia’s retirement savings system and focused on how to improve retirement income. It identified three pillars of retirement funding: superannuation, the Age Pension and voluntary savings, including home equity.

Although its been in play since the 2014 Financial System Inquiry, the retirement income covenant (RIC) formally passed through parliament on 10 February 2022 and comes into effect on 1 July 2022. The RIC requires super trustees to develop a retirement income strategy for their members; the aim, to improve the financial outcomes for Australian retirees. While the RIC does not place obligations on financial advisers – or on SMSF trustees – you will need to understand the retirement income strategy offered by the super fund for each of your clients.

Establishing financial goals for retirement can, and where possible, should start before retirement. Whether it’s a trigger event such as we’ve seen during the Covid-19 pandemic, a planned exit from the workforce or a gradual wind-down, advisers can help their clients make the transition. As detailed in an earlier article a Transition to Retirement (TTR) strategy can be useful for pre-retirement clients, specifically those aged 58 or over, who have reached their preservation age and are still working. A TTR enables clients to access their super as an income stream while they are still working and can be used to achieve different objectives.

Once retired, sources of each client’s retirement funding need to be assessed (figure one). Retirees need income to meet their lifestyle needs. They also need access to capital: for home modifications or repairs, a new car, travel or medical expenses.

Retirement is characterised by change, both expected and unexpected. Changing family structure can change both the conversation and the retirement outlook for individuals. For example, 40 percent of separated, divorced or widowed Australians are forced into retirement by health issues[3]. This cohort also demonstrates less financial resilience.

Change can also come from external forces, such as a market correction that impacts financial assets or changes to interest rates. Or, as we’re currently experiencing, cost of living pressures. Such change will have a much bigger impact on the future decision making for retirees on a fixed income.

There’s significant wealth built up and transferring into this space and, at the same time, there’s plenty of complexity. The latter only grows with the government consistently changing rules around super, tax and Centrelink entitlements. There are also opportunities such as the government’s downsizer contribution to consider, and the RIC will no doubt deliver new financial products to explore.

Retirement housing

Australians have long regarded their home as their castle. For many retired Australians, home is also a safe haven, reinforced by the Covid-19 pandemic. However, the desire to age in place, at home, is not new. Research stemming back to 2013[4] shows a strong propensity for retired Australians to remain in the family home for as long as practicable.

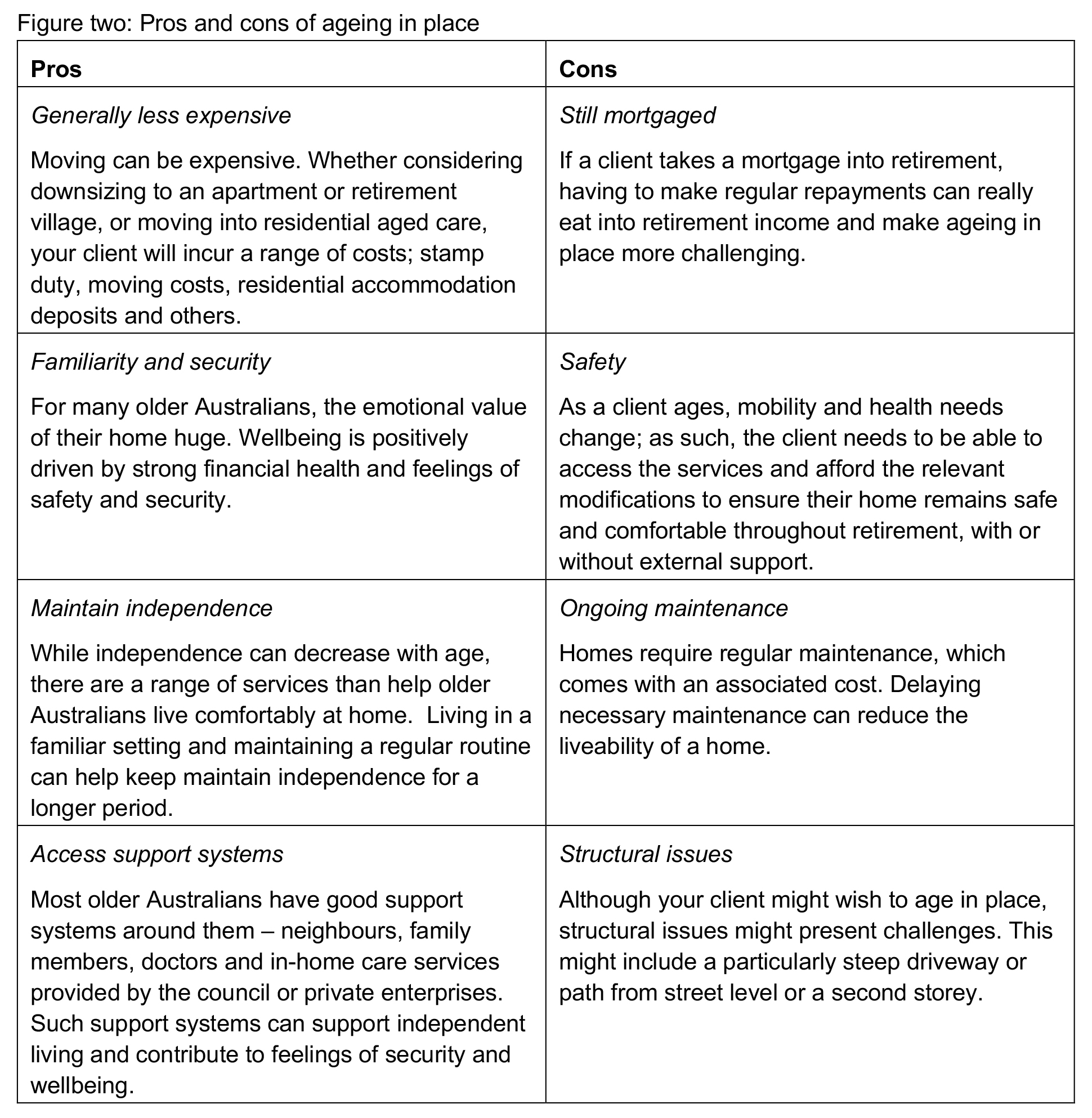

For your clients, staying in one’s own home, retaining independence and autonomy as they get older and as their health needs change may be important to their health and wellbeing. A familiar home improves perceptions of security, helps to maintain social connections within community, provides access to services and proximity to family and friends. It may also be the largest financial asset your client has ever owned! However, there are advantages and disadvantages (figure two).

Retirement housing also provides an opportunity to provide retirement funding in two key ways: through downsizing and releasing equity in the home, or through using an equity release scheme to access home equity funding.

Downsizing

While there are numerous reasons for downsizing, they generally fall into three categories: financial, practical and lifestyle.

From a financial perspective, downsizing enables retirees to move to a less expensive home. It’s a simple calculation – sell the family home, buy something cheaper and use the change to fund retirement. The effectiveness of this strategy this will vary and is largely dependent on the availability of cheaper housing in your client’s chosen location. It also presents an opportunity to top up super using the downsizer contribution.

From a practical perspective, downsizing might provide your client with better accessibility and easier maintenance. It might be a new home without stairs, with a more manageable garden or one doesn’t need modification to make it safe and comfortable for retirement.

From a lifestyle perspective, downsizing might see your client move into a retirement ‘lifestyle village’, tree change or sea change, or from outer to inner suburbs to make the most of their chosen city.

The downsizer contribution

Introduced on 1 July 2018, the federal government’s downsizer contribution allows older Australians to top up their super with some of the proceeds of selling their family home.

Clients aged 65 years upward can contribute up to $300,000 (for singles) or $600,000 (for couples) of the proceeds of selling your family home, regardless of caps and restrictions that otherwise apply to topping up their super. From 1 July 2022, the age requirement drops to include those aged 60 plus.

No work test or upper age limits apply to downsizer contributions; usually, clients aged 67 to 74 need to satisfy a work test to make voluntary super contributions. People aged 75 and over are generally ineligible to make any voluntary contributions to their super.

To make a downsizer contribution, your client needs to be able to answer yes to each of the following:

- you are 65 years old or older at the time you make a downsizer contribution (60 years old from 1 July 2022)

- the amount you are contributing is from the proceeds of selling your home where the contract of sale exchanged on or after 1 July 2018

- your home was owned by you or your spouse for 10 years or more prior to the sale

- your home is in Australia and is not a caravan, houseboat or other mobile home

- the proceeds (capital gain or loss) from the sale of the home are either exempt or partially exempt from capital gains tax (CGT) under the main residence exemption, or would be entitled to such an exemption if the home was a CGT rather than a pre-CGT (acquired before 20 September 1985) asset

- you have provided your super fund with the ‘downsizer contribution into super’ form either before or at the time of making your downsizer contribution

- you make your downsizer contribution within 90 days of receiving the proceeds of sale, which is usually at the date of settlement

- you have not previously made a downsizer contribution to your super from the sale of another home.[5]

Home Equity Access Scheme

The federal government has also broadened accessibility to its Home Equity Access Scheme (HEAS), formerly known as the Pensions Loans Scheme. Since 2020, all Australian homeowners of Age Pension age have been able to use the scheme to access home equity, including self-funded retirees.

Administered by the Department of Human Services, the scheme allows retirees to borrow up to 1.5 times of the maximum Age Pension, paid in fortnightly instalments. From 1 July 2022, some capital payments will also be accessible. The loan and all costs and accrued interest must be repaid to the Commonwealth. Repayments can be made at any time.

There are other commercial reverse mortgage schemes that can draw on home equity to provide income and/or capital to retirees.

Wellbeing in retirement

As people age, their expense profiles change. While retirees in the early stage of retirement may spend more on travel and lifestyle, those in the latter stages are likely to spend more on medical and care expenses.

Planning early can help ease the transition for retirement clients…and not just in a financial sense. To stay healthy and happy in retirement, people need a sense of purpose, to remain a part of their existing community and support network. Personal and lifestyle objectives are supported by financial objectives. Being able to look forward with confidence is the greatest contribution an adviser can make to a retired client’s lifestyle.

By engaging with clients pre-retirement, you can have the conversations that best position the client for a successful retirement, and for those clients already retired, there’s an opportunity to continue the conversation. How is their retirement tracking and does it meet expectations? Have their retirement goals changed and how can you work together to ensure they’re met?

As baby boomers reach retirement age there’s an unprecedented opportunity for advisers to work with this cohort to optimise their retirement. Financial security underpins a comfortable and happy retirement and helps clients achieve their retirement goals. The feeling of control, inextricably linked to financial security will reinforce the value of your financial advice, while providing your clients with agency and a sense of wellbeing.

———-