Bruce Apted

The recent sell-off in markets has been savage. Many investors are now looking for the opportunities and interest in “market bottoms” is on trend.

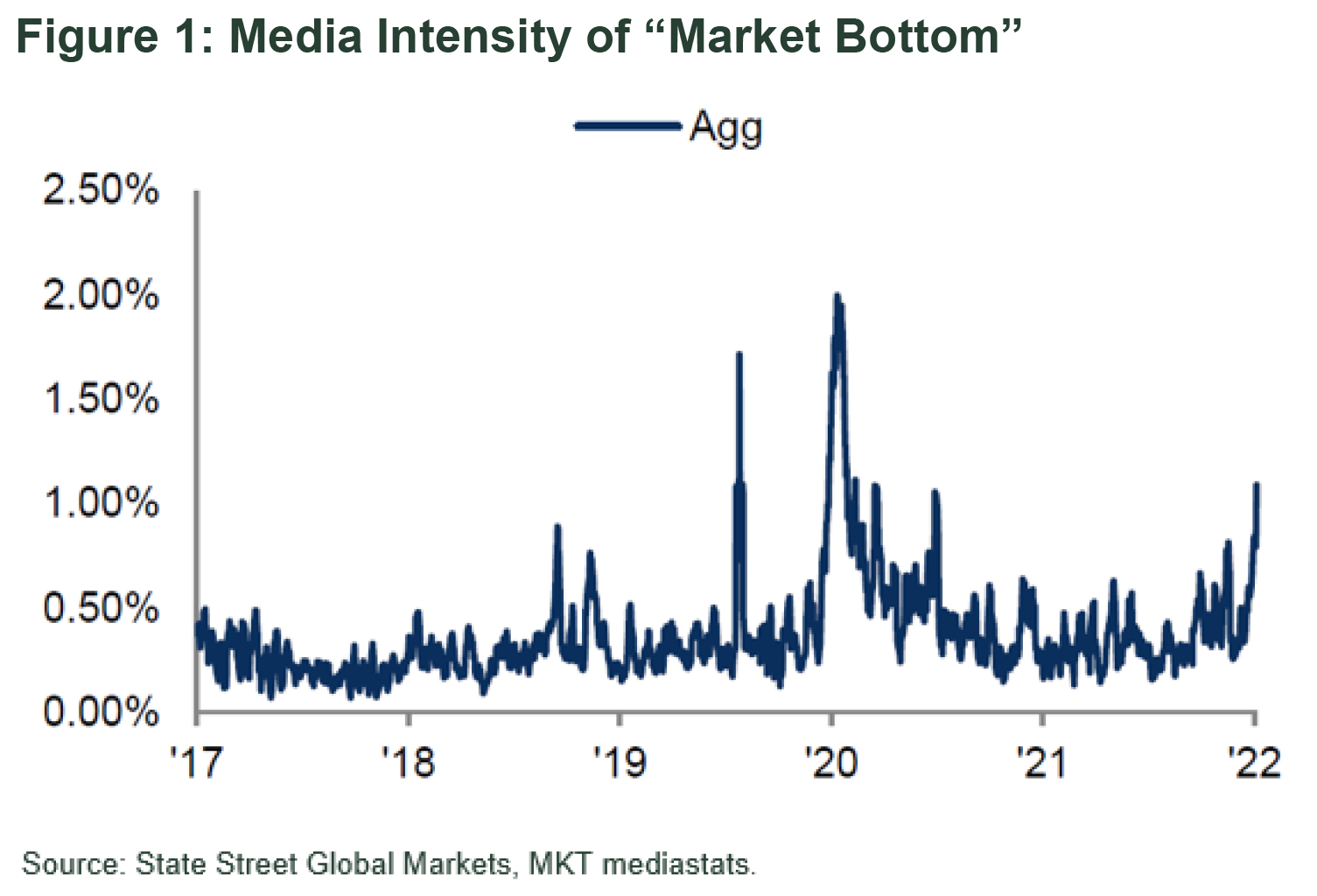

Media intensity of “Market Bottom” trending higher

Year to date the MSCI World Index is down -15.7%, the technology sector is down -26.5% and consumer discretionary sector down -29%.1 After such a large correction many investors are now looking for the opportunities. As shown in figure 1 interest in “market bottoms” is on trend. In this monthly note we take a closer look at the characteristics of this correction to help assess the future opportunities.

Market sell-off consistent with long-term investor preferences

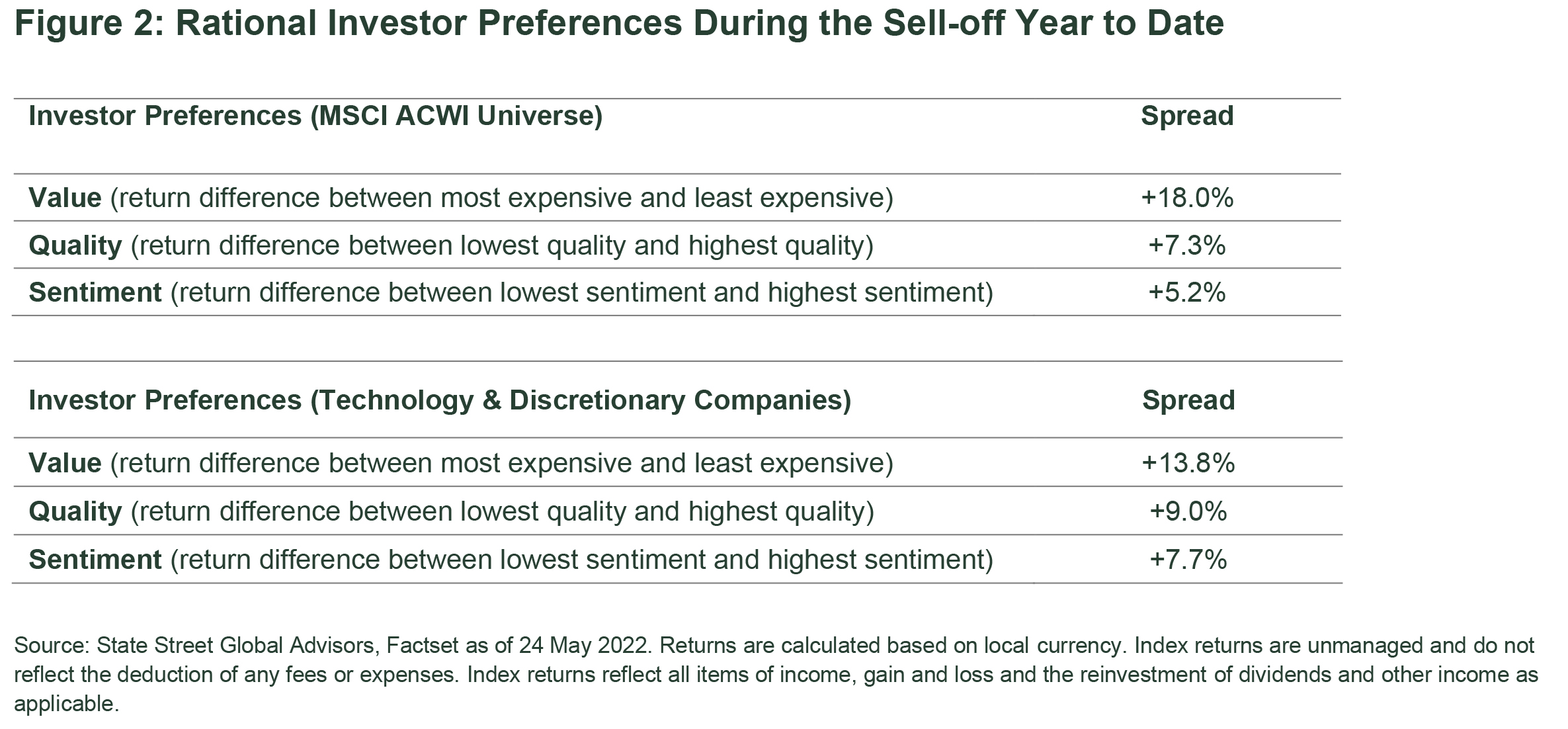

The sell-off in markets has been savage but has largely been rational. As the market has sold off we have seen investors act in line with longer term preferences. We expect investors to prefer less expensive companies and to prefer high quality proven business models and to favour companies that have improving outlooks. Year to date these investor preferences have dominated stock selection and there is little evidence of the baby been thrown out with the bathwater. Figure 2 below highlights the excess return from owning value (+18.0%), quality (+7.3%) and sentiment (+5.2%). This has also been evident in the sectors that have sold off the most, namely technology and consumer discretionary. Across those sectors investors have differentiated based on value (+13.8%), quality (+9.0%) and sentiment (+7.7%).

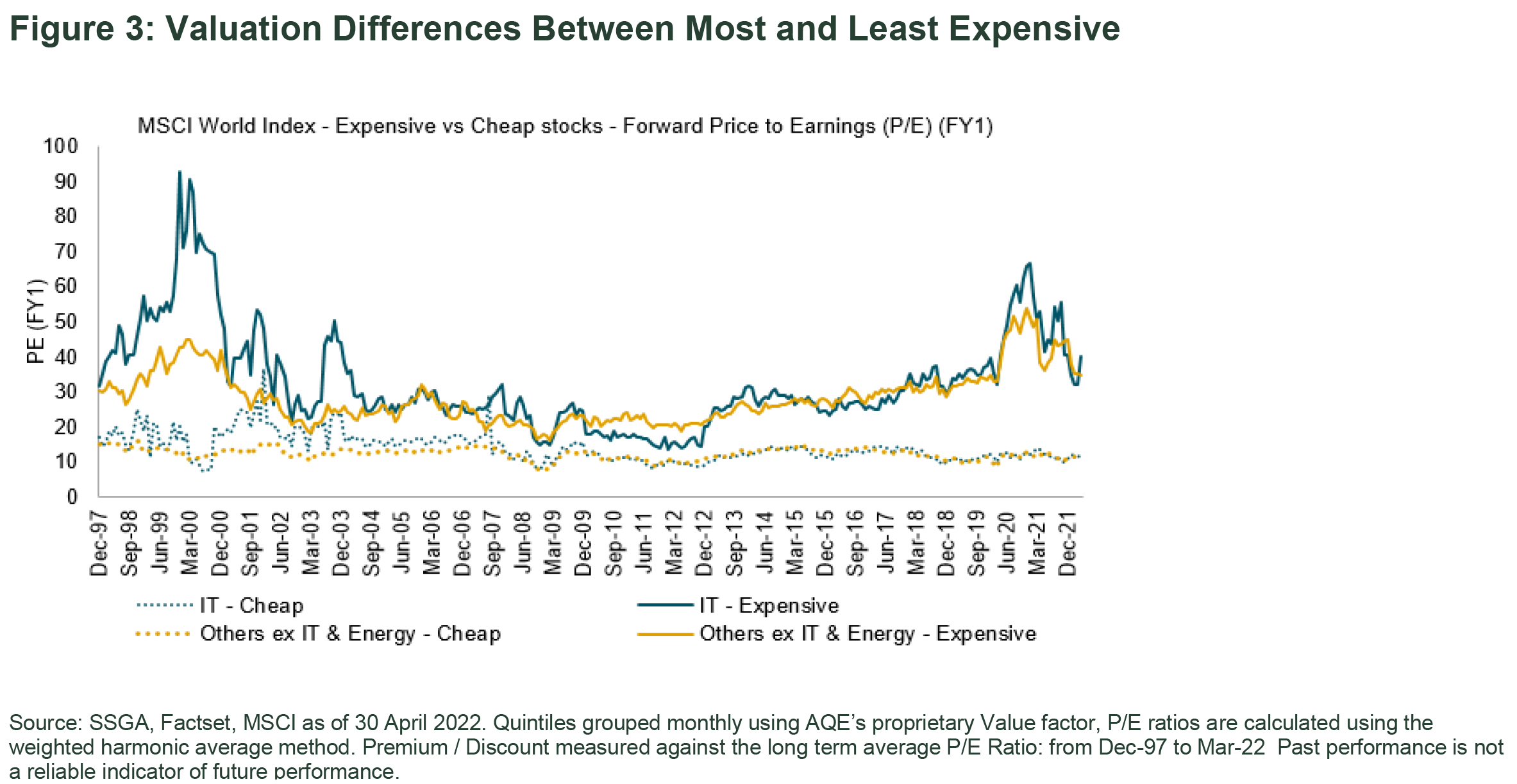

The recent correction is renormalising the market back towards fundamentals after many years of distorted mispricing of securities. Figure 3 provides some insights on the extent of the mispricing within value companies. Figure 3 shows the difference in price earnings ratios between the most expensive and least expensive cohorts back to the technology bubble more than 20 years ago. We have definitely seen the most expensive companies de-rate but using the 2000 experience as a guide there is still room for the most expensive names to de-rate further and for the cheaper companies to re-rate higher. The “buy the dip” mentality appears to be alive and well and we have not as yet seen capitulation from investors buying into expensive growth.

Technology and Consumer Discretionary Preferences Largely Unchanged Across the Technology and Discretionary companies we are not seeing large changes in our preferences since the sell off. Technology Hardware and Storage was our most preferred cohort within the Technology sector at the start of the year. This group of companies outperformed this year (down only -15%2 ) and remains our preference in the Technology sector. Software was one of our least preferred areas within Technology at the beginning of the year and even after underperforming this year (down -34%2 ) remains one of our least preferred. This trend is similar across Consumer Discretionary names. Internet and Direct Marketing was one of our least preferred groups within Consumer Discretionary and remains one of our least preferred despite being down on average – 44% year to date. 2 Preferred Industries Post Sell-off Looking forward we prefer some of the more defensive sectors including Communication Services, Multi Utilities and Healthcare Service Providers. On the cyclical side we prefer a number of industrial subgroups including Construction and Engineering, Marine and Trading Companies. The Bottom Line Investors are naturally interested in looking for the opportunities post a significant market correction. After examining the returns we find no obvious areas of mispricing. In contrast we find investors have differentiated between securities in line with the long term return drivers of valuation, quality and sentiment. In what may appear somewhat contrary we continue to prefer some of the sectors that have outperformed year to date.

By Bruce Apted, Head of Portfolio Management, Australia Active Quantitative Equities