The importance of inflation regimes to asset allocation decisions

Understanding the framework around asset allocation that will assist with client discussions and portfolio strategy in uncertain and changing times.

This is the second of three articles aimed at providing advisers with a framework around asset allocation that will assist with client discussions and portfolio strategy in these uncertain and changing times.

In this article we extend our framework to assess how asset prices behave in the face of significant moves in inflation and real interest rates. As with the growth framework we outlined in our first article, we categorise the inflationary environment into four regimes (see Figure 1). When there is a significant change in inflation, it triggers a change in regime. We define a significant change as being a move in excess of 15 basis points over a three-month period in either a country’s actual inflation rate (measured by the appropriate consumer price index (CPI)) or expected inflation rate (measured by break-even inflation). Since the early 1970’s we have been in one of these four regimes for approximately 60% of the time.

Analysing returns over different inflation regimes gives some unexpected results

When we analyse the historical data, one finding that seems somewhat counterintuitive is the extent to which higher CPI, breakevens and real rates appear to be the most constructive environment for risk assets, such as equities. Whilst a focus on relative value would suggest the opposite, it seems that perhaps the pro-growth backdrop implied by regime E, where both inflation and real rates are rising, more than outweighs other considerations. In Figure 2 we can see that the historical returns of equities are generally above average during periods in regime E – the regime is also one which tends to see more modest drawdowns and volatility. Returns are also attractive in regime F, where real rates (the cost of capital) are declining but inflation is rising, although to a lesser degree than regime E.

A combination of sharply falling rates and inflation (regime H) is the worst environment for risk assets. Returns are often negative; equity drawdowns are worse than in any other environment and equity volatility is highest (see Figure 3). With this backdrop it is unsurprising that regime H is also the one in which government bonds and investment grade credit are the best performing asset classes.

Drawdowns have also been surprisingly large when real rates are rising and inflation is falling (see Figure 4, regime G). This makes sense in that it implies an environment where the cost of capital is going up at the same time that cyclical forces (as reflected in breakevens) are declining.

So is inflation driving returns, or growth?

With the most constructive regimes (E and F) for risk assets being the ones where inflation is rising, a natural assumption is that this must be explainable by a third factor, growth – with perhaps a particularly strong growth environment being responsible for the upward move in both inflation and risk assets.

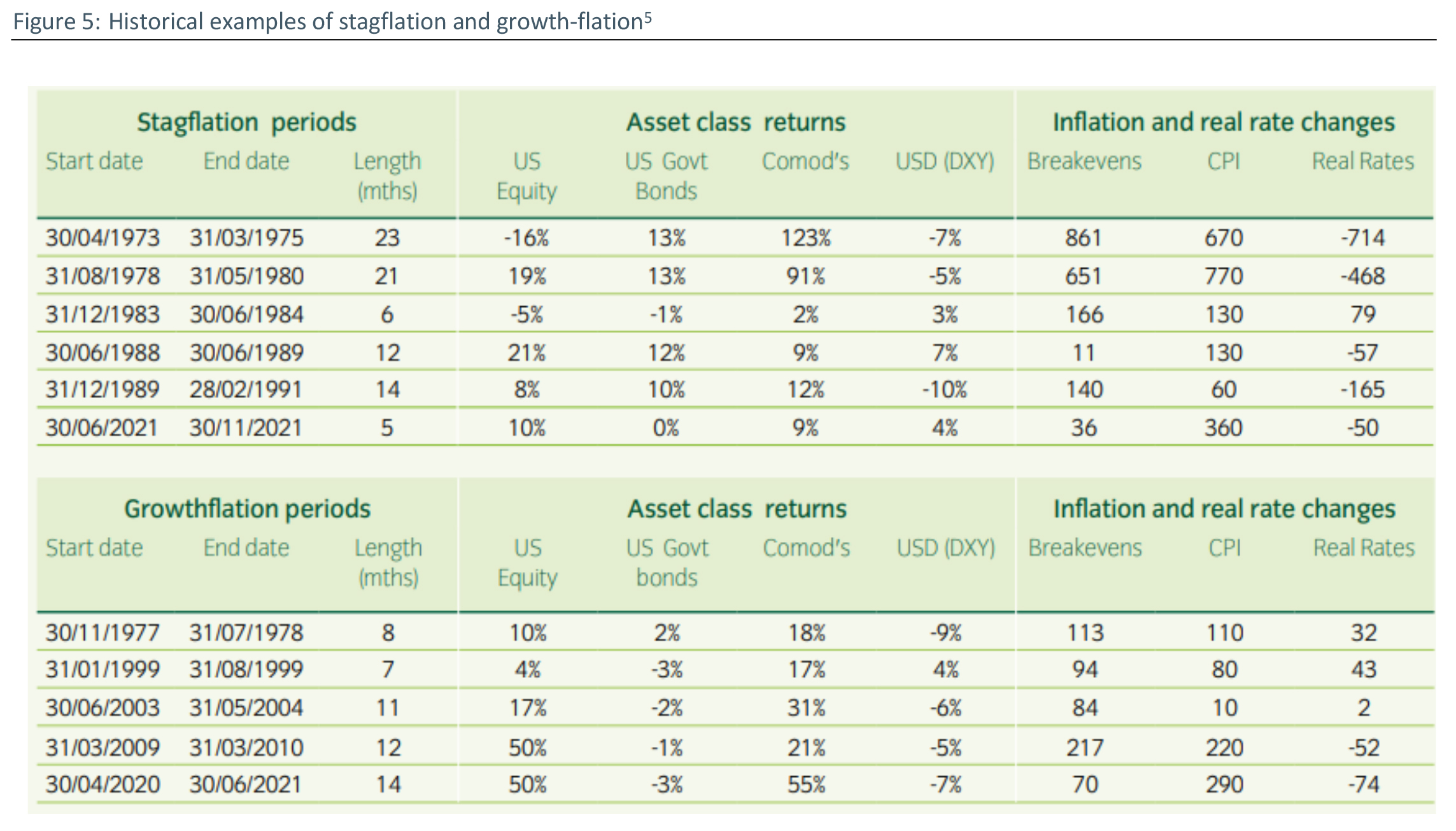

To determine whether this assumption is correct, we can dig deeper into the historical data. Looking back over the past 50 years, we have looked for periods of six months or more where inflation is rising, and we have then extracted periods where growth is either improving (which we define as being in either the Accelerating or Rising growth regimes that we outlined in our first article), or where growth is deteriorating (which we define as being in either the Moderating or Falling growth regimes). These periods of rising inflation where growth is deteriorating, we have categorised as ‘stagflation’ and the periods where growth is improving we have categorised as ‘growth-flation’ – we outline the most notable examples of both in Figure 5.

Our first observation is that the prevailing market narrative that periods of stagflation are inherently bad for risk assets has simply not been true historically. There are plenty of occasions where US equities delivered positive returns despite high inflation and deteriorating growth.

In fact, our analysis shows that inflation, when viewed in isolation, is generally a positive factor for equities rather than negative. During periods of higher inflation, companies can potentially benefit from increased pricing power and thus as a rule, company revenues tend to follow nominal, rather than real GDP. This is compounded when growth is gaining momentum, with the periods of ‘growth-flation’ being among the most positive periods for risk assets historically.

In the final line of each table, we show how the COVID recovery has followed the same trajectory as historical precedent.

The importance of real rates

Although potentially compelling, the conclusion above misses a key point – the importance of real rates.

Real yields can best be thought of as a ‘cost of capital’ for firms, and they matter for risk assets for three reasons:

- Real yields determine the ease of credit flow across global markets. Increasing real yields make it more expensive for companies to borrow, reducing capex investment and ultimately growth.

- Real yield-driven cost increases are not easily passed to consumers (who at the same time will see their own borrowing costs going up) and thus exert margin pressure.

- Real yields serve as a key input to both absolute valuation metrics (as the true ‘discount rate’) and relative valuation attraction between assets (i.e., negative real yields reduce the attractiveness of bonds relative to equities, all else being equal).

To examine the importance of real rates we repeated our analysis looking for periods where real rates were rising and growth was either deteriorating (which we have named ‘stag-tightening’) or improving (which we have named ‘growth-tightening’).

The results demonstrate that a backdrop where growth is gaining momentum and real yields are rising is a comparably positive environment for risk assets as the ‘growth-flation’ environment – reaffirming that ultimately growth has been the dominant factor in equity returns. Periods where growth is losing momentum and real yields are rising have historically been some of the worst for equities, reaffirming our belief that it is necessary to capture the dynamics of both inflation and real rates to best inform our asset allocation decisions.

Growth is key for equity returns but inflation and real rates matter

When we analyse equity markets across the four types of growth and inflationary environments we have outlined above, we can see that in periods of improving growth equities generally perform well, despite either (or both) rising inflation or real rates. When growth is deteriorating, rising inflation helps equity markets, allowing a sideways or mixed performance. The worst environment by far is one in which growth is deteriorating and real rates are rising. If we think of real rates as the effective cost of capital for corporates, this makes intuitive sense.

This reaffirms our view that capturing both inflation and real rate dynamics in our framework is a much more holistic approach to help inform asset-allocation decisions.

Using our framework to analyse the short-term outlook

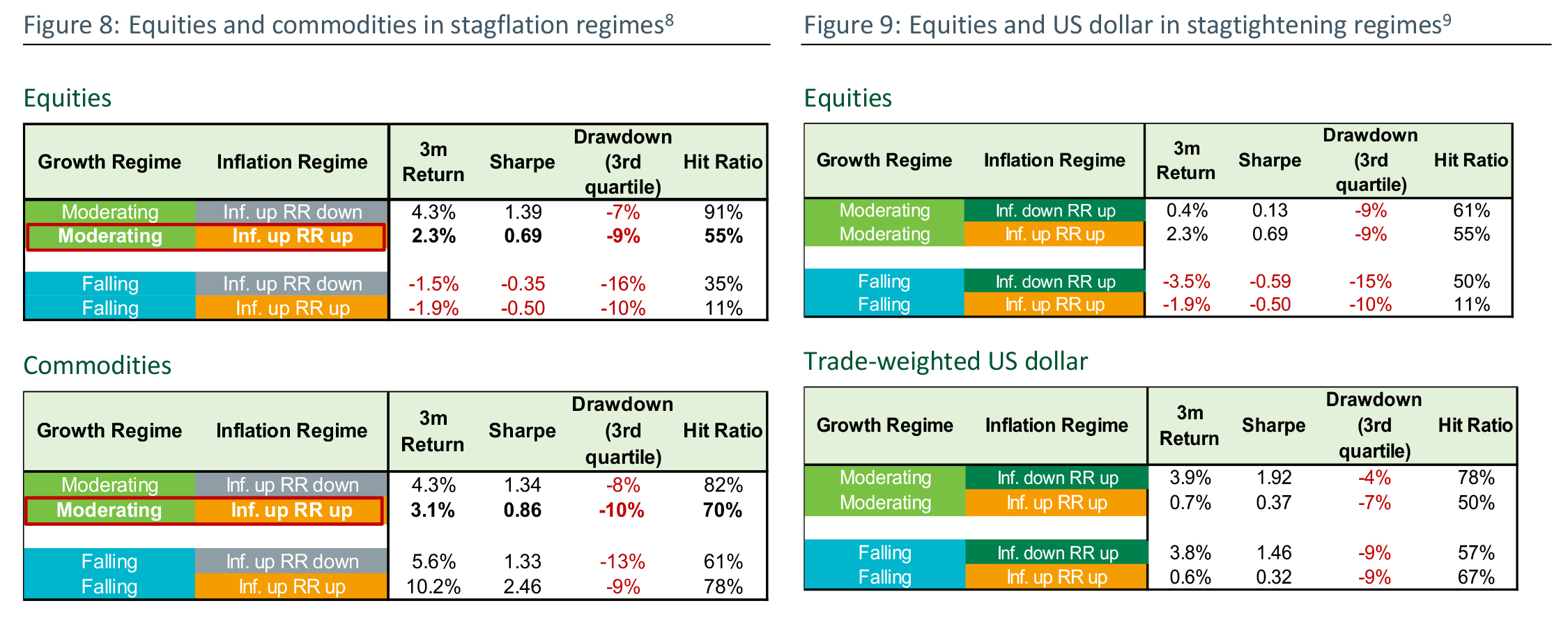

In Figure 8 we have analysed historical data for periods with similarities to the outlook we face today – where growth is moderating and both inflation and real rates are rising. When we compare these to other inflationary environments there are a number of interesting observations we can make. Despite some prevalent market commentary to the contrary, history shows us that equities have still, on average, delivered positive returns when inflation is rising and growth moderating, even when real rates are also rising.

Another interesting observation is when we examine commodity markets using the same framework, returns have historically been attractive during periods of inflation, with growth and real rates only varying the degree of attractiveness. This is intuitive given the intrinsic linkage between commodity prices and inflation.

From a diversification perspective, it is interesting that some of the best regimes for commodities have historically been some of the worst for equities. Commodities may, therefore, represent an attractive source of diversification to equity risk in a world of rising inflation.

Conclusion

It is clear that inflation and real rates are important factors for the returns and volatility of different asset classes, but that their impact is ultimately heavily dependent on growth. In our third and final article we will bring growth and inflation together within our framework and explore how analysing the interaction between the two can help deliver a better asset-allocation outcome.

We trust that this look at inflation regimes provides a helpful lens for your discussions with clients and look forward to sharing our final article in this three part series assessing the interaction of growth and inflation regimes and how this can affect asset prices.

By Matthew Merritt, Head of Multi-Asset Strategy Group

Read part 1: CPD: The importance of growth regimes to asset allocation decisions

———