Best practice client engagement – Understanding women as the drivers of investment growth

The increase in female investors isn’t just about Millennials.

Jedi Knights, Millennials, and other Census tales

Yes, it’s that time again. Every four years, we get to pore over the Census results and see how the picture of Australia has changed.

As you can imagine, collecting and analysing the data from 25 million people and 10 million households is a mammoth exercise, which is why the Australian Bureau of Statistics releases its findings in a staged approach, starting in June 2022 with high level housing and population data, continuing with labour force and location-based analysis in October 2022, and more complex socio-economic analysis to be released mid 2023.

Along with discussions about the seemingly reducing importance of religion to Australians, (I’m not sure how many people identified as Jedi Knights this time around), the main story from this census is about the rise of the Millennials, who, as a group, are now the same size as the Baby Boomers – each representing around 21.5% of the population. Sandwiched between those two groups is Generation X, who accounts for just over 19% (see Figure 1, below).

Understand the trend and stay ahead of the curve

Digging deeper into data can help businesses – including financial advice firms – stay ahead of the curve by understanding trends, anticipating customer needs, and adjusting their proposition and client experience accordingly.

For example, the prominence of the Millennial group, and their increasing difficulty in entering the housing market, has seen rapid growth in demand for renovation/home improvement products that can be used in rental properties (such as stick-on picture hooks and bathroom accessories).

For financial advisers, the rise of the Millennials, the oldest of which are about to turn 40, could well be the catalyst to rethink the importance of this segment. Afterall, as well as being the biggest spending group, the Millennials stand to benefit from the great intergenerational wealth transfer starting to unfold.

Of course, the Census is just one of many data sources that can give advisers a glimpse of the future. Other, more finance specific, research can be equally, if not more, powerful in helping advisers anticipate the evolving needs of clients.

And when we broaden our data horizons, we can see that, arguably, a more fundamental trend unfolding is the increasing power of female investors.

The rise of the female investor

Much has been made of the growth in female investor numbers – especially younger females – since the start of the pandemic.

According to the ASX [2], 2020 saw women make up 45% of all new investors in Australia – up from 31% among those who started five to 10 years ago. And this trend appears set to continue, with women accounting for 51% of those planning to invest in the future.

These findings are reinforced by Investment Trends’ research[3], which identified the role of young women in driving growth in exchange-traded fund (ETF) investing (with the number of female ETF unitholders nearly doubling to 423,000 in 2021, and the biggest growth among 18-34 year old females), and in online investing more generally (with the proportion of online investing accounts opened by females more than doubling over the last 5 years[4]). Indeed, according to micro investing app, Sharesies, 60% of its customers are female[5].

The same trends have been observed globally too, with research by trading platform eToro[6] suggesting that 42% of current female investors only started investing in 2020 or 2021. Like Australia, it is younger females accounting for much of this growth.

But this isn’t just about Millennials

While much media focus has been on the growth of the Millennial female investor, the more significant ‘power shift’ is actually occurring at the older end of the age scale, where simple demographics will soon see women control the majority of invested wealth.

US research[7] – likely equally applicable in Australia – estimates that women currently control around one third of investable assets, and 70% of investable assets are controlled by Baby Boomers (two thirds of these assets owned by joint households). To the extent that women typically outlive men (in Australia, average life expectancy is around 81.2 for males and 85.2 for females[8]), the next few years are expected to see a massive shift of wealth into the surviving female partners.

In fact, by 2030, American women are expected to control much of the $30 trillion in financial assets that Baby Boomers will possess[9]. The same thing is likely to occur in Australia.

But what does this mean for financial advisers?

On the one hand, research suggests women are more likely than men to seek out expert financial advice. But on the other, the death of a spouse can act as a significant catalyst to change financial advisers. According to McKinsey[10], 70% of women switch their wealth relationship to a new financial institution within a year of their spouse’s death.

Retaining female Baby Boomer clients can thus become a real sustainability challenge for advice practices.

Understanding female investors

Without overdoing the whole ‘men are from Mars, women are from Venus’ narrative, the truth is there are some fundamental differences – uncovered by research – in motivation, mindset, and behaviours between male and female advice clients. Understanding these differences can help advisers tailor their practices across client acquisition, engagement and communication, and advice and portfolio construction. Ultimately, this understanding is crucial to delivering the optimal advice experience and building more effective and long-lasting relationships with female clients.

More self-aware, less self-confident, more demand for advice

The world of investing can be very complicated, with many traps for the unwary. Being highly educated and earning a big income doesn’t necessarily translate into financial literacy. And while research has shown gender-based differences in investment knowledge and confidence, much of this is likely to come down to a lack of exposure by women. On the other hand, a tendency for men to overestimate their investment knowledge has been frequently observed. An IPSOS study[11] in the US found 61% of men considered themselves to be ‘good investors’, compared to 47% of women.

It is perhaps a greater self-awareness around a lack of investment experience and knowledge that explains why female investors are far more likely to seek out a financial adviser for help. According to the ASX[12], female investors are almost 50% more likely than males to seek the help of a financial adviser when making investment decisions.

Motivated by different outcomes

Male and female investors are often motivated to invest for different reasons.

The Australian Investor Study[13], when looking at personal and financial goals over a three-year horizon, found men were more focused on planning for retirement than women. Women were found to value other goals, such as volunteering, going back to study or learning a new skill, and getting their finances in order.

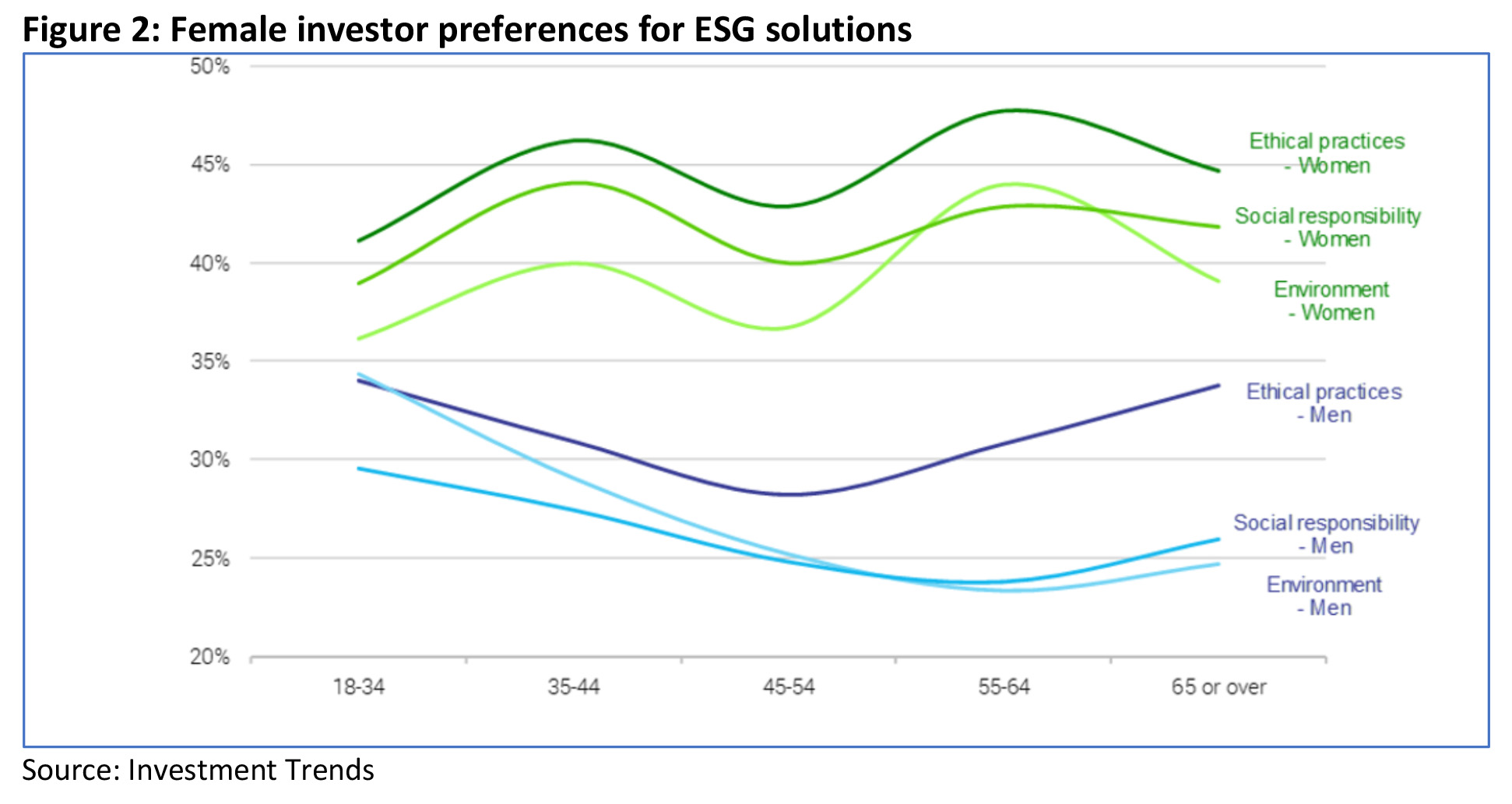

Numerous studies have also found women are more likely than men to prioritise ESG and philanthropic investment goals.

For example, Investment Trends research[14] (shown in Figure 2 below) shows female investors in Australia place markedly higher importance on ethical practices, social responsibility, and protecting the environment, when making investment decisions.

Often, differences in life roles also drive different investment motivations. Women more often find themselves in the role of caregivers, either to their own children or for elderly parents. Census data shows women as the sole parent in 80% of all single parent families in Australia[15]. This means they are more likely than men to prioritise goals involving their children, such as long-term care and estate planning.

Looking for different things in an adviser

The different motivations for investing also translate into differing needs from a financial adviser.

Cerulli[16] researchers observed that female investors would rather engage in a holistic, goals-based process that prioritises financial planning over portfolio construction. Investments are more likely to be a means to an end, so emphasizing their alignment with end goals and objectives is critical for financial advisers who want to address their key concerns.

Women also place a high degree of importance on the relationship aspects of working with an adviser, well ahead of investment performance, as seen in Figure 3 below. This importance generally translates into more loyalty, with female advice clients being a third more likely than males to follow their adviser to another firm[17].

Different risk preferences, different responses

Almost two thirds of Australian female investors surveyed by the ASX[19] indicated a preference for guaranteed or stable returns, compared to just half of male investors. Conversely, male investors were more than twice as likely to accept high variability in exchange for greater potential performance (21% v 10%).

Despite this, female investors were found to be more likely to stay the course and be patient in the event of a downturn. When asked[20] how they would respond to a sudden 20% market fall, 42% of females said say they would be concerned but would wait to see if conditions improved before making any portfolio changes (compared to 20% of males).

Perhaps contributing to this greater patience is a lower tendency to be distracted by the ‘noise’ around investment and market performance. Almost half of all male investors surveyed by the ASX said they check their investment performance daily or weekly, compared to around one quarter of female investors[21].

Do women make better investors?

In light of the evidence suggesting female investors are more considered, more patient, and more willing to seek expert help, it’s perhaps unsurprising that various studies have concluded that women are also better investors.

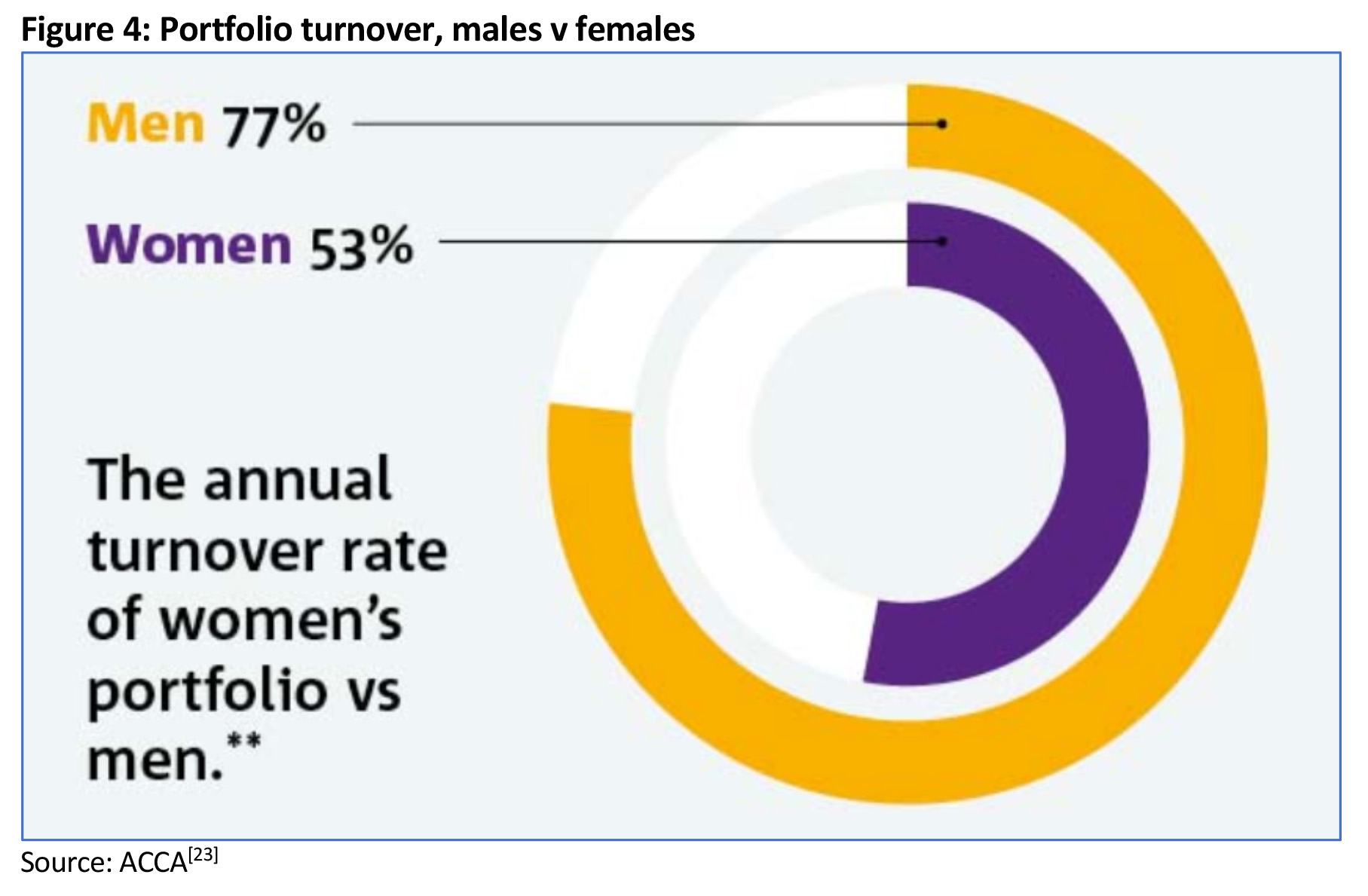

A 2018 study[22] of 2,800 investors by the UK’s University of Warwick found that female investors had outperformed the FTSE 100 over the last three years, outperfoming their male counterparts.

While annual returns on investments for men were on average a marginal 0.14 per cent above the performance of the FTSE 100, female investors outperformed men by a further 1.8% per annum, a significant margin, especially were it to be replicated over the longer term.

Among the biggest contributing factors to this difference were a lower tendency by females to trade (thus saving on fees), and their lower exposure to more speculative stocks.

Professor Neil Stewart, who oversaw the research, commented:

“Women take a more long-term perspective, trading less frequently. This possibly means women are investing more to support their financial goals, whereas men are attracted to what they see as the thrill of investing.”[24]

Tailoring your proposition to better meet the needs of female clients

Eye tracking research[25] revealed that advisers (both male and female) who were meeting a heterosexual couple focused their eye contact on the male 60% of the time.

But aside from removing this type of unconscious bias from your interactions with female clients, how else can you adjust your proposition to better meet their needs?

A good starting point is to revisit your client discovery and onboarding processes. Are they skewed, intentionally or not, towards capturing investment objectives and goals that are more financial and less holistic? If so, this should be corrected. Is your ESG proposition up to scratch, in terms of both your access to ESG options, but in the way you connect clients’ holistic values with your advice and recommendations?

As always, communication is crucial. Cerulli’s Best Practices[26] for advisers working with female investors highlight the importance of:

- use of active listening techniques

- small, personal gestures such as recognising milestones, offering condolences, and expressing gratitude for referrals

- equal engagement and ongoing involvement of both partners in planning conversations, review meetings and ongoing communication which emphasises progress towards goals, rather than investment performance.

In terms of your overall offering does it recognise the importance of children, for example, by offering multi-generational planning services?

And, to help bridge the confidence and knowledge gap, do you have a strong financial literacy offering through educational resources such as videos or webinars or other channels and materials? And is any of this material suitable for their older children?

Special consideration should also be given to the circumstances and needs of those female clients ‘in transition’ because they have been widowed, separated or divorced. Advisers working with these clients must be adept at understanding grief timelines, showing compassion, and adapting to clients’ desired pace throughout the process, which may literally take years. In particular, emotional support becomes a key part of the role because advisers who express vulnerability and empathy create a safer environment for women to grieve and rebuild their lives. In many cases, advisers targeting this segment (as some do) will often work in concert with an extended network of professionals (e.g., lawyer, mediator, estate agent, therapist, life coach, and accountant).

In summary

Whilst the rise of the Millennial female investor has captured much recent media attention, a far more fundamental trend with respect to older female investors has been building, one that will soon see them at the forefront of the looming intergenerational wealth transfer, and which will ultimately see them control the majority of investable personal wealth.

Female investors typically exhibit important differences to males when it comes to investment objectives, style, and risk tolerance. They are generally more holistic in their goals, more risk aware, and more likely to be disciplined and patient in sticking to a plan. They also place more importance on ESG factors when making investment choices. They are also more likely to be acting as a primary caregiver to their children or elderly parents, which can often inform a different perspective on investment objectives.

Advisers seeking to offer the optimal advice experience to female clients must be mindful of these differences, and reflect them across their approach to client acquisition, engagement, communication, and planning and portfolio construction processes.