Sustainable investing in Emerging Markets equity – seven implications for investors

Seven important ESG factors when investing in Emerging Markets equities.

The terms ‘ESG’, ‘Responsible’ and ‘Sustainable’ have become commonplace in the investment industry. This article frames the strong interconnectivity between financial returns and environmental and social values, the importance of which is pronounced in Emerging Markets. Emerging Markets specialist Ashmore Investment Management, a PAN-Tribal Asset Management investment partner, considers seven implications for investors.

Although the terms ‘ESG’, ‘Responsible’ and ‘Sustainable’ have become increasingly commonplace in the investment industry, their definitions often remain unclear and subjective. This can lead to misconceptions of how they enhance fundamental investment. For Ashmore, Sustainable/ESG Investing promotes high quality and long-term orientated companies with low ESG risk exposures that understand and address such exposures to the benefit of all stakeholders.

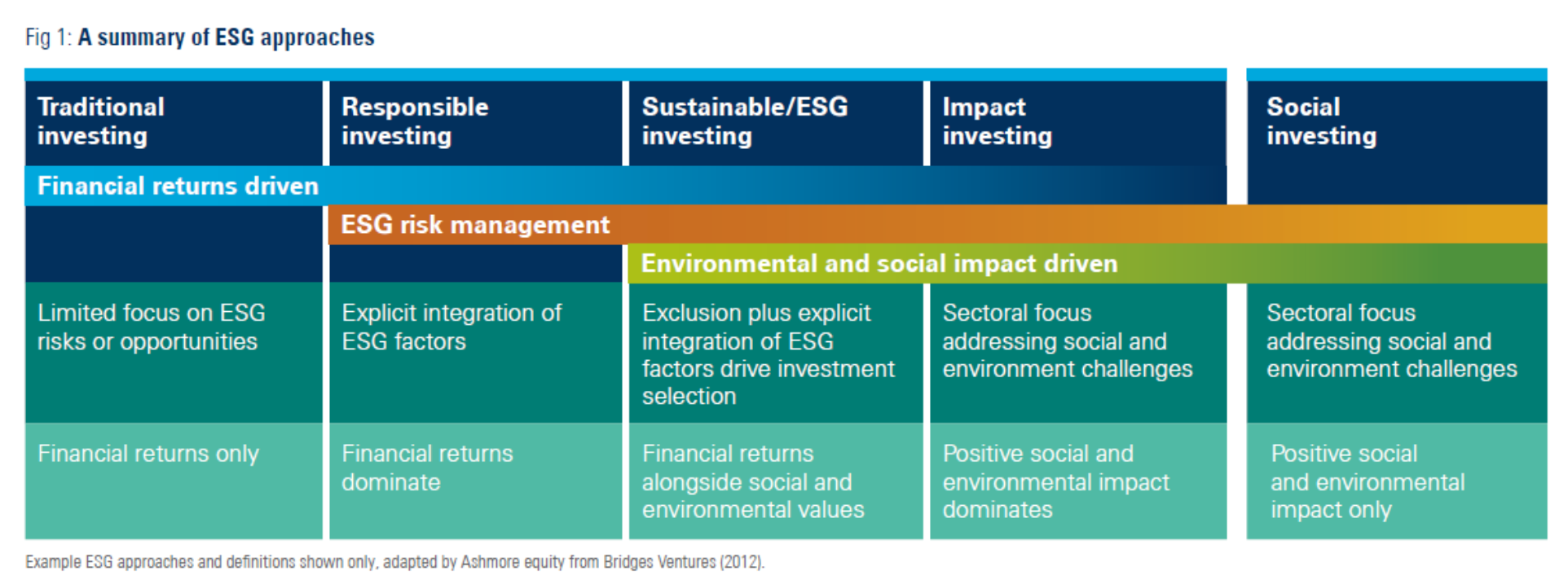

1. The spectrum of ESG investing

Sustainable or Environmental, Social and Governance (ESG) investing (the two terms are used synonymously in this article) has seen significant evolution, yet definitions still remain broad and can be interpreted in different ways. Consequently, it is important to clearly define an investment approach.

Historically, ‘Traditional’ investing was focused on maximising financial returns without giving credence to any ESG risk considerations.

In today’s world, ‘Responsible’ investing goes a step further. It integrates ESG risk assessment alongside other fundamental factors in a ‘Traditional’ investment process, while maintaining a focus on maximising financial returns for investors.

For Ashmore, Sustainable/ESG Investing goes another step further. By excluding certain industries and stocks, while embracing active ownership and engagement, the approach fosters corporate quality as well as the sustainability of future growth. This benefits both long term shareholder returns, as well as broad social and environmental values.

At the other end of the spectrum, there are ‘Impact’ and ‘Social’ Investing which prioritises environmental and social impact over financial returns.

Takeaway 1: The spectrum of ESG investing

Sustainable/ESG Investing targets financial returns alongside social and environmental values.

2. Why is sustainability important?

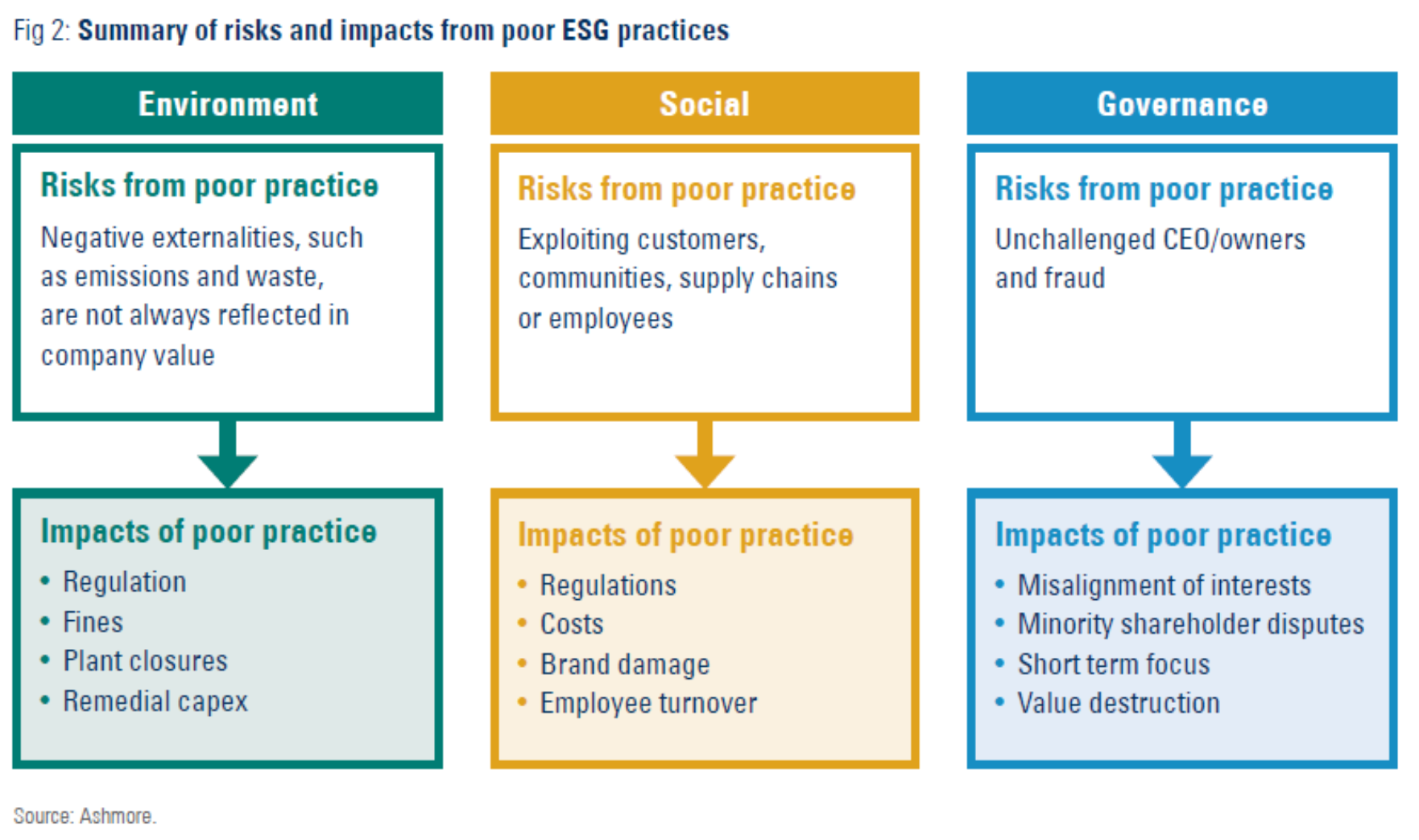

Sustainability matters because, first and foremost, large negative outcomes for profitability, growth and shareholder returns can arise from poor ESG practices. One only needs to recall the negative consequences and impact on share prices from Hyundai Motors land acquisition in September 2014, or Vale’s Brumadinho dam disaster in January 2019, as some of the more dramatic case studies which demonstrate the advantage of embracing Sustainable/ESG Investing.

The virtues of incorporating ESG factor assessment extend beyond risk reduction. Strong ESG performance can also have a positive impact on a company’s profitability. Consumers are often willing to pay a premium for sustainable products while businesses are increasingly incorporating ESG factors when choosing new suppliers.

As a result, strong ESG practices are likely to help a company win new clients, grow revenues and open up new opportunities. Strong ESG practices can also help a company attract and retain talent creating strong competitive advantage in businesses which depend on human capital.

An additional benefit is that strong ESG principles and policies are reflective of a business that is well run and has a long-term orientation. A company which integrates ESG factors into its business plan is indicative of a management team which is better at planning and managing the long term risks.

Hence, it guides an investor towards stronger management teams. Further, such companies are better able to allocate capital and execute their growth plans by overcoming operational challenges that can arise from weak ESG practices.

Takeaway 2: Why is sustainability important?

Sustainable/ESG Investing mitigates permanent loss of capital risk while also steering investors to attractive long-term investments, which can enhance risk adjusted returns.

3. What is sustainable investing?

Sustainable/ESG Investing promotes companies that have strong business models and practices, and which consider their impact upon the environment, employees, communities and other stakeholders. This enables the company to grow sustainably while concurrently contributing towards broader socio-economic development.

Sustainable/ESG Investing is underpinned by and guided by international standards and principles, as well as global development initiatives. These include the UN Global Compact and UN Sustainable Development Goals, as well as the OECD principles for responsible business conduct.

Companies that consider all stakeholders can enhance the sustainability of their returns over the long term and lower operating risk. In contrast, uneven consideration undermines sustainability and risks reputational damage, regulatory intervention, employee protest and value destruction.

A company’s sustainability can be assessed by the strength and enduring nature of their competitive advantages, which are supported by long term planning, sensible business practices and investment. ESG factors are inextricably linked to an assessment of a company’s competitive advantage and its growth potential.

The greater the research, analysis and engagement undertaken on ESG issues, the stronger are the insights into the quality of a business and the sustainability of its returns. Companies which score poorly on ESG signal that their returns are unsustainable in the long run, hence will be poor investments.

The explicit incorporation of ESG into an investment approach promotes a long term investment mind set which is fundamental to stewardship of capital. It also ensures an investor has an in depth and more complete understanding of the quality and underlying drivers of a company. This enables longer term and higher conviction investing.

The alignment of company behaviour with the long term interests of key stakeholders is possible via effective stewardship. This involves regular interaction with investee companies to encourage better ESG practices, in turn creating additional shareholder value.

Takeaway 3: What is sustainable investing?

Promoting companies that have strong business practices which incorporate the impact on all stakeholders fosters the company’s sustainable growth and contributes to wider socio-economic development.

4. Balancing the demands of ESG stakeholders

The total value created by a company is the profit delivered to shareholders as well as the benefits delivered to customers, suppliers and employees. Increasingly, it is being acknowledged that total value includes the benefits delivered to wider society and the environment. Companies that deliver value to all stakeholders have more sustainable returns over the long term, with significantly lower operating risk. Unfair distribution of value among stakeholders is ultimately unsustainable.

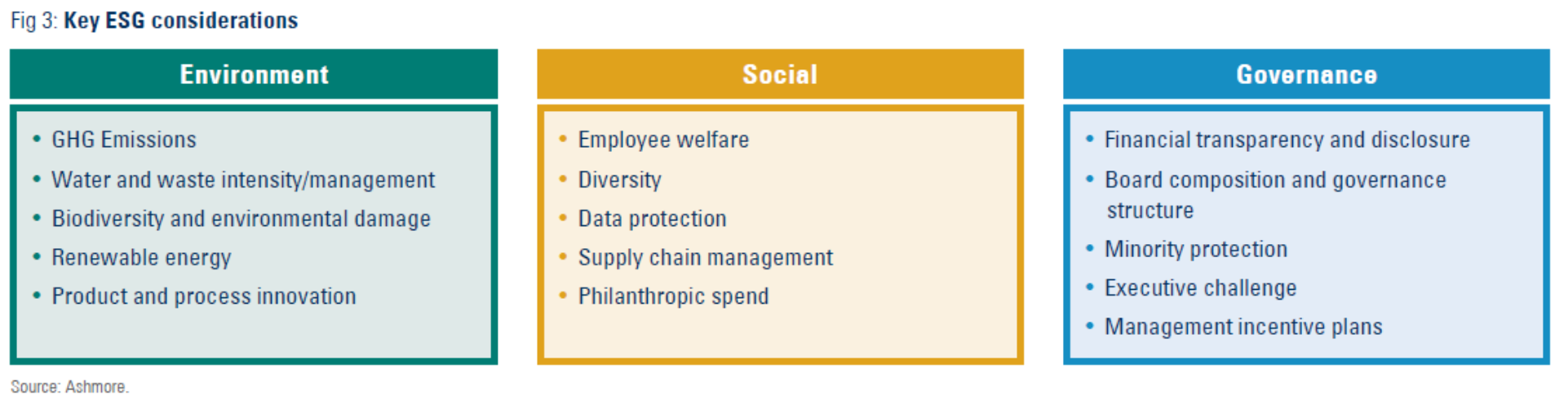

ESG analysis needs to consider multiple factors and these need to be evaluated and scored on a consistent basis. Some of the key criteria are summarised in figure three.

To sustain a company’s long term growth trajectory, the needs of environment, social and governance interests need to be balanced. However, there are often conflicting demands between stakeholders. Consequently, it is important to assess the materiality of ESG risk to a specific business model. ESG risks to a mining company are very different to the risks to an internet business, for example.

To be able to judge materiality requires an in depth knowledge of the business. This means an integrated approach, in which the fundamental stock analyst also carries out the ESG assessment, is optimal. Relying on third party ESG scores or an independent ESG team can result in a formulaic view and hence diluted value.

ESG interests frequently diverge. An investor must have a consistent framework for assessing and, in the case of a sustainable approach, excluding industries and stocks. For example, the use of resource intensive materials, such as cement, for use in infrastructure projects can be crucial in supporting local socio-economic development. Should the extractive industry be penalised in an ESG framework, or not?

A balance needs to be struck between the societal requirement for infrastructure and development with the environmental impact of the extraction and production of cement and other such materials. The answer is invariably idiosyncratic to the company’s business model, and this reiterates the importance of building in depth knowledge and a proprietary view.

Takeaway 4: The spectrum of ESG investing

Balancing the needs of ESG demands is key to a company’s sustainable growth.

5. Overcoming the challenges

Sustainable Investing requires overcoming several challenges, especially in Emerging Markets. One of the most predominant is around data.

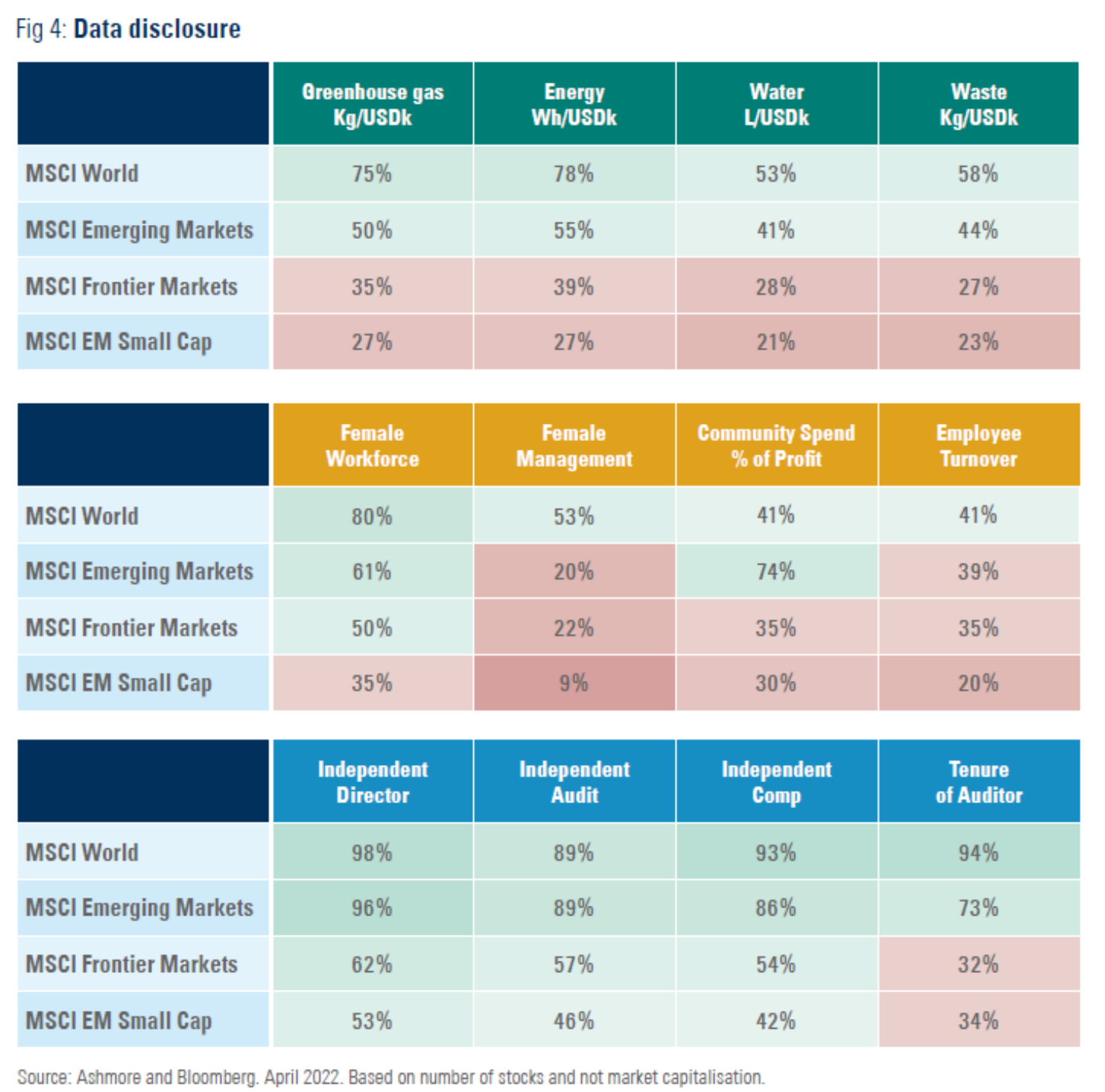

First, data disclosure in Emerging Markets can vary meaningfully. Figure four provides a synopsis of ESG data availability for companies based on the percentage of a common index. Overall, there is meaningful disclosure across E, S and G by Emerging Markets companies although G stands out as most advanced.

Generally speaking, as one looks towards smaller companies the level of disclosure falls. Consequently, while some larger cap Emerging Markets companies have world class disclosure, aggregating a universe of ~1,400 companies pushes the percentile disclosure lower.

Absent or poor historical data disclosure can also make it challenging to map a company’s sustainability ‘journey’. Consequently, it is imperative to have a deep understanding of a company to be able to ascertain the likely underlying exposures and also to build a view on its trajectory.

The more underlying asset owners and investors embrace Sustainable Investing and engage, the faster the improvement in disclosure to offset this challenge. For example, in 2017 the percentage of issuers in Emerging Markets with data available for GHG emissions was 27% compared to 50% currently[1].

Second, data standardisation is mixed at best. Currently, data disclosure and standardisation are inconsistent between reporting frameworks and they also vary according to country regulations. There have been significant developments towards better standardisation of global ESG policies and reporting.

Indeed, the Climate Disclosure Standards Board (CDSB), the Global Reporting Initiative (GRI), the International Integrated Reporting Council (IIRC) and the Sustainability Accounting Standards Board (SASB) recently co-published a shared vision and statement of intent for more comprehensive and standardised corporate reporting. However, while such global initiatives provide a roadmap, ultimately local regulatory frameworks and their mandatory implementation will drive data improvement.

Third, the subjectivity of assessment (data materiality), in combination with the inconsistent levels of disclosure and standardisation, mean that ESG factor views will vary significantly. Just as ‘traditional’ investors have differing views on the importance of different stock fundamentals, the same can be said for ESG factors.

Non-financial factors that are harder to quantify offer more information asymmetry and hence greater ability for an active manager to add value. Proprietary research and engagement with companies is therefore crucial to understand their business and long term sustainability, rather than relying on third party data providers.

Takeaway 5: Overcoming the challenges

ESG challenges are solvable and themselves a source of added value to an active manager.

6. Have Emerging Markets embraced ESG?

Emerging Markets investing is often prone to misperceptions owing to their developing nature and sometimes entrenched investor views. The same will likely also be true for ESG.

Attitudes towards ESG are changing dramatically in Developed Markets, given the interlinked global economy this is also spreading to Emerging Markets. Despite being at an earlier stage of economic development, Emerging Markets are making progress, which is only set to accelerate in the upcoming years. A few examples of change are detailed below:

- Colombia, Argentina, Chile and Brazil are working with the UN on a programme to enhance the integration of the SDGs in corporate sustainability reporting.

- China has committed to be carbon neutral by 2060 and South Korea by 2050. Incidentally both countries are home to some of the world’s leading companies in electric vehicles and renewables.

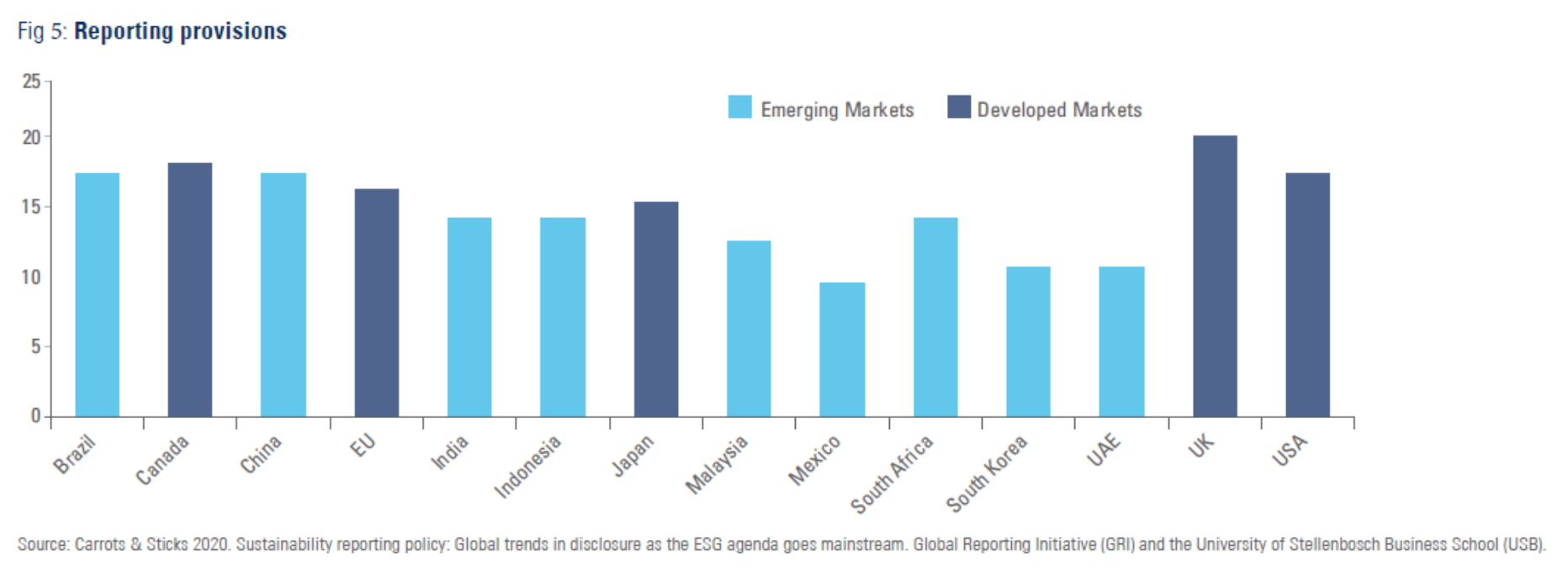

Figure five shows reporting provisions, defined as reporting requirements (e.g. policies) and reporting resources (e.g. guidance documents) across countries. It shows comparable levels of disclosure in Emerging Markets compared to Developed Markets.

Companies are important contributors to socio-economic development in Emerging Markets and hence they play a key role in promoting sustainability. This, in turn, can provide an attractive long term operating environment. By identifying and promoting high quality companies that can balance the needs of the community, environment and shareholders, the returns, both quantifiable and non-financial, can be rewarding.

ESG risks can be more pronounced in Emerging Markets due to sometimes weaker regulatory oversight, lower disclosure requirements and a more dynamic policy environment. The higher ESG risks mean that there is likely to be a greater divergence in performance between companies that successfully manage ESG risks and those that do not. In our experience, this reinforces the importance of carrying out primary research and building proprietary views.

Takeaway 6: Overcoming the challenges

Sustainable/ESG Investing can have a proportionately larger reward when investing in Emerging Markets

7. Implications for portfolio characteristics

There are several direct and indirect implications for the likely characteristic of a portfolio that embraces sustainability, in our experience. This includes a longer-term mind set and hence longer investment time horizon and holding period. It also lends itself to higher conviction investing implying fewer stock holdings.

Exposure to stocks with inherently shorter term and more cyclical drivers will comprise a smaller percentage of such a portfolio, while the focus and hurdle on quality attributes would be greater. Therefore, at a sector level, energy, materials and industrials are likely to feature much less.

Takeaway 7: Implications for portfolio characteristics

Sustainable/ESG Investing can buoy risk adjusted returns, support global socio-economic sustainability, as well as provide portfolio construction diversification advantages

———–