A family affair – the challenges of retaining intergenerational wealth

The great intergenerational wealth transfer presents enormous challenges to financial advisers.

The great wealth transfer – opportunity or threat?

The impending multi-trillion-dollar intergenerational wealth transfer, and its social, economic, and political consequences, has been a hot topic in the media for a few years now.

Naturally, it has also been a ‘front of mind’ issue for many financial advisers grappling with the implications of this shift of money – from their clients to their clients’ children – on longstanding relationships, and even on the future sustainability of their practice. With research suggesting that many Gen X and Millennial inheritors are likely to seek their own financial adviser rather than stick with the one used by their parents, the challenge to retain transferred wealth can indeed be a significant one.

For those advisers seeking to retain this wealth – by serving the next generation within a client family – understanding the motivations and mindset of younger clients is critical, as is a framework to facilitate more forward planning, transparency and communication between your clients and their heirs.

The nature of the challenge

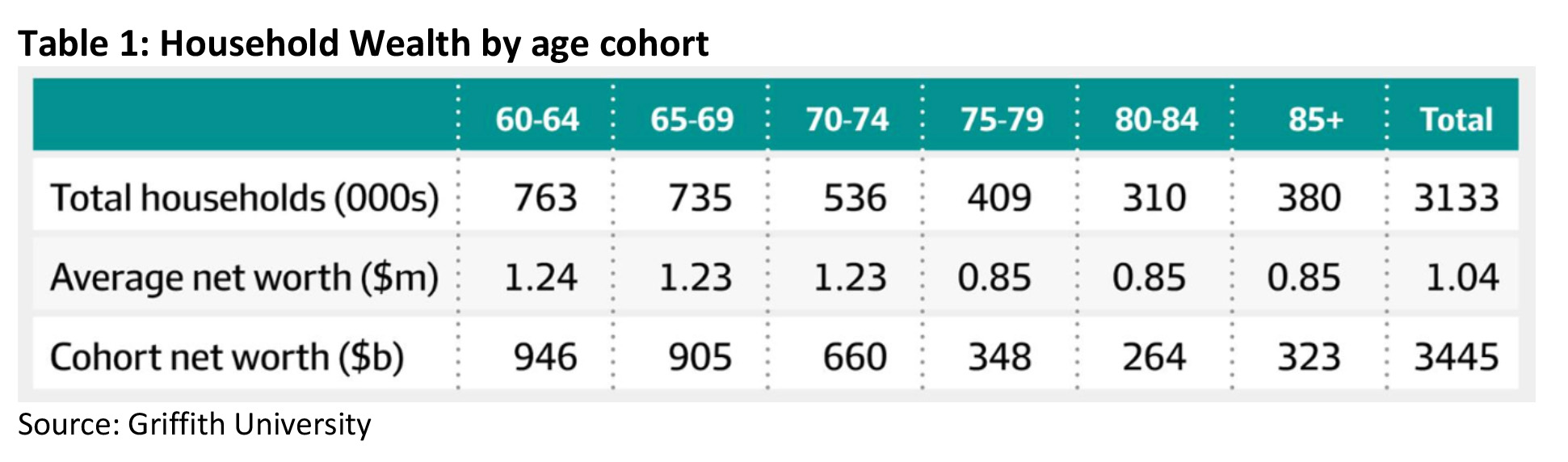

According to research by Griffith University[1], the amount of wealth that is ripe for transfer over the coming years is around $3.5 trillion. And while the majority of transfer is likely at least a decade away, as Table 1 below, shows, around half a trillion in wealth is currently sitting with individuals aged 80 or older, with transfer therefore imminent.

Experts estimate Gen Xers will inherit just over half (57%) of this wealth, with Millennials set to collect the bulk of the rest[2].

Advisers seeking to keep managing this transferred wealth can face an uphill battle to do so. This is partly because of the complex dynamics of parent-child relationships, and partly because of the different financial behaviours and attitudes that characterise younger clients.

Perhaps best summing up the scale of this challenge is US research[3] by Investment News, that found that 66% of children terminate the services of their parents’ financial adviser once they have inherited their wealth.

(As a quick exercise, what would the loss of two thirds of your baby boomer clients do for your practice – and your ability to keep serving your other clients?).

Research by Coredata[4] explored this topic in more detail with UK and US based advisers and found that even advisers themselves were pessimistic. When asked “What percentage of your primary clients’ heirs do you think will retain your services after your client passes away?”, US based advisers estimated just over half (57.1%), whereas UK advisers guessed a mere 41.7% of clients would stay.

So, what’s at play here?

The uncool parent phenomena

Certainly, one explanation can be found in the deep-seated psychology of parent-child relationships. In simple terms, it is normal for each generation to dismiss their elders as ‘uncool’. This characterisation extends from everything to the way our parents behave, to the music they listen to, and the products they buy. It also often extends to the professionals they use (who get thrown into the same bucket).

This almost innate tendency to regard our elders as ‘out of touch’ with contemporary society, coupled with our own need to forge our own identities independent of our parents, can be explained by basic psychological theory.

A fundamental premise of self-determination theory is the way the achievement of autonomy and competence positively drives our overall wellbeing[5]. These needs manifest as a desire to become independent, and to show we are capable of such independence. Consciously and visibly doing things different to our parents is an easy – and common – way to demonstrate this independence. And whilst this behaviour usually starts in our teenage years, it frequently extends into adulthood.

In many cases, this means the basis for making many of adult decisions, such as what to buy, where to invest, or what financial adviser to use is often shaped more by a desire to be different to our parents than by the actual merit of those decisions.

For advisers, this means no matter how great a job you have done managing your clients’ money, in the eyes of their children you are ‘uncool’.

Younger investors want more control

Much has been written about the Robin Hood phenomenon and the massive growth in retail sharemarket investors since the start of the pandemic. Driving this growth is younger investors attracted to the plethora of DIY share trading platforms such as Stake, Raiz, and Superhero. Indeed, Australians using micro investing apps doubled – to 1.8 million – over the year to March 2022[6].

ATO data[7] suggests this desire for control even extends to superannuation, with the take up of SMSFs by younger investors so strong that around half of all SMSF trustees are now under age 45 (compared to just a third in 2012). And whilst Investment Trends research[8] suggests around three quarters of SMSFs are ‘unadvised’, this proportion is likely higher for younger investors.

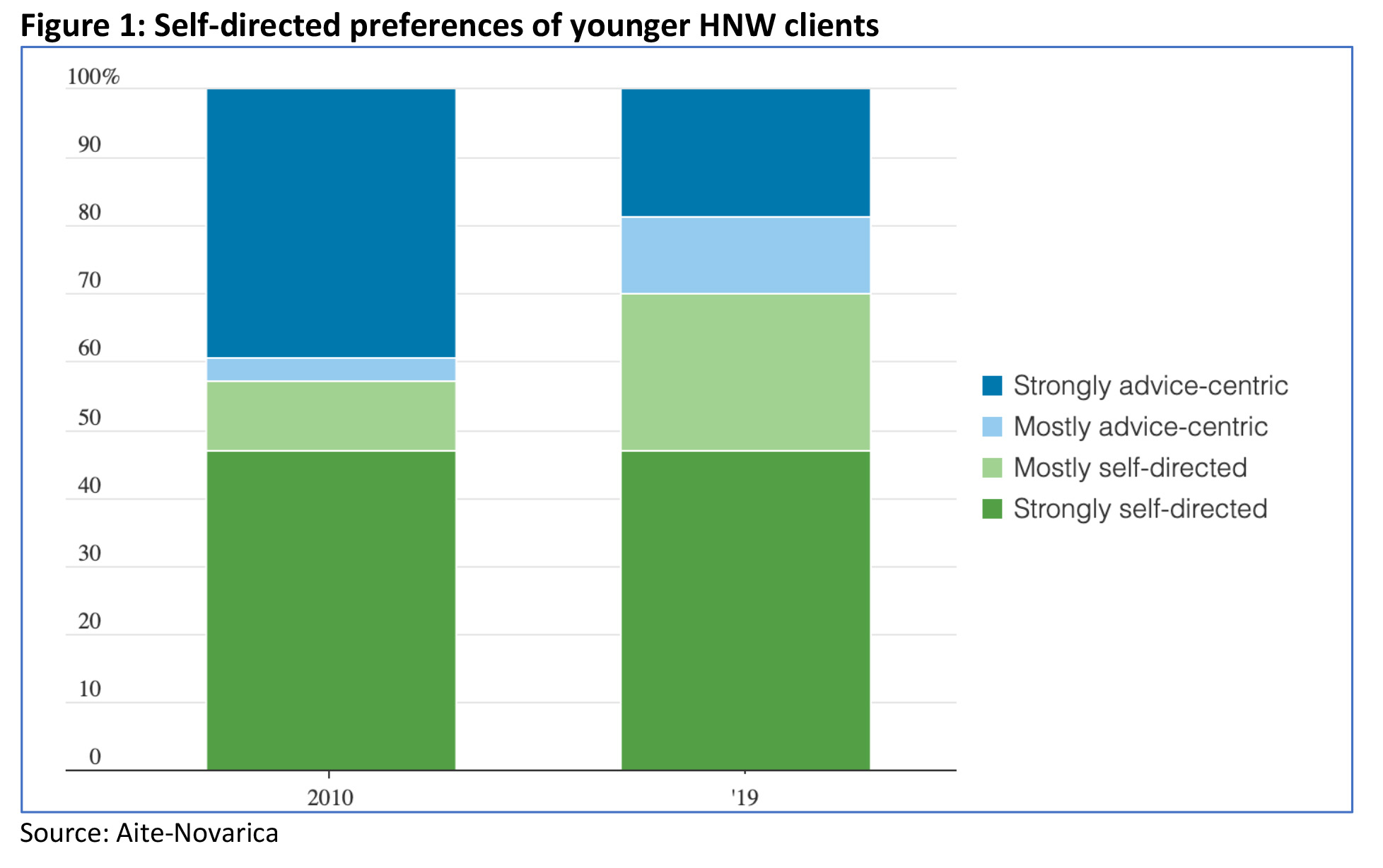

Importantly, the DIY approach is not limited to the less affluent younger investor. Research by US firm Aite-Novarica[9] found the proportion of households with a net worth of $500,000 USD or more, headed by a person under 45 years who identified as self-directed investors, grew from 57% in 2010, to 70% in 2019 (see Figure 1, below).

Failure to communicate

The third, and according to Investment News[10], biggest reason that so many inheritors decide not to use the services of their parent’s adviser – even though they don’t have their own adviser – is because their relationship with the adviser is weak or non-existent.

Sadly, it seems many advisers simply don’t prioritise building relationships with their client’s adult children. At best, this lack of priority sees advisers make communication and engagement efforts that are ill-suited to the needs of younger clients. At worst, it sees no communication or engagement at all.

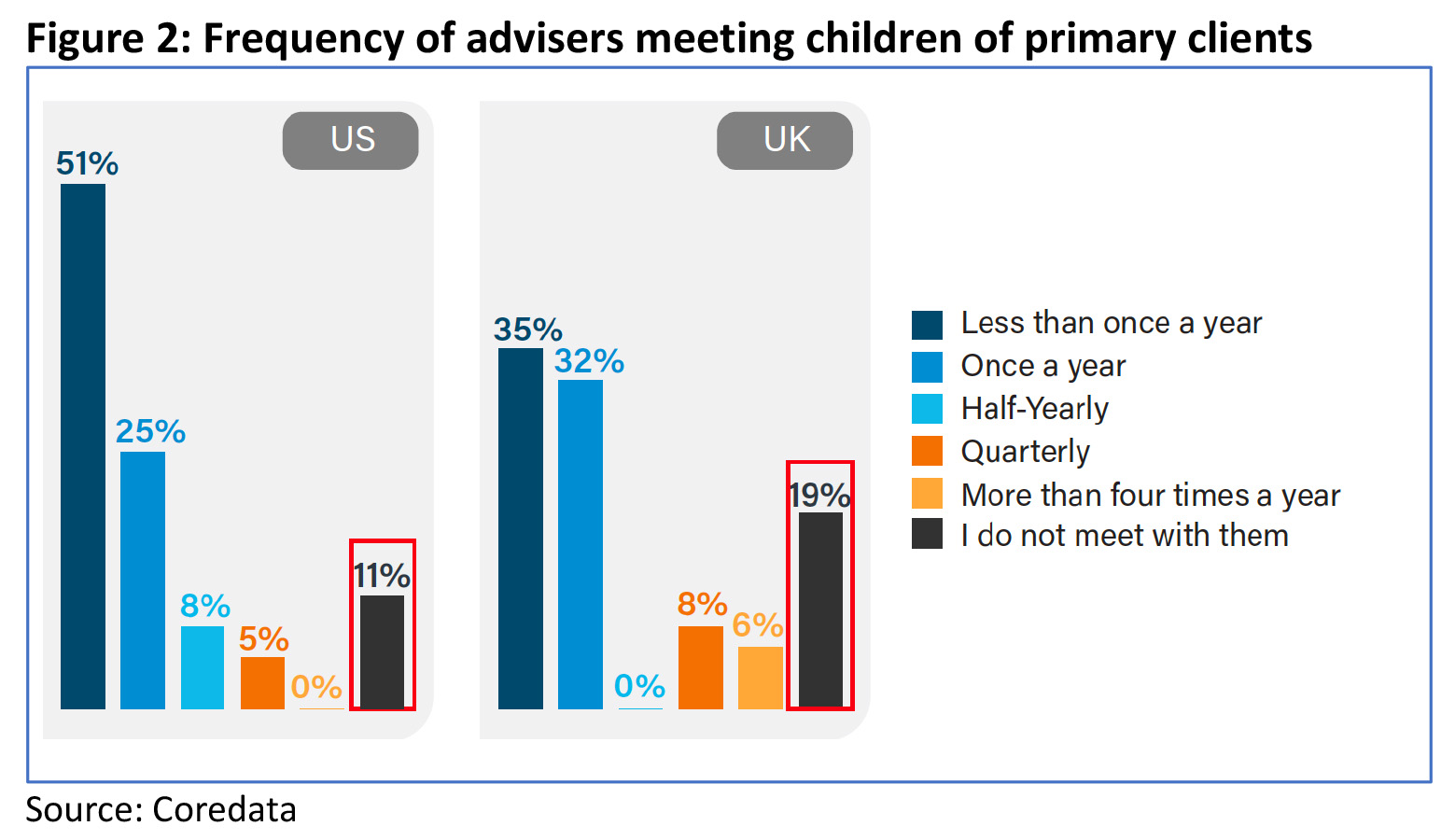

Coredata’s study[11] of UK and US advisers found that, despite the potential loss of significant assets under management upon the transfer of their clients’ wealth, few were making the effort to actively build relationships with their primary client’s children.

As can be seen in Figure 2 below, around 85% of advisers responding to the study said they met the children of their primary clients once a year or less. And in the UK, almost 1 in 5 advisers said they didn’t meet their clients’ children at all.

This absence of engagement increases risk on two fronts. Firstly, it makes it more likely that the heirs will change adviser (the chances of which are already high). Secondly, and worse, it increases the risk those heirs will go it alone and spend or lose most of that money within a few years, courtesy of poor discipline or poor decision making.

Ask yourself this: Would your current client want you to do all you could to ensure their heirs used their inheritance wisely?

A game of golf won’t cut it

Assuming your clients’ children will want to engage in the same way as your clients is a recipe for disaster, so forget inviting them to your annual golf day.

The key to building relationships with these clients of the future is appreciating the generational differences.

New generations of inheritors are likely to have different needs and expectations across three important dimensions:

- information and communication channels

- the way advice and services are delivered and accessed

- investment strategies and solutions.

Engaging with client families

There are numerous advantages in bringing adult children into estate planning conversations as early as possible. Chief among these are that potential issues can be identified and solved much earlier, minimising the likelihood of lengthy, wealth destroying disputes down the track. Just as importantly, this is an opportunity for you to start building and/or strengthening your relationship with those heirs.

So, what are the things to bear in mind when starting to engage on a more family wide level?

The whole technology thing

Confidence with and reliance on technology is generally inversely related to age, and both Millennials and Gen Xers are likely to be far more ‘tech savvy’ than their elders.

This typically manifests as heavy usage of apps and mobile tech to research and purchase products and conduct their financial affairs. Most categories are lifting their digital game these days, meaning the bar is set quite high, and client expectations of a seamless online/offline experience and easy-to-use interfaces extend to financial advice too.

Can a poor digital experience be a game changer for clients choosing an adviser? Absolutely.

For advisers, this means an absolute priority should be to assess their digital offering.

Fortunately, the prevalence of platforms – most of which allow a fair degree of white labelling – makes it easier for the back-end experience to measure up. The ability to access portfolio details, view performance data, and conduct transactions is pretty much a hygiene factor these days, and platforms enable even small advice firms to offer this to their clients.

Another digital offering of relevance – especially for younger clients – is cash management and budgeting software, such as My Prosperity, often available in both free and paid versions. (Some advisers make it mandatory for their clients to sign up for such services).

But the front end – the advice practice website – can’t be neglected either. Too many adviser websites still look they came out of the same studio in 2008, making for a jarring interface between website and platform and undermining any effort to build a contemporary brand.

Thanks to the growth of template-based web building offerings like Wix and Squarespace, refreshing a website needn’t be a complex or expensive exercise, even when you get a designer involved.

Think too about your Google experience, not just your search presence but your profile in Google maps. Nowadays, it’s pretty standard to use Google maps to check everything from office hours to parking, as well as basic navigation. You can edit your Google business profile easily and free of charge, and even enhance it with photos and information about your business. (Surprisingly few business owners do so).

The preference for a digital experience also extends to communication channels. The younger the client, the more likely they are to rely on social platforms, video and direct messaging to communicate and consume information. Podcasts are undergoing a renaissance and are a convenient way to communicate and consume more detailed information.

And a degree of personalisation – even a small signal that the information being sent is based on an understanding of that person’s interests and needs – is essential. Mass-produced, generic email newsletters are unlikely to cut it.

How contemporary is your client communication strategy?

A desire to be educated

The popularity of personal finance content on social platforms such as Instagram and TikTok (where #personalfinance has over 4.4 billion views and #stocktock has over 1.4 billion views) shows that younger investors are hungry for financial education. The challenge for advisers is to ensure that the style of communication (including language) and the delivery channel, is keeping up with the preferences of the audience.

Advisers who perhaps already have a financial literacy and education offering for their clients should consider making these resources available to younger clients. Additionally, consider one off, bespoke sessions where you can take them through some basic financial foundations, as well as topics related to inheritance. And if your clients’ heirs already have their own adviser and are reasonably financially savvy, offer to run a session where you explain your investment philosophy or give some sort of market update. Your effort could well be rewarded.

Modular advice

Younger clients may not want the full holistic planning experience that you have delivered to their parents or grandparents. Indeed, consumers more broadly prefer the idea of ad hoc modular advice on specific topics than all-encompassing advice (by a ratio of two to one, according to research[12]).

If your practice doesn’t currently offer modular/scaled advice – perhaps for economic or compliance reasons – consider doing so just for this specific group of clients. (Remember we are talking about building relationships before they inherit, so this is advice around their pre-inheritance circumstances).

The appeal of modular advice is that it is seen as more accessible and affordable, and so an hourly rate or flat fee is likely to be the most appropriate way to go here. (Some advisers, who play a very long game, may even provide such advice on pro-bono basis). When assessing the economic viability of this offering, make sure you take a family wide perspective – including your primary client – rather than just focusing on their inheritor(s).

They want to invest responsibly

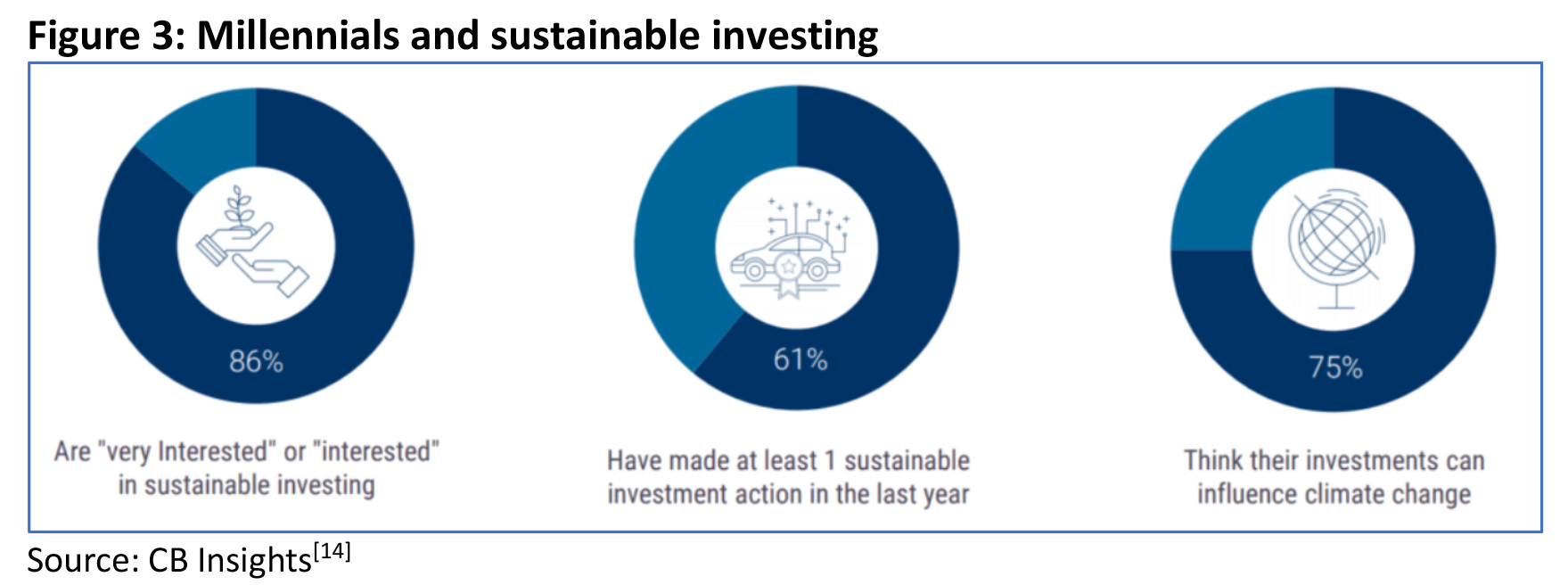

Another preference inversely related to age is that for responsible, or ESG investing. Research[13] found that investors aged 35 – 54 are almost twice as likely to expect an ESG overlay on their investments than those over 55. The need to invest for impact is particularly strong amongst Millennials, 86% of whom are interested or very interested in sustainable investing, and 75% of whom believe their investments can influence climate change (see Figure 3 below).

Of course, strengthening your ESG knowledge and offering makes sense, not just to help build credibility with your client’s heirs, but to help maintain your relevance more broadly, in line with overall increased investor demand for responsible investment options.

Team composition

It’s a truism that we often engage better with our own generation. If you have the opportunity to involve team members who are more aligned to the heirs in waiting, and you think this may improve the quality of the engagement, then consider bringing them into the conversations.

Consider a Family Money Mission Statement

Beyond formal estate planning instruments and the other documentation you would regularly share with your clients, another expert tip is to consider formulating a Money Mission Statement, or Family Constitution.

Work by US researchers Williams and Preisser[15] , emphasises the importance of having a family mission statement specific to wealth. In their work, they found that families with Mission Statements were more likely to retain control of assets within the family.

Ideally, the client and their direct heirs (and even younger generations) will be involved in its formulation, and it will include a long-term target, goal, and destination. Such a process can be an ideal opportunity for you to build relationships with, and demonstrate your expertise to, the heirs and the wider family.

Finally, this isn’t just about keeping wealth in your practice

Finally, it’s worth remembering that there is a more fundamental reason to engage your clients’ heirs – and that is to do the right thing by your client right now.

Another finding of the William and Preisser study referenced above16, was that 25% of wealth transition failures stemmed from poor preparation of heirs. In many of these instances, the issues were a direct extension of the prior poor communication and a lack of trust.

This is less about maintaining AUM once wealth has been transferred, and more about giving your current client the peace of mind that their financial legacy will not be frittered away by unprepared heirs.