Mind the gap – the impacts of inadequate retirement savings (part one)

Globally there’s a shortfall in retirement savings, creating a funding gap when it comes to retirement savings.

When it comes to saving for retirement, each of your clients has unique financial circumstances and individual aspirations for life after work. How can you best support them to make the most of Australia’s superannuation system and attain their retirement goals? This article is proudly sponsored by Russell Investments.

When compulsory superannuation, the Superannuation Guarantee (SG) system, was introduced in July 1992, the core objective was to “provide an adequate income to ensure all Australians achieve a comfortable standard of living in retirement, supplementing or substituting the Age Pension”.[1]

While that objective stands, the environment has changed. Since the SG was introduced, average Australian longevity has increased by a decade; this means the five million or so just-retired or soon- to-be retired baby boomers (and those who follow) need to fund a comfortable retirement for 20-30 years beyond their working life.

However, it’s not just Australians facing retirement funding challenges. Globally there’s a shortfall in retirement savings, creating a funding gap when it comes to retirement savings. The global ‘retirement gap’, measured in trillions of dollars by most estimates, has captured the attention of the world’s largest institutional investors for decades.

A little history

Independent analysis by the World Economic Forum (WEF), which spanned some of the largest established pension systems in the world, estimated a collective retirement income shortfall of US$70 trillion (A$107.10 trillion) as at 2015. This shortfall is set to rise dramatically to US$400 trillion (A$612 trillion) by 2050[2].

Historically, Defined Benefit (DB) plans were the most dominant form of retirement savings vehicles. After years of work, employees would be rewarded with a pre-agreed monthly income throughout retirement: the defined benefit. While the responsibility for managing the investments used to fund your retirement lay with the plan trustee, the responsibility for funding the liability lay entirely with the employer. They carried the investment risk and the responsibility to cover any shortfall.

The problems embedded in the DB system were brought to light by Greece’s woes following the global financial crisis (GFC). The pension system in Greece had been based on a generous public pension pillar, with voluntary occupational and private pension plans of minor importance or impact.

The amount of money held in its centralised pension funds dropped €25bn in the five years following the GFC, an issue compounded by demographics as pensioners comprise more than one-fifth of Greece’s population. At the same time, youth unemployment is high, which means a lower volume of contributions from the working population.[3]

Immediately following the GFC, monthly pensions dropped to an average of €833 from an average of €1,350 in 2009 and, during Greece’s decade-long financial crisis, it slashed pensions more than 10 times to meet its fiscal targets. In July 2022, the Greek government promised to increase the pension rate for the first time in a decade[4].

Shifting responsibility from institutions to individuals

As Defined Contribution (DC) plans have replaced DB globally, the responsibility has shifted away from well-resourced institutional investors (employers) to individuals. Unlike a DB plan with a set benefit, DC plans have a set contribution rate. Ensuring the contributions (and investment earnings) will adequately fund retirement is the responsibility of the individual.

If the asset allocation is inappropriate, or the contributions insufficient, the individual shoulders the risk and will need to live with the consequences.

The Australian retirement system is broadly considered among the best, ranking third behind the Netherlands and Denmark in a Mercer comparison of 37 retirement systems[5]. This ranking is a result of our mandated employer contributions, tax incentives to encourage voluntary contributions, and the safety net provided by the Age Pension, which sees Australians in a significantly better position relative to people in many other countries.

Despite this, 23.7 percent of retired Australians experience ‘pension poverty’, living with an income lower than 50 percent of median equivalised household disposable income. The OECD average is 13.1 percent.[6]

Not unrelated is WEF data that highlighted a US$1 trillion shortfall in Australia’s retirement savings, projecting Australians will outlive their retirement savings by a significant margin. Based on an average of 23 years in retirement, the WEF estimated Australians will only be able to maintain 70% of pre-retirement income for an average of 10 years. Once exhausted, they will need to rely on the age pension, an income that allows little spending beyond the necessities.[7]

The real retirement gap

Each of your clients will have their own unique perspective on an adequate level of retirement income, based on their circumstances and expectations. These diverse income requirements are not captured by standardised income levels. Therefore it’s challenging to determine the real retirement gap, the gap that matters most to each individual—how they are tracking relative to what they are trying to achieve.

Unfortunately, analysing how Australians are tracking towards their retirement income aspirations on a national basis is not possible—the data simply doesn’t exist. To shed some light on the issue, Russell Investments analysed data outlining the retirement goals and financial circumstances of 8,120 superannuants. This analysis enabled a projection on how each is tracking to their retirement income goal.[8]

The findings were significant (figure one). More than half (64%) of the participants were projected to fall short of their desired income by more than 10%. The analysis uncovered a second, poorly understood issue. The potential for overfunding—unintentionally saving more than needed. Over one in ten participants were projected to exceed their goal by more than 10%, sacrificing spending now to achieve a future retirement income well above what they want.

Closing the retirement gap

Where can change have the biggest impact?

Figure two highlights the two primary levers you have to directly influence retirement income: the level of contributions and the investment returns. These drivers will have the greatest impact on retirement adequacy.

There are three factors that have the greatest influence on retirement savings:

- How much money goes in

For example, $1,000 contributed per year, $46,000 over a working life, would provide roughly $3,720 in additional retirement income per year (when earning 7% p.a.)* - How long the money is invested

For example, contributing the same $46,000 as above, but starting at age 40 instead of age 21, provides only $1,520 in additional retirement income per year** - Investment earnings

For example, while an after-fee return of 7% delivers $3,720 per year in the above example, adjusting the return to 6% would only deliver $2,750 per year*

Assumptions

* Working life assumed to be 21 to 67. Disclosed assumed return is after fees and tax. $46,000 in total contributions paid in equal instalments of $1,000 p.a. throughout the working life at the end of each year. Accumulated lump sum amount at retirement age 67 was converted into a retirement income using the Moneysmart retirement calculator using standard Moneysmart assumptions. Retirement income results shown are discounted back to age 21 into ‘today’s dollars’ using a deflator of 3.2%p.a. ** As per disclaimer above, except the total payments of $46,000 are split into 27 equal instalments of $1,703.

Optimising contributions

Contributions—the savings put towards retirement—is the first of the two primary drivers of retirement income. There were $44.5 billion of contributions in the June 2022 quarter, an increase of 15.2 percent compared to the year to June 2021. Contributing factors include lower unemployment and an increase in the SG contribution rate. Personal contributions were $37.9 billion in the year to June 2022, up substantially compared to the year to June 2021. Household savings are at high levels by historical standards and part of this has flowed through to superannuation contributions[9].

Russell Investment’s analysis shows optimising contributions at the personal level can play a significant role in closing the real retirement gap. For example, helping your clients optimise contributions (contributing up to 5 percent of their salary in additional contributions when tracking behind would result in the proportion of members on track to their goal increasing by more than half).

Why optimise contributions at the individual level?

Compared to other countries, Australia is in an enviable position with substantial levels of existing savings. We have a mandated contribution rate of 10.5% of salary and there are significant tax incentives to motivate additional voluntary contributions.

Independent research shows a blanket increase to mandated superannuation contributions would be punitive, particularly to low-income earners. Simplistically, increasing the Superannuation Guarantee (SG) rate would mean Australians accumulate more superannuation over their working lives, increasing the likelihood of a comfortable retirement. However, the reality is much more nuanced.

Unlike a DB system, where any broad benefit will be shared by all members, Australia’s largely DC system places the risk of falling short on each individual. Increasing contributions broadly, thereby improving the average, can hide significant impacts at the individual level—impacts that won’t be shared across other participants.

The right level of contributions is not the same for everyone. It depends on the individual and their personal situation, and the retirement income they are trying to achieve.

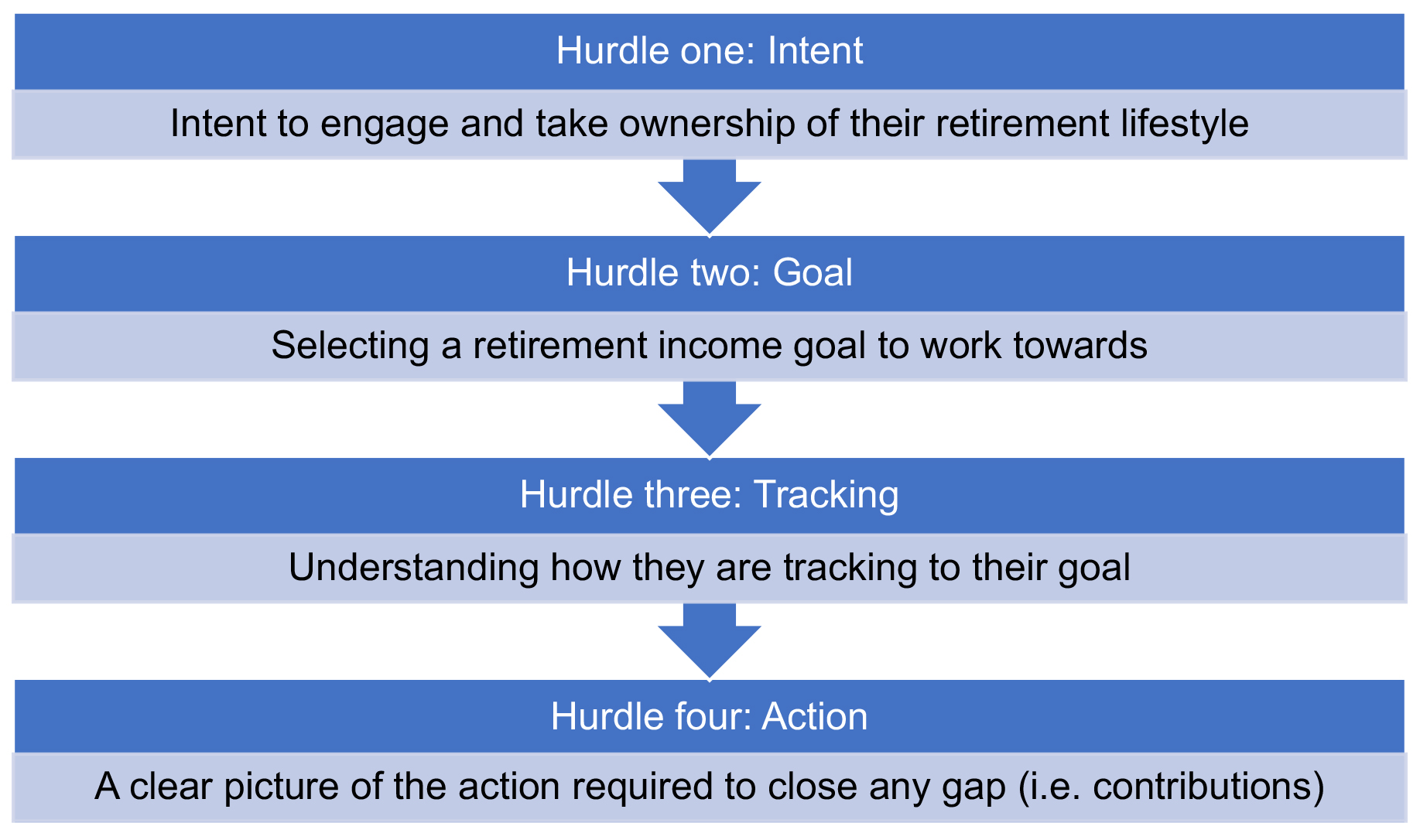

Russell Investment’s research identified four key hurdles individuals must overcome prior to being in an informed position, ready to make and maintain optimal contributions. This provides an opportunity for you to engage with existing and prospective clients to overcome these hurdles and position themselves for a retirement outcome that will meet each individual’s needs.

These hurdles are:

As well as overcoming these hurdles, there is the investment aspect to consider. There’s a significant body of research that suggests that asset allocation drives over 85 percent of the investment outcome for an individual, both inside and outside of super.

Without your guidance, investors risk selecting an inappropriate asset allocation for their retirement savings, one that won’t enable them to meet their investment objectives and needs. Investors may not set the right investment strategy for their circumstances and many lack the knowledge and/or time to research the many investment options available. With the renewed focus on super fund performance metrics, there’s the added temptation to chase performance and overreact to market events.

Financial advisers are best placed to help Australians understand their retirement goals, overcome these hurdles and best position themselves to achieve the retirement outcomes. Advisers have the potential to add significant value to an individual’s retirement savings over the long term, by helping clients overcome these hurdles and select an appropriate asset allocation to best meet the client’s objectives. Part two of this series will examine these themes in more detail.

——–