Andrew Yap

With Australia experiencing its highest inflation levels since the early 1990s, advisers face a common problem – how to maintain the purchasing power of client portfolios and deliver a level of return consistent with investment objectives.

Over the past year, the global inflation spike has weighed on market sentiment, contributing to a broad-based sell-off across many asset classes, with only a small number generating positive returns. In such an indiscriminate market, there’s been limited scope for our real return universe to deliver positive returns, with the median manager returning -3.86% for the 12 months ending 31 August 2022.

The market declines have been so widespread that even those markets perceived to be safe havens in rising inflation scenarios, such as gold and inflation-linked bonds, have struggled, with the latter impacted by the widening of nominal bond yields. For example, Australian inflation-linked bonds retraced by approximately -9.4% over the year, which means that despite their inflation protection qualities, returns looked very similar to other bond markets.

The real return category is a group of strategies that target CPI plus outcomes and therefore seek to deliver long-term returns that outpace inflation and deliver consistent capital growth. Targeting real outcomes is a ‘client friendly’ concept, however the recent environment has highlighted the challenge of building truly ‘inflation proof’ portfolios.

The breadth of asset classes with direct linkage to rising inflation is limited to a few markets, such as inflation-linked bonds, commodities and some equity sectors (eg. energies, precious metals, consumer staples). Therefore, building a portfolio that could outperform in a rising inflation environment is likely to be challenging, particularly where managers seek to retain portfolio diversification to enhance the capital preservation qualities of their portfolios.

The recent inflation spike has highlighted that managers in the real return sector rely on the indirect inflation hedging properties of traditional asset classes to deliver real long-term returns, as opposed to building portfolios with direct inflation linkage. While this isn’t surprising, it reinforces the importance of investing over the longer term, the role of real return managers in managing portfolio exposures in terms of allocating capital across different asset classes, and the inclusion of a broad set of strategies to generate attractive real returns.

Equities – the cornerstone of real return investing

Across our real return category, we’ve observed that the exposure to equity beta has been the largest contributor to total return. This observation is unsurprising and is also the case across more traditional strategic asset allocation (SAA) centric diversified strategies.

The sensitivity to movements in equity markets varies based on a manager’s view on relative value, exposure to lowly correlated asset classes, and the use of capital preservation strategies (eg. tail hedging, allocating to safe haven assets).

In theory, equities should provide an effective hedge against inflation as equity holders own a claim on the future earnings of a company, which should be able to pass on increased costs over the long run. For example, rising wage and input costs should be able to be passed onto the end consumer, assuming that the product isn’t perfectly substitutable or subject to high demand elasticity.

Further, several equity sectors tend to directly benefit from high inflation, such as energy companies, whose earnings are highly correlated to movements in oil and automotive fuel prices. Other sectors where demand is relatively inelastic and lowly correlated to the economic cycle, such as agriculture, consumer staples and precious metals, also tend to perform well.

However, the relationship between equity returns and inflation is unstable, reflecting the impact of other macroeconomic factors on equity valuations. In addition, the equity market tends to respond to changes in inflation expectations well in advance of ‘actual inflation’ being recognised in the official data (noting that such releases are lagged post quarter end).

In rising inflation environments, the relationship has been unstable and tended to weaken and revert to close to zero. As detailed earlier, changes in inflation expectations are likely to have a stronger effect on equity valuations, correlating more closely with changes in inflation expectations versus ‘actual’ higher inflation.

In terms of equity valuations, they tend to suffer when inflation expectations are rising, as investors price in the impact of higher discount rates on future expected corporate earnings and the premium required to hold equity risk increases, in a higher inflationary environment.

Equity risk: a long-term contributor to total return

Over the long term, the equities allocation in real return portfolios is expected to deliver positive real returns and provide a foundation upon which CPI plus objectives are achieved. An exposure to equities alone will not, however, be sufficient for managers to achieve these objectives. To illustrate this, the following chart plots the return of the Australian equity market over rolling five-year periods, with the blue line representing a CPI plus 5% p.a. objective, for the past 30 years.

As shown above, there have been few instances post GFC where Australian equities achieved CPI plus 5% over a rolling 5-year period. What can be concluded therefore, is that performance success is likely to be strongly aligned to a manager’s market timing skills and their preparedness to position their portfolios ahead of market inflection points. Arguably, this is an area where real return managers should outperform relative to their SAA-counterparts who have less flexibility to alter their portfolio mix in anticipation of changing market dynamics.

The role of fixed income

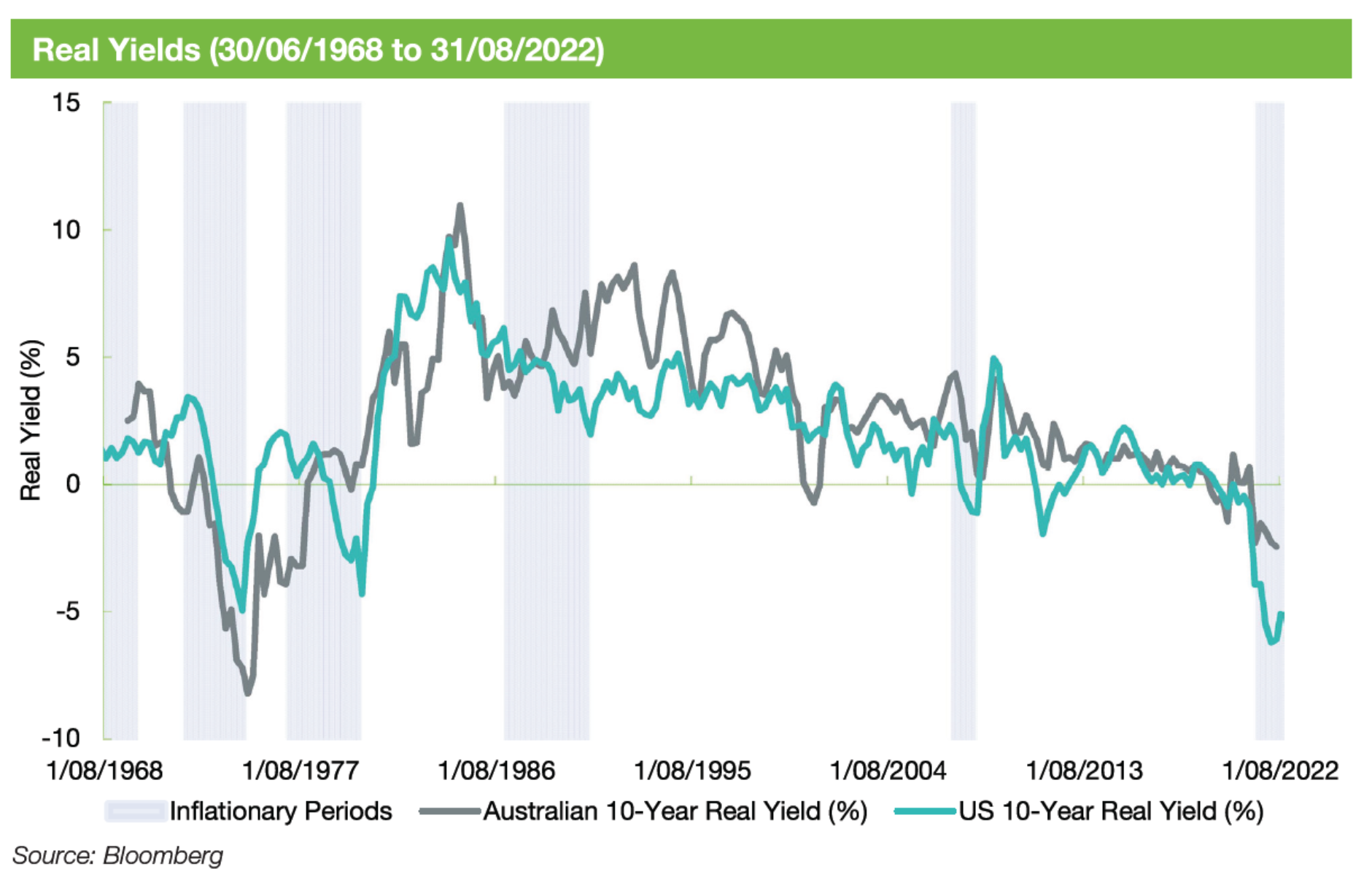

Fixed income remains a key allocation across the real return universe, both as a source of return and a diversifier of equity risk. Inflation is widely regarded as being harmful to fixed income, as it erodes the capital value of bonds and reduces the purchasing power of fixed coupon. Therefore, the inflation beta of fixed income is structurally negative, albeit the strength of the relationship changes over the investment cycle.

Nominal bonds are susceptible to rising inflation which is a challenge for real return managers seeking to deliver CPI plus outcomes. Over the long term, we’ve observed bonds deliver positive real returns, however, through periods of high inflation, real yields can be negative.

Real return managers have the flexibility to structure their fixed income portfolios to navigate periods of rising inflation and nominal bond yields. This can be achieved via a combination of active asset allocation (eg. reducing the allocation to fixed income) or through more stratified approaches such as running duration overlays, allocating to external managers who share similar views on the environment and/or preferring shorter dated or floating rate securities.

Generally, the real return universe has been proficient in managing fixed income exposures with a tendency over the past year to be short or underweight relative to longer-term positioning. The following chart illustrates the average fixed income allocation across the real return universe.

From the above chart, it’s evident that managers have been active in altering their fixed income exposures, most notably increasing their allocations as the yields on 10-year bonds rise. We view this move as considered, noting that a rise in portfolio yield introduces defensive qualities which can aid with capital preservation.

Cash Plus versus CPI Plus

We believe Cash Plus objectives to be more suitable for real return and diversified strategies, given cash is an investable concept and represents a starting point for allocating risk across portfolios. Furthermore, defining a return objective linked to an un-investable benchmark has the potential to create expectations that portfolio returns are linked to inflation changes.

Cash isn’t a perfect benchmark and can produce negative real returns in high inflation environments or stagflationary regimes where central banks prioritise full employment and economic growth over inflation. However, we view it as a superior benchmark against which manager performance can be observed, particularly in environments where inflationary pressures are either sustained or meaningful.

By Andrew Yap, Head of Australian Fixed Income and Multi-Asset Research