Reserve Bank Board meeting

- The Reserve Bank (RBA) Board has lifted the cash rate by 25 basis points (quarter of a percent), taking the cash rate to a 9½-year high of 2.85 per cent

The Big Picture

- The Reserve Bank Governor has indicated that the normal or neutral range for the cash rate is 2.5-3.5 per cent. The question now is where do we go from here? At some point the Reserve Bank needs to pause and assess the impact of the near decade-high cash rate on the broader economy – and inflation in particular. The aim is to push inflation back to the 2-3 per cent target band while keeping the economy ticking along and holding on to the hard-won gains of the lower unemployment rate. Over the last few days, there have been encouraging signs of a slowing of price pressures – from the monthly Melbourne Institute inflation gauge and the S&P Global manufacturing index. And the NAB’s September business survey also showed an easing in price pressures.

- The Reserve Bank has indicated a preference for ‘normal’ 25 basis point (bp) rate hikes. Not only can rates be lifted modestly, finessing the slowdown of the economy. But the announcement effect of rate hikes – or the threat of rate hikes – adds power to the rate move. Larger 50bp hikes from here are riskier – a sledge hammer rather than hammer – and likely to mean that the interest rate objective is achieved too quickly, resulting in a move to the sidelines for a number of months. As a result, the added power of announcement effects is lost.

- Also, in recent communications, RBA speakers have expressed some concerns about the deteriorating global economic outlook and reservations about the yet unknown impact of restrictive policy on consumer spending. In fact, there is typically a 3-month lag between when the official cash rate is hiked and when household mortgage repayments materially increase. The full effect of this transmission to household budgets won’t be known for a few more months. Also, the RBA meets 11 times per year, unlike other central banks, affording it more time to incrementally lift rates by smaller amounts.

- Commonwealth Bank (CBA) Group economists expect the Reserve Bank to lift the cash rate another 25 basis points at the December Board meeting to 3.10 per cent. This gives the RBA time over the Christmas/New Year period to assess the impact of Australia’s most aggressive rate hiking cycle.

Perspectives on interest rates

- The RBA lifted the cash rate by 25 basis points (bp) or a quarter of a per cent to 2.85 per cent – a 9½-year high. This follows a 25bp increase in October, 50bp rate increases in June, July, August and September and a 25bp increase on May 3, 2022. The RBA last cut the cash rate from 0.25 per cent to 0.10 per cent on November 3, 2020. Before the Covid-19 health and economic crisis, the official cash rate was 0.75 per cent on February 5, 2020.

The Equity Lens: What does it mean for borrowers, depositors and investors?

- Consumer spending is slowing and will slow further once a key cohort of fixed rate borrowers move their loans to those with markedly higher interest rates. Investors need to reflect on sales and earnings announcements from retailers and other consumer-focussed businesses – they could prove even more illuminating than the constant stream of economic indicators.

- The Reserve Bank Governor has identified consumer spending as the indicator to be closely watched over coming months. The hard part is to gauge price and quantity components when there is discussion if consumer spending.

- The sharemarket has already priced in a slower expansion path for Australian and global economies. Once the upward path of inflation is halted, and central banks pause rate hikes, then investors will focus on the recovery path. This transition may be already underway. But there are always setback risks, so investors must be ready to pivot. Investors should expect an even greater focus on earnings and profit margins as economic activity slows.

- Returns on residential property are now easing whereas the slowdown in annual decline in returns on shares is nearing a trough. Annual returns on residential property is 1.8 per cent while the annual decline on sharemarket returns is 3.5 per cent. So investors have choices to be made.

The Statement

- Below is the statement from today’s November 1, 2022 meeting (emphasis added by CommSec):

—————

|

Media Release No: 2022-36Date: 1 November 2022 Statement by Philip Lowe, Governor:Monetary Policy Decision At its meeting today, the Board decided to increase the cash rate target by 25 basis points to 2.85 per cent. It also increased the interest rate on Exchange Settlement balances by 25 basis points to 2.75 per cent. As is the case in most countries, inflation in Australia is too high. Over the year to September, the CPI inflation rate was 7.3 per cent, the highest it has been in more than three decades. Global factors explain much of this high inflation, but strong domestic demand relative to the ability of the economy to meet that demand is also playing a role. Returning inflation to target requires a more sustainable balance between demand and supply. A further increase in inflation is expected over the months ahead, with inflation now forecast to peak at around 8 per cent later this year. Inflation is then expected to decline next year due to the ongoing resolution of global supply-side problems, recent declines in some commodity prices and slower growth in demand. Medium-term inflation expectations remain well anchored, and it is important that this remains the case. The Bank’s central forecast is for CPI inflation to be around 4¾ per cent over 2023 and a little above 3 per cent over 2024. The Australian economy is continuing to grow solidly and national income is being boosted by a record level of the terms of trade. Economic growth is expected to moderate over the year ahead as the global economy slows, the bounce-back in spending on services runs its course, and growth in household consumption slows due to tighter financial conditions. The Bank’s central forecast for GDP growth has been revised down a little, with growth of around 3 per cent expected this year and 1½ per cent in 2023 and 2024. The labour market remains very tight, with many firms having difficulty hiring workers. The unemployment rate was steady at 3.5 per cent in September, around the lowest rate in almost 50 years. Job vacancies and job ads are both at very high levels, although employment growth has slowed over recent months as spare capacity in the labour market has been absorbed. The central forecast is for the unemployment rate to remain around its current level over the months ahead, but to increase gradually to a little above 4 per cent in 2024 as economic growth slows. Wages growth is continuing to pick up from the low rates of recent years, although it remains lower than in many other advanced economies. A further pick-up is expected due to the tight labour market and higher inflation. Given the importance of avoiding a prices-wages spiral, the Board will continue to pay close attention to both the evolution of labour costs and the price-setting behaviour of firms in the period ahead. Price stability is a prerequisite for a strong economy and a sustained period of full employment. Given this, the Board’s priority is to return inflation to the 2–3 per cent range over time. It is seeking to do this while keeping the economy on an even keel. The path to achieving this balance remains a narrow one and it is clouded in uncertainty. One source of uncertainty is the outlook for the global economy, which has deteriorated over recent months. Another is how household spending in Australia responds to the tighter financial conditions. The Board recognises that monetary policy operates with a lag and that the full effect of the increase in interest rates is yet to be felt in mortgage payments. Higher interest rates and higher inflation are putting pressure on the budgets of many households. Consumer confidence has also fallen and housing prices have been declining following the earlier large increases. Working in the other direction, people are finding jobs, gaining more hours of work and receiving higher wages. Many households have also built up large financial buffers and the saving rate remains higher than it was before the pandemic. The Board has increased interest rates materially since May. This has been necessary to establish a more sustainable balance of demand and supply in the Australian economy to help return inflation to target. The Board expects to increase interest rates further over the period ahead. It is closely monitoring the global economy, household spending and wage and price-setting behaviour. The size and timing of future interest rate increases will continue to be determined by the incoming data and the Board’s assessment of the outlook for inflation and the labour market. The Board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that. |

———-

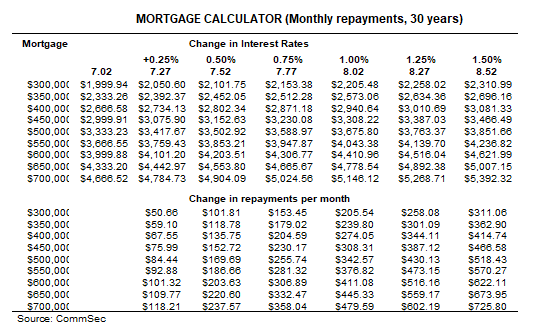

Implications for borrowers

- The following table shows current monthly repayments on a range of mortgages and projections if rates are increased by major lenders in response to the higher cash rate. The Banks Standard Variable owner-occupier rate is currently 7.02 per cent. And the Banks Discounted Variable owner-occupier rate is currently 5.95 per cent