The value of a Financial Adviser – Part 2

Advisers know that good financial advice can benefit clients.

The value of financial advisers – and the advice they dispense – can be challenging to quantify but for the majority of clients, is highly valued. This is particularly so during disruptive periods, such as that we now face: geopolitical uncertainty, volatile financial markets, spiralling inflation. This is a time when financial advice is more important than ever. This article, proudly sponsored by Russell Investments, examines the value of financial advisers.

Financial advisers provide valuable assistance to clients, helping them to review their evolving goals, needs and circumstances. This value is heightened during periods of change and upheaval. Such holistic wealth management requires a deep discovery process, planning and ongoing coordination, all of which can be more difficult when emotions run high and uncertainty prevails.

Those advisers who helped their clients remain invested through the turbulence of the pandemic, who helped them prepare for an uncertain future, who worked with them to determine their post pandemic goals, can look back with a real sense of having provided true value.

To help you articulate that value, a recent paper[1] detailed the five factors that measure and provide true adviser value to clients in a recent paper. These factors are:

- asset allocation

- behavioural coaching

- helping clients through choices and trade offs

- expertise

- tax savvy planning and investment.

Part one of this series examined the importance of asset allocation and behavioural coaching as key inputs into the measurement of adviser value. Asset allocation can have a huge impact on whether a client achieves their investment goals, driving over 85%[2] of the investment outcome for an individual.

Behavioural coaching helps to keep your clients on track, to avoid falling prey to the common investor emotions during market downturns. That can stop them from abandoning their investment plan due to fear because, as you well know, pulling out of the market when it is volatile can lock in losses and lead to missing out on any subsequent rally.

In part two of this series, the remaining three factors will be unpacked: helping clients through choices and trade-offs, demonstrating your expertise and tax savvy planning and investment.

C is for choices and trade-offs

Advisers provide a holistic wealth management approach throughout a client’s financial life. While the adviser’s role in each client’s journey will start at different milestones of that journey, the value an adviser can add from the beginning of the relationship is crucial. As you will have experienced, most people’s lives invariably become more complex over time. To help achieve an individual’s goals, an adviser will incorporate many inputs into the design of a personalised strategy.

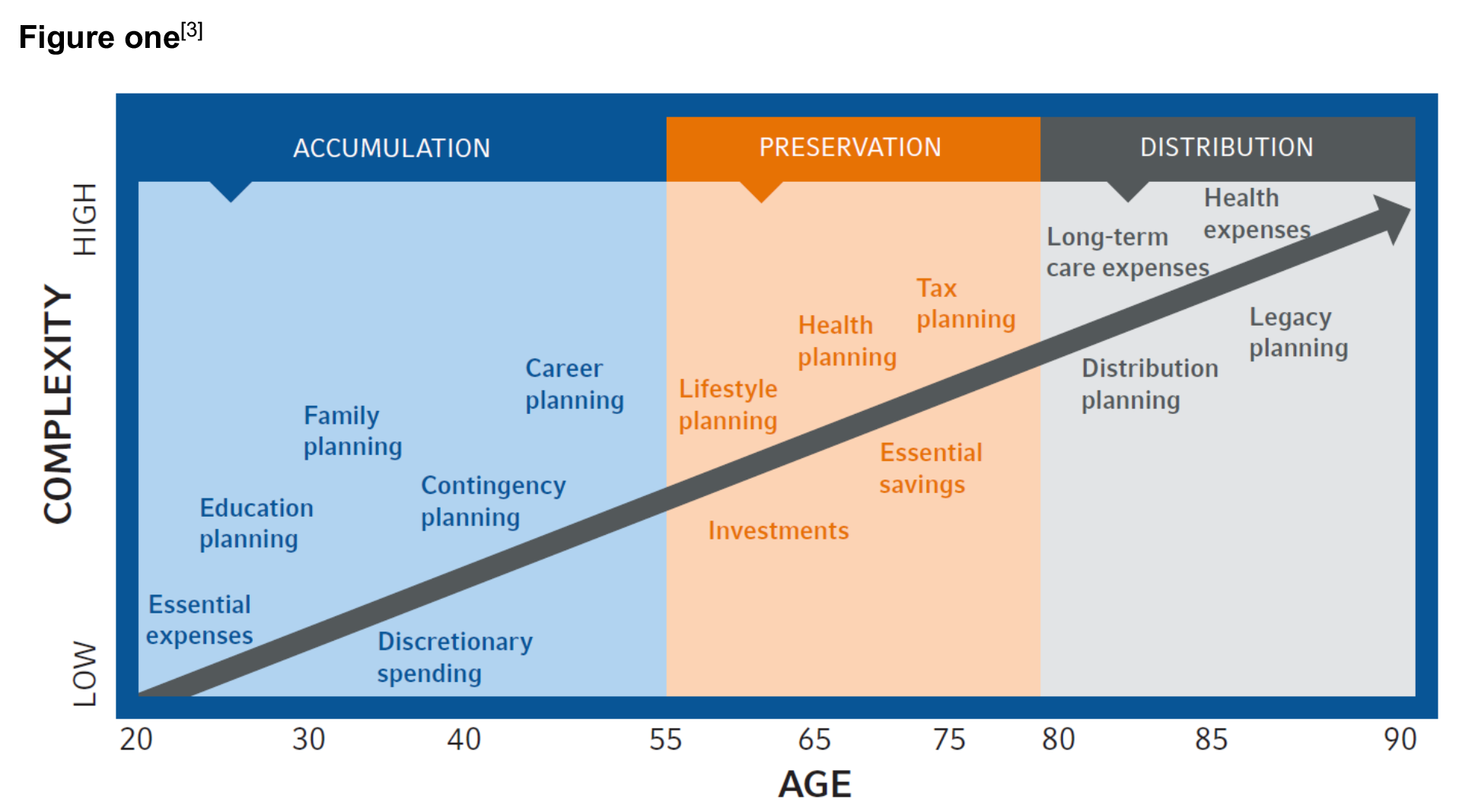

Every client has a unique set of circumstances, preferences and considerations, which increase in volume as they age, and in complexity as their needs and experience develop over that time (figure one). The sheer number of decisions to be made and the knowledge required to understand their implications can lead to decision fatigue and increases the risk of poor outcomes.

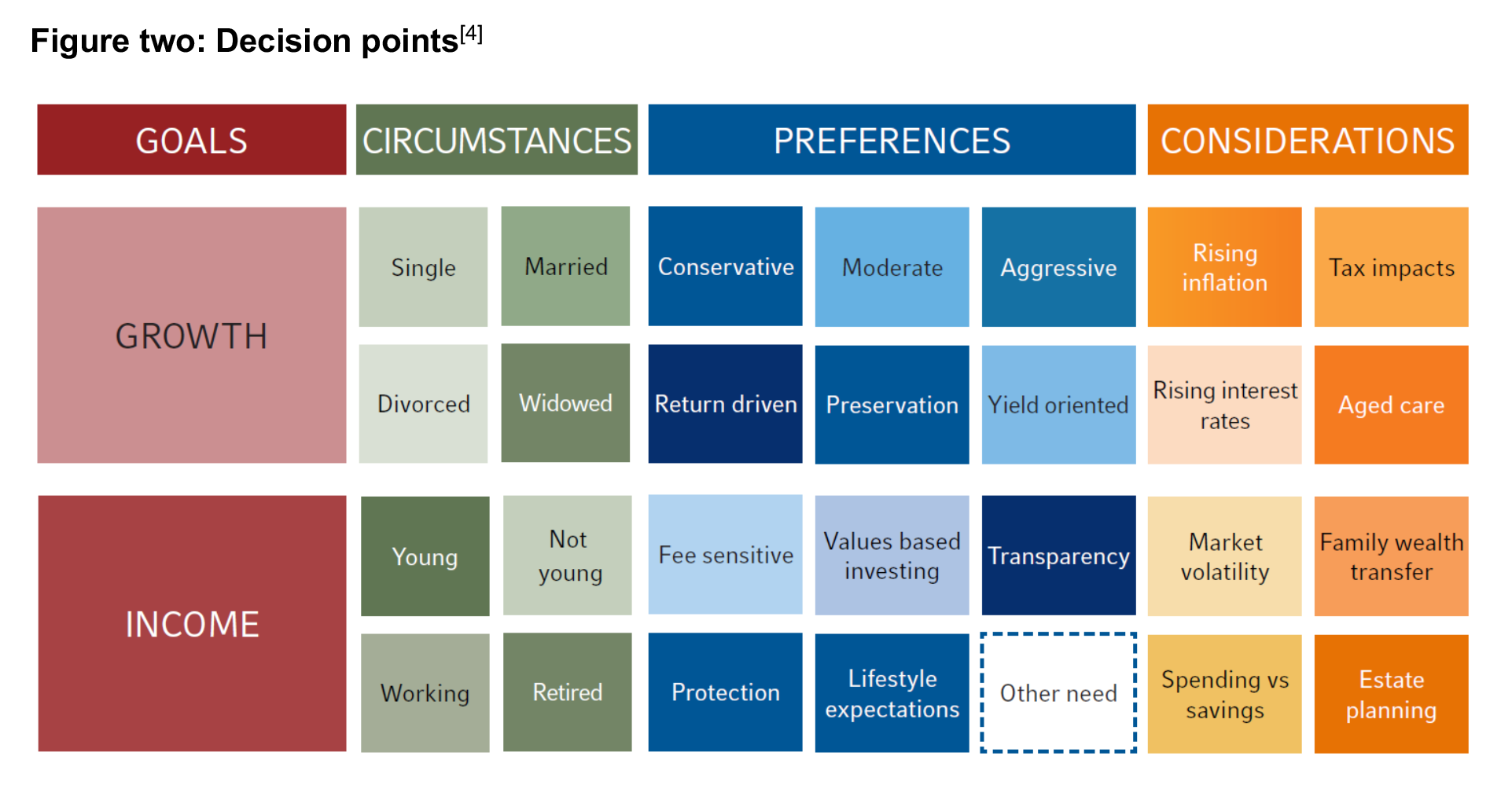

An adviser can help evaluate and prioritise these decision points (figure two). The impact of implementing the right strategy to meet an individual’s unique set of needs, while maximising the outcomes of these choices and trade-offs can be invaluable.

Circumstances

In the accumulation phase, individuals may be planning for key events like establishing their careers, buying a home, paying for a wedding, or starting and raising a family with all of the expenses that entails. When they enter the preservation stage before retirement, different needs take priority, such as caring for elderly parents or managing their own health. Finally, in the distribution phase when they are no longer working, they may need to consider long-term care or creating a legacy.

Preferences

Individuals will also have personal preferences that need to be integrated into advice considerations. These may include a preference to reduce or increase investment risk, or how their portfolio is constructed. Advisers can help provide options in circumstances where clients are price conscious, prefer investments aligned to their sustainability or ethical values, or want to see detailed information about where their money is invested.

The critical value an adviser can provide is helping a client understand the impacts of these trade-offs, and to avoid any unintended consequences. For example, helping a price conscious investor to understand that a passive portfolio is unlikely to significantly outperform the market, or that a sustainable portfolio will likely perform differently to a broad market index due to the nature of the respective investment strategies.

Sometimes these preferences can be in conflict, and an adviser can help a client to prioritise these preferences and ensure they are aligned to the client’s overall goals and will help them to achieve their financial objectives.

Considerations

In addition to personal circumstances and preferences, advisers can also help their clients evaluate and navigate external factors. The current environment is shaping up to be a ‘once in a generation’ event, with a mix of external impacts such as rising inflation and interest rates, ongoing market volatility and the Ukraine conflict.

Household savings are at record high levels[5], which can be a benefit to some individuals’ strategy or could leave others exposed to poor behaviours with longer-term consequences.

The anticipated significant increase in intergenerational wealth transfer[6] means an inheritance event is an additional advice consideration for a growing number of clients and prospective clients. The adviser’s role here is to help manage personal wealth to potentially reduce tax impacts or take advantage of benefits and incentives available.

Depending on an individual’s personal circumstances, preferences and considerations, there are a broad mix of these complex factors that require expert knowledge and advice to evaluate the choice and trade-offs at play, and what is right for each client’s specific goals and needs.

Actions advisers can take

- Can you articulate your Unique Value Proposition and the services you provide?

- Do you provide clients with a roadmap detailing how you will work with them to address their specific needs and objectives?

E is for Expertise

In the best of times, advisers help clients achieve life-long goals, and celebrate personal and family milestones along the way. In challenging times, advisers can add value through cases of trauma, illness, financial crises, estate planning and death.

This unique combination of technical skill and emotional expertise that is regularly demonstrated by advisers provides a priceless form of value to their clients.

Technical expertise

Managing wealth in the Australian financial system is complex at the best of times. Navigating the requirements of superannuation, taxation, insurance and legal requirements can be extremely challenging for most individuals. When you also consider the issues of limited financial literacy and low engagement with finances, the result is not a recipe for success.

The flip side is that advisers develop investment expertise – understanding financial markets and portfolio construction is key to their training and experience. Advice teams are consistently researching investment solutions, decoding technical terminology to determine what is appropriate for different clients.

As your clients progress through life their personal wealth management are likely to increase in complexity. It’s not only about how much wealth they have to manage, there are other considerations – navigating business ownership, dependencies, health concerns and estate planning all require additional expertise.

The value of working with an experienced adviser is about tapping into the accumulated expertise they’ve developed over their career. Together with ongoing education, this invaluable knowledge leverages previous client problem solving insights, and learnings from peer and industry connections.

Emotional expertise

With almost 50 percent of Australians experiencing financial stress at some point in their lives[7], the value of advisers doesn’t stop at the technical.

Providing emotional support is a critical part of the value of an adviser. Technical skills only get part of the job done – the ability to engage with and gain the trust of a client is critical to a successful relationship and achieving the best outcomes. This is where advisers draw on their essential interpersonal skills – empathy, caring and genuine curiosity.

An adviser’s role

Through the best and worst times of a client’s life, as their needs grow and change, an adviser can act in many different roles:

Guide

Be a trusted adviser to help manage the emotional burden of making decisions and considering the impacts. For clients who choose to be in control, advisers can act as a coach and sounding board, providing guidance and support to the client and their broader family.

Guru

In other circumstances, an adviser can provide perspective – acting as both an expert and a voice of reason, helping with education, understanding and even wisdom.

Gladiator

If needed, an adviser can be an advocate on a client’s behalf. Challenging an insurance claim, chasing beneficiary payments, managing the financial administration – your help with these responsibilities can allow a client and their family to focus on what is important to them.

While articulating such intangible value is challenging, an overwhelming majority of those that have experienced the technical skills and emotional support of an adviser see value in their relationship.

Actions advisers can take

- Take a sharper look at communicating the value of your advice.

- Have a clear value proposition, advice philosophy and service model that helps illustrate your offering.

- Use existing client case studies that highlight how elements of your expertise helped clients and the outcome you delivered. Share these with new clients to understand the intangible value you deliver.

- Understand the different motivations for seeking advice and have examples to use with new clients on how you deliver sometimes intangible yet appreciated value.

T is for tax savvy investing and planning

Tax is often considered the realm of the accounting profession. However, an adviser can also provide expertise in managing and optimising investment tax for their clients. The concept of investment tax isn’t just limited to what goes into a tax return. Investment tax can have an impact on an asset’s value or on portfolio returns, even though it may not always be seen.

Stand out from the crowd

Providing a more tax-effective approach to investing is an area where advisers can distinguish themselves and demonstrate some of the more specific advice strategies that can deliver real gains to clients.

Most investors are familiar with the concept of superannuation and its tax benefits. However, the technical expertise required to minimise a client’s tax position through super is often daunting and confusing. Not to mention the fear of getting it wrong and being answerable to the Australian Taxation Office!

Maximising available incentives

Increasingly, advisers are also playing a role in assisting clients to maximise their tax incentives and benefits at different life-stages. From childcare rebates and family tax benefits through to navigating superannuation top ups, health care cards, concessions and Age Pension entitlements.

Business owners have additional opportunities to be considered for grants and incentive programs. Many of these considerations are imbedded into the comprehensive advice provided – and should be recognised for the value added to the client.

Implementing solutions

As part of the implementation, advisers can provide guidance on choosing appropriate tax effective solutions and strategies that can deliver meaningful value to clients. For example, advisers can add value by:

- considering investment solutions that actively implement strategies such as lower turnover styles, tax-minimisation overlays and centralised portfolio management

- tax advice through superannuation contribution strategies (salary sacrifice and transition to retirement) and reinvesting tax savings

- insurance premium – identifying tax deduction benefits in super and reinvesting these tax savings

- optimising tax for non-superannuation assets and managing ‘tax surprises’ as regulatory changes occur (e.g. recent superannuation legislative changes).

Advisers have an opportunity to remind clients and reinforce this often embedded and overlooked component of advice. It is important for advisers to highlight the direct and indirect tax implications of their recommendations. Tax is a key consideration for many investors. Therefore, advisers need to be proactive and remind clients of intentional tax strategies, asset allocation and tax benefits intrinsic to their advice.

Actions advisers can take

- Know each client’s marginal tax rate, tax sensitivities and opportunities.

- Provide access to solutions that have tax-savvy strategies for your clients.

- Explain the different tax-smart decisions you include in your advice and ongoing implementation.

The uncertainties that surround the Covid-19 pandemic, now in its fourth wave across Australia, coupled with the new geopolitical environment presents an ideal time for you to reassess the value you deliver to your clients and how to best communicate it.

Many advisers worked with their clients over the course of the pandemic to have them stick to their investing path. By helping clients avoid the behavioural mistakes that many investors made in the market turbulence, you’ve likely already provided value above and beyond your fee. Add to that your other services – appropriate asset allocation, customised client experience and expertise you give them, and the savings from a tax-effective approach – it seems clear that the total value advisers deliver is significant. Focus on the value you provide, and your clients will more readily recognise and appreciate it.

———-