The most significant retirement risk of them all

Sequencing risk can interact with, and exacerbate, a range of other risk factors to challenge retirement plans.

It’s estimated that 670,000 Australians intend to retire between now and 2028[1]. As this cohort approaches retirement, they’re in the ‘retirement risk zone’ where volatile markets can make or break their retirement plans. In this article, proudly sponsored by Allianz Retire+, sequencing risk and its impact on other risk factors is put under the microscope.

It’s not new news that Australians are living longer, healthier lives and enjoy a more active lifestyle than their parents and grandparents. For those who retired during a bull market, retirement can be a succession of halcyon days enjoying all that life has to offer. However, for those who experience volatile markets in the lead up to and early days of retirement, it can be quite a different story, one beset by anxiety and fear.

Defining sequencing risk

In retirement, market volatility can have a major impact on how long your clients’ savings last and how long they can live a comfortable lifestyle. At its simplest, sequencing risk can be described as the risk that the order and timing of your client’s investment returns are unfavourable, resulting in less money for their retirement.

Unfortunately, retirees have no control over the sequence of returns. Ideally, Australians would only retire during periods of reduced volatility when their investment outcomes can be planned for with a greater deal of certainty!

The order, or sequence, in which investment returns occur becomes crucial in the lead up to retirement. If a portfolio sustains significant losses early on, it can have a lasting and detrimental impact on the overall wealth and sustainability of the portfolio.

In fact, the market conditions that prevail in the seven years just before and after a client retires can make an enormous difference to how long their funds last. Those crucial years are often called ‘the retirement risk zone’ (see figure one); a period when retirees are most vulnerable to market volatility. This is when clients’ savings are at their highest, but also when they are most vulnerable to market shocks and volatility.

If a client is fortunate enough to retire in a period of upbeat markets, then their income drawdowns will be fully or partially offset by investment returns. However, if the ‘retirement risk zone’ coincides with a period of negative returns, retirees may start eating into their savings at an accelerated rate, potentially emptying the nest egg.

Market shocks during the most vulnerable period will leave retirees with less time to recover, while falling asset prices and drawdowns for income or capital can magnify the scale of capital losses. Ultimately, any losses will diminish the total value of the remaining assets.

Market shocks and sequencing risk

A large decrease in the value of a client’s portfolio can arise from a market shock. The timing of this shock in an investor’s lifecycle can have a significant impact on retirement and affect the longevity of investor’s capital.

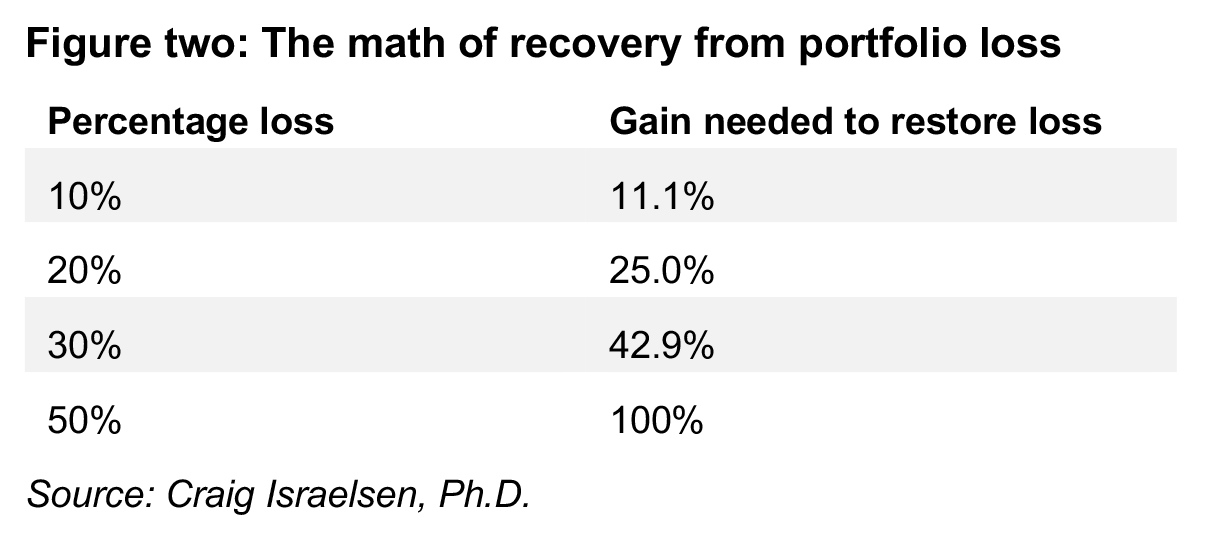

Market risk is exacerbated when multiple asset classes experience significant loss. A significant capital loss requires a significant gain to get back to the same point. As illustrated in figure two, there is a nonlinear relationship between gains and losses; as the loss grows, the gain required to restore the loss escalates.

Clients in the accumulation phase generally have the advantage of time to recover losses, as well as the opportunity to invest more during market downturns, taking advantage of lower priced assets and benefit from dollar cost averaging. Unfortunately, a retiree in decumulation phase does not generally have this opportunity and, when this happens in early retirement, the effect can be disastrous.

The timing and size of a market correction can have substantial consequences to retirement savings. As illustrated in figure three, the prevailing market conditions at the time of, and after, retirement can determine how long a retiree’s capital could last when investing in a balanced portfolio. It was chance that dealt 1982’s retirees buoyant markets, and chance that presented 1929’s retirees with a crash and rapid capital depletion.

The impact of sequencing risk on the other retirement risks

There are a range of risks that impact retirement…after all, no one knows how long they’ll live for, how the cost of living might impact lifestyle choices or the funding requirements they may have in the future. Typically as retirees age, a greater focus (and proportion of expenditure) is given to meeting health care and aged care needs which are, in most cases, unpredictable.

In the event of market volatility during the retirement risk zone, the impact of these risk factors is exacerbated and likely to have a much greater impact on the client’s retirement than if they retired during a period of market buoyancy.

Longevity risk

Australians dying with sizeable super balances is often spruiked by the media as resulting from a bequest motive, to transfer that remaining wealth to the next generation. However, an AFSA study[2] found that the majority of people exhaust all of their superannuation well before their death, with a small proportion passing on some superannuation to their spouse and a smaller proportion again bequeathing it to children or grandchildren.

Given the uncertainty of life and death, it’s impossible to work out precisely how much retirees can afford to draw down each year. Instead, many retirees face a decision: should they live more frugally, or risk running out of money?

The additional uncertainty around future investment returns throws a further complication into the mix. Australians cannot simply plan their retirement based on contemporary market movements as they need to account for unknowable changes in returns.

A survey of pre-retirement age Australians in 2022[3] found 47 percent expected to outlive their super and most respondents expected they would not reach their desired retirement income level. Consequently, many retirees ‘self-insure’ against longevity risk by living more frugally than they’d likely anticipated, in an attempt to preserve their super or other savings for as long as possible.

Sequencing risk heightens longevity risk; a poor sequence of returns during the ‘retirement risk zone’ is more likely to result in faster consumption of retirement savings, particularly in situations where capital protection strategies are not employed prior to entering that risk zone.

Inflation risk

Inflation risk has been top of mind for all Australians as the cost of living continues to spiral. A basket of goods and services that cost $100 in financial year 2017/18 would now cost $117.01, an increase of 17 percent over five years[5]. Many other services, such as health care, have increased well past the rate of inflation. A recent study by National Seniors Australia[6] suggests 68 percent of older people have recently gone without or hesitated to access essential healthcare because of cost.

Higher inflation can reduce retirees’ purchasing power and introduces the risk that spending needs in the future will be higher than originally planned. This, in turn, may exacerbate the fear of running out of money and increase loss aversion.

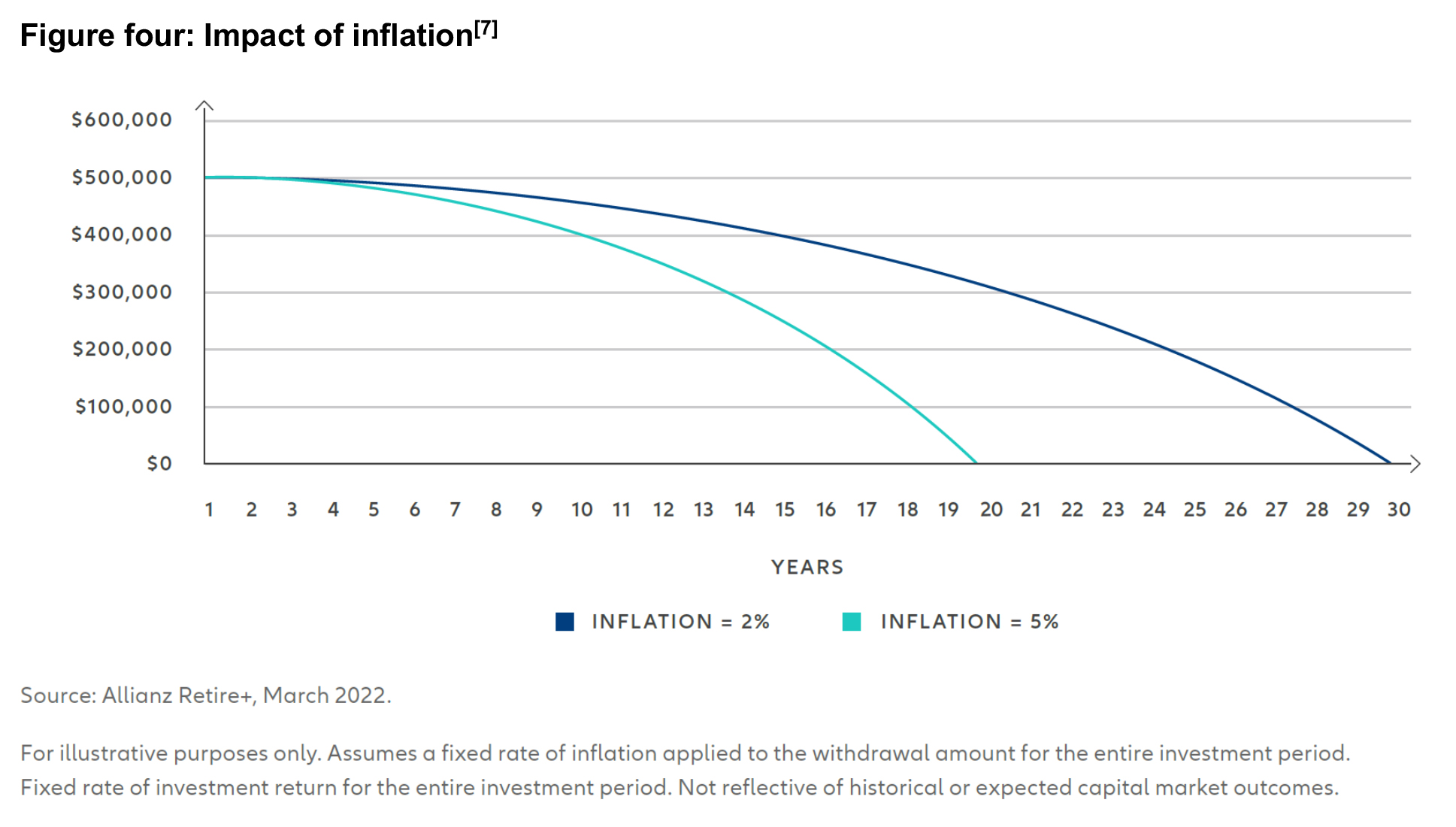

The compounding impact of inflation over time can erode retirement savings. Figure four draws on an example of a retiree with $500,000. An annual inflation rate of five percent would result in their savings running out 10 years sooner than if inflation remained at two percent. Inflation combined with sequencing risk is a double-edged sword, as the two forces combine to hasten the erosion of retirement savings.

Behavioural risk – or ‘loss aversion’

As retirement savings are eroded by market forces, it’s not uncommon for clients to experience loss aversion.

Loss aversion is a psychological phenomenon that refers to the tendency of individuals to feel the pain of losses more intensely than any pleasure derived from equivalent gains. For retirees reliant on their accumulated savings and investments to fund their post-employment years, market fluctuations can trigger heightened anxiety and emotional distress.

The fear of losing a significant portion of their nest egg during periods of market turbulence can lead retirees to make hasty and potentially detrimental financial decisions, such as selling investments at a loss or shifting to overly conservative portfolios. This aversion to losses may result in missed opportunities for market recovery and can have lasting consequences on the sustainability of their retirement funds.

Financial advisers must be attuned to this behavioural bias, employing strategies that balance risk and reward while helping retirees navigate the emotional challenges associated with market volatility. A range of behavioural studies have illustrated traits and biases that can impede your clients from making reasonable decisions about their retirement savings.

These biases might stem from others’ experiences, the fear of outliving their savings or the fear of losing capital. Research from Investment Trends, although a year old, identified three retirement fears (figure five) that remain pertinent in the current environment.

While loss aversion is a major factor influencing investor behaviour, particularly in retirement when it’s difficult to recoup losses, understanding other biases and fears that may negatively impact your clients’ decision making is essential to retirement planning.

Given the prevalence of these risks it’s no surprise that funding post-work lifestyles is a cause of stress for Australians close to retirement. Health authorities note that worries relating to money are a leading source of stress in Australia and can lead to depression and anxiety[8], compounding the health issues many retirees face as they age.

The interconnected nature of retirement risks underscores the complexity faced by retirees, and advisers, in safeguarding their financial wellbeing. At the centre of this is sequencing risk where the timing of market fluctuations can significantly impact the sustainability of a retiree’s portfolio.

Amid this delicate dance of risk, inflation emerges as a pervasive catalyst, influencing both market dynamics and retiree behaviour. The erosive effects of inflation on purchasing power not only pose a threat to financial security but can also amplify longevity risk, as retirees may need to fund an extended retirement period.

Furthermore, the insidious nature of inflation can shape retiree behaviour, fostering a heightened sense of loss aversion and prompting more frugal living habits as individuals seek to preserve their diminishing purchasing power.

While prudent planning and financial education can help mitigate some of these risks, it’s crucial to acknowledge that external factors, such as sequencing risk, market fluctuations and inflation rates remain largely beyond an individual’s control, necessitating a thoughtful and adaptable approach to retirement planning.

——–