Ready for a reset: Fidelity International’s 2024 analyst survey

The past two years have been marked by a fear of how bad the first sustained economic slowdown since 2008 might become. Yet, according to Fidelity International’s (“Fidelity”) annual Analyst Survey[1], conditions are settling into place for companies to look towards expansion, with Japan looking set to become the world’s economic bright spot in 2024.

Fidelity analysts have more than 20,000 company meetings every year. Put another way, on any working day one of its analysts is speaking to a company’s management every 10 minutes. Each year, the company surveys its analysts globally, probing their knowledge of the companies and sectors they cover. Taken together, the responses paint a vivid picture of how different regions and sectors will fare in the year ahead – and beyond.

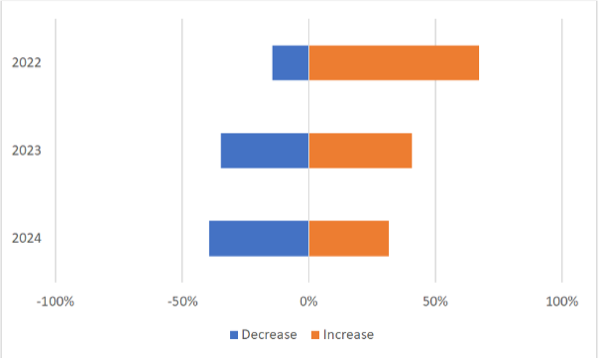

For the first time since the pandemic, more of Fidelity’s analysts think companies’ cost inflation will fall rather than rise in the year ahead. “According to our North American analysts, no one talks about inflation anymore. Labour wages were the last sticky aspect, but these seem to be normalising quickly as well,” said Gita Bal, Global Head of Fixed Income Research, Fidelity International.

Chart 1: For the first time since the pandemic more Fidelity analysts think companies’ cost inflation will fall rather than rise in the year ahead

Chart shows responses to the question: ‘How, if at all, do you expect inflationary pressures within your companies’ cost bases to change over the next 12 months?’ Analysts who responded ‘No change’ are not shown on the chart. Source: Fidelity International, January 2024.

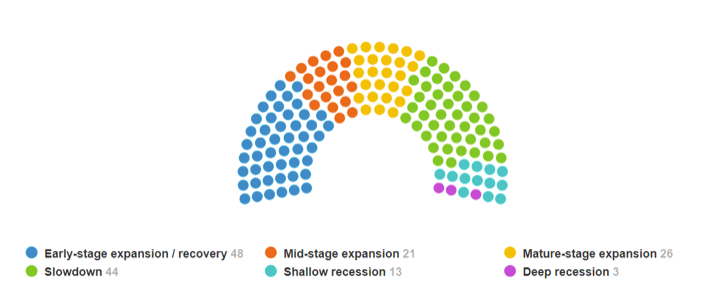

For most sectors, the analysts who cover them expect that they will show improvement this year, with the proportion who say their sector is in expansion mode rising from 52 per cent right now to 61 per cent who expect that to be the case in 12 months’ time.

Chart 2: Stage of the cycle in your sector in 12 months?

Chart shows responses to the question: “What stage of the cycle will your sector be in 12 months from now?” Chart shows percentage of analysts. Source: Fidelity International, January 2024. The survey was conducted in December 2023.

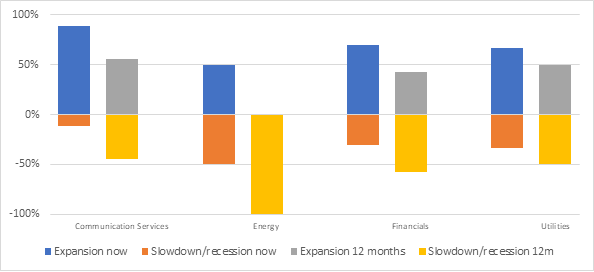

There are, however, a handful of sectors where responses suggest conditions may prove tougher as the year goes on. Analysts that cover North American and European oil and gas firms cite lower commodity prices as a headwind for the energy sector. The financial sector will also see the flip side of the retreat in interest rates.

Chart 3: Stages of the cycle – under threat

Chart shows responses to the questions: “What stage of the cycle is your sector currently in?” and “What stage of the cycle will your sector be in 12 months from now?” Chart shows percentage of analysts. Source: Fidelity International, January 2024

Gita Bal adds “A year of elections around the globe adds to existing geopolitical concerns. Yet, meetings with management teams have been surprisingly positive on the 2024 outlook, despite immediate risks on the horizon. That said, energy and financial sectors have scored lower according to our analysts. Lower commodity prices and the prospect of falling interest rates are clearly impacting overall sentiment here.”

Optimism balloons from Japan’s reflating economy

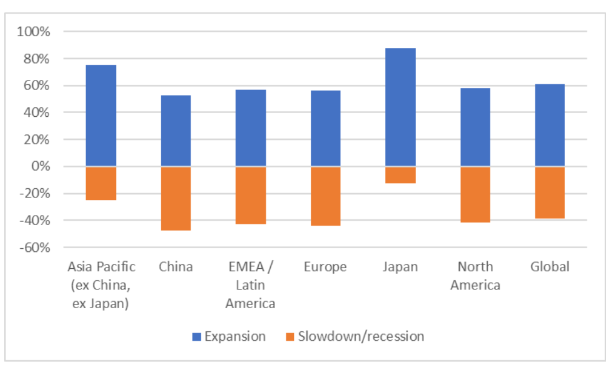

Japan is looking set to become the world’s economic bright spot in 2024. Expectations for revenue and earnings growth in 2024 are higher for Japan than for any other region. Analysts covering Japan are also the most optimistic about widening earnings margins.

Japan leads the pack when it comes to expectations for capital expenditure, returns on capital, dividend increases, ability to pass on costs to consumers, and whether or not its companies will be in an expansionary phase of the business cycle by this time next year.

Chart 4: 88 per cent of Japan analysts expect their sectors to be in expansion in 12 months’ time.

Chart shows percentage of analyst responses to the question: “What stage of the cycle will your sector be in 12 months’ time?” Source: Fidelity International, January 2024.

Chart shows percentage of analyst responses to the question: “What stage of the cycle will your sector be in 12 months’ time?” Source: Fidelity International, January 2024.

The optimism contrasts with a higher level of caution in our previous annual survey conducted towards the end of 2022. For example, nearly a third of Japan analysts then said that the company CEOs they covered were expecting no earnings growth in 2023, the most pessimistic among all regions except EMEA/Latin America. The current survey has found all Japan analysts saying that CEOs expect earnings to grow.

Gita Bal comments: “There is a straightforward reason for much of this optimism. The Japanese economy has finally emerged from more than two decades of recessions and stagnation, with encouraging signs of broad-based price increases. While inflation has been a big headache for much of the world over the last few years, it’s a good problem to have in Japan right now.”

Grey Swans?

There is a huge number of elections this year with more people being asked to cast a vote in 2024 than in any other previous year in history, creating the risk of disruption. However, one of the survey’s most striking findings is that most analysts (65 per cent) say their companies are not talking about elections at all.

Of those that are, there is division among companies when it comes to talking about election risks. Much boils down to particular scenarios in specific sectors. Only 28 per cent of all Fidelity analysts surveyed say the current geopolitical backdrop is encroaching on investment plans – the smallest proportion of analysts to say this since we started asking this question in 2017.

Chart 5: How will geopolitics affect strategic investment plans of the companies you cover?

Chart shows responses to the question: “To what extent is the geopolitical backdrop having an impact on the strategic investment plans (capex and M&A) of the companies that you cover?” Chart shows percentage of analysts who say impact will be positive or negative. Analysts who responded “No impact” are not shown on the chart. Source: Fidelity International 2024.

Chart shows responses to the question: “To what extent is the geopolitical backdrop having an impact on the strategic investment plans (capex and M&A) of the companies that you cover?” Chart shows percentage of analysts who say impact will be positive or negative. Analysts who responded “No impact” are not shown on the chart. Source: Fidelity International 2024.

Looking ahead, Gita Bal, added: “The end of the era of zero rates was always going to bring tensions. We are already in a period where companies tighten belts, demand comes under more pressure, and pricing power declines. Yet this year’s survey offers clear signs that, however the slowdown plays out, for most companies the system will reset and the next phase will lift them up rather than cast them down.”

——–