Investing targeting four key equity factors delivers long-term outperformance

Dan Miles

An equity portfolio built with shares displaying value, momentum, low volatility and quality characteristics will likely outperform a traditional portfolio tracking a market-capitalisation weighted index over the long term, according to new analysis from Innova Asset Management.

While equity portfolios offer significant returns over the long term, they also come with substantial risks given the inherent volatility in share markets. These can be mitigated by targeting equity factors or characteristics that can boost returns over time, according to Dan Miles, Innova Managing Director and Co-Chief Investment Officer and co-author of the research paper, Better Equity Investing[1].

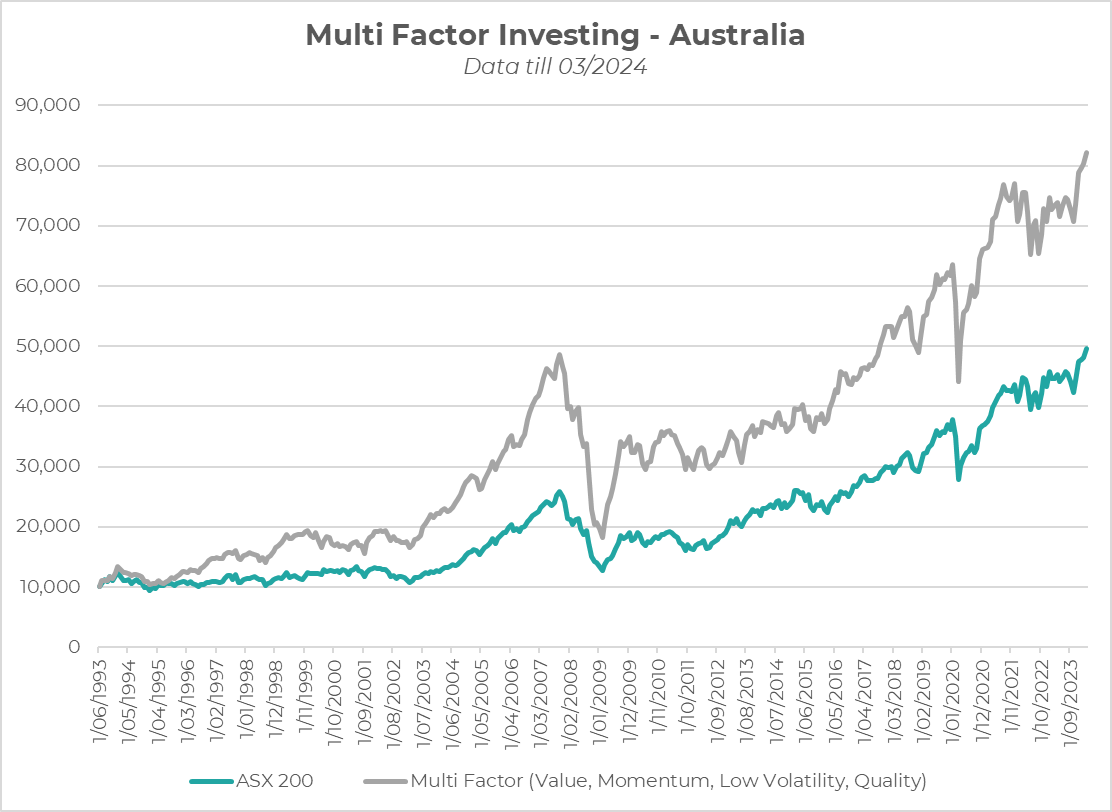

“Our research has found that an equity portfolio built using the four factors of momentum, quality, value and low volatility and invested in either the Australian or Global share market delivered significantly higher returns between 1982 and 2023 compared to the share market benchmarks in both markets,” Mr Miles said. The graphs below highlight this outperformance.

The graphs below highlight this outperformance, of 1.74% p.a. for an Australian multifactor portfolio and 1.57% p.a for a global multifactor. Different factors drive equity returns depending on financial or economic fundamentals. Value stocks have low prices relative to their financial fundamentals such as earnings. Momentum refers to investing in companies with strong price trends where strong past returns are associated with strong future short-term returns.

Source: Bloomberg and Innova, as at 31/03/2024

Source: Bloomberg and Innova, as at 31/31/03/2024

Quality involves investing in companies that exhibit stable earnings, low leverage and high profitability while companies with low volatility typically enjoy defensive earnings and more stable share prices.

“These factors are now available to investors through low-cost exchange-traded funds (ETFs), which can have management fees as low as 0.25 per cent,” Mr Miles said. “The US market is the most advanced in the world, where ETFs represent 12.7 per cent of all US equity assets[2] compared to 4.4 per cent across the Asia-Pacific. US-focused ETFs can cover value, momentum, low volatility and quality factors, as well as many others. While the Australian market is not quite as advanced, there are still ETFs for many factors available. Investors can still create Australian equity multi-factor portfolios using a combination of ETFs and other investment structures, such as managed funds; while there may not yet be a momentum or value Australian equity ETF, there are still momentum and value managers offering factor-based investment options,” Mr Miles said.

While a multi-factor can reasonably be expected to deliver a higher return over time, the approach may require fine tuning as different factors perform differently over the economic cycle. “Innova takes an active approach to portfolio construction, rotating into and out of these factors as market conditions change. This approach increases the chances of delivering higher returns while managing the extra volatility and size of drawdowns associated with equities,” Mr Miles said.

———-