Positive outlook for emerging markets as domestic growth looks to outpace US

John Moorhead

Several factors point to a stronger year ahead for emerging markets, where select country share market gains could outpace those in the US and other developed nations, says John Moorhead, head of global emerging markets at Maple-Brown Abbott.

These include a likely peak in interest rates, lower inflation and attractive equity valuations, which could see investor capital flow to emerging markets.

Mr Moorhead believes emerging markets are at a turning point after hitting a 35 year low relative to the US share market.

“The last decade was relatively challenging for any market outside the US; the next decade is likely to be better for emerging markets, a number of which are showing higher growth and higher real interest rates than developed nations, suggesting a turn in the cycle could come soon.

“Select emerging markets are well ahead of developed markets in raising interest rates and they are also ahead of the curve in fighting inflation. We think we’ll see capital flows pick up in key markets, which will likely strengthen their currencies and help to lower inflation further. We could potentially then see more rate cuts in emerging markets, which would support local economies, corporate earnings growth and share markets,” he said.

The strength in Latin America and Eastern Europe stands out, where Maple-Brown Abbott believe share markets have some of the greatest potential.

“For instance, while China may appear cheap at 9-times price-to-earnings (P/E), other markets such as Greece trade on less than 5-times price-to-earnings (P/E). More important than valuation alone is the direction of change. Corporate earnings in China continue to disappoint in aggregate. While we are finding some opportunities in China where valuations are cheap and company fundamentals are strong, the overall negative changes leave us cautious on China at a country level.

“Greece, on the other hand, is undergoing a renaissance in terms of its economy and corporate earnings and therefore has one of the highest positive change scores across the universe,” he said.

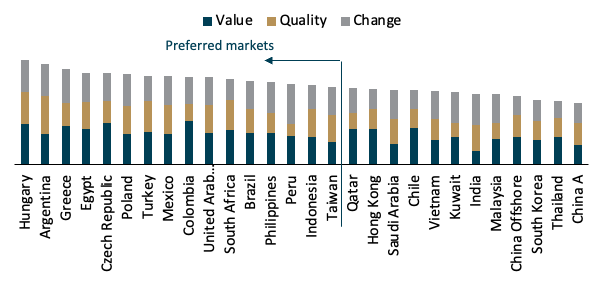

The chart below shows Maple-Brown Abbott’s preferred emerging market opportunities at the country level based on three distinct criteria: value, quality and change.

Source: Maple-Brown Abbott, April 2024.

Mr Moorhead says while India has generated a lot of attention in the past year, and its corporate and economic fundamentals are strong, this is more than offset by very high share market valuations. Bloomberg consensus data has India’s share market on 23-times next year’s earnings, compared to about 12 times for the broader MSCI emerging markets.

More recently, the Chinese equity market has been supported by a quarterly earnings season that saw an increase in the number of corporates announcing shareholder-friendly capital management policies. Outside Asia, Turkey was a standout market with a 14% gain (USD terms). The market strength was supported by foreign investor inflows as investors are positive on the Government’s pledge to maintain orthodox economic policy.

Mr Moorhead pointed out that emerging markets are idiosyncratic and encompass higher investment risk, so experience, active management and bottom-up research count.

“We can invest across a universe of 3,000 listed companies within a 24 country cohort, with each of those countries going through their own phase of economic development and shorter-term economic cycles. We apply a bottom-up approach and look at individual businesses and industries based on our three key metrics of value, quality and change.

“Focusing on the impact of cyclical and structural change on companies, we use a rigorous and repeatable process to construct a concentrated portfolio which captures the opportunities offered by the dynamic nature of emerging markets,” he said.