Maple-Brown Abbott sees strong investment opportunities for US listed utilities powering data center growth

Georgia Hall

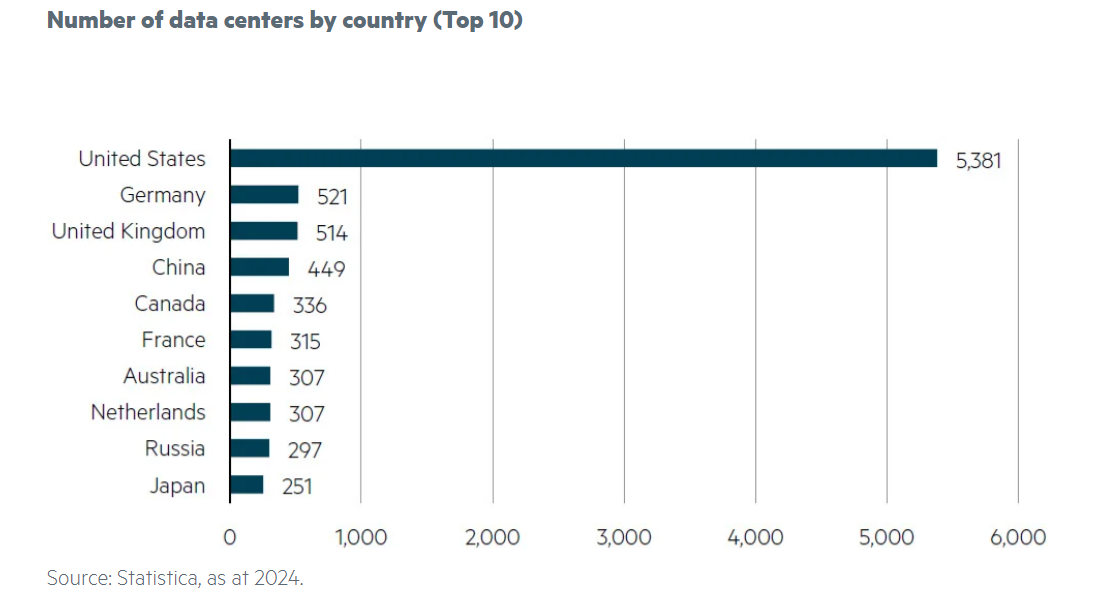

The exponential growth of data centers raises critical questions about electricity sourcing and the infrastructure investment needed to support digitalisation and decarbonisation. According to Maple-Brown Abbott, insatiable demand for data centers is creating attractive investment opportunities in the US power sector where one third of the world’s data centers are situated.

“We are positive on the US electric utilities sector because of compelling valuations coupled with emerging opportunities around data center growth, digitalisation and decarbonisation” says Georgia Hall, ESG Analyst, Global Listed Infrastructure at Maple-Brown Abbott.

“Data centers form the backbone of the digitalised world, supporting various services from cloud computing to e-commerce and artificial intelligence – but they are voracious consumers of electricity. According to the Electricity 2024 report by IEA, estimates suggest global power demand from data centers could surpass 1,000 terrawatts per hour (TWhs) by 2026 – roughly the equivalent of Japan’s entire electricity consumption. While data centers are driving electricity consumption to unprecedented levels, we also believe their growth is helping to accelerate energy transition infrastructure investments.

“Data center growth presents a major opportunity for regulated electric utilities to expand their customer base and revenue streams while spreading the energy transition costs across more consumers. This is especially true in the US, where landmark policy incentives such as the Inflation Reduction Act are turbocharging investments in renewables and grid infrastructure.

“We believe underappreciated structural growth tailwinds will persist for decades to come but are not yet reflected in the market prices for these assets. Our current allocation of 37 per cent to US electric and multi-utilities in the Maple-Brown Abbott Global Listed Infrastructure strategy reflects our conviction in the sector,” Ms Hall said.

‘Hyperscalers’ such as Amazon, Apple, Alphabet, Meta and Microsoft all have zero carbon or 100 per cent renewable commitments and rely heavily on data centers as part of their core business. According to research by S&P Global Market Intelligence, these five companies alone account for over 45GW of corporate renewable purchases worldwide – more than half of the global corporate renewables market.

“Grid capacity is critical not only for the decarbonisation of the transport, industrial and residential sectors – but also for data center interconnection. Integrating large quantities of variable solar and wind generation, whose peak output may not match moments of peak demand, requires significant investment and the sophisticated management of electrical grids. Hence, the timing of grid investment has never been more important.

The long lead time of grid planning versus the shorter timeframe to plan and build data centers creates a potential shortfall of capacity, thereby placing pressure on utilities and regulators to accelerate investments.” Ms Hall said.

The recent energy crisis in Europe and the ongoing need for zero carbon baseload power to complement renewables has re-ignited the debate around nuclear power, especially in the context of data centers.

“It is reasonable to assume that greenfield large and smaller-scale nuclear power plants are unlikely to solve the near-term need for load growth. However, existing nuclear fleets with spare capacity have potential to assist hyperscalers with their electricity and zero carbon needs.

“That said, not all nuclear plants have this optionality. Nuclear power could solve for some, but not all, data centers’ electricity needs. Therefore, more creative solutions are needed for pairing renewables with baseload and/or energy storage technologies, where viable. Much of this comes down to technology and project development timelines, having the right policy incentives and ensuring bill affordability,” she said.