An allocation to private equity can provide valuable diversification benefits to investor portfolios.

Private equity (PE) refers to the ownership or interest in a corporate entity that is typically not publicly listed or traded. PE managers usually raise capital from high-net-worth individuals or institutions to create PE funds, which they then use to invest in private companies or to acquire public companies, often taking them private. The goal is to implement long-term value creation strategies.

Private equity vehicles can be either listed or unlisted. Listed Private Equity (LPE) includes publicly traded entities that primarily invest in private companies, private equity funds, or the managers of these funds.

Incorporating PE and LPE into an investment portfolio can offer diversification benefits, and many successful global investors have significant allocations to private equity (figure one). Consequently, there’s been significant growth in this sector. Private markets assets under management totalled $13.1 trillion as of 30 June 2023 and have grown nearly 20 percent per annum since 2018. Dry powder reserves—the amount of capital committed but not yet deployed—increased to $3.7 trillion in 2023, marking the ninth consecutive year of growth[1].

Further, the PE market is expected to expand at a compound annual growth rate (CAGR) of 9.72 percent from 2024 to 2033, bolstered by the rising start-up culture[2].

Both PE and LPE give investors access to a broader investment universe, including companies in the earlier stages of growth that are not listed on public stock exchanges. This is increasingly important as more companies choose to “stay private for longer,” prompting investors to consider how they can tap into these growth opportunities.

Private equity explained

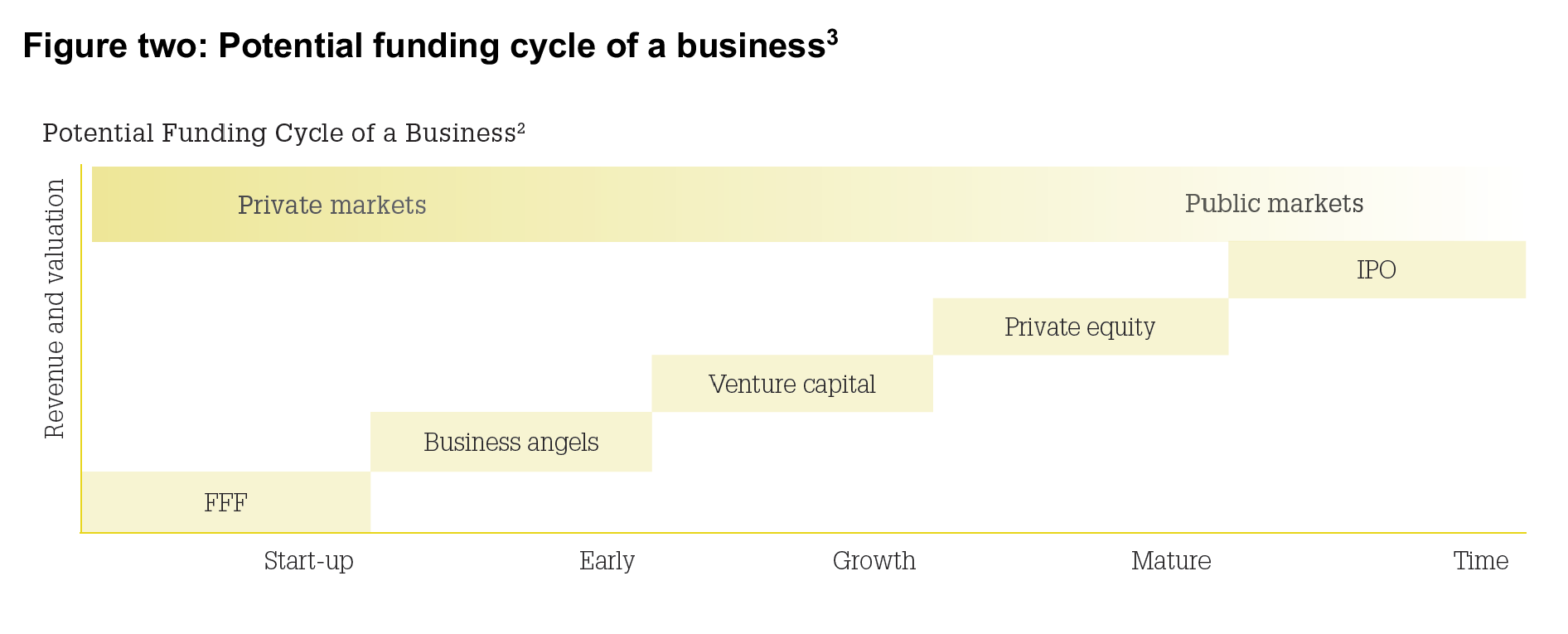

Every company begins as an idea. While some ideas falter, others grow into organisations that generate billions in revenue. Throughout a company’s lifecycle, there will inevitably be moments when it needs access to capital, and there are specific types of investors suited to support each stage of growth (figure two).

Private equity (PE) represents one of these funding stages, available to certain types of businesses, not just private companies. In fact, public companies are increasingly receiving significant PE backing.

PE is traditionally associated with investment funds that acquire and restructure non-publicly traded companies, often viewed as a distinct asset class involving both equity securities and debt. However, as the market has evolved, the term has also come to describe the practice of taking a company into private ownership to restructure it before selling it again for a potential profit.

PE investments are typically made by PE firms, venture capital firms or angel investors. Each of these investment stages comes with its own set of goals, preferences and strategies, but they all provide working capital to help a company expand, develop new products or restructure its operations, management or ownership.

Importantly, PE is not just about providing funding; it’s about transforming an average company into a better one and unlocking greater value for both the business owners and the investors.

This century, private equity it has grown by eight times – twice as fast as public market capitalisation. As a result private markets have graduated from the fringes of the global economy to the mainstream<[4]. A confluence of factors have combined to create strong tailwinds for the PE industry and the attraction of PE as a standalone asset class for investors. These factors include:

- Trends in private markets growth

- Market factors, such as elevated valuations in equity markets and lacklustre fixed income markets

- The performance characteristics of PE

- Growth in PE assets under management

- Diversification benefits.

Performance characteristics of private equity

The hunt for yield in a sustained low interest rate environment fuelled investor appetite for return seeking – with PE and private debt seemingly filling that void. Despite increased rates, they remain historically low and an easing cycle looms on the horizon. Inflation has eroded returns, notably those derived from cash and cash like investments.

What is it about the PE model that has enabled it to generate strong returns on invested capital over long periods? A private company’s partnership with a PE-backer can be considered to be a ‘relationship’. There is a genuine alignment between the PE-backed company and the PE owners/management, which creates strong governance. PE managers tend to have representation on the board, remain in very close communication with the management team and operate a remuneration model far more aligned to value creation.

Good PE firms that can affect significant transformational change on underlying companies are capable of generating attractive multiples on invested capital. The attractive nature of the return potential from PE has been a significant driver of the growing investor demand and inflows into this alternative asset class.

Diversification benefits

PE has diversification benefits when used as part of a broader investment strategy. It does so by providing investors with exposure to an investment universe that sits outside of the types of businesses that underlay the traditional asset class options – for example, companies in the earlier stages of their growth lifecycle and private companies not listed on public stock exchanges.

There are also sectors and regions where PE is able to provide better access relative to listed equity markets– for example, industries such as consumer facing businesses, healthcare and information technology.

Private market investing does have its challenges, particular for individual investors. Direct investment into private companies and traditional private equity funds require:

- Large capital outlays

- Long lockup periods

- Investors to take a concentrated, illiquid exposure to a small number of private companies, many of which are often leveraged.

PE management fees can sometimes be significant.

Access to PE investing has evolved over many years, particularly as a great number and range of investors develop interest in this asset class. This evolution is exemplified by the notable growth in the Listed Private Equity (LPE) universe. Publicly traded entities that invest in privately held businesses, and PE-backed listed companies, are an attractive gateway for broader investors to access the diversification and risk/reward characteristics of PE. They are liquid, regulated, diversified, and easily investable[5].

Because many investors do not have the capacity to own illiquid, long term PE investments, or the capital required to meet the minimum investment levels to gain exposure, LPE can provide an accessible entry point to this investment opportunity.

Listed private equity

Blackstone Group (BX), Apollo Global Management LLC (APO), Carlyle Group (CG) and Kohlberg Kravis Roberts/KKR & Co. (KKR) are some of the larger global PE firms. Many are referred to as alternative asset managers because they have diversified beyond PE, to invest in other alternative assets such hedge funds, real assets such as property and infrastructure, and private debt/credit.

At the same time, many PE managers have become more specialised, with firms often focusing on specific industries, sectors or aspects of the businesses lifecycle. Often the PE firm brings with them a broad range of skills, resourcing and capabilities that company management can draw upon, such as:

- Knowledge of specific industries

- Operational experience

- Financial modelling and analytical skill

- Customer, competition and market research

Each of these specialist skills can be leveraged to benefit the strategy and direction of the company the PE manager is backing.

What is listed private equity?

There are more than 200 Listed Private Equity (LPE) entities and over 500 PE-backed listed companies worldwide. Almost a third of these companies are domiciled in the UK, while Europe and the US account for the remainder. There are a small number in the Asia Pacific region.

The sector includes listed entities that specialise in some, or all, stages of PE investing, including:

- buyouts, including leveraged and management buyouts

- expansion or growth capital

- venture capital

- distressed or special situations

- mezzanine capital

- secondary investments

- fund of funds, and

- private debt.

Typically a company will specialise in one of these investment strategies and will often limit their focus to certain geographic regions. More recently, PE and Alternative Asset Managers have listed their firms on public stock exchanges; this enables a broader range of investors to own their shares and benefit from the economics of managing alternative assets, including PE and LPE.

A diversified exposure to private markets

Traditionally only the largest institutional investors have had the resources to build out a diversified portfolio of PE funds, and even then it can take years to achieve. Conversely, investments in LPE tend to be globally diversified across funds, strategies and vintages. A portfolio of LPE securities, however, can provide an instant portfolio of private equity interests – diversified by geography, deal stage, vintage year and manager[6].

LPE diversifies across a number of areas including:

- Vintage exposure

- Sector exposure

- Geographic exposure

Vintage exposure

Vintage exposure refers to the year in which a fund began making investments or, more specifically, the date in which capital was deployed to a particular company or project. Unlike investments in traditional asset classes, the commitment to a PE fund is gradually drawn over the investment period (anywhere between three and five years) and does not require an upfront investment of the entire amount[8]).

What is significant about vintage exposure is that investments in unlisted PE funds can experience what is known as the ‘J-Curve’ effect (figure three). This refers to a phenomenon whereby an initial investment in a PE fund stagnates for two to three years before (in an ideal scenario) appreciating. It can take time for general partners to deploy capital and for investments to pay off. Meanwhile, management fees eat into the principal.

A LPE fund, on the other hand, can reduce this effect because the underlying portfolio will typically comprise a range of existing investments that are at differing stages of maturity (similar to a secondary transaction).

Sector exposure

Sector exposure

Sector exposure refers to different types of LPE investments. Often the various sectors are in different parts of the private equity cycle, which reinforces the benefits of being able to selectively diversify in these areas.

Sector examples include:

Buyouts / venture capital / growth capital: A buyout refers to an investment transaction where one party (e.g. a PE firm) acquires control of a company, either through an outright purchase or by obtaining a controlling equity interest. The buyout can be funded through debt or equity financing – usually a structured combination of both.

The transaction often takes place in situations where the purchaser considers a firm to be undervalued or underperforming, and has the potential for improvement operationally and financially under new ownership and control. Like any other investment, a buyout will take place when the acquiring party believes that there is an opportunity of making a good return on their investment.

Some companies specifically focus on readying the organisation to be buyout target, whether by a PE firm or a competitor. For other companies it may be the unintended consequences of poor management, or an unforeseen opportunity that arises. The source of return is generated mainly from earnings growth from the underlying portfolio companies, which leads to NAV growth.

PE-backed listed companies: A PE-backed listed company is one where a PE manager holds significant equity ownership, or controlling stake, of a listed public company’s shares. The PE manager would typically have representation on that company’s board.

Alternative asset managers: An asset manager that manages alternative assets, which might include PE, venture capital, real assets (e.g. property and infrastructure), hedge funds, commodities, derivatives or private debt. Its source of return is generated mainly from management fees and performance fees, however it may also hold a balance sheet of investments on which returns are generated.

Private debt: Private debt is a transaction where a lending source directly provides a loan to the borrower without the use of an intermediary. This is facilitated by the lender working directly with the PE sponsor or owner/operator of a middle market company, commercial project or commercial real estate. Its source of return is generated mainly from loan interest.

Geographic exposure

Geographic exposure refers to the underlying countries where the investments are domiciled. LPE comprises entities listed on international stock exchanges whose main activity is investing in private companies or PE funds.

The investment case for listed private equity

An LPE is a publicly traded vehicles that is liquid, regulated, diversified and easily investable. Importantly, LPEs can help investors avoid post-commitment declines that are typical of PE investments and provide access to the asset class for both retail investors and institutions”[8].

Access to private equity, and the investable ecosystem of private market opportunities, continues to evolve and increasingly, listed PE funds are available to investors. This creates a system where the PE firm has access to permanent capital to fund its investment activities, and one that provides investors with greater flexibility because of the liquidity that comes with a listed vehicle. LPE has made PE more accessible to a broader range of investors.

The PE model provides a superior governance and ownership model, one that enables PE managers to take a genuine and strategic long-term view to execute on value creation and maximise returns on capital for PE fund and LPE investors.

There is also evidence to support that:

- PE outperforms public markets over the medium term[9]

- LPE net asset values (NAVs) perform similarly to traditional PE[10][11]

- Investor returns are ultimately driven by NAV growth

- Inefficiencies in the LPE market arise from information asymmetry, lack of broker research coverage and a lack of attention from institutional investors.

LPE has diversification benefits when used as part of a broader investment strategy. It does so by providing investors with exposure to an investment universe that sits outside of the types of businesses that underlay the traditional asset class options. Investors get immediate exposure to a diversified portfolio of companies that are at varied stages of operational improvement, which better distributes the return to investors through time.

There are also sectors and regions where PE is able to provide better access relative to listed equity markets – for example, industries such as consumer facing businesses, healthcare and information technology.

PE has demonstrated an attractive return profile over many years, relative to public equity returns. As an inefficient market, there is good potential for manager skill to generate alpha from the active management of this universe.

LPE provides investors with the potential to capture the private equity return premium over time but with genuine daily liquidity. LPE does carry more market-like volatility given the daily priced nature of its listed investible universe.

How can investors access LPE?

Strategies in private assets, especially LPE, can present good opportunities for investors who are keen to seek greater diversification and greater potential sources of return in their investment portfolio.

While the LPE universe continues to grow and evolve, it’s important to acknowledge that these entities are not well covered by the broader research community. There are only a few specialist PE-focused firms and global asset managers who have identified this investment opportunity and spend the time and resources to (a) mine the market in an attempt to identify these companies and (b) undertake in-depth coverage and research to identify these opportunities.

Investors have an increasing number of options available to them. They can:

- Invest directly in an individual LPE

- Invest in an ETF that mimics an LPE focused index such as the LPX50, which represents the global performance of the 50 most highly capitalised and liquid LPE companies

- Invest in an actively managed fund that invests in LPE opportunities.

In the latter category, it’s important to focus on managers that are research driven in their pursuit of LPE investment opportunities and actively managed to deliver maximise the alpha delivered.